GST (Goods and services tax) is a major tax reform implemented in India on 1st July 2017 across all the states. The new tax scheme has subsumed around 17 indirect taxes of both central and state levels. It is said that the goods and services tax will end the currently prevailing cascading effects of taxation which was one of the main reasons for unnecessary inflation.

The GST is a dual structure tax scheme that will be applicable in the terms of central and state wise. The purpose is to keep both state and central monetary independent. Also, the GST will make a unified market eliminating all the variable taxation in the country. The goods and service tax will be managed and the decisions will be announced by the dedicated GST Council which is also the apex authority to make decisions regarding all the matters of GST.

Latest Update in B2B & B2C

12th January 2021

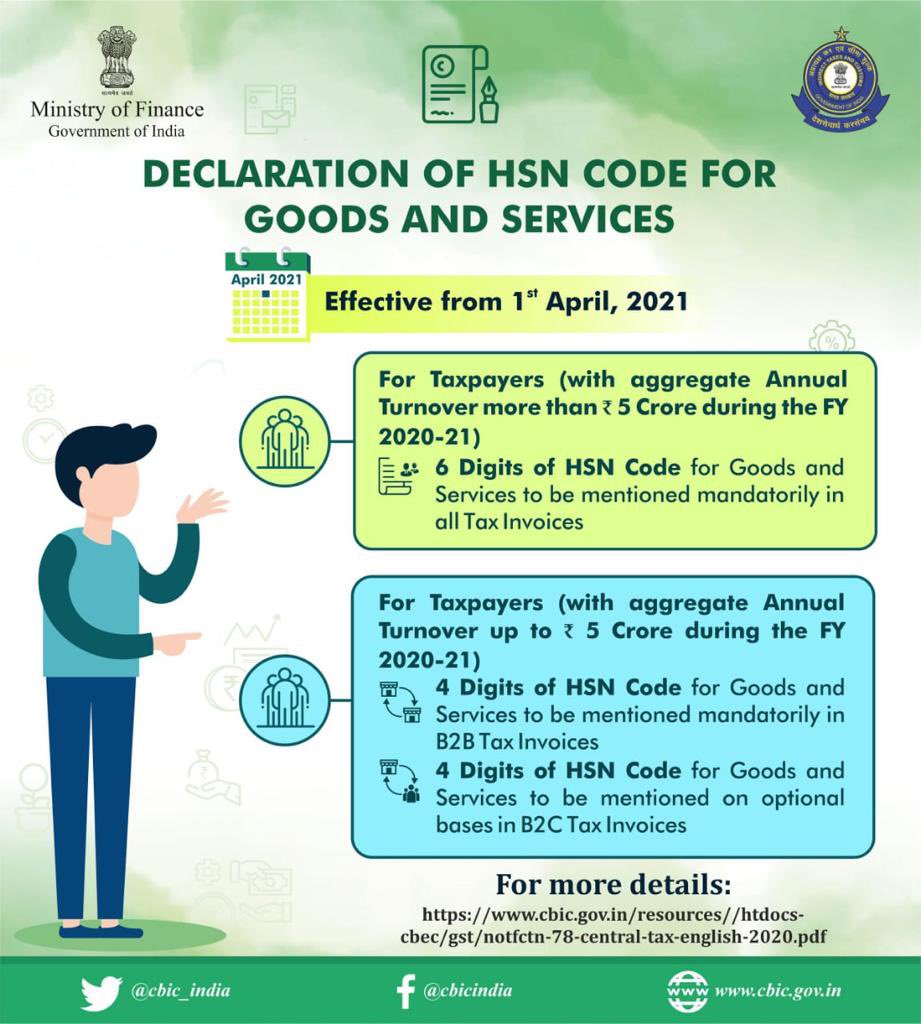

- “Statement of GST HSN (Harmonized System of Nomenclature) code starting from 1 April 2021 for B2B and B2C supplies according to the turnover.” Read more

5th October 2020

- “For taxpayers with aggregate turnover of more than Rs. 5 Crores, HSN code to be mentioned at 6-digit level and for those with aggregate turnover of less than Rs. 5 Crores making B2B supplies, HSN code to be mentioned at 4-digit level”. Read more

The GST is Divided Further into Three Categories:

- Central Goods and services tax (CGST) – Central GST is a central tax duty that will be applicable on every transaction and will be collected by the central government.

- State Goods and services tax (SGST) – SGST duty will be collected by the state government on all intra-state transactions.

- Integrated Goods and services tax (IGST) – The integrated GST will be levied and collected by the taxpayers which will be further divided on a pre-decided rate between the state and the center.

Read Also: Complete Details on SGST, IGST, CGST with Input Tax Credit Adjustment

What According to GST is a Taxable Entity?

- Any organization whose turnover exceeds the INR 20 lakh threshold limit in a year (10 Lakh for the North Eastern States). If a supplier is doing supply of goods the threshold has been increased to INR 40 lakhs so it is clear that any person whose turnover is not above 40 lakhs in a financial year is not eligible or to say not necessary to take the GST registration. Also if he has not done inter-state supply and is not a nonresident taxable individual. This all has been clearly notified by Notification No. 10/2019 – Central Tax dated March 7, 2019, levied from April 1, 2019

- Any individual selling through an e-commerce operator.

- E-commerce firm itself

Select the GST Category for Which You want to Find the Solution

- For Consumers

- For Business to Business (Manufacturer and Wholesaler)

- For Business to Consumer (Retailer)

GST Solution for a Consumer

A consumer is the first person in a row to get affected by the newly implemented goods and services tax. As a destination-based tax scheme, the ultimate tax weight will be borne by the consumer itself which means, all the value chain individuals i.e. dealers, traders, and wholesalers will be only passing the tax towards an upcoming purchase with no value addition.

The goods and services tax will then also require certain awareness from the consumers as in various cases, the traders with no GST background charge CGST and SGST on their own.

Some of the important aspects of a Consumer after GST:

A Consumer must be aware of the basic step which has to be taken while having a deal with the trader. It is very much needed to check a trader is registered or not with the GST. It will validate the taxes charged by him and will ensure that the taxes paid by the Consumer must go into decided pockets.

It is also to be noted that the recent government announced that a service charge applied by certain restaurants is completely illegal and it is only upon the customer to pay it or not. So, a common man should also be aware of his rights and can say no to extra charges.

GST Solution for B2B (Manufacturer and Wholesaler )

Goods and service tax in the business-to-business scenario has created a lot of issues in the recent time period. Many of the industries and sectors were affected on a large scale and the production was hit badly upon the arrival of GST.

The GST Council and the government equally tried to increase the compliance upon the loose operating industries in order to get them in line with the latest market trends. Numerous strategies were taken on account of the implementation of GST with plans and policies changes for the time being.

Almost every business took some stand in front of GST and on the basis of it, there are views and articles which can be a reference from the mentioned list:

- The sellers must check out that if the purchaser is registered within the GST or not, as it will impact the overall Input tax credit of the business unit

- The reverse charge mechanism must also be ensured, in which both the parties must decide at what proportion the dealers will share the tax ratio in order to suffice the government tax quota

What is the Importance of GST Identification Number?

Each and every tax-paying entity will be assigned a unique Goods and Services Tax identification number. The assigned number will hold importance in each transaction carried out by the business unit.

So, in order to validate the transactions, the taxpayers will be allowed this unique 15 digit Goods and Services Tax identification number. And to obtain this unique identification number, the taxpaying entity must have a PAN card for the attachment. It is suggested that one should obtain the PAN card before applying for registration and if it has any mismatch in the PAN card or Aadhar card, it is said to fix these issues as soon as possible.

The GST Council also proposed a compliance rating feature based upon the tax filing habits of taxpayers. The individual taxpayers will be rated according to the previous transactions regularly to check if the individual submitted the tax file returns and with minimum or no reconciliation. The merit basis refund claim is said to be based on the rating, for example, a rating of 9 will be eligible for a 90 percent instant refund.

Goods and Services Tax for B2C (Retailers)

Goods and service tax is a complex and elongated tax scheme that is held for greater technical feasibility across the nation. The consumers of the country are well inhibited with consumerism and have a long-term relationship with the business entities providing stable goods and services to the general public on a healthy platform.

GST upon its arrival started making this platform and chain more partial and accurate with its open system of transaction. More and more compliance induced into the operation of business made a direct effect on the consumer habits in the market.

There are various effects and impacts on the overall consumer community in India which can be understood by the mentioned links.

What According to GST is a Taxable Entity?

- Every person who is registered in the previous tax regime (Excise, VAT and Service Tax) is required to register under GST

- Casual Taxable Person

- Non- Resident Taxable Person

- Those are paying taxes under the Reverse Charge Mechanism

- Input Service Distributor

- E- commerce operator or regulator

- Everyone who drives inter- state of supplies

- Agents of a supplier

- Anyone who supplies goods through e-commerce operators

- A person supplying online information database access or retrieval services outside from India to a person in India, other than a registered taxable person

- Anyone whose annual turnover above Rs 20 lakhs (Rs 10 lakhs in case of hill states and North- Eastern)

Some of the important aspects to be taken care of B2C structure:

- Whenever a dealer is making a transaction, he must take the category in which he applies that particular transaction. For example – In the case of a B2C Large transaction in which, it is mentioned that any inter state only transaction above the value of INR 2.5 lakh and above must be specifically recorded in the B2C Large and not be mistaken with any other category

- While in the same case, when a transaction having a value less than INR 2.5 lakh at the interstate level and a transaction in intrastate level with no limits, must be captured in small category i.e. B2C Small

{kind=link}

Sir,

God Afternoon,

We have applied for GST refund against Inerted Structure unutilized input tax we have to apply for gst refund now our Supdt says is not eligible for refund against clearance to B to C. Hence pl advise whether to get eligible.