Income Tax Return Filing

Filing an income tax return is a responsibility of every citizen of the country and also mandatory for each one of them. Income Tax Return is the form in which an assessee furnishes all his Income and tax details and thereon submit it to the Income Tax Department. Various ITR forms are ITR 1 Sahaj form, ITR 2, ITR 3, ITR 4, ITR 5, ITR 6 and ITR 7.

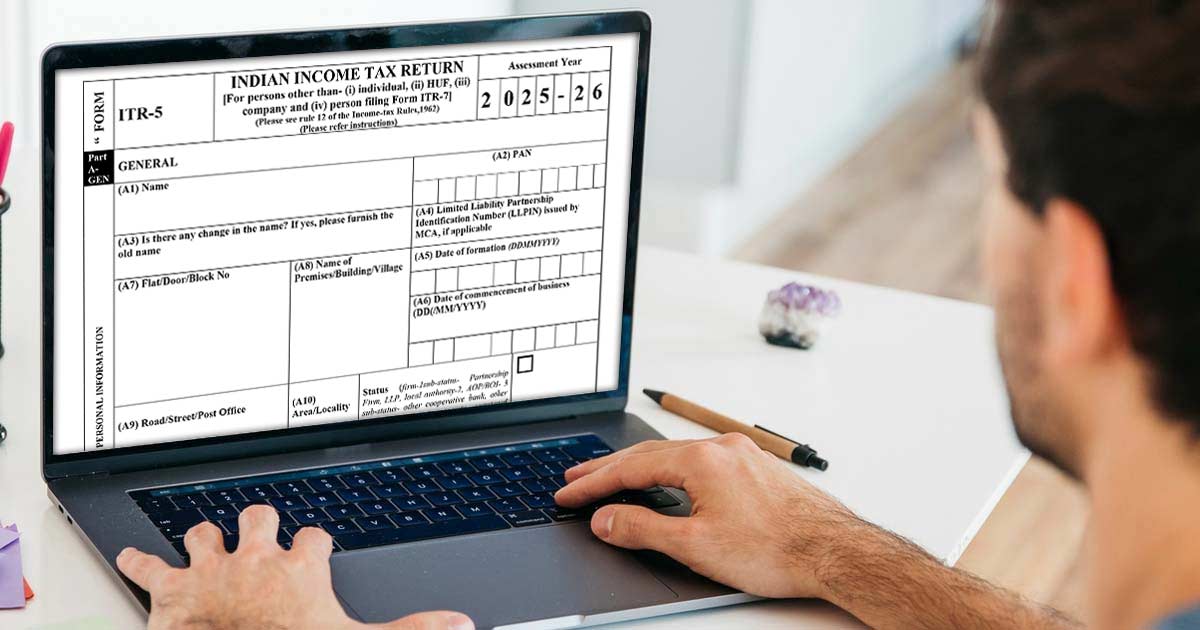

For filing the tax returns, every assessee should know and choose an appropriate ITR form, depending on his income and profession. ITR 5 Form is one of the income tax return forms that are to be used by specific parties. [For persons other than- (i) individual, (ii) HUF, (iii) company and (iv) person filing Form ITR-7]

Latest Update

- Taxpayers can now download the Excel-based utility, JSON schema, and validation utility for the ITR-5 form. Download Now

Gen IT Software Demo for Filing ITR-5

Who can File the ITR 5 Form?

ITR 5 Form can be used by Firms, Limited Liability Partnerships (LLPs), Association of Persons(AOP) and Body of Individuals (BOIS), Artificial Juridical Person, Cooperative society and Local authority, subject to the condition that they do not need to file the return of income under section 139(4A) or 139(4B) or 139(4C) or 139(4D) (i.e., Trusts, Political party, Institutions, Colleges, etc.). Individuals, HUFs (Hindu Undivided Families), and Companies are not eligible to use the ITR 5 Form.

E-Filing Audit Reports

After the AY 2013-14, it has become mandatory for an assessee to furnish a report of audit under sections 10(23C)(iv), 10(23C)(v), 10(23C)(vi), 10(23C)(via), 10A, 10AA, 12A(1)(b), 44AB, 44DA, 50B, 80-IA, 80-IB, 80-IC, 80-ID, 80JJAA, 80LA, 92E, 115JB or 115VW, electronically on or before the date of filing the return of income.

Consequences of Late Filing: Failure to file the audit report electronically by the specified deadline can result in a penalty under Section 271B (0.5% of turnover or ₹1.5 Lakh, whichever is less) and the potential disallowance of certain tax exemptions or deductions (especially for Chapter VI-A deductions like 80-IA).

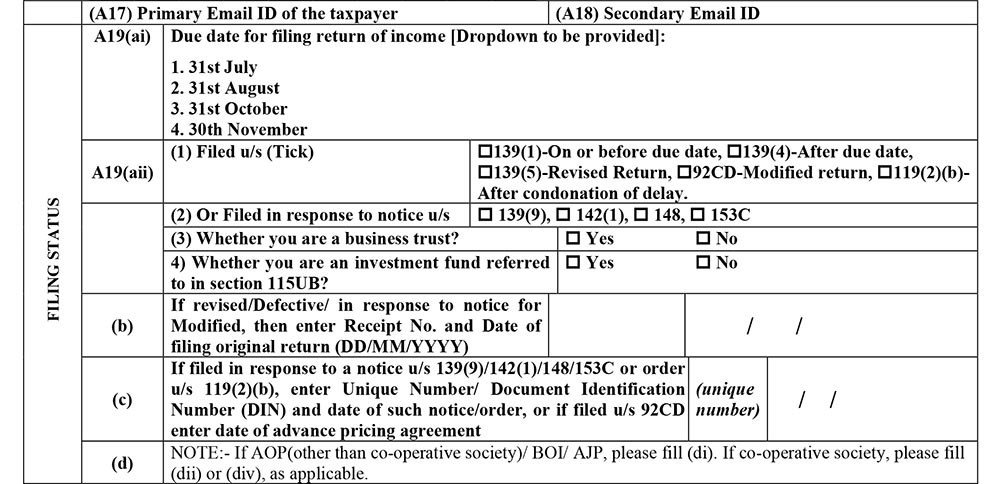

Due Date of ITR 5 Form Filing for AY 2026-27

| Annual Year | For Non-audit Cases | For Audit Cases |

|---|---|---|

| AY 2026-27 | 31st July 2026 (For Assessee not having income from Business or Profession) 31st August 2026 (for Assessee Having Income from a Business or Profession) | 31st October 2026 |

Instructions for Filing ITR 5 Form

When a schedule is not applicable, mention it as “—NA—”.

When an item is inappropriate, write “NA” against that item.

“Nil” stands for nil figures. Write Nil to denote figures of zero value.

For a negative figure or loss, write “-” before such a figure, other than provided in the form. All figures should be represented in the round-off manner to the nearest one rupee. In the same way, the figures for total income/ loss and tax payable should be rounded off to the nearest multiple of ten rupees.

How do I File My ITR 5 Form?

The ITR-5 Form can be filed with the Income Tax Department by two methods, i.e. online and offline. The form can be filed offline by furnishing through json file.

However, in the Online way, it can be filed by furnishing the return through the department’s online utility verification of ITR done by digital signature EVC or sending copy of ITR-V, duly signed by the assessee, within 30 days of filing the return to Post Bag No. 1, Electronic City Office, Bengaluru–560100 (Karnataka) via ordinary post. The other copy should be kept by the assessee with himself as a record.

Read Also: Penalty Provisions If Not File Income Tax Returns for the Current FY

Note: It is mandatory for a firm to furnish the return electronically under a digital signature, whose accounts are liable to audit under section 44AB.

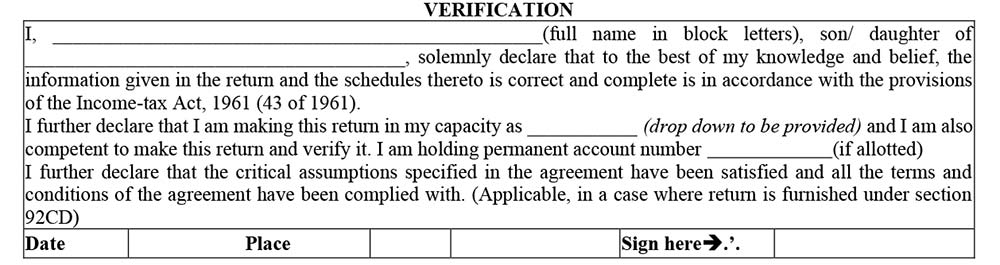

How to Fill Out the Verification Document?

Furnish all the required information in the verification document. Make sure that the verification has been duly attested before filing the return. Mention the designation of the person signing/attesting the return.

Note: Any individual making a false/wrong statement in the return or in the related schedules shall be liable to be hauled in the court under section 277 of the Income-tax Act, 1961 and shall be punishable under the section with imprisonment and fine after the court’s decision against him.

Note: ITR-5 form corrigendum via Notification No. 60/2026. Read More

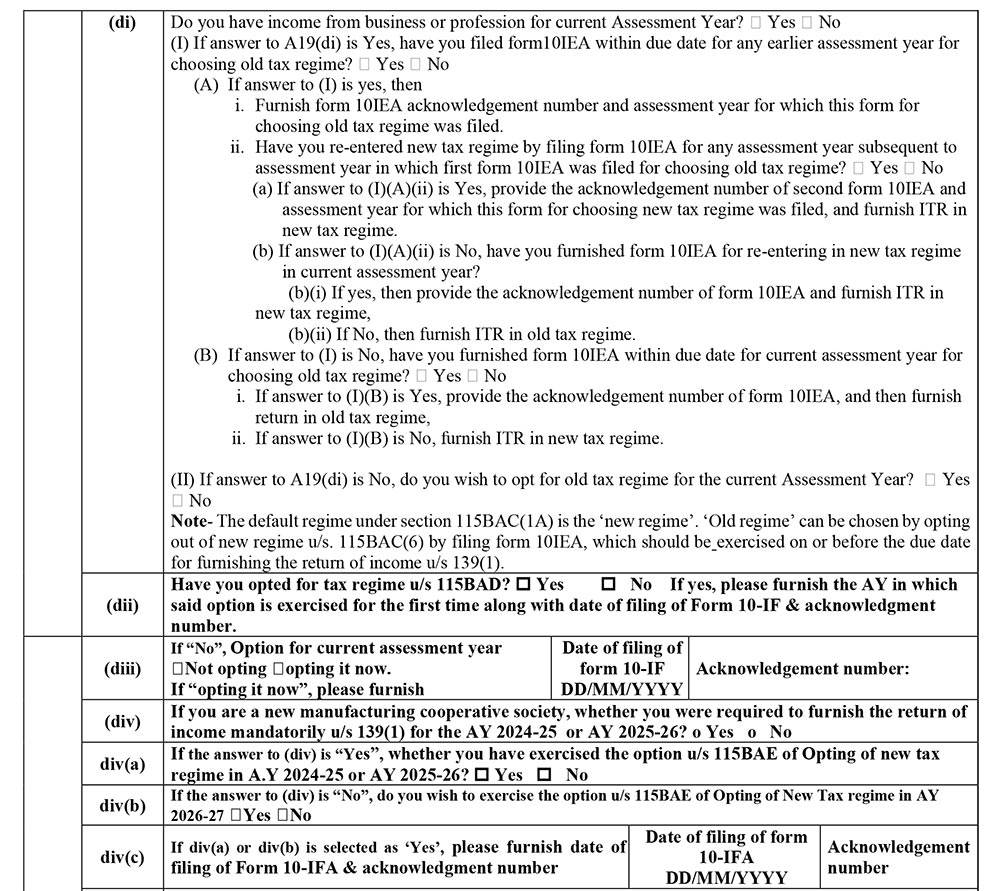

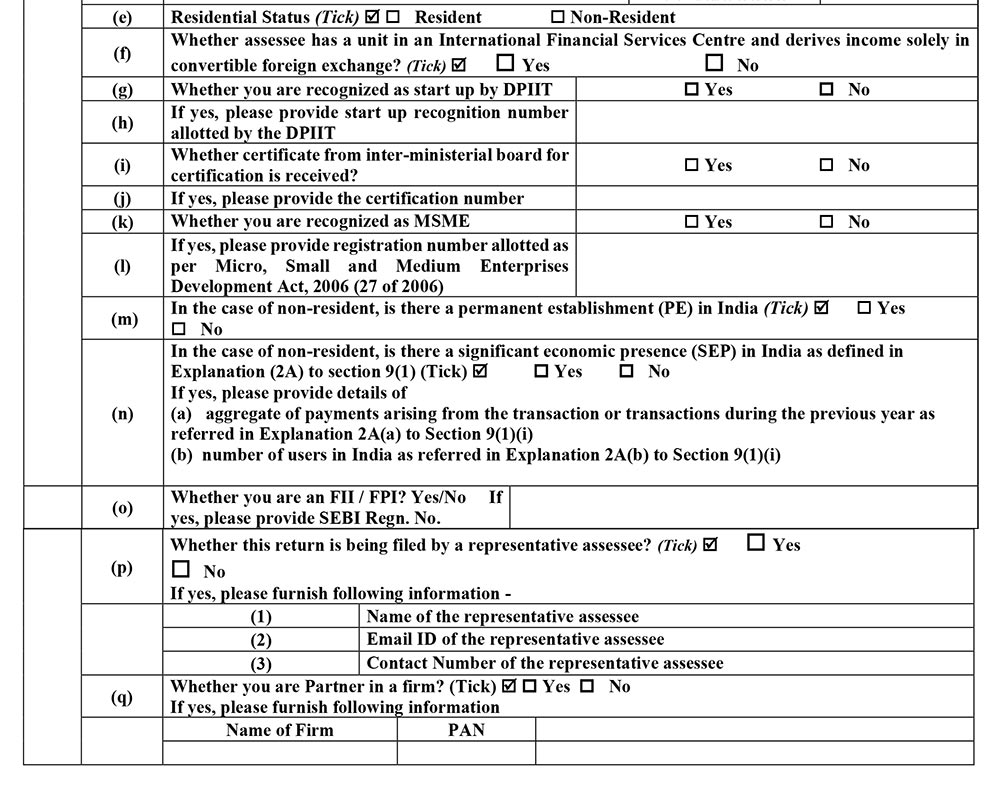

Step-by-Step Guide to File ITR 5 Form for AY 2026-27?

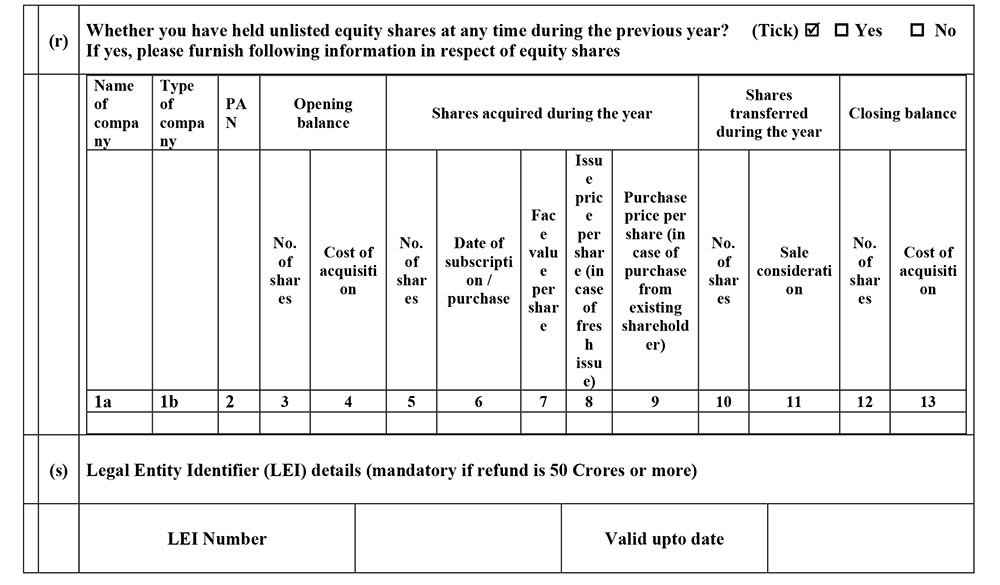

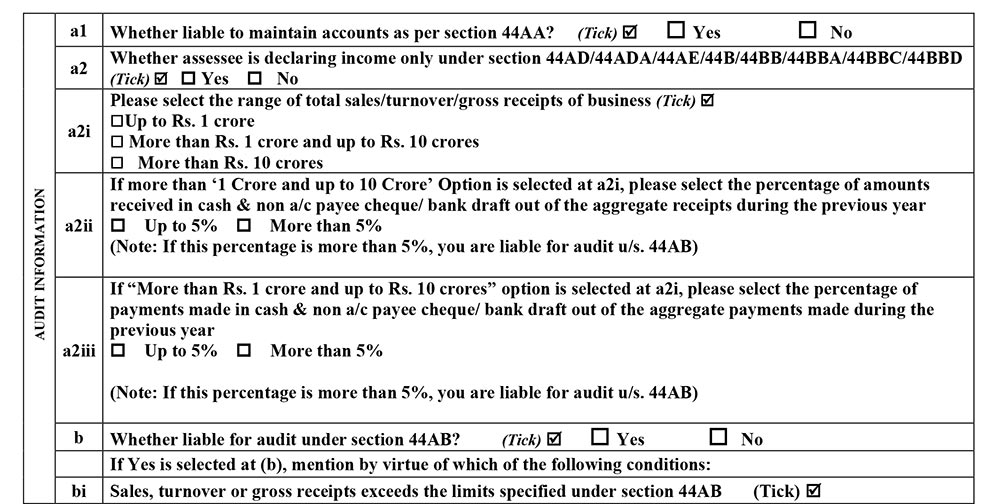

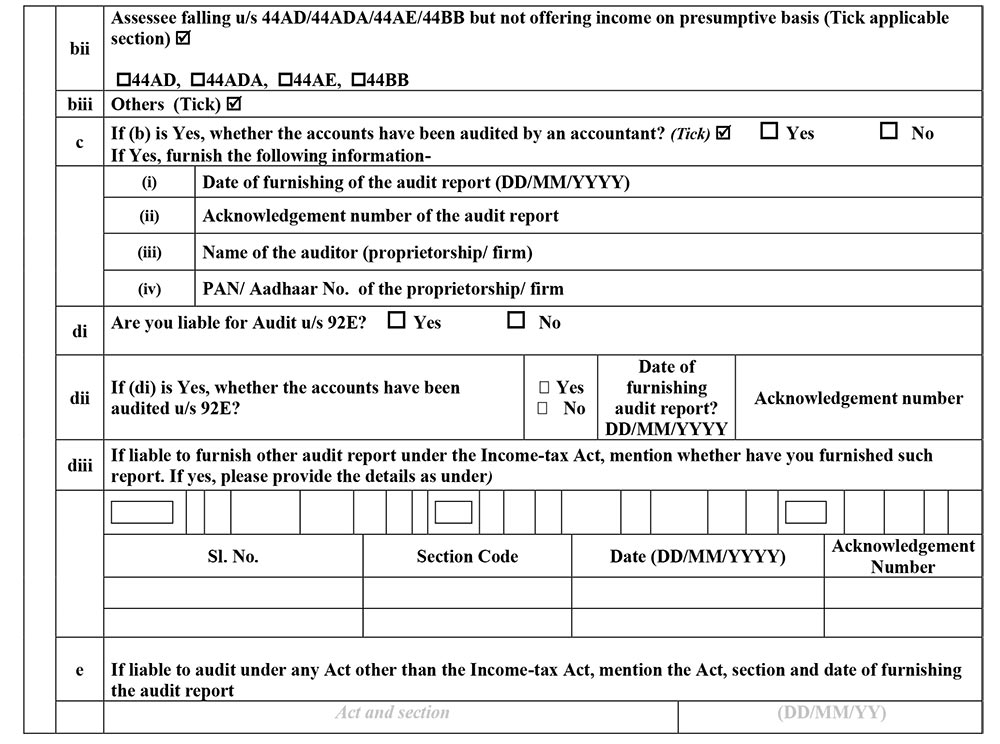

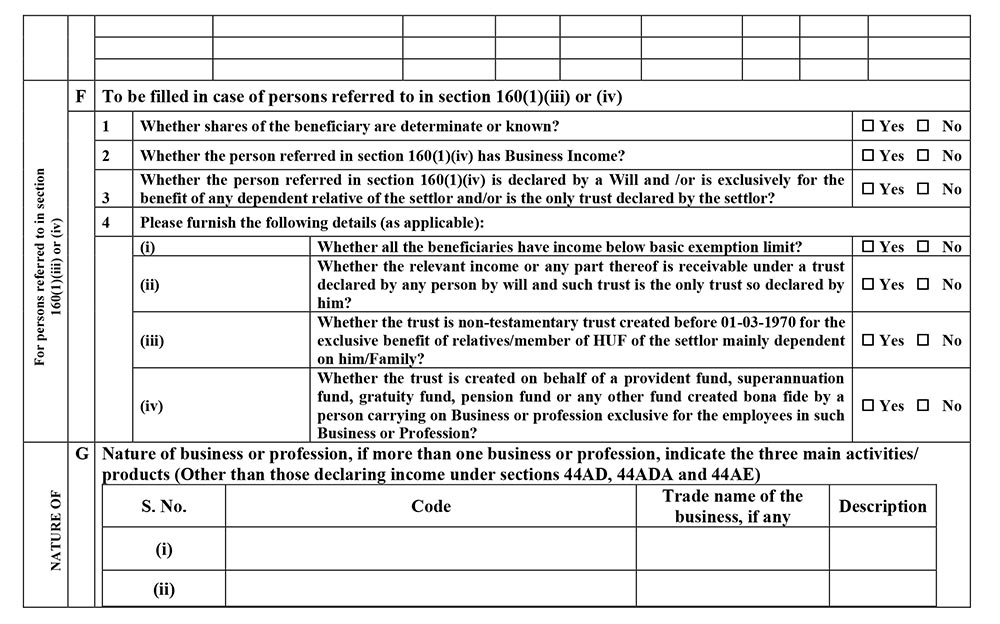

Part A General

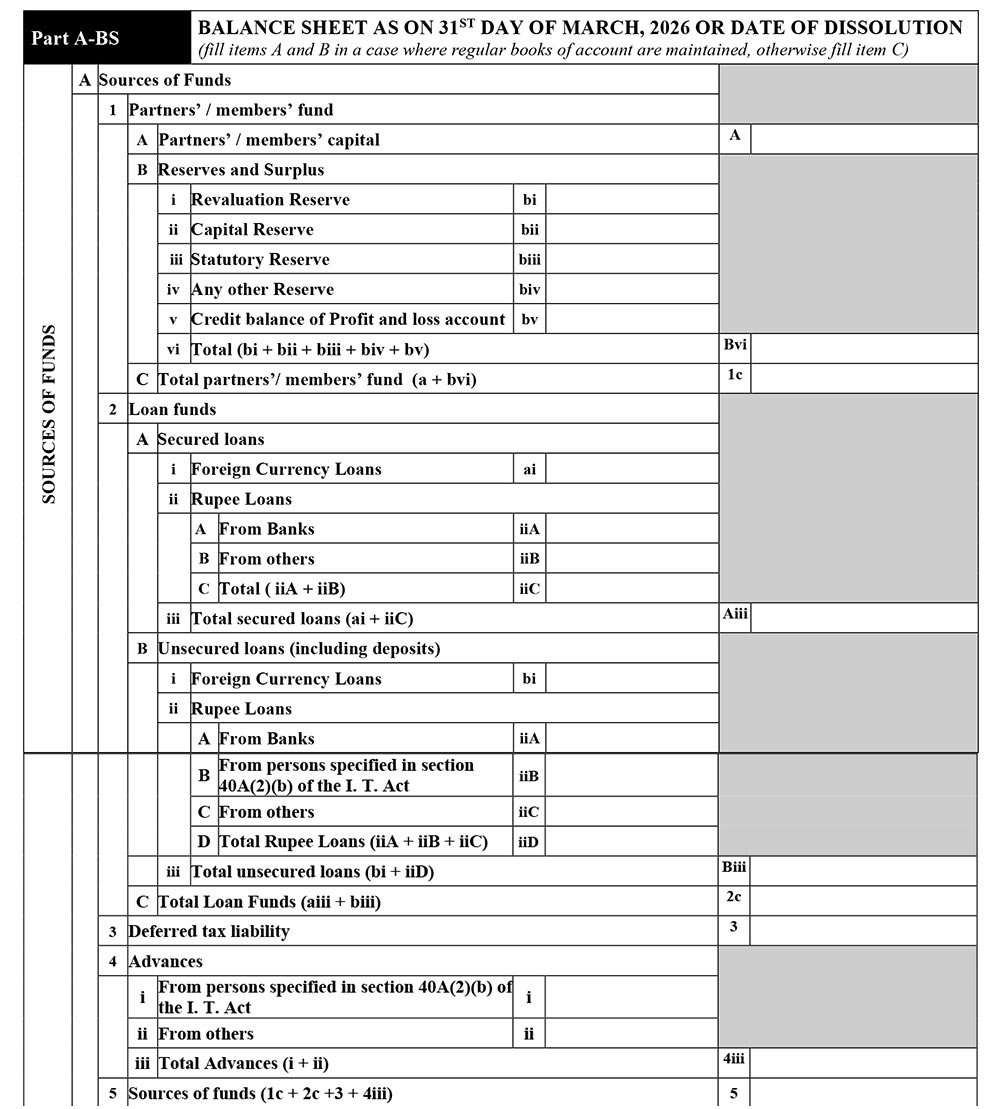

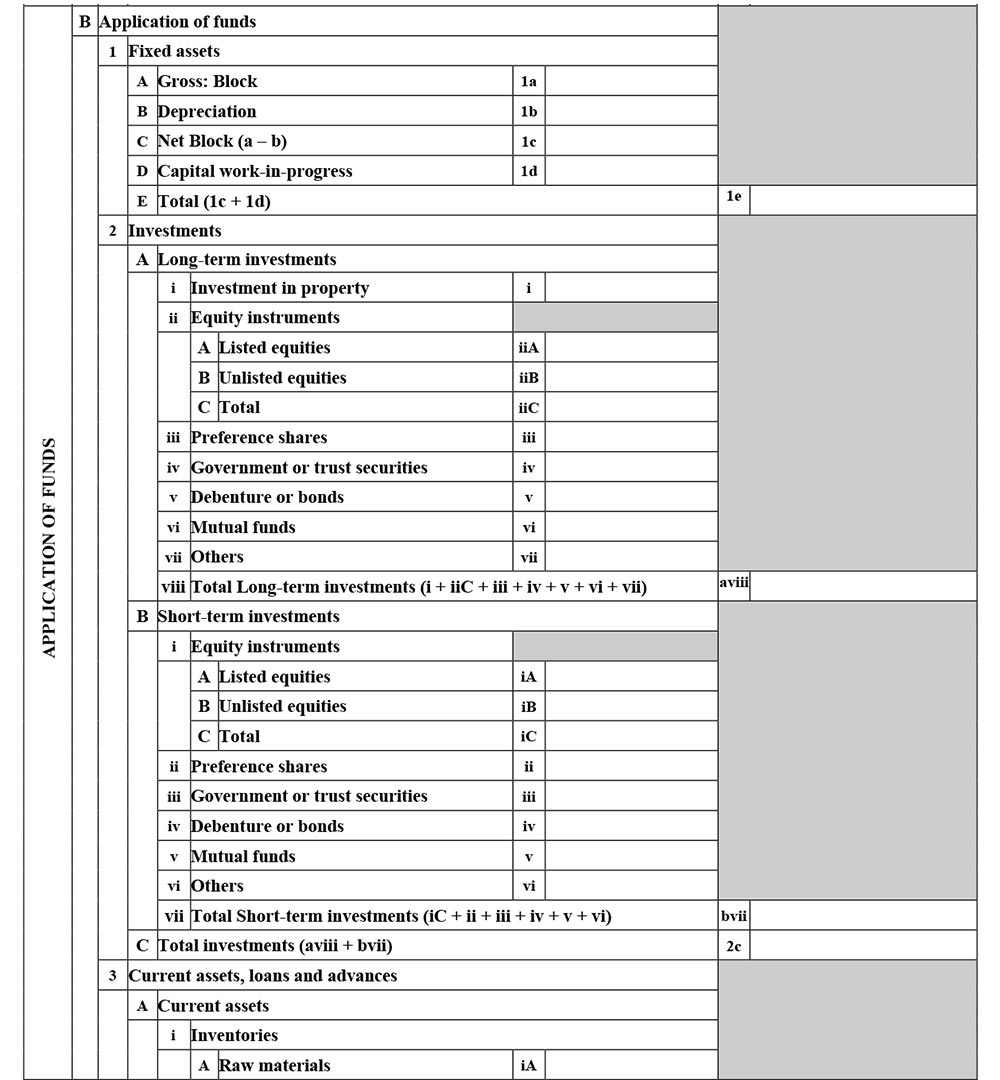

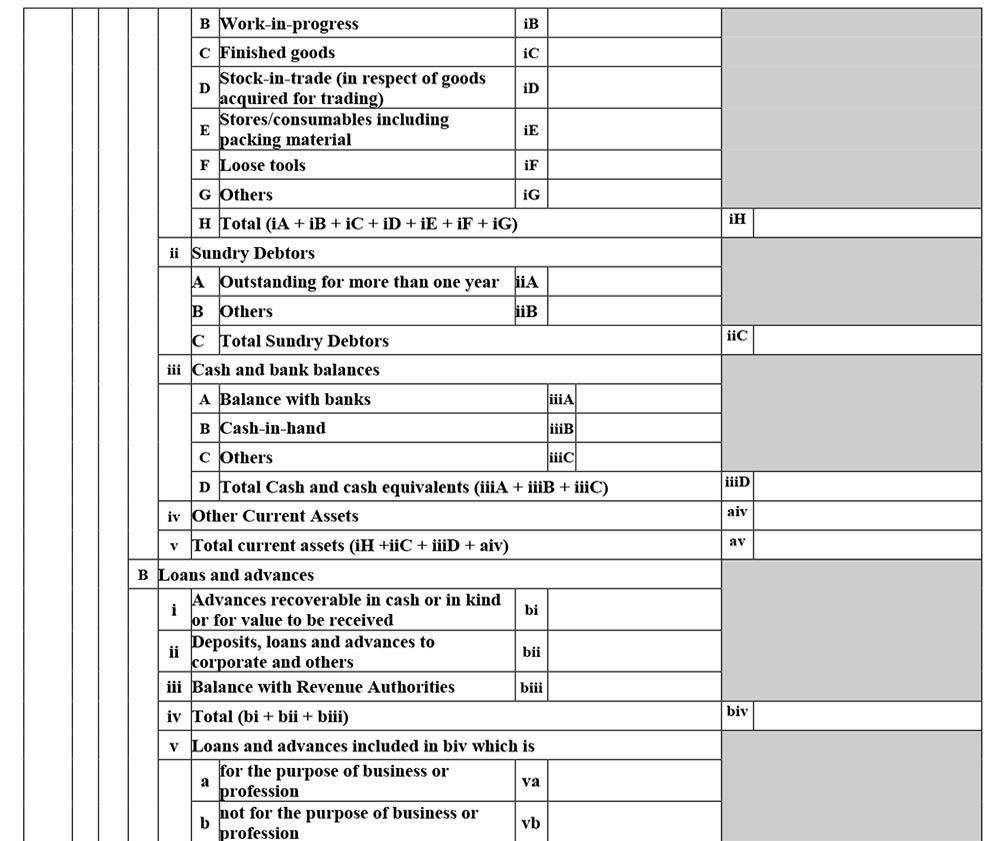

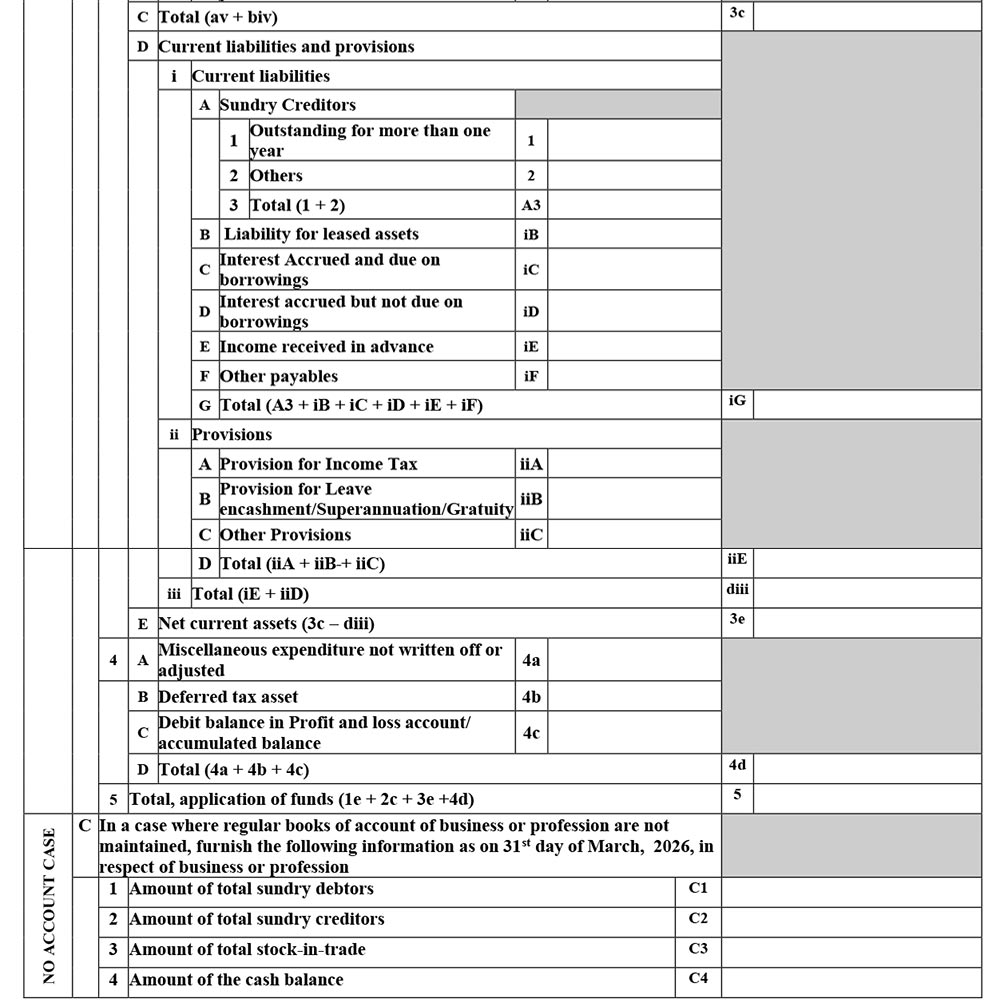

Part-A BS

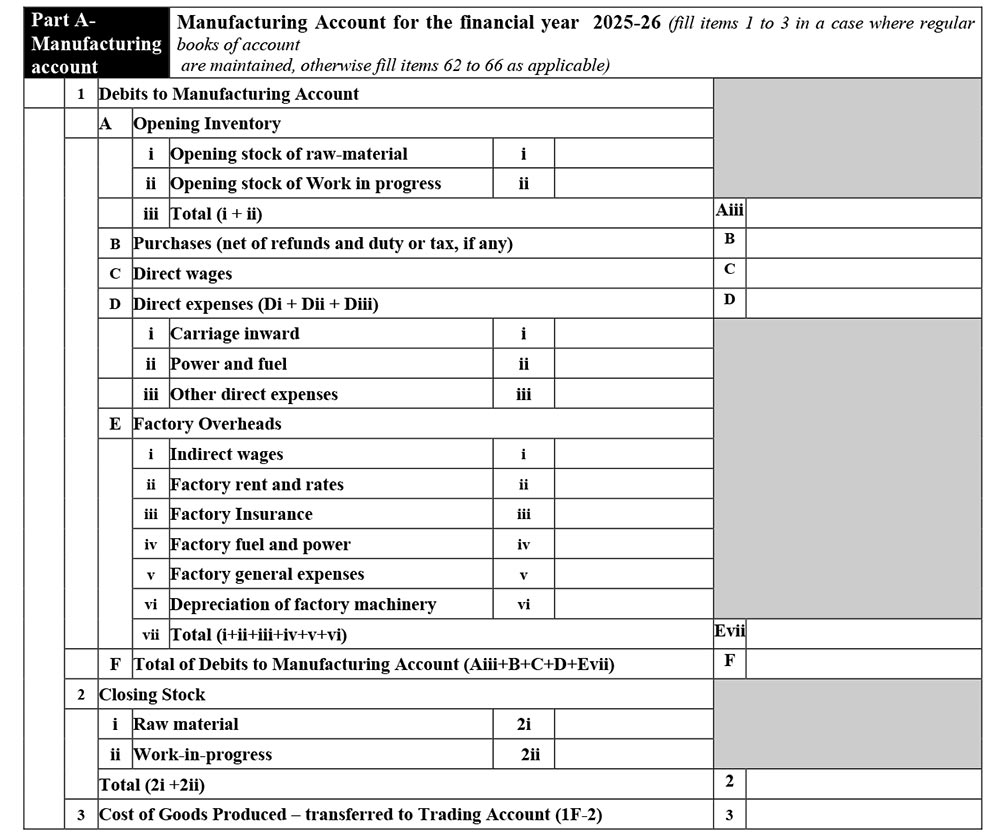

Part-A Manufacturing Account

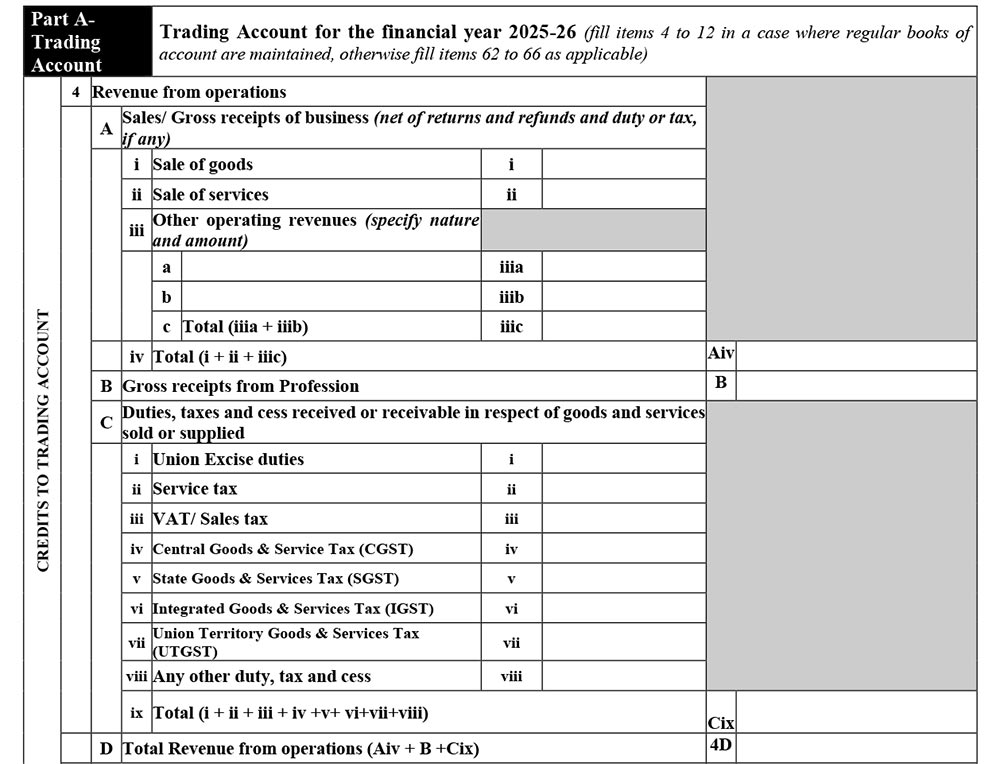

Part-A Trading Account

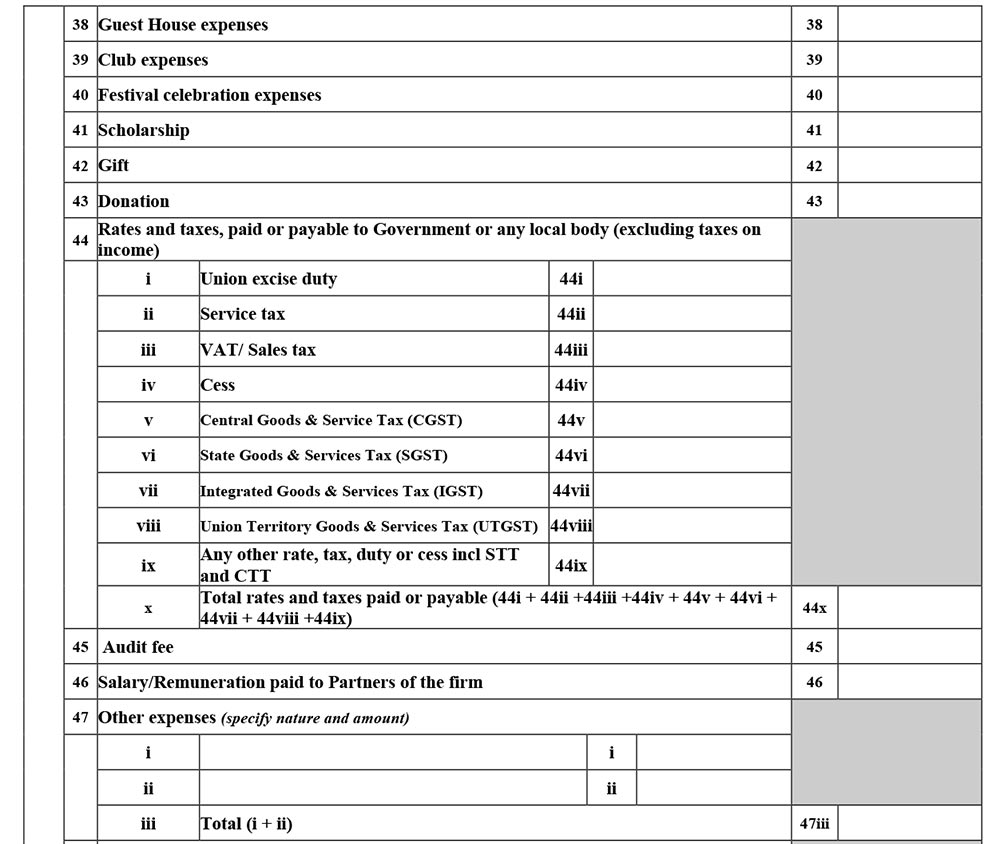

Part-A P&L

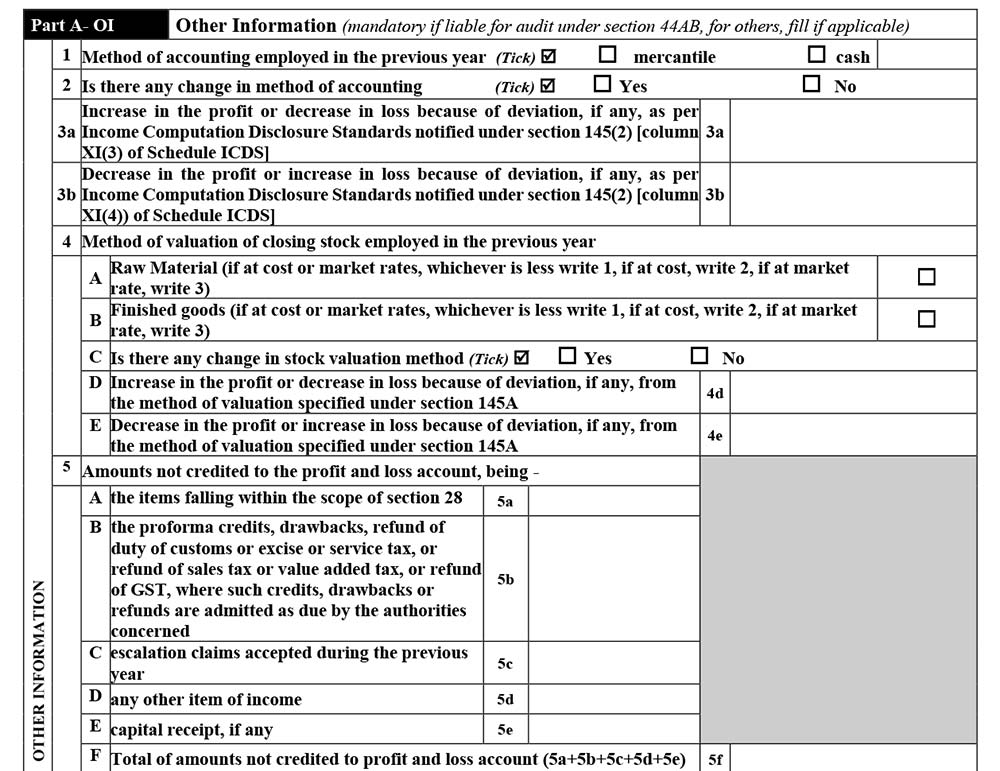

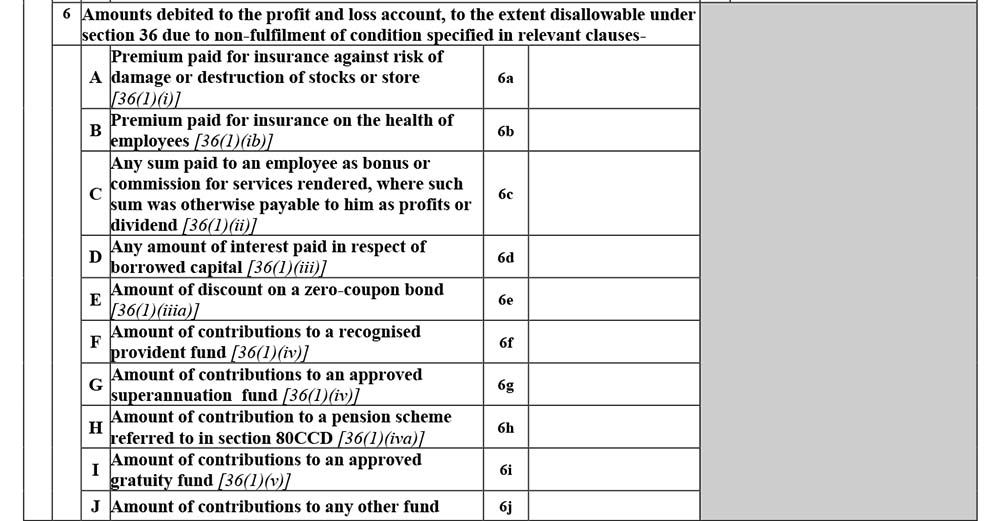

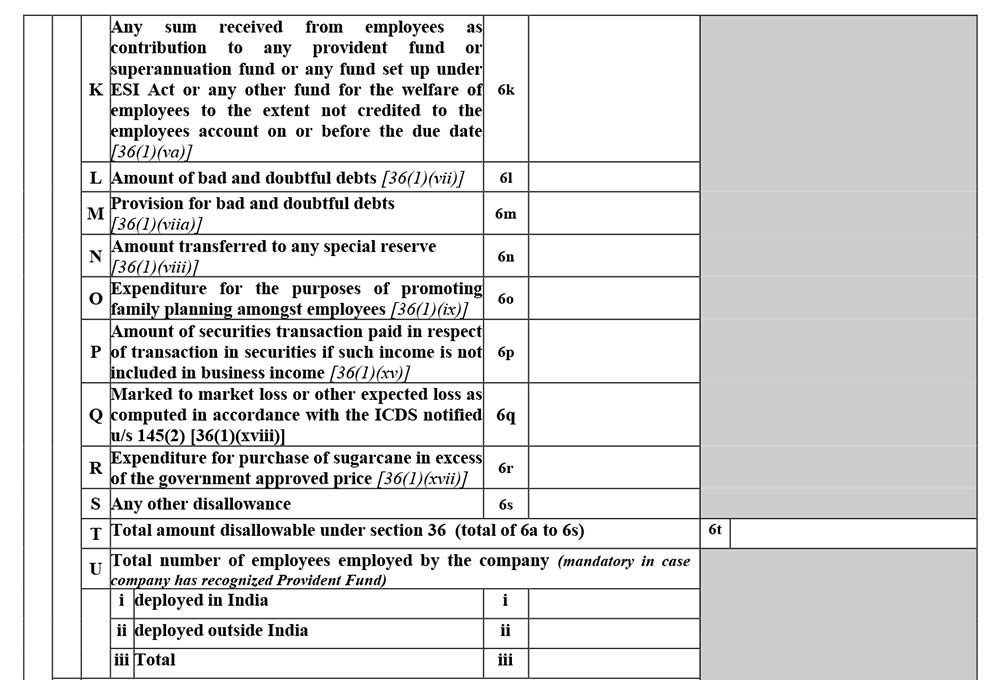

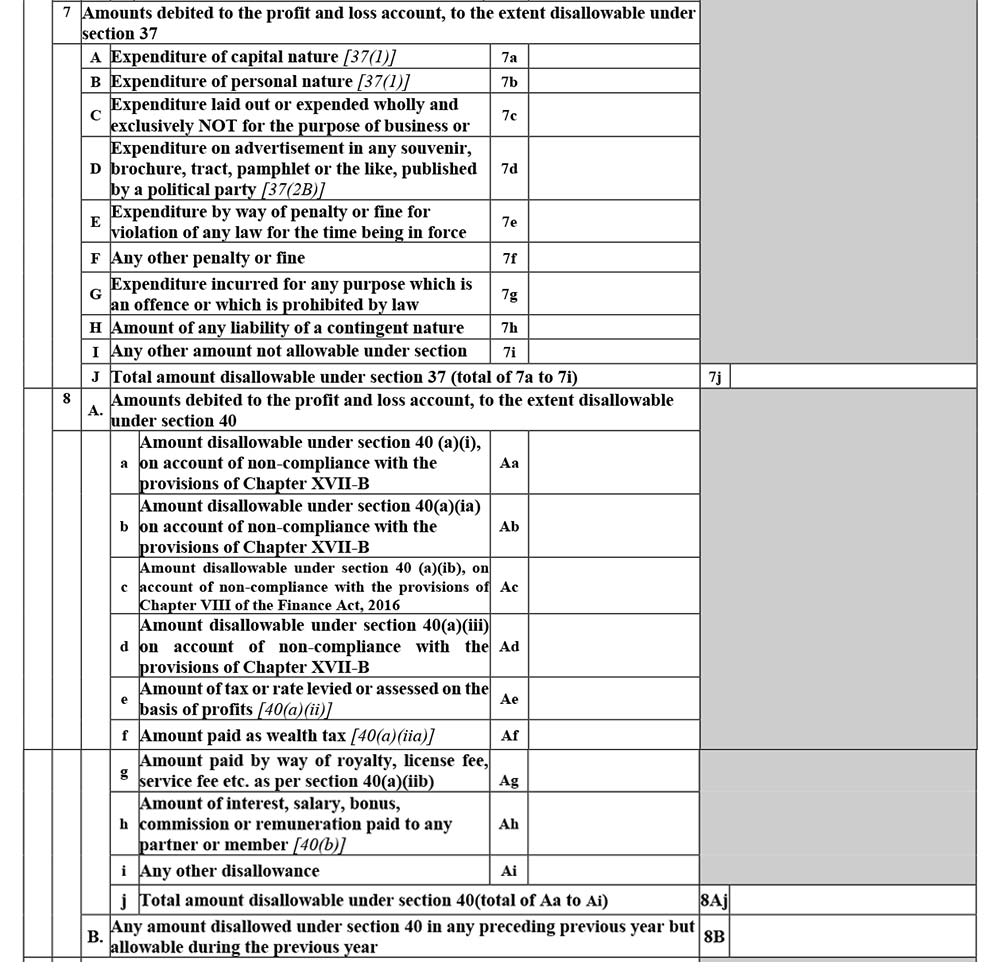

Part-A OI

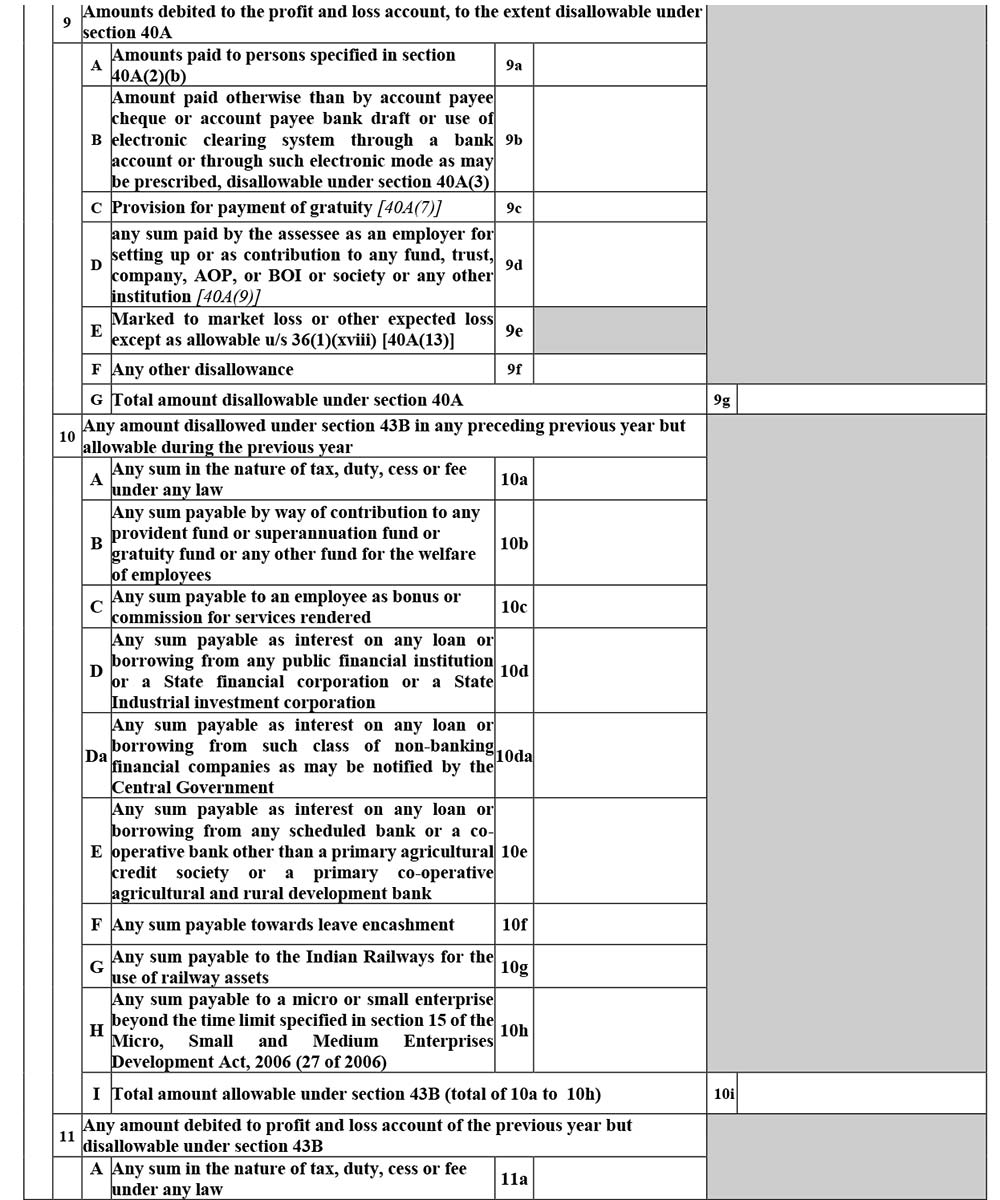

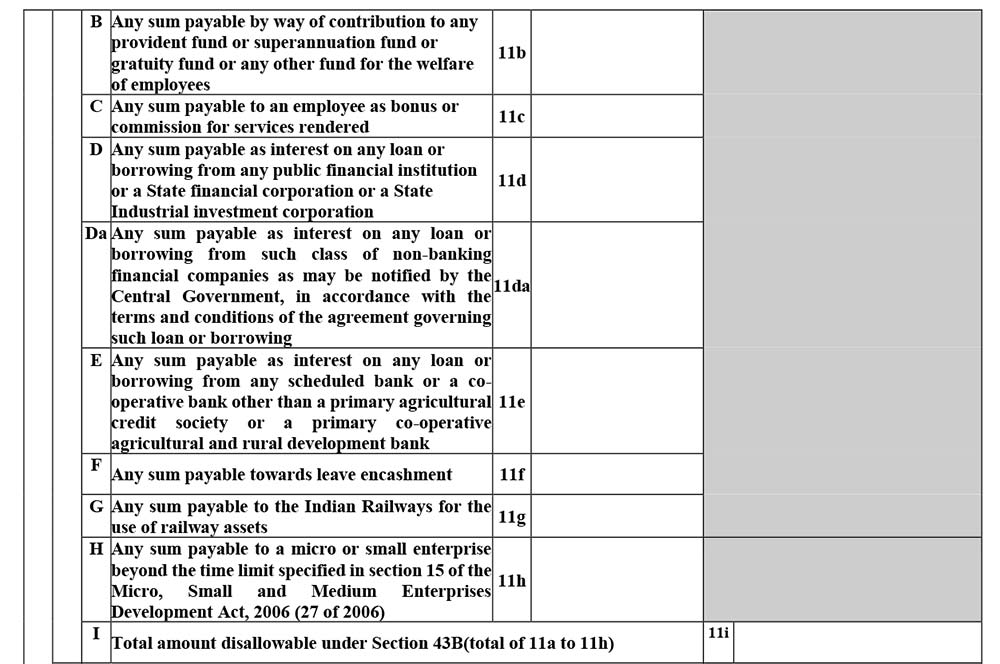

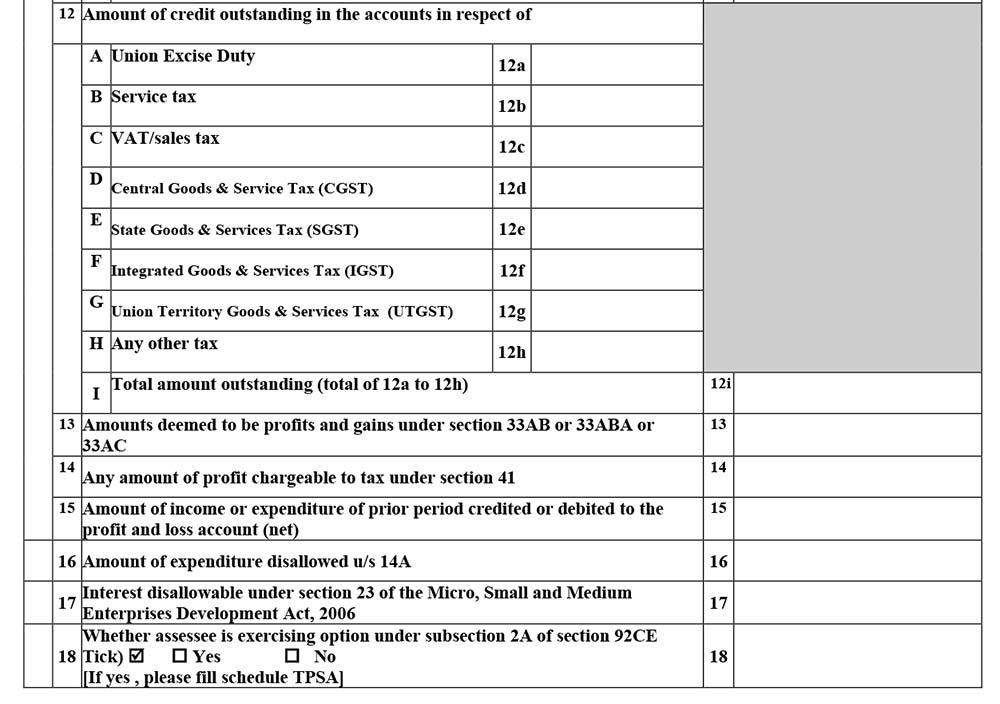

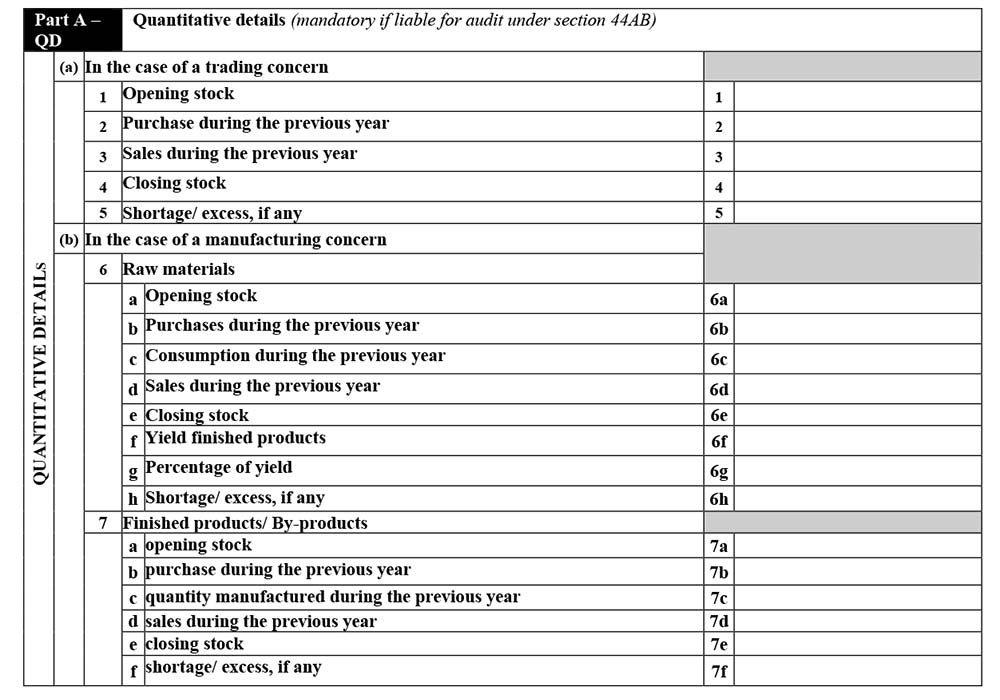

Part-A QD

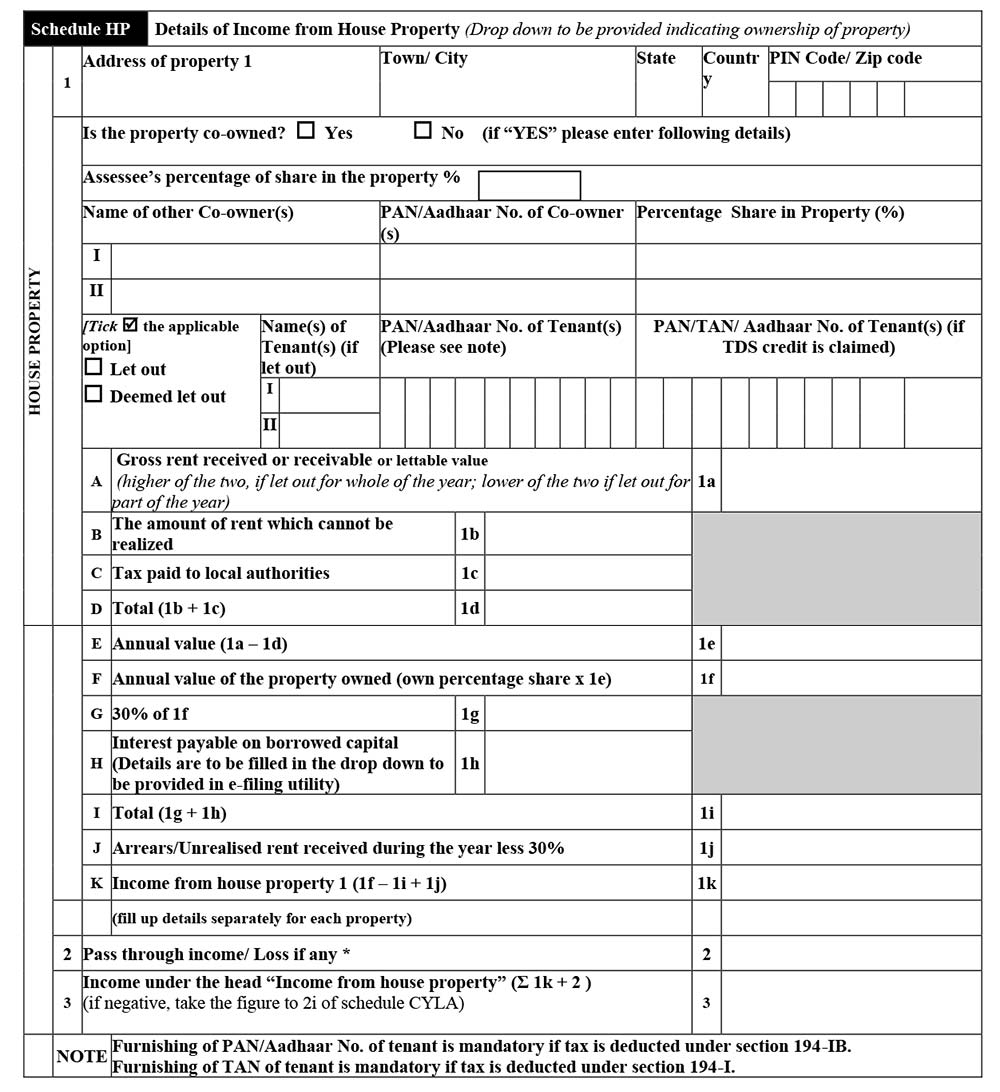

Schedule HP

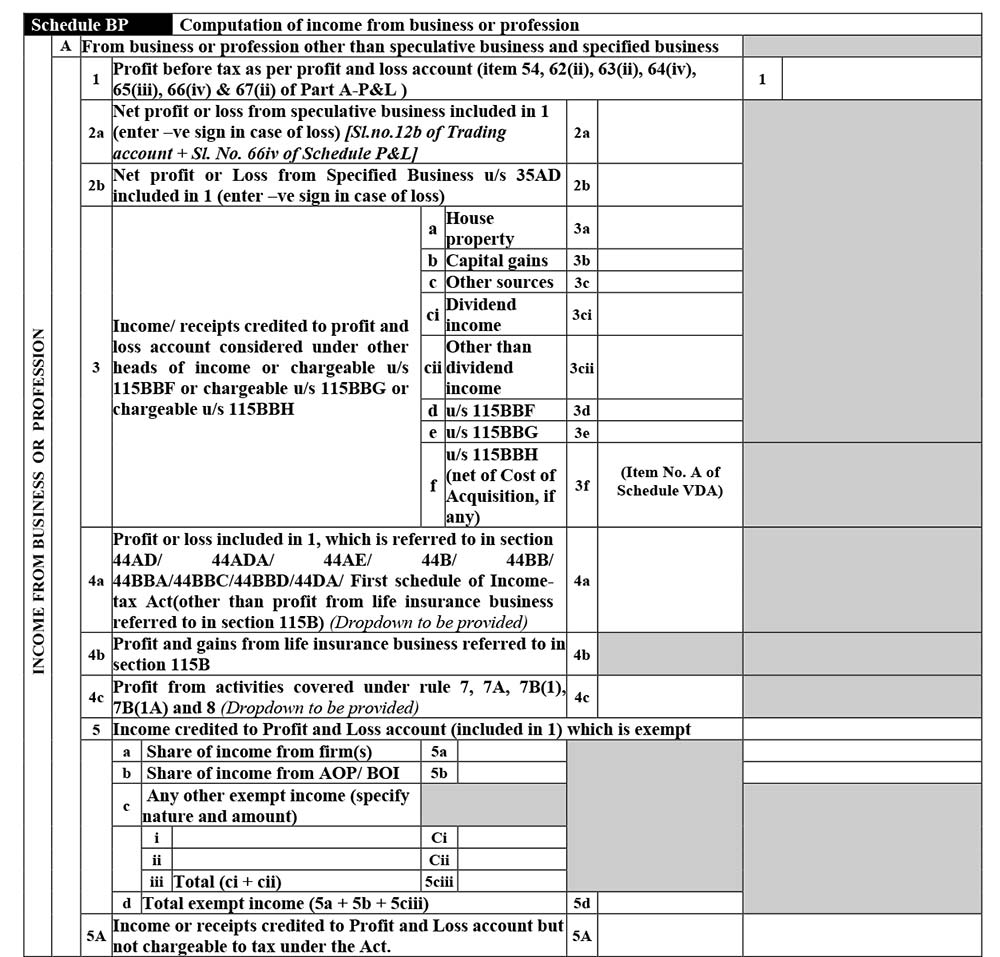

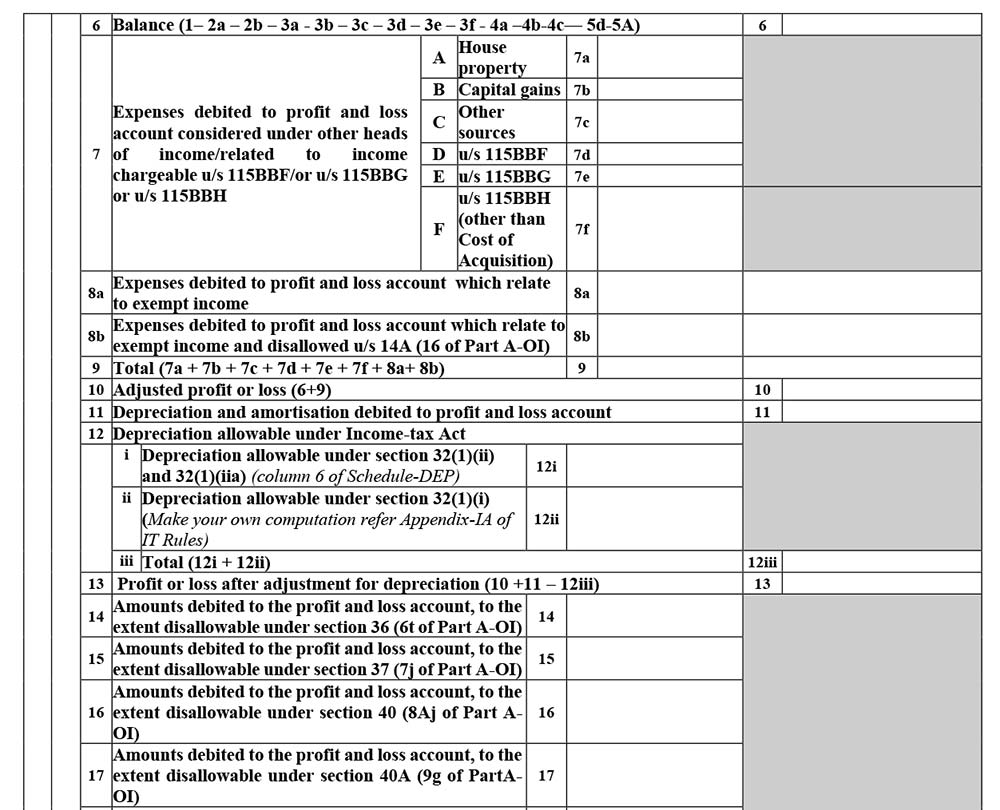

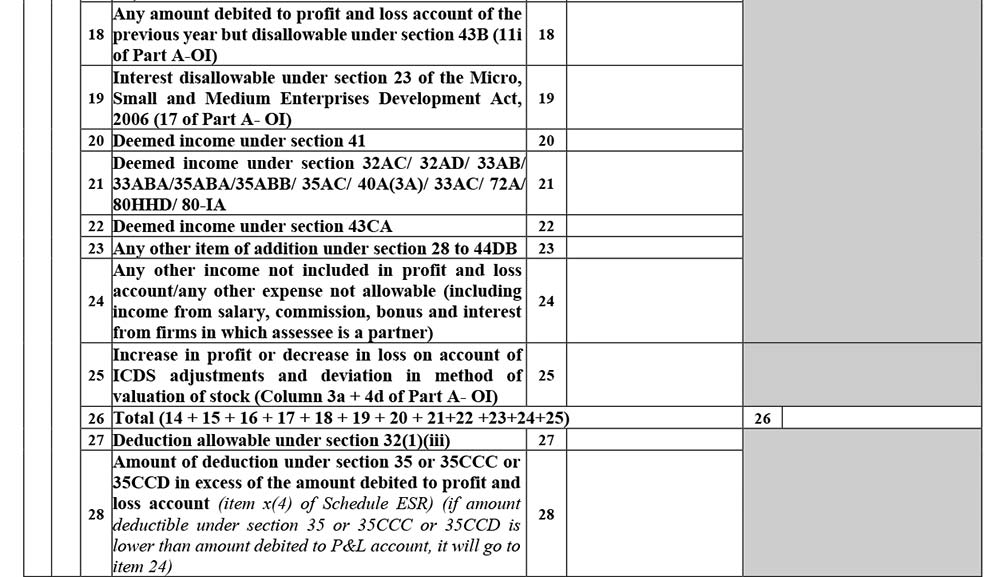

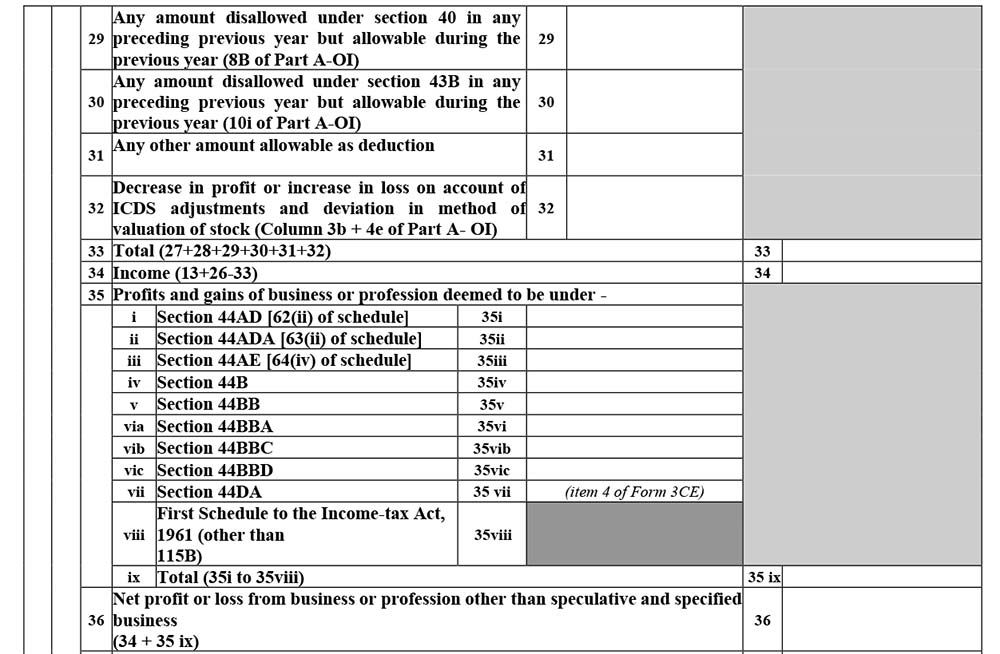

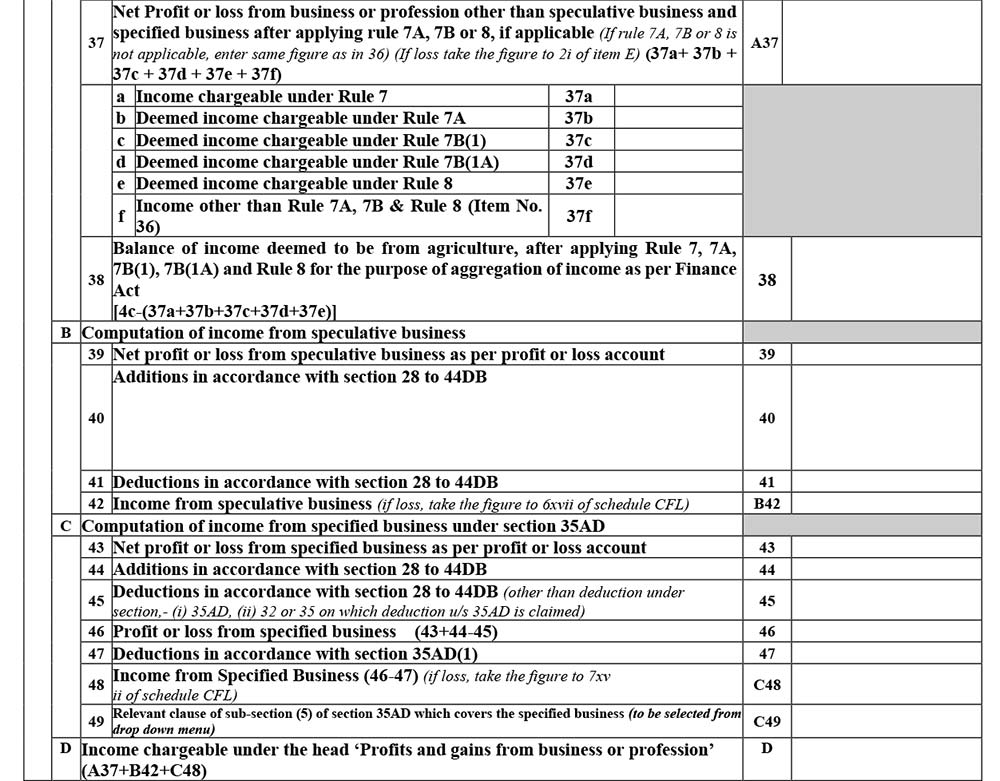

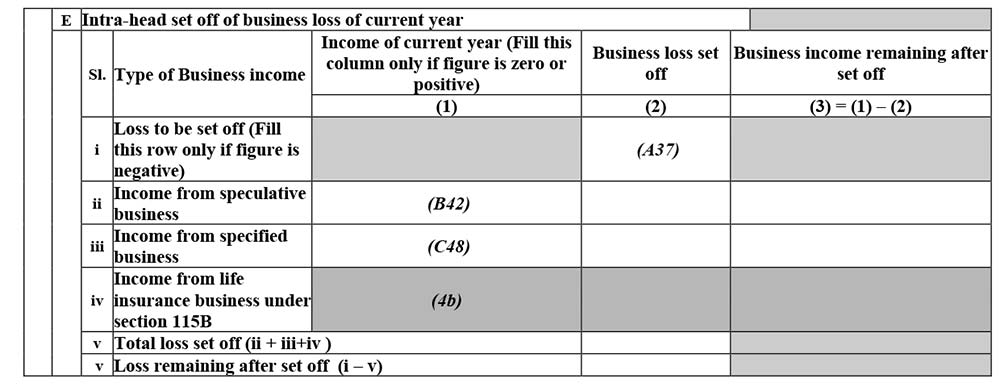

Schedule BP

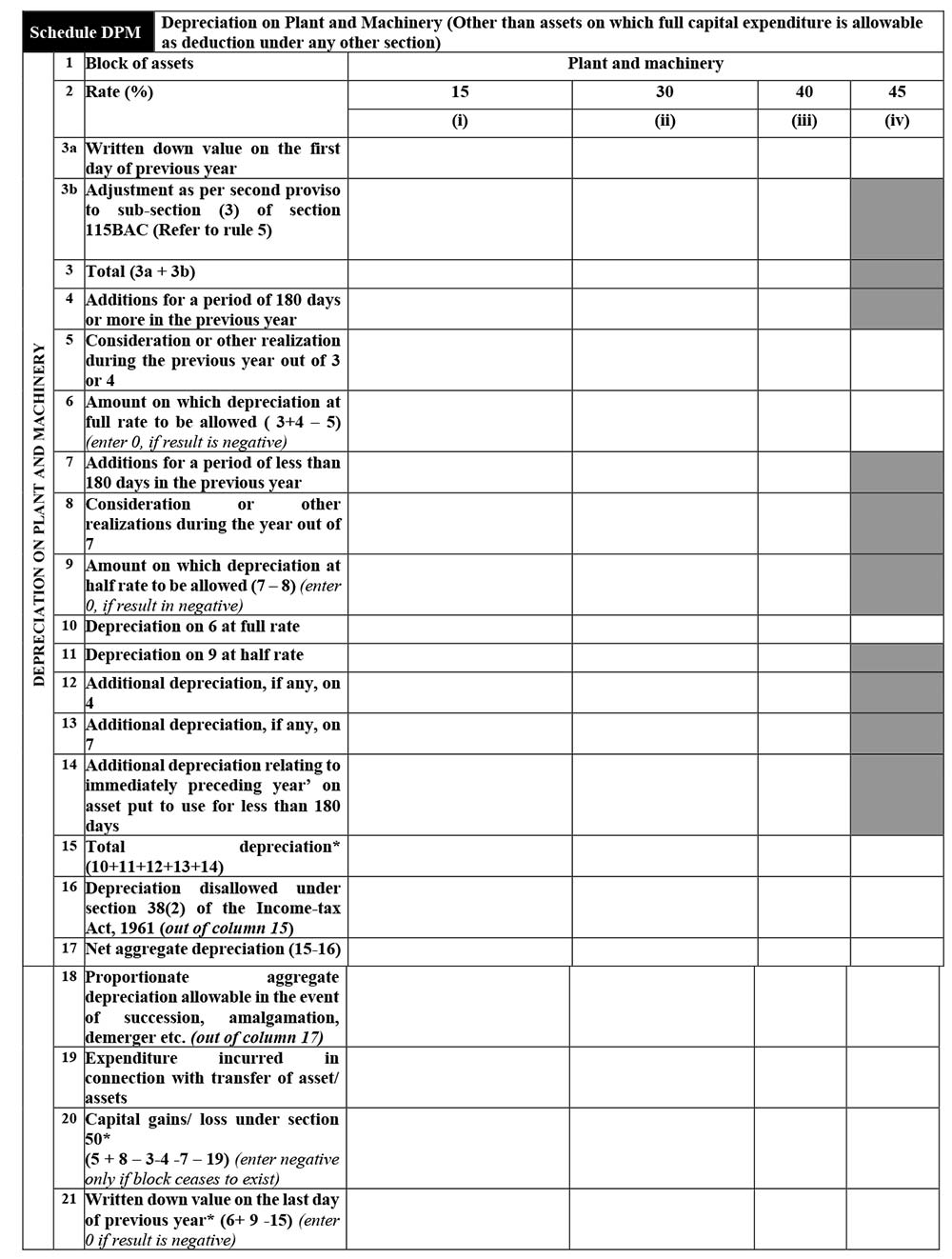

Schedule DPM

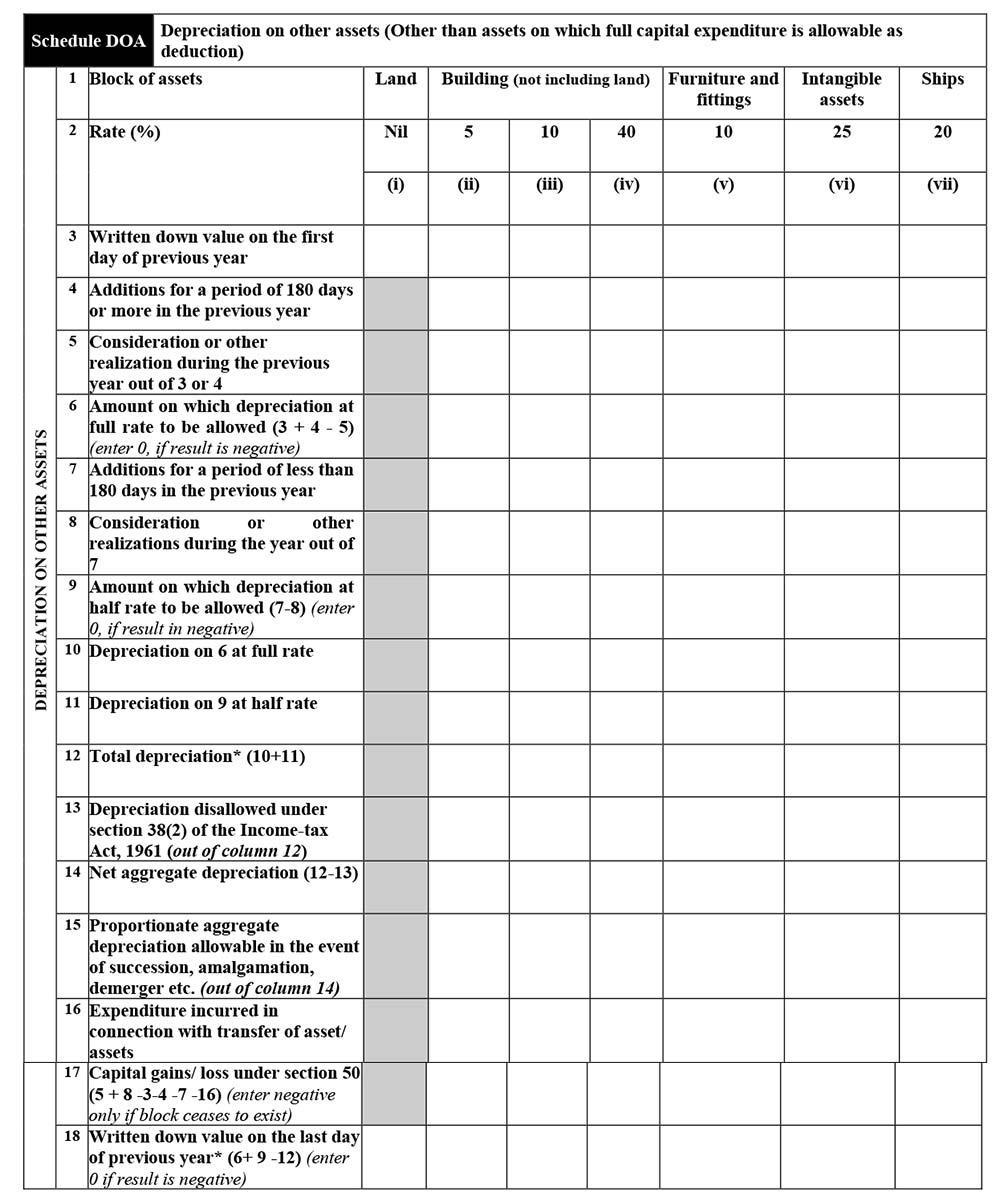

Schedule DOA

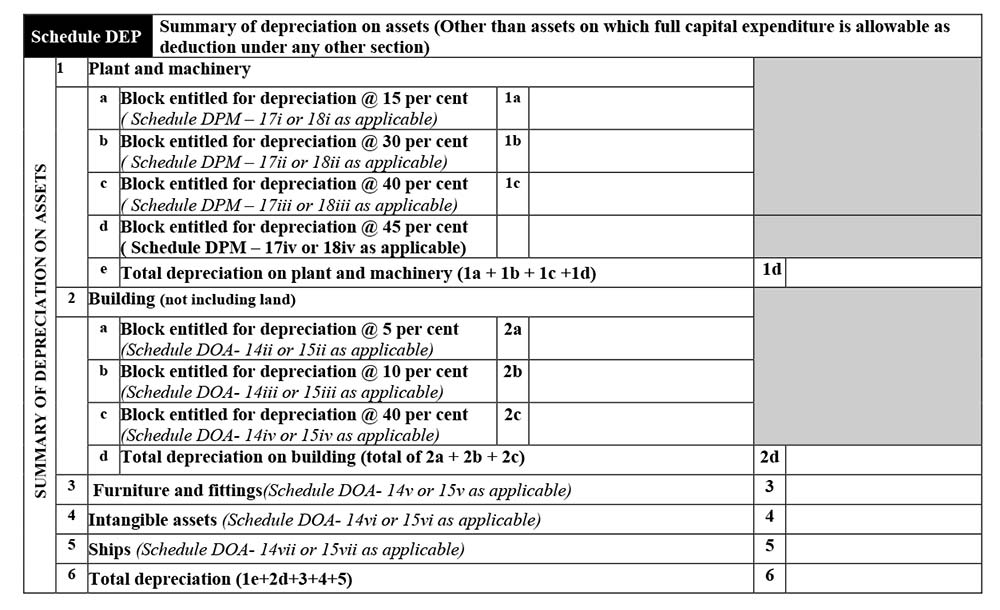

Schedule DEP

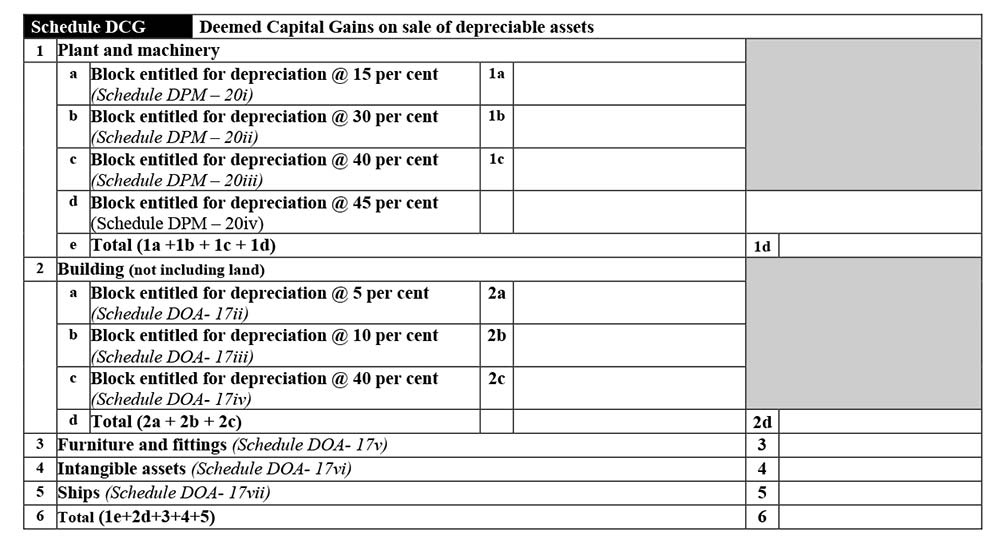

Schedule DCG

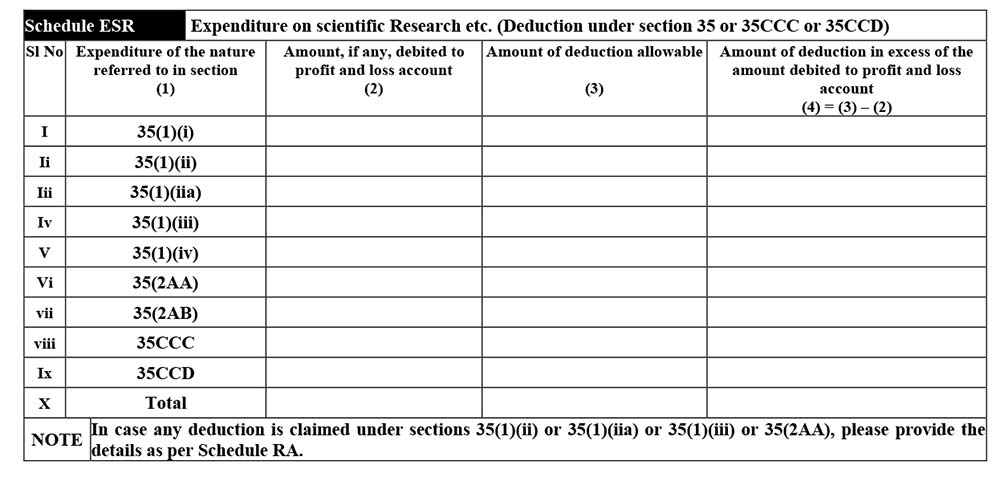

Schedule ESR

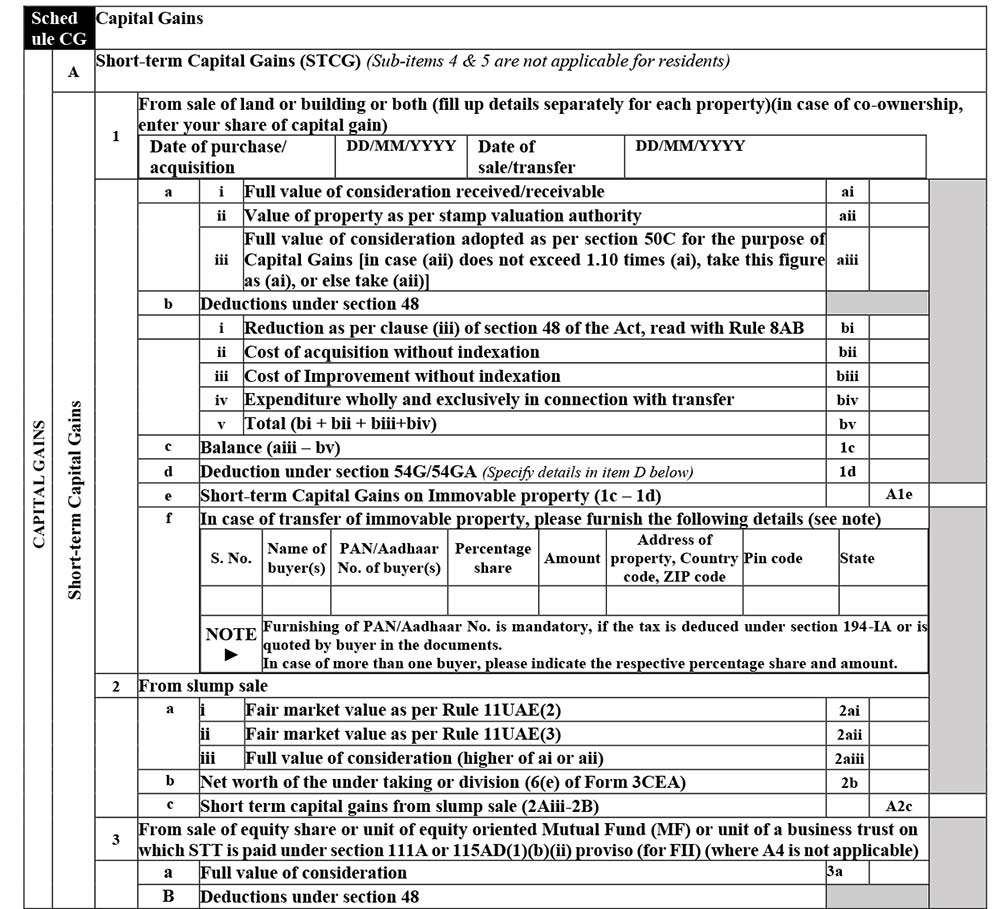

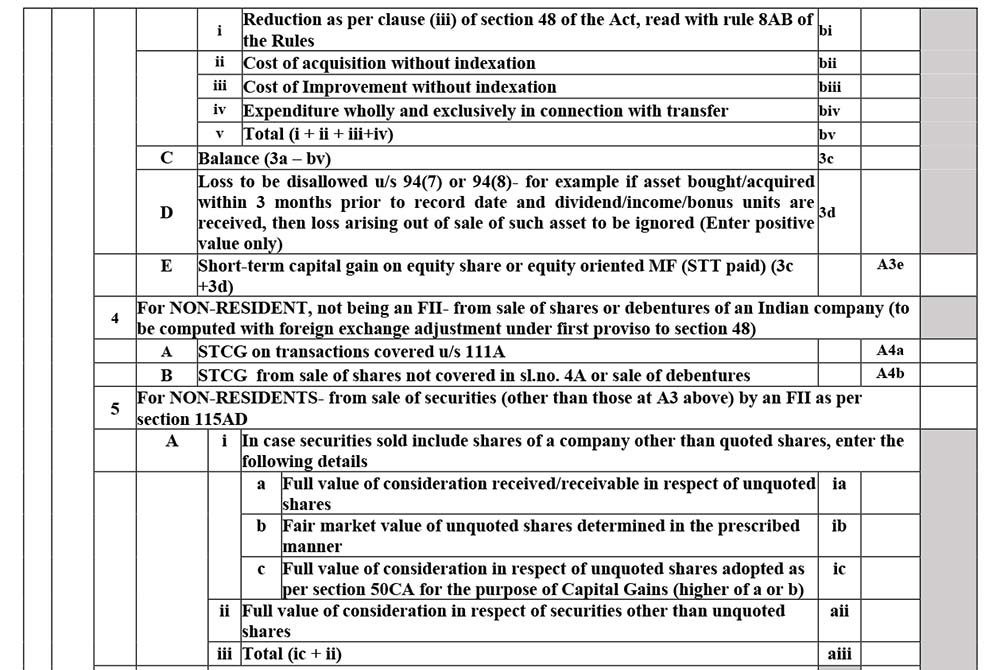

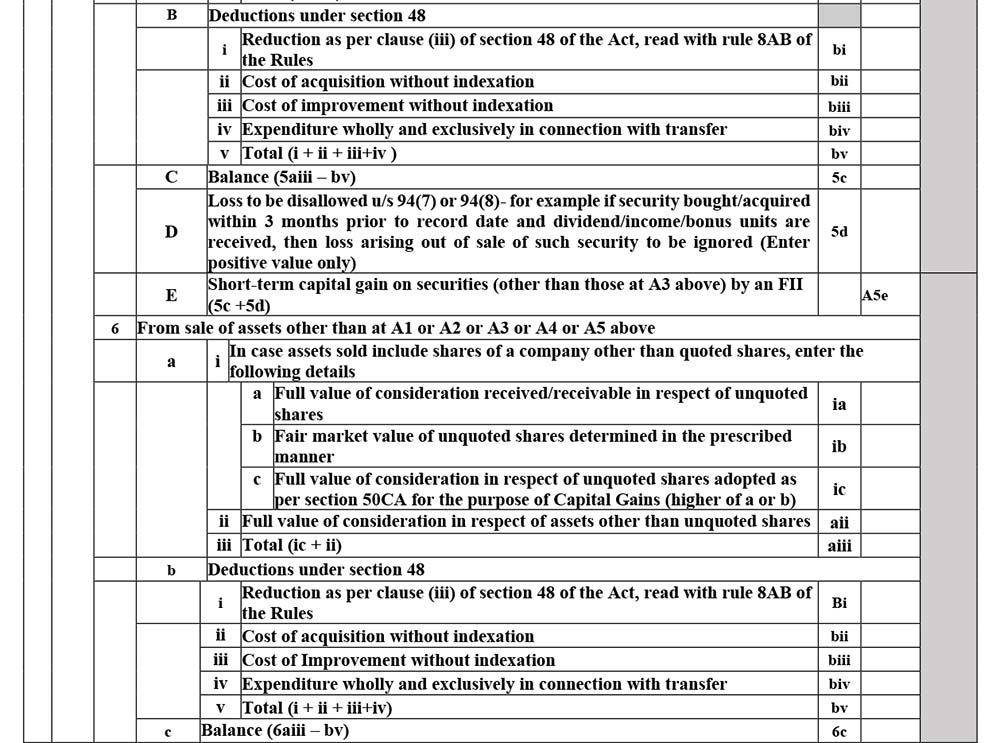

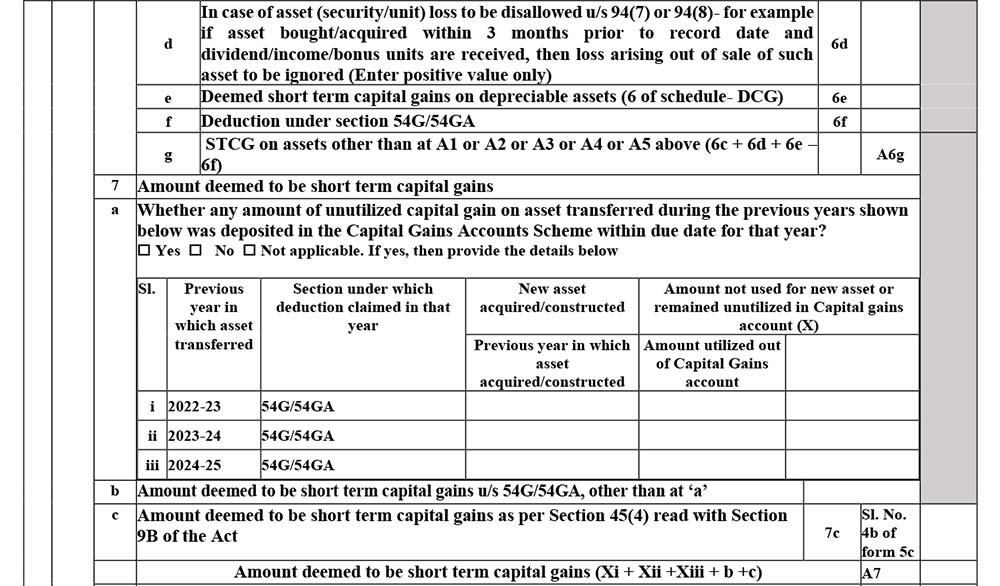

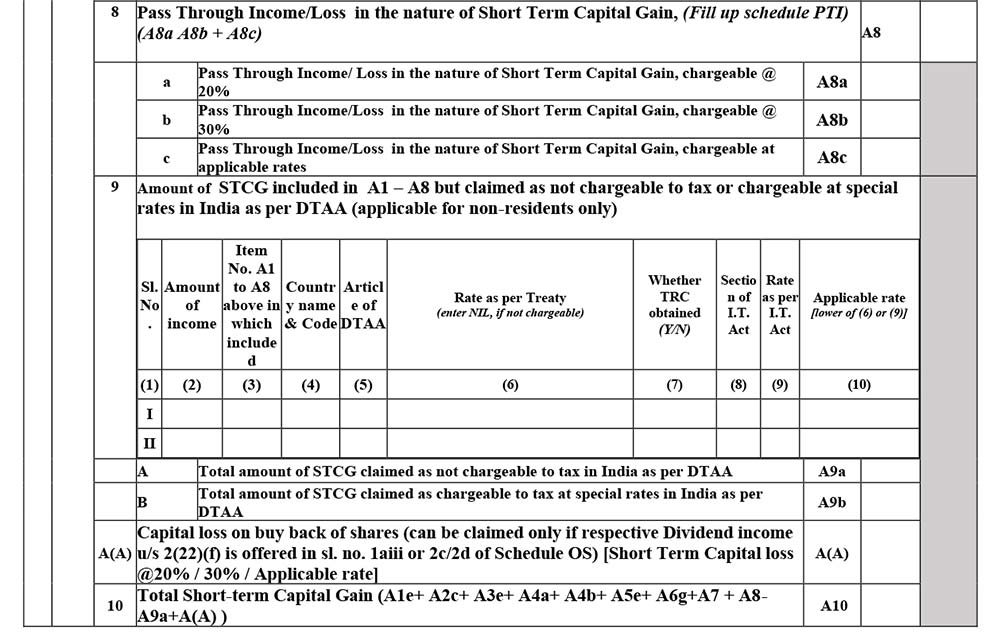

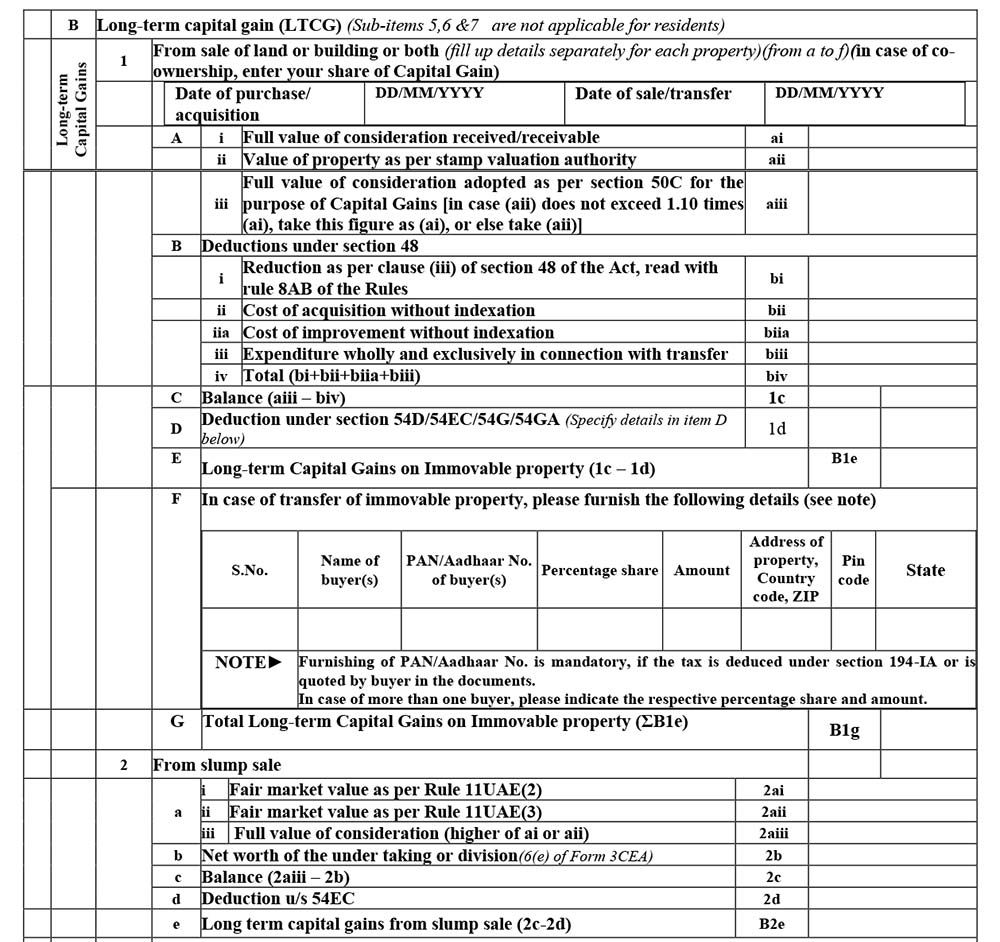

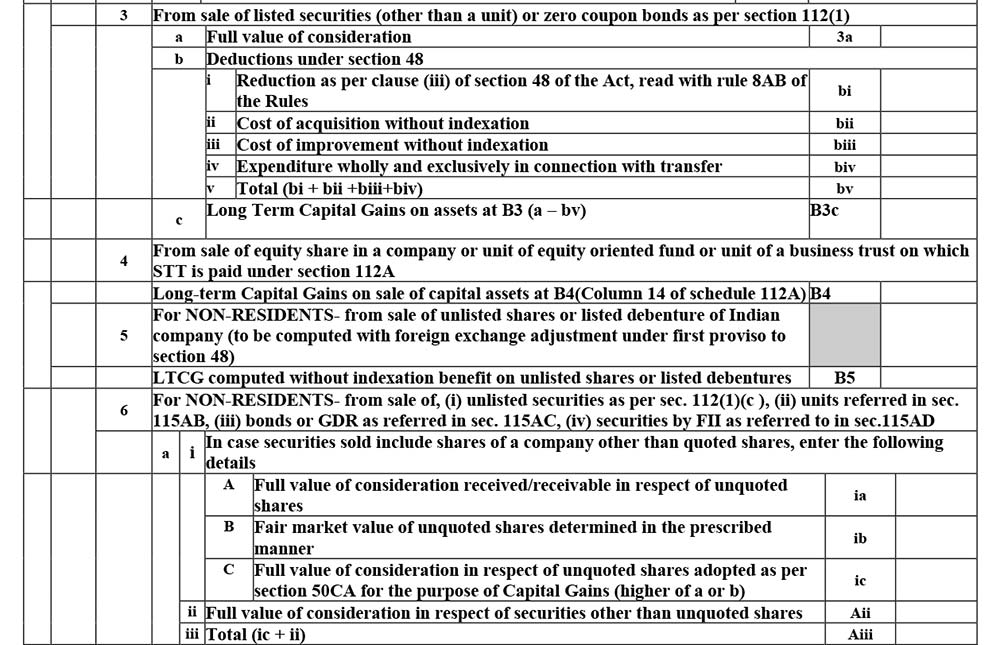

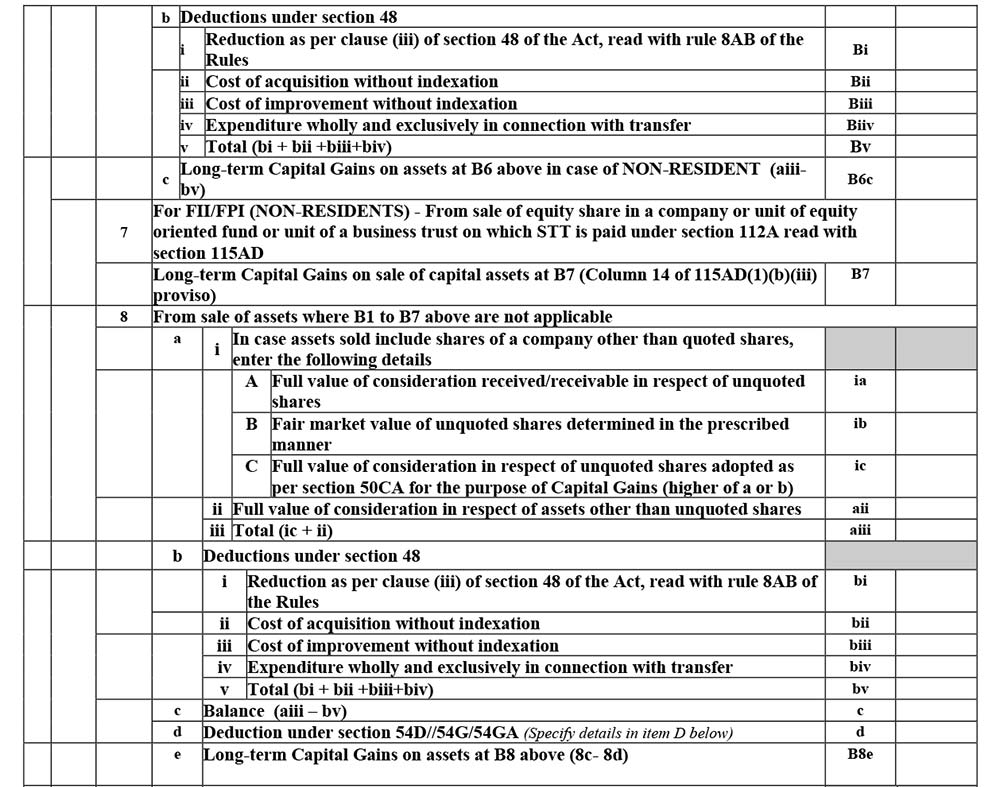

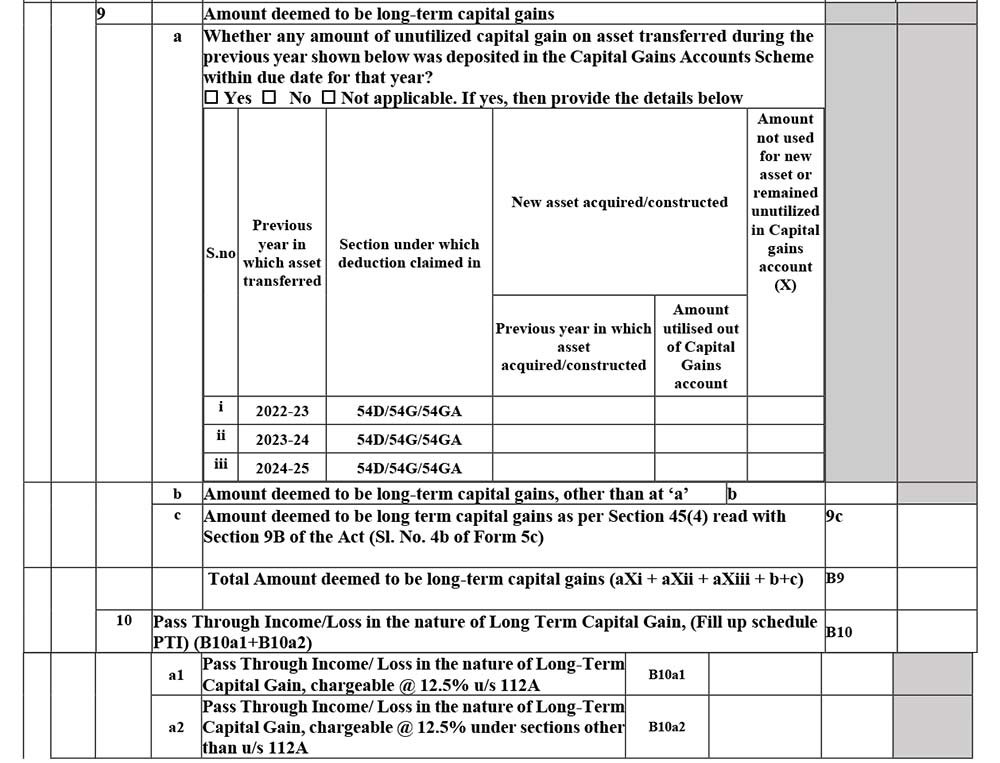

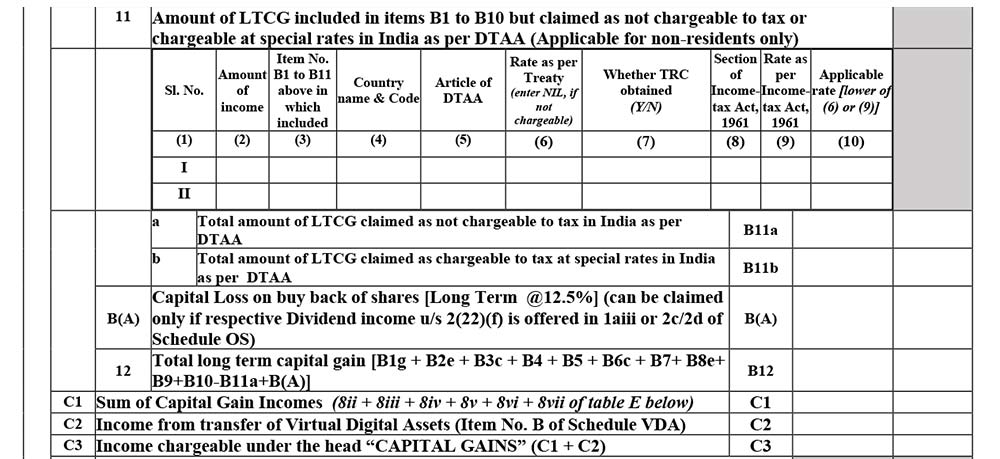

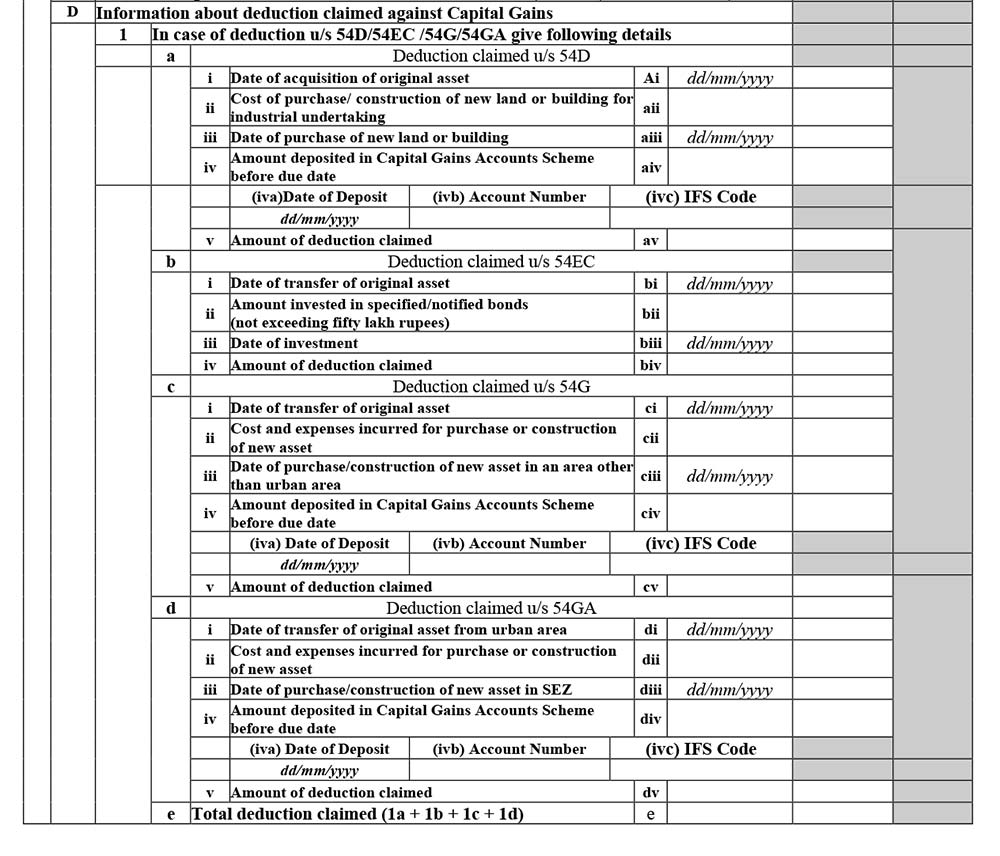

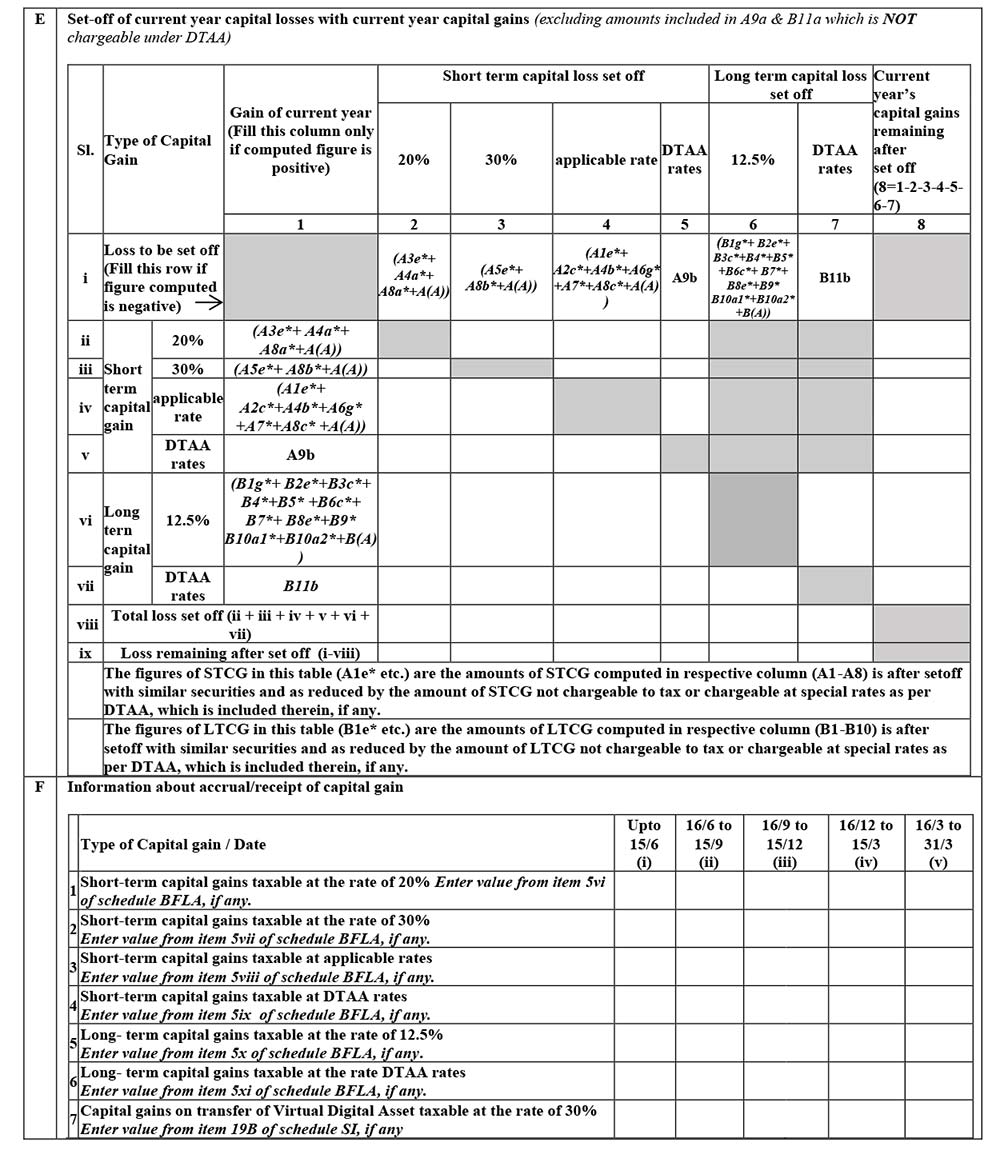

Schedule CG

A. Short-Term Capital Gain

B. Long-Term Capital Gain

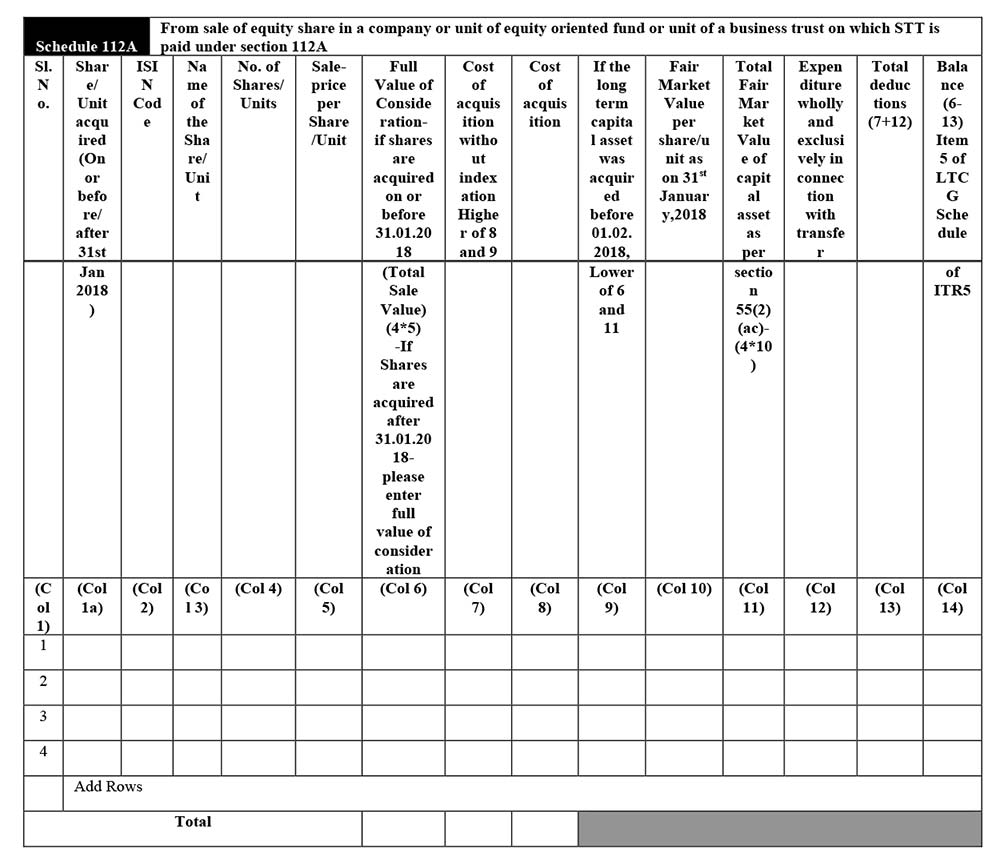

Schedule 112A

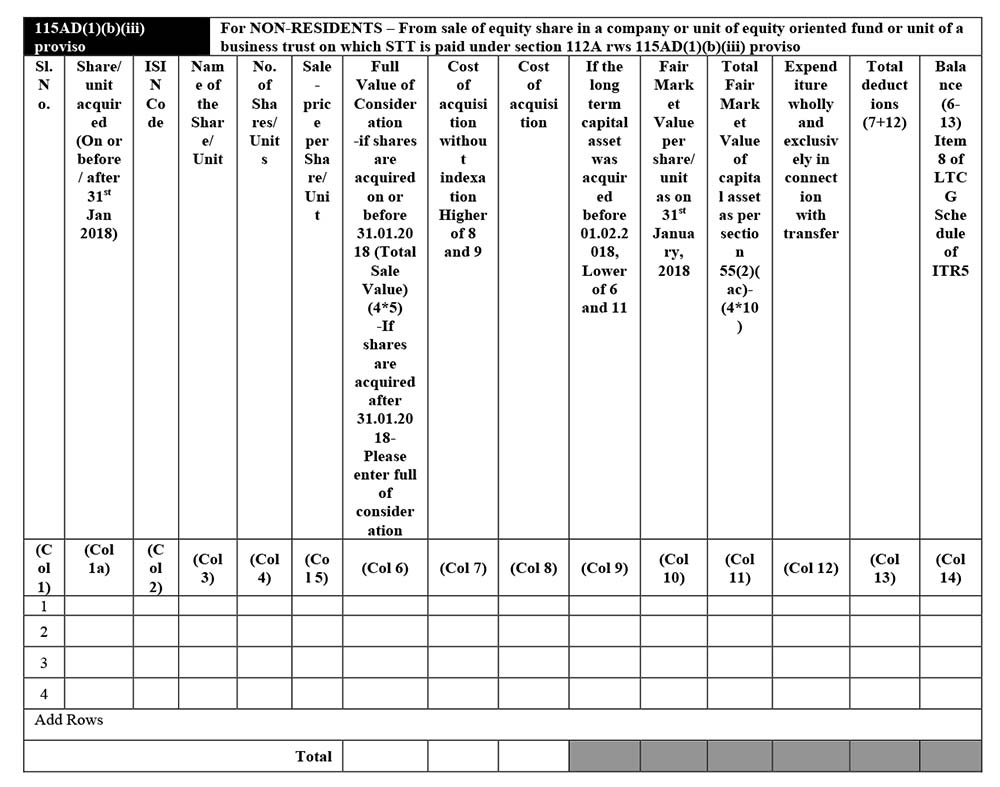

Schedule 115AD(1)(b)(iii) Proviso

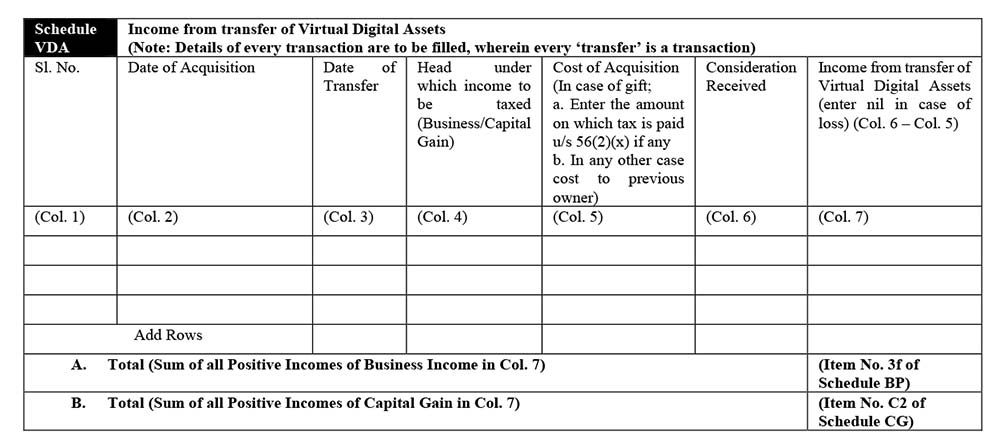

Schedule VDA

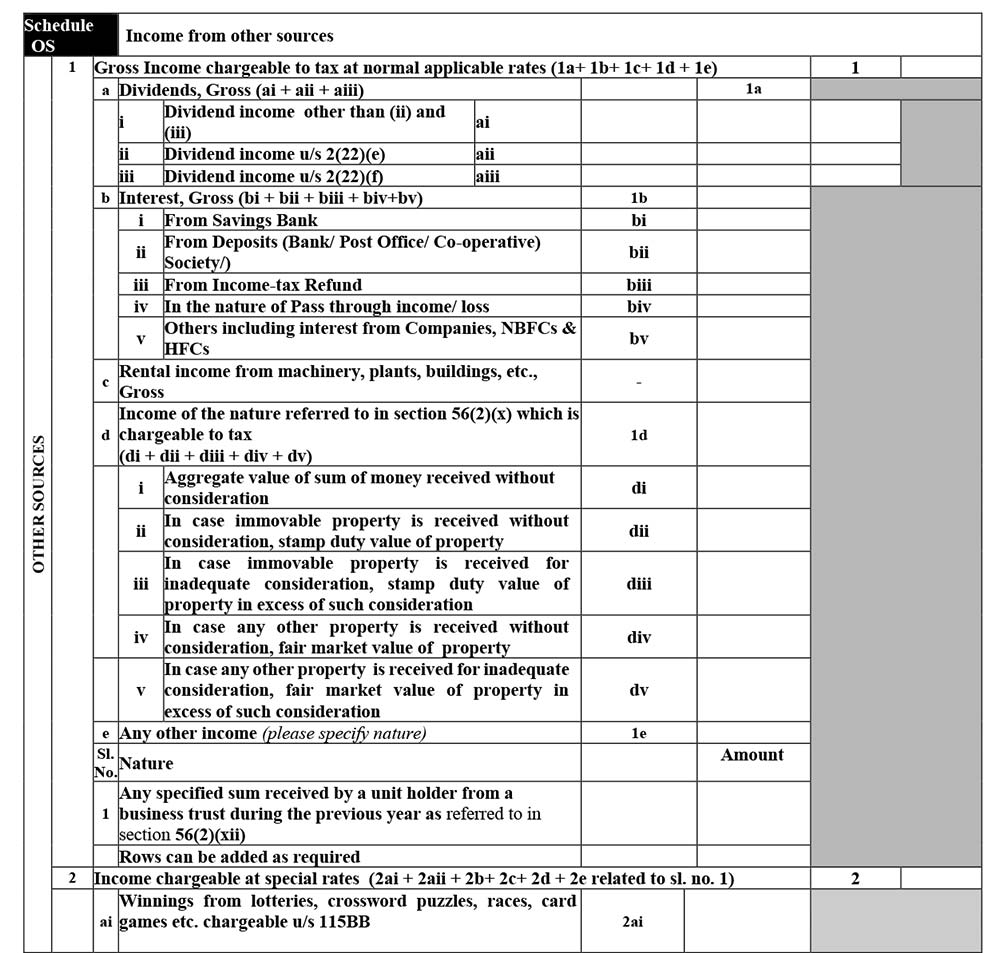

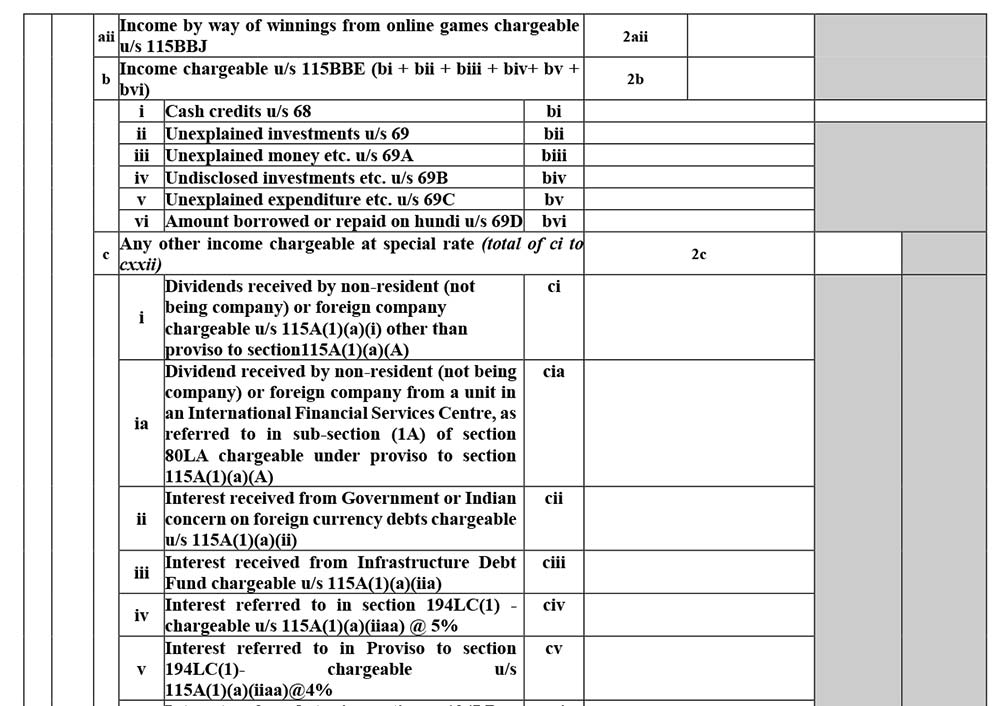

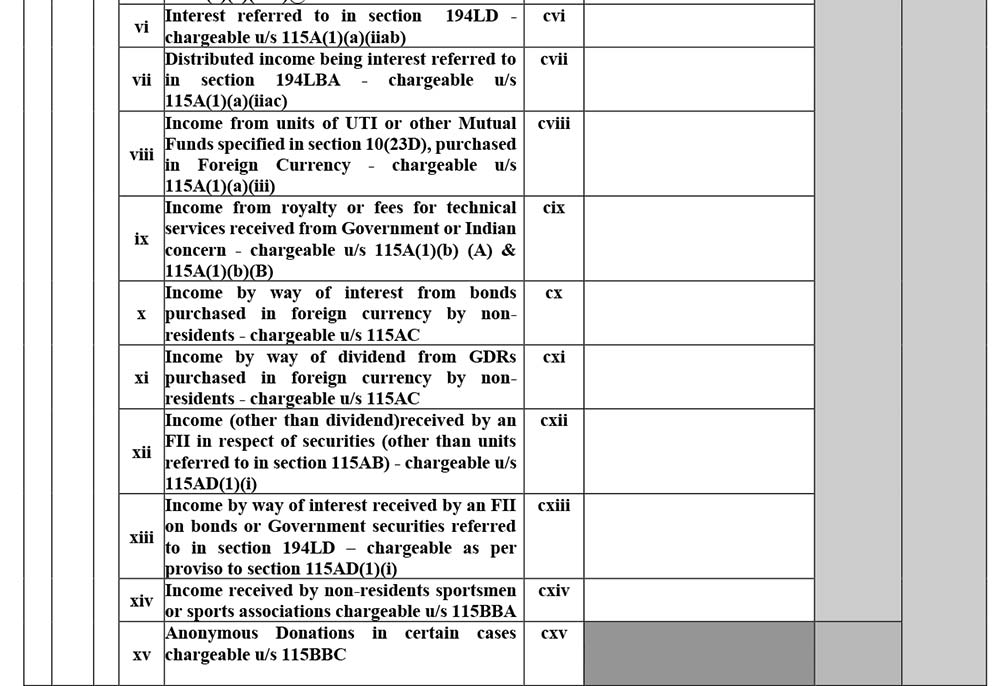

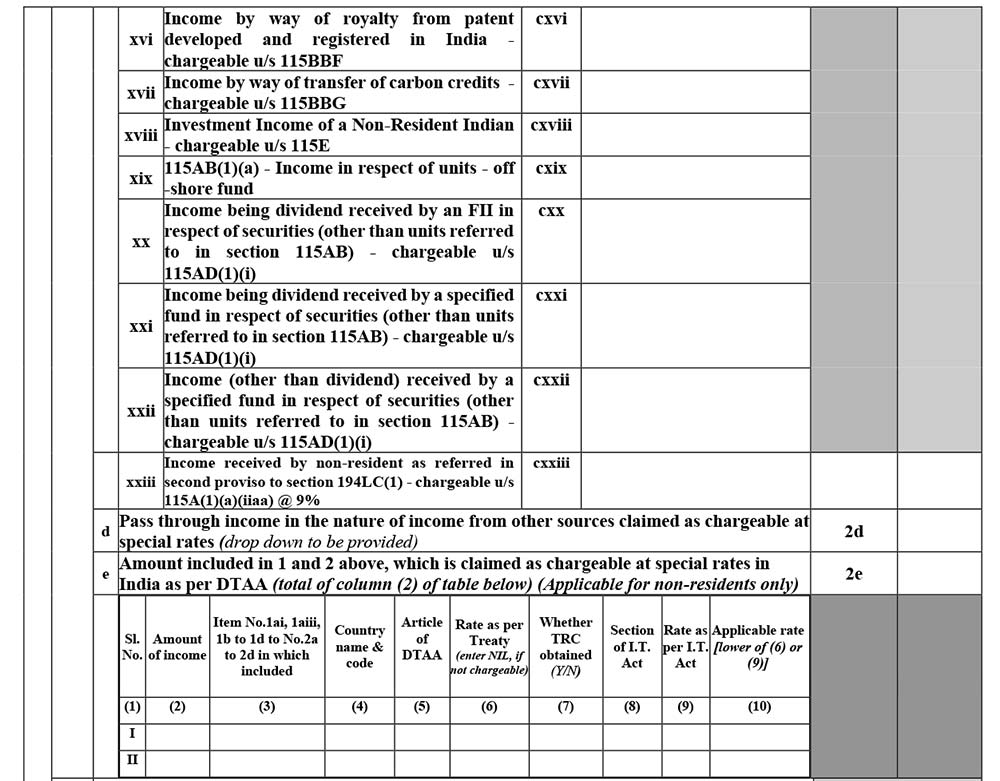

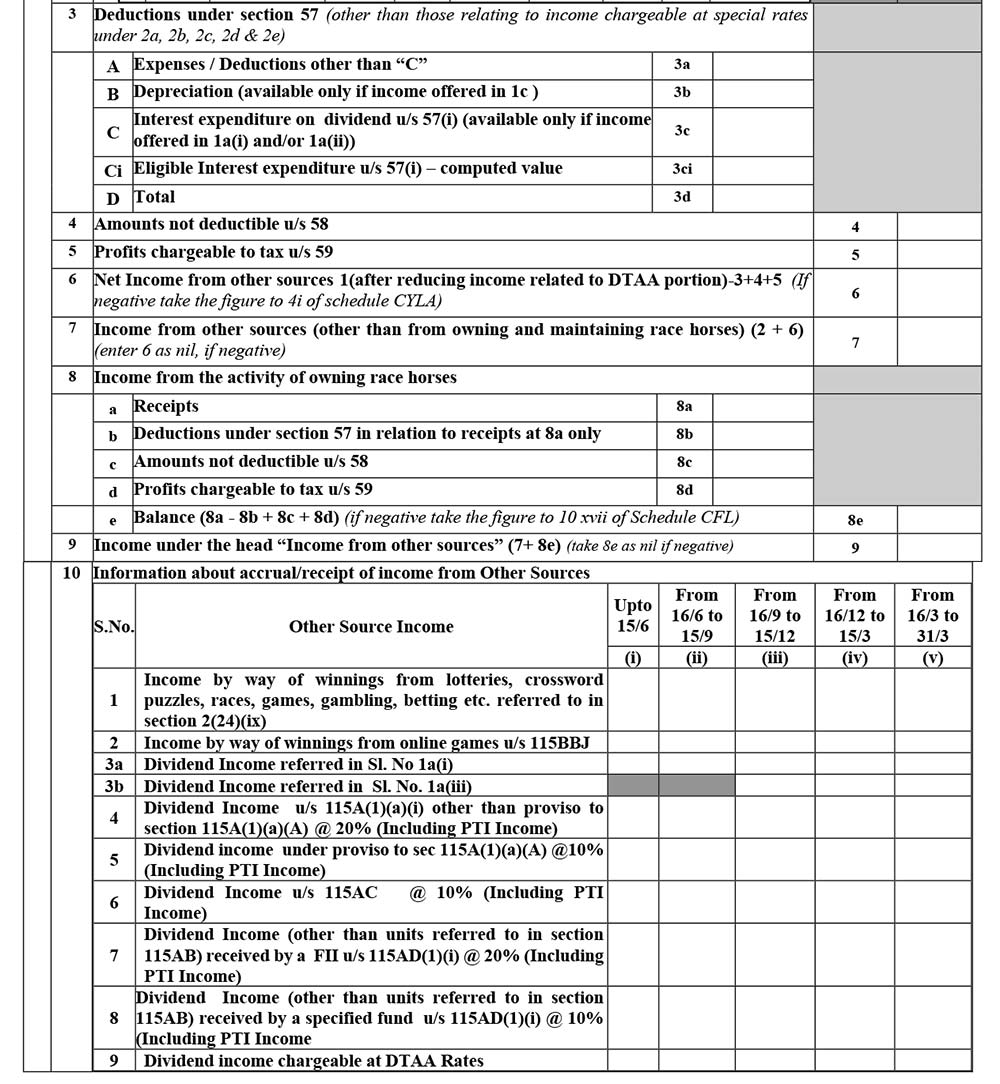

Schedule OS

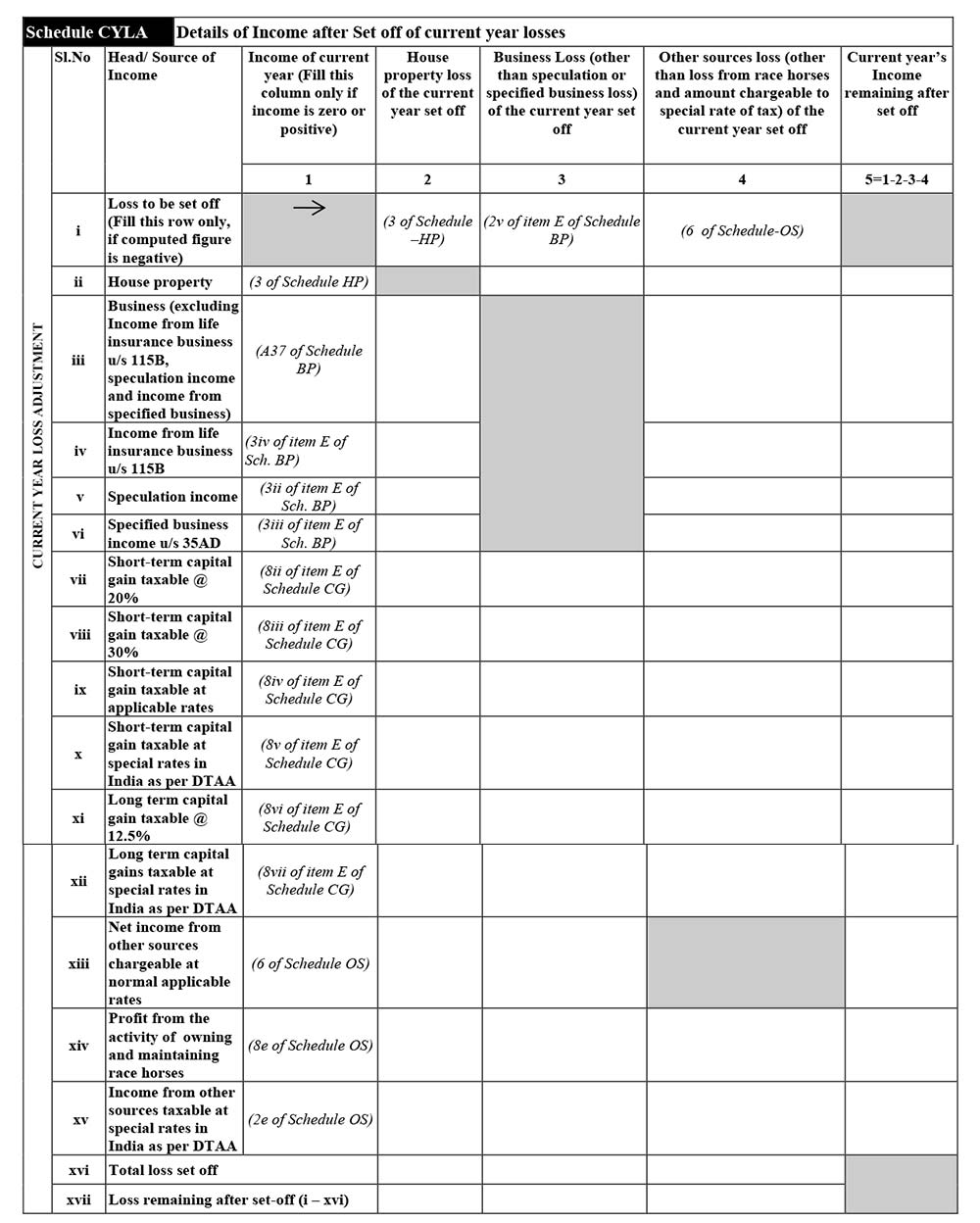

Schedule CLYA

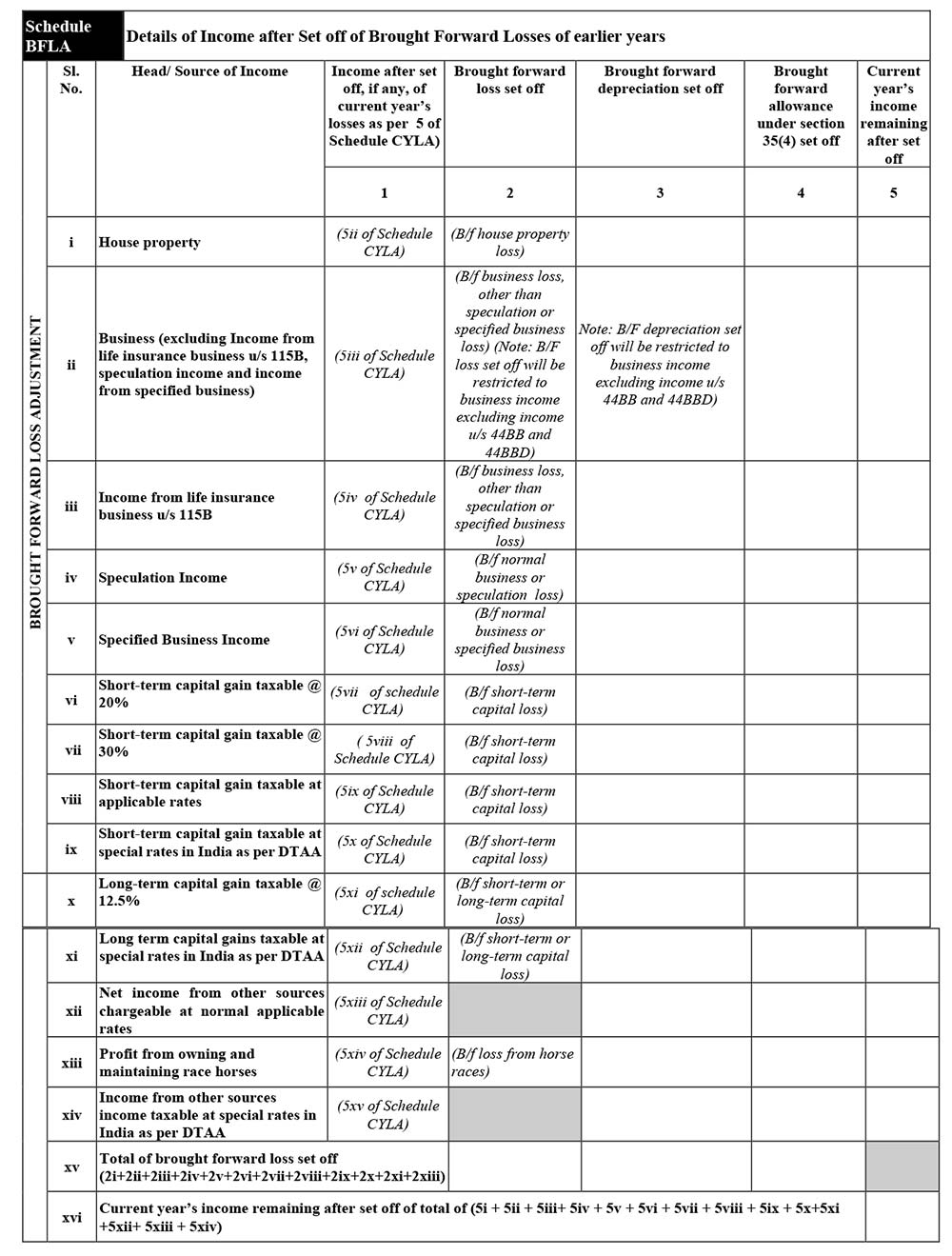

Schedule BFLA

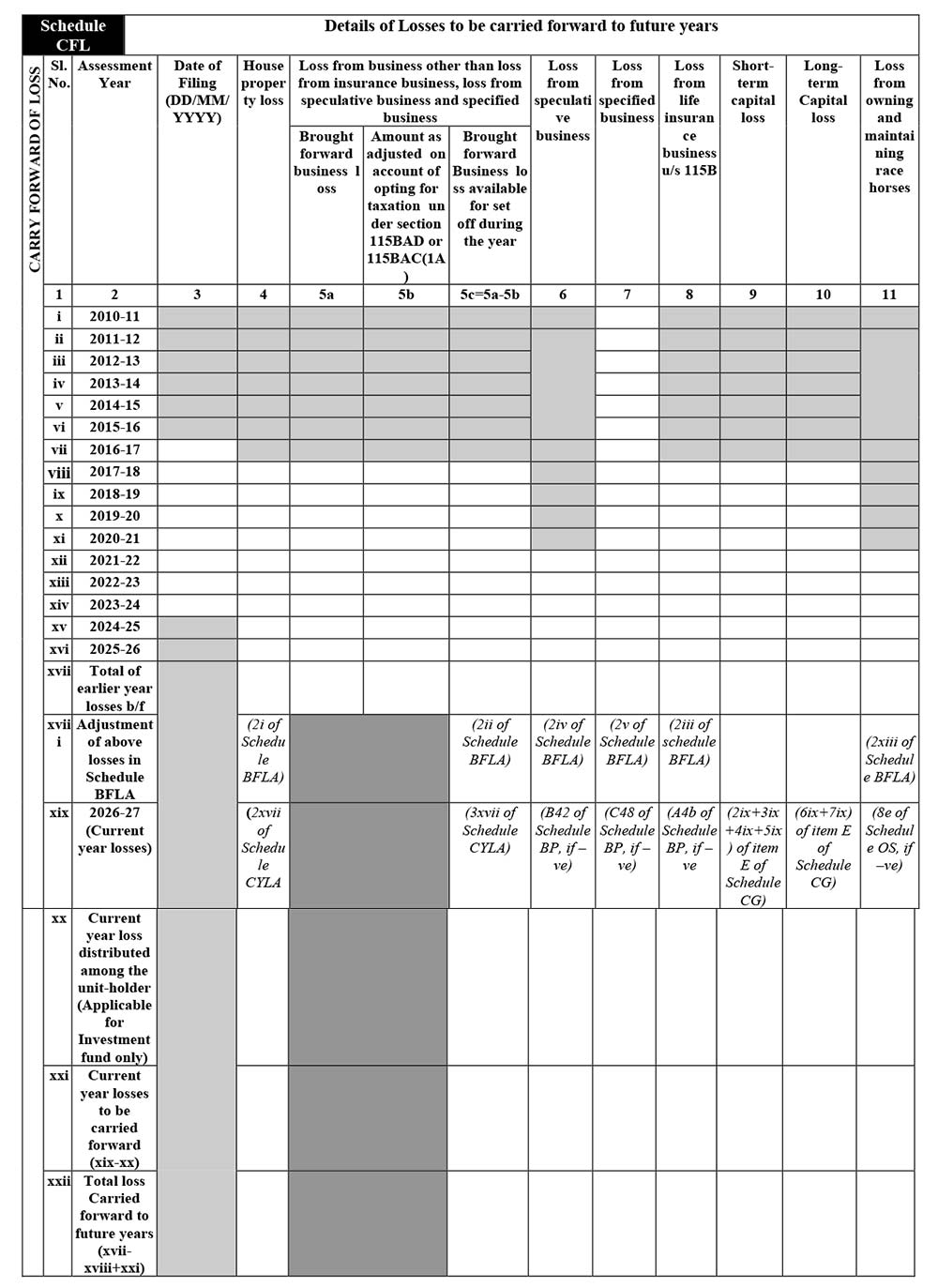

Schedule CLF

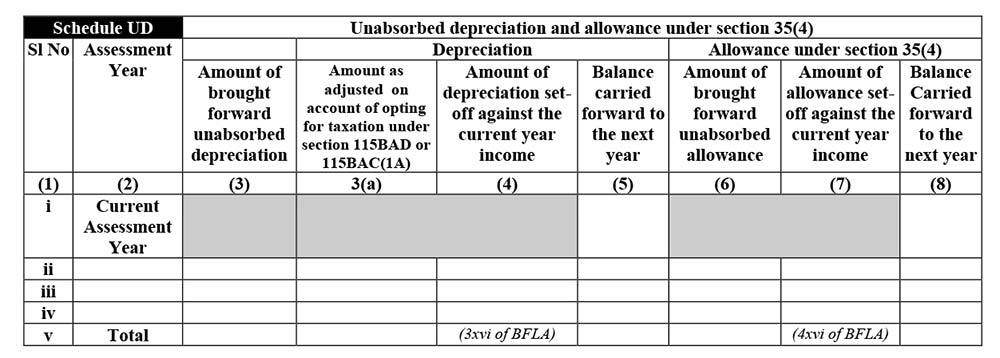

Schedule UD

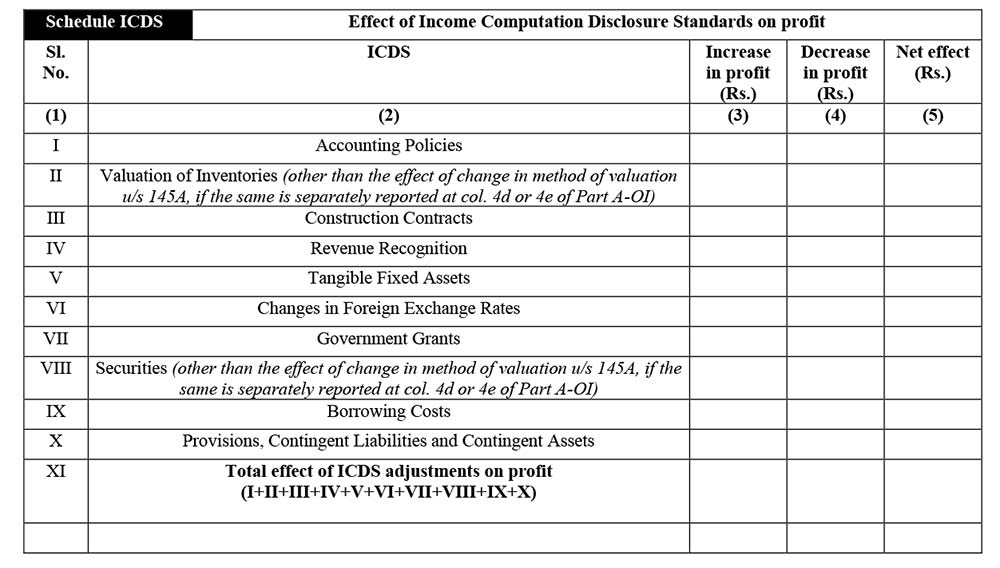

Schedule ICDS

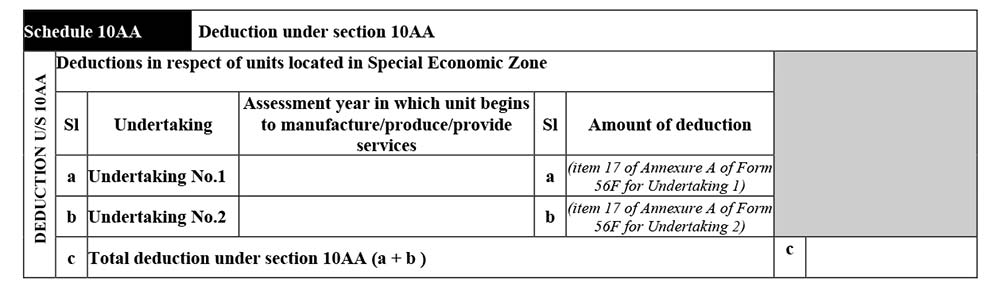

Schedule 10AA

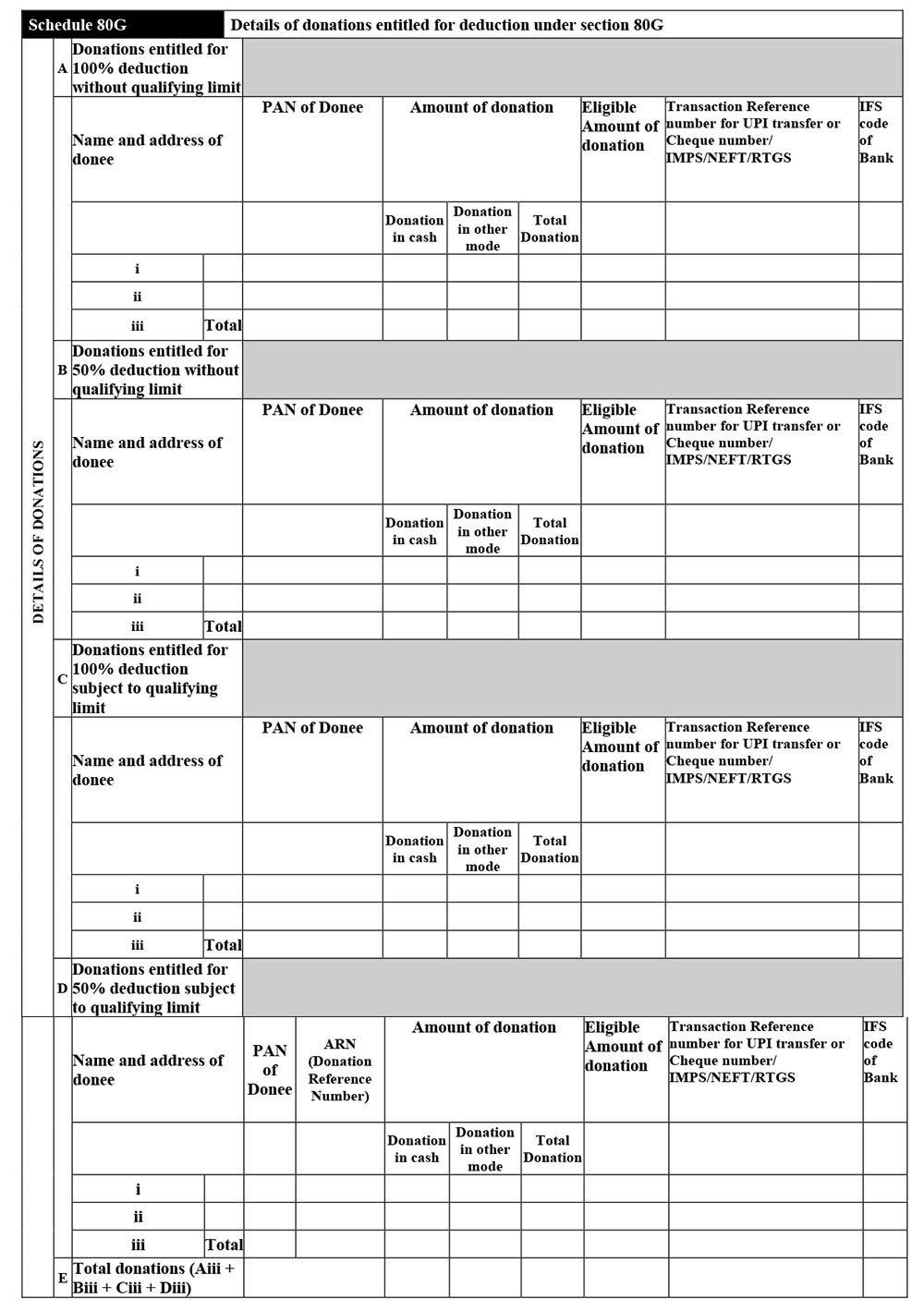

Schedule 80G

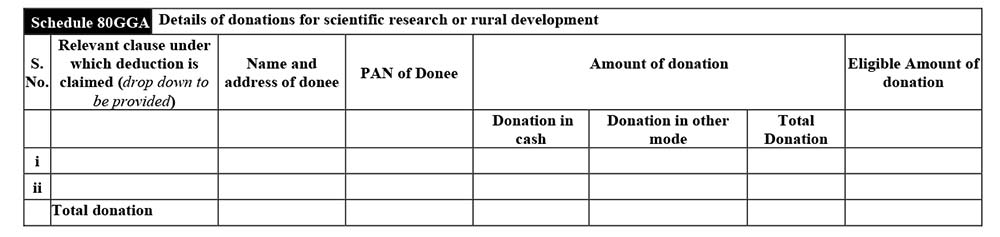

Schedule 80GGA

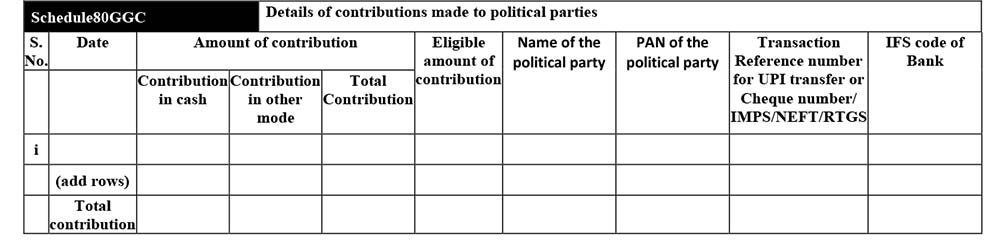

Schedule 80GGC

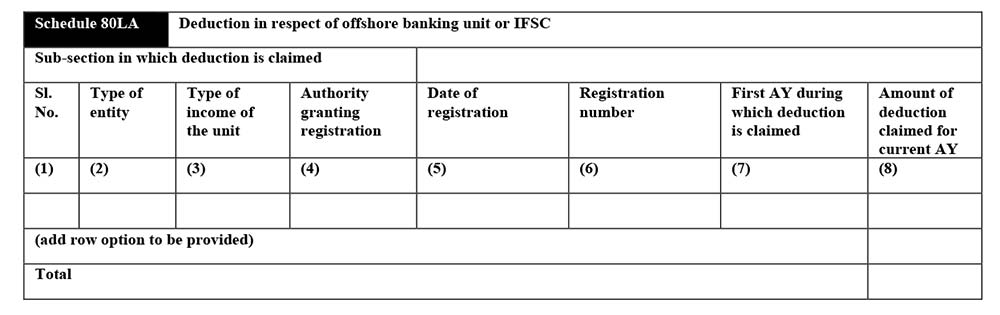

Schedule 80LA

Schedule 80ICA

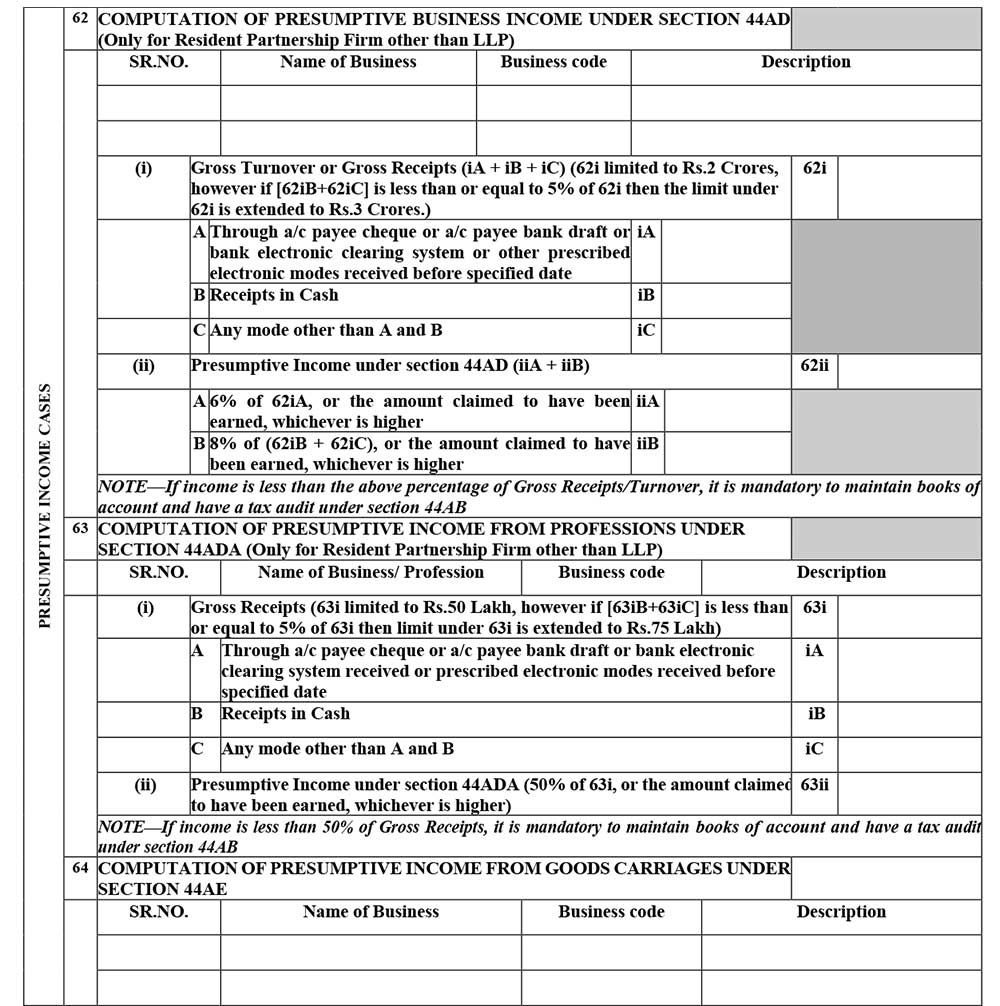

Schedule 80RA

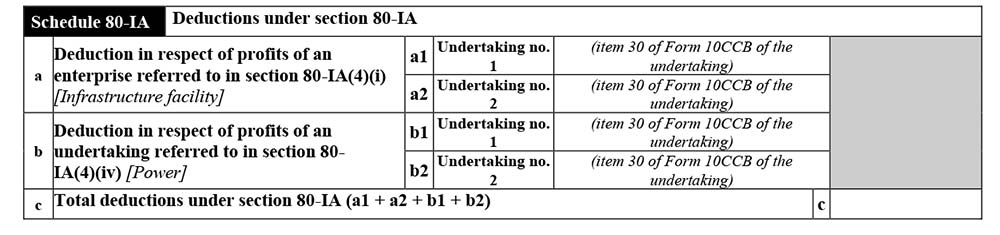

Schedule 80-IA

Schedule 80-IB

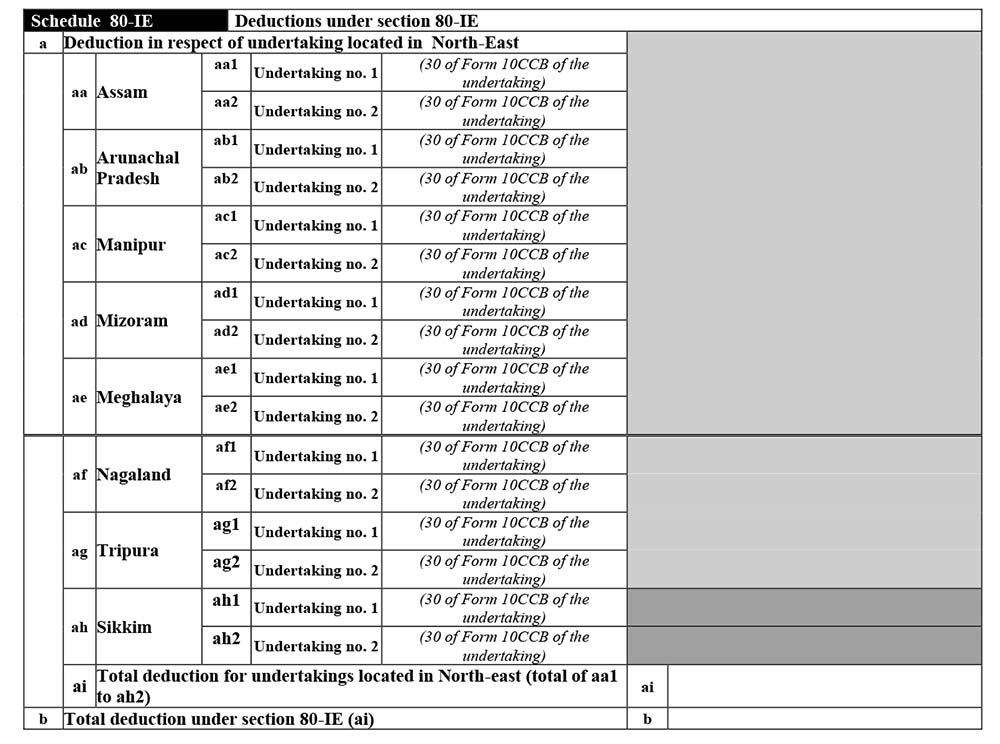

Schedule 80-IE

Schedule 80P

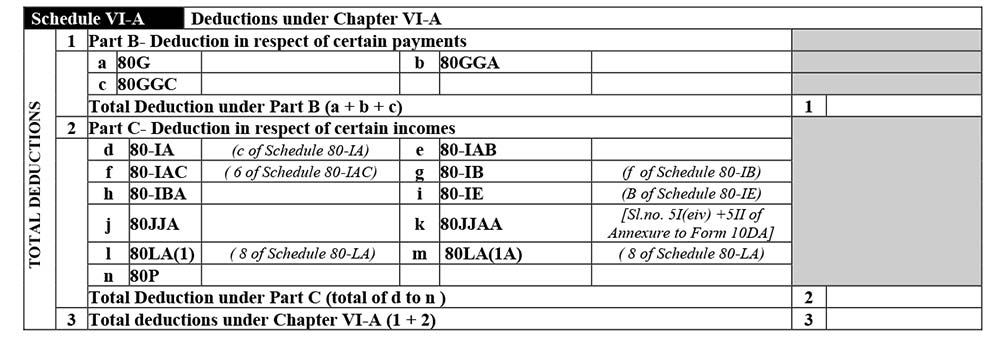

Schedule VI-A

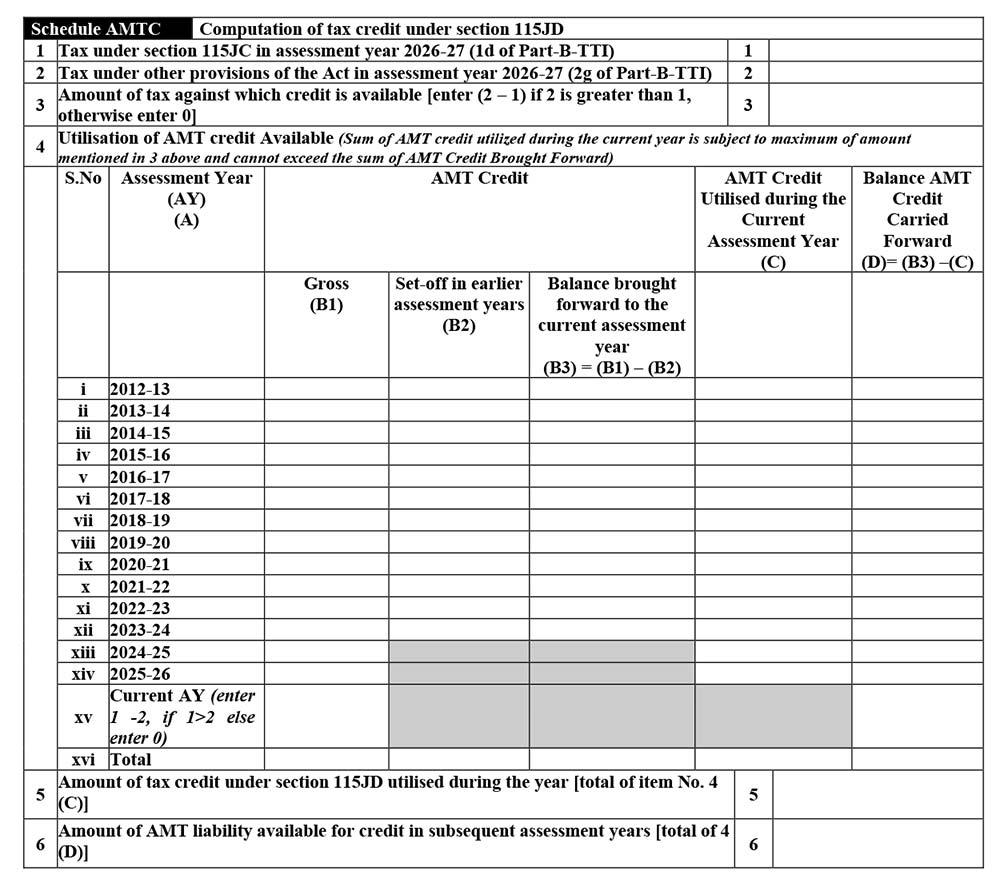

Schedule AMT

Schedule AMTC

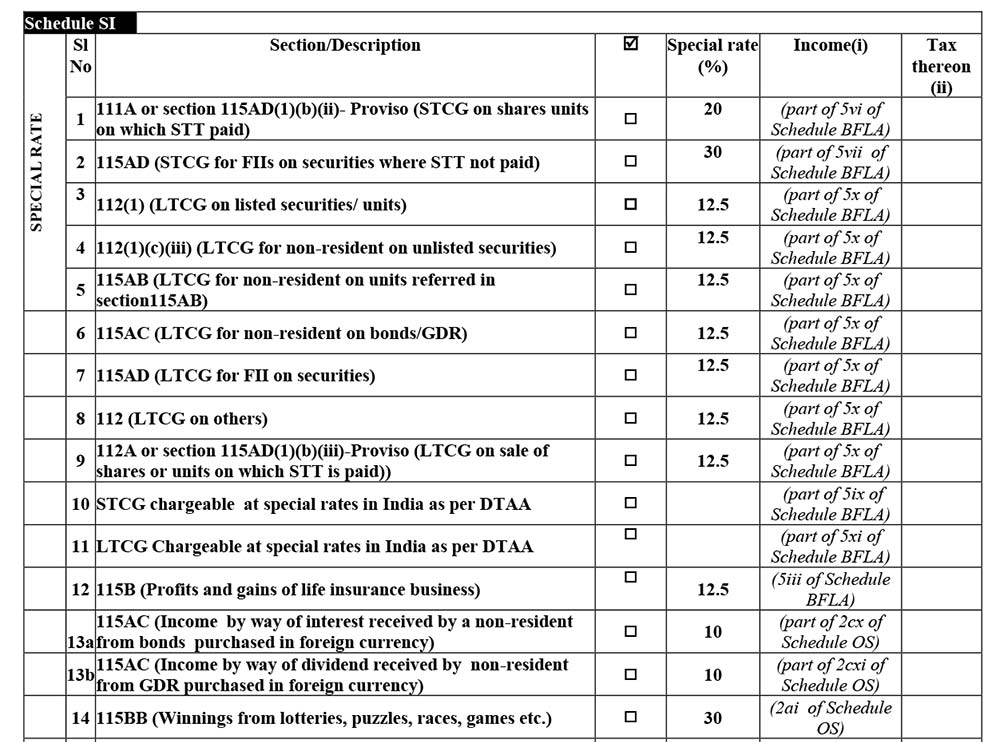

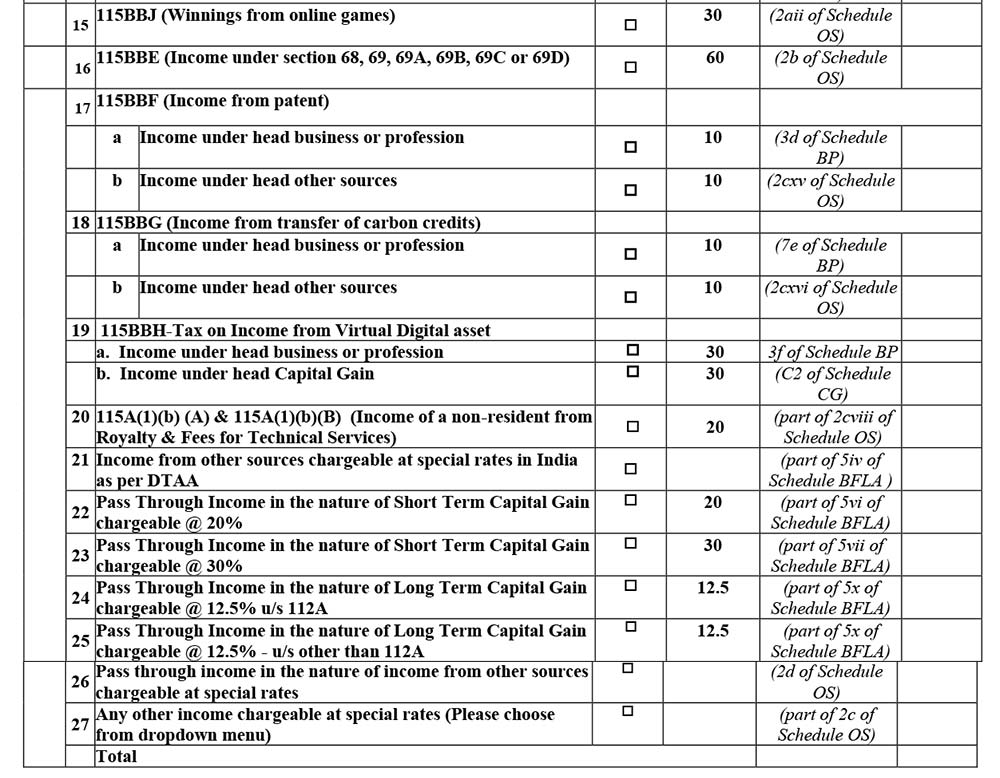

Schedule SI

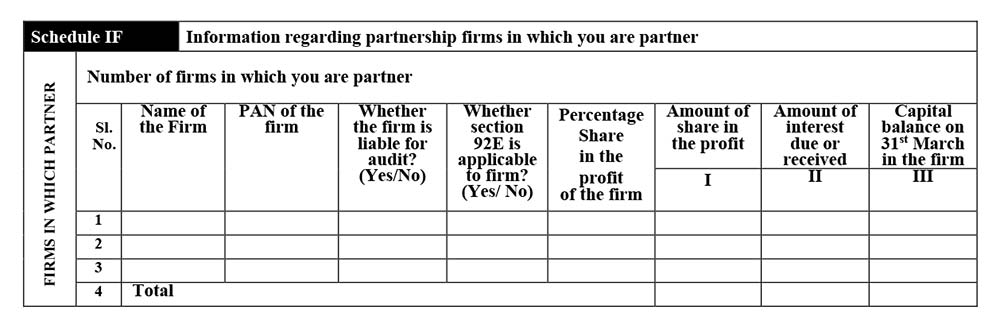

Schedule IF

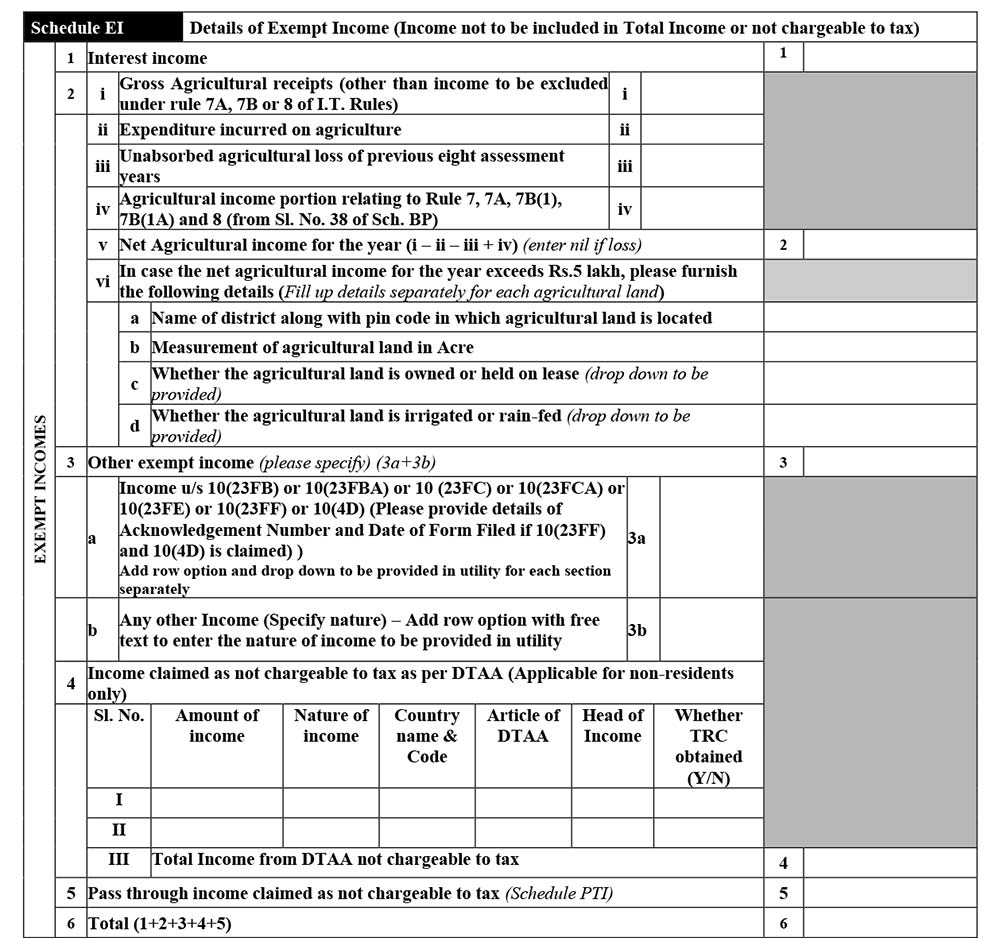

Schedule EI

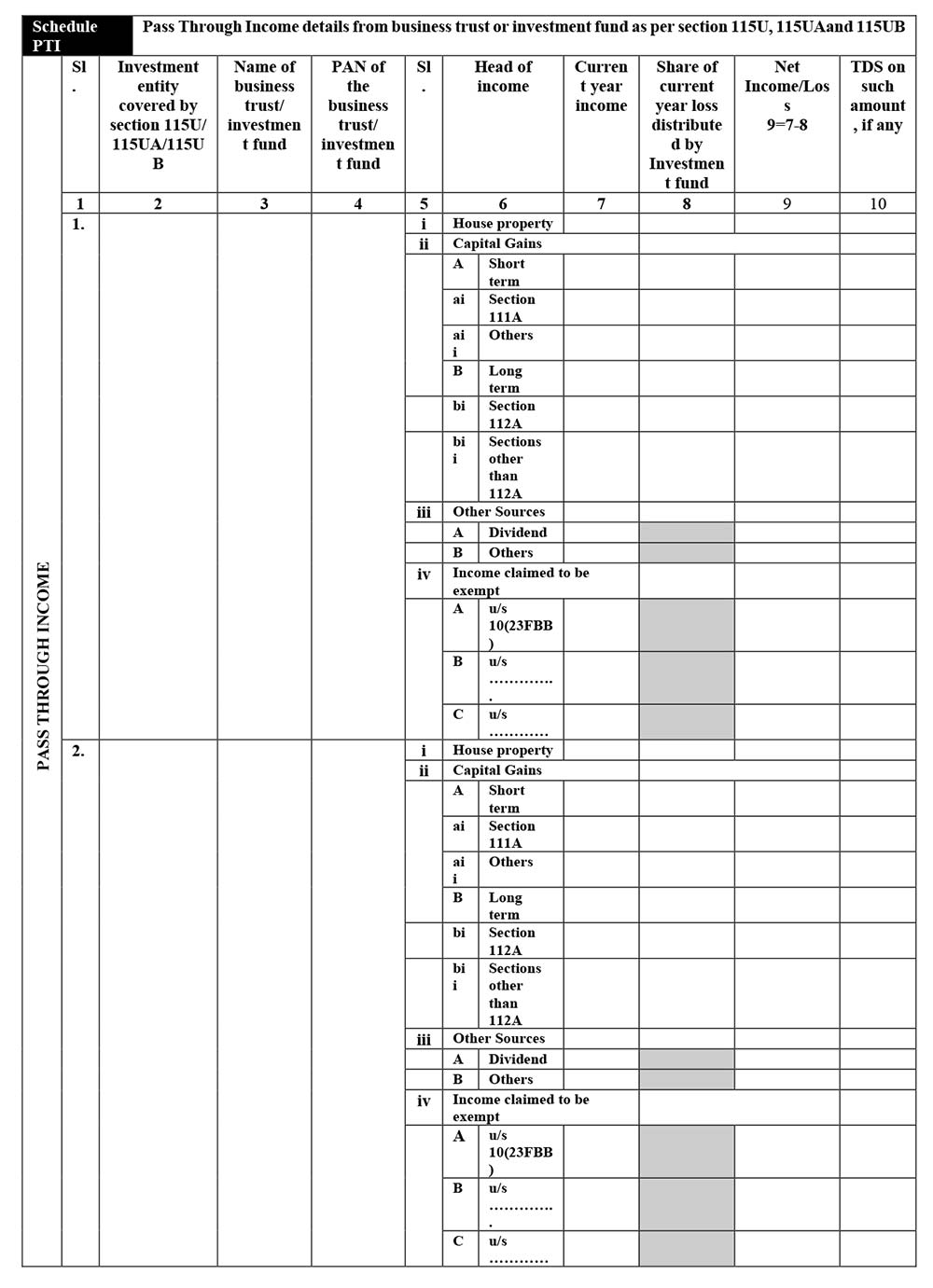

Schedule PTI

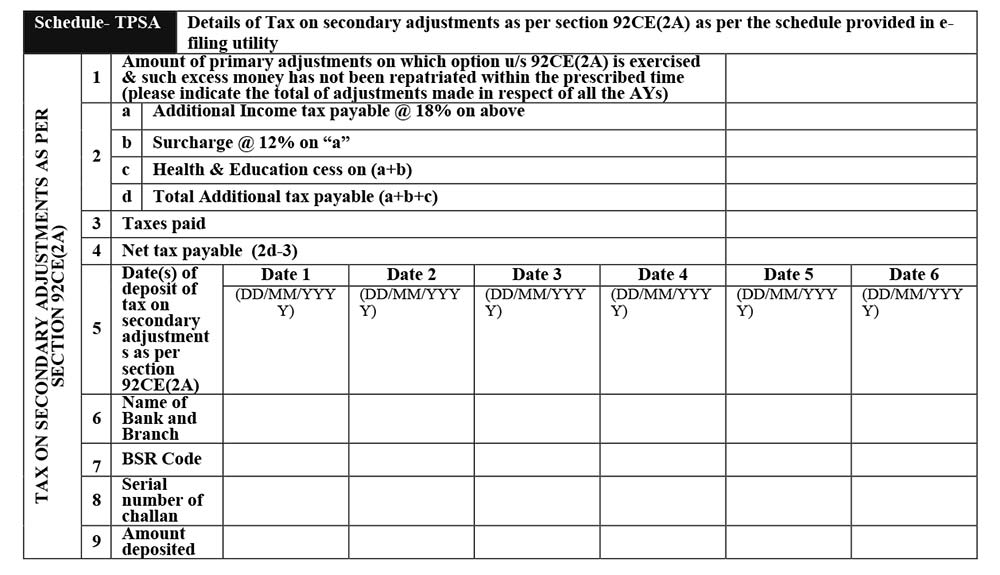

Schedule TPSA

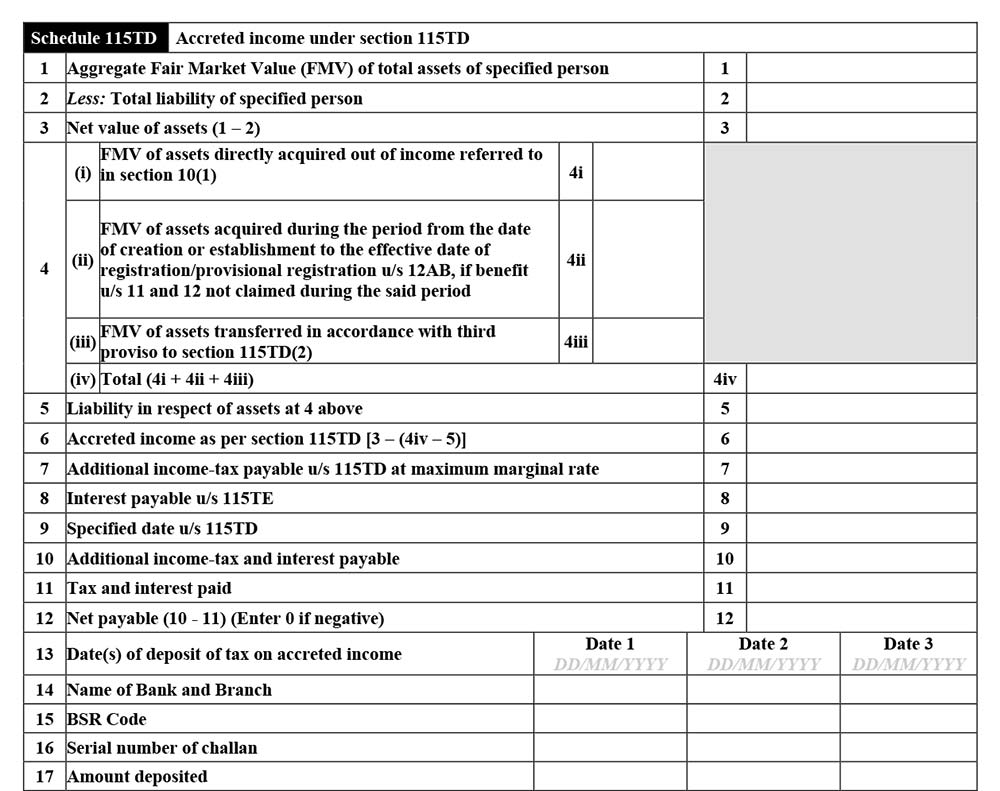

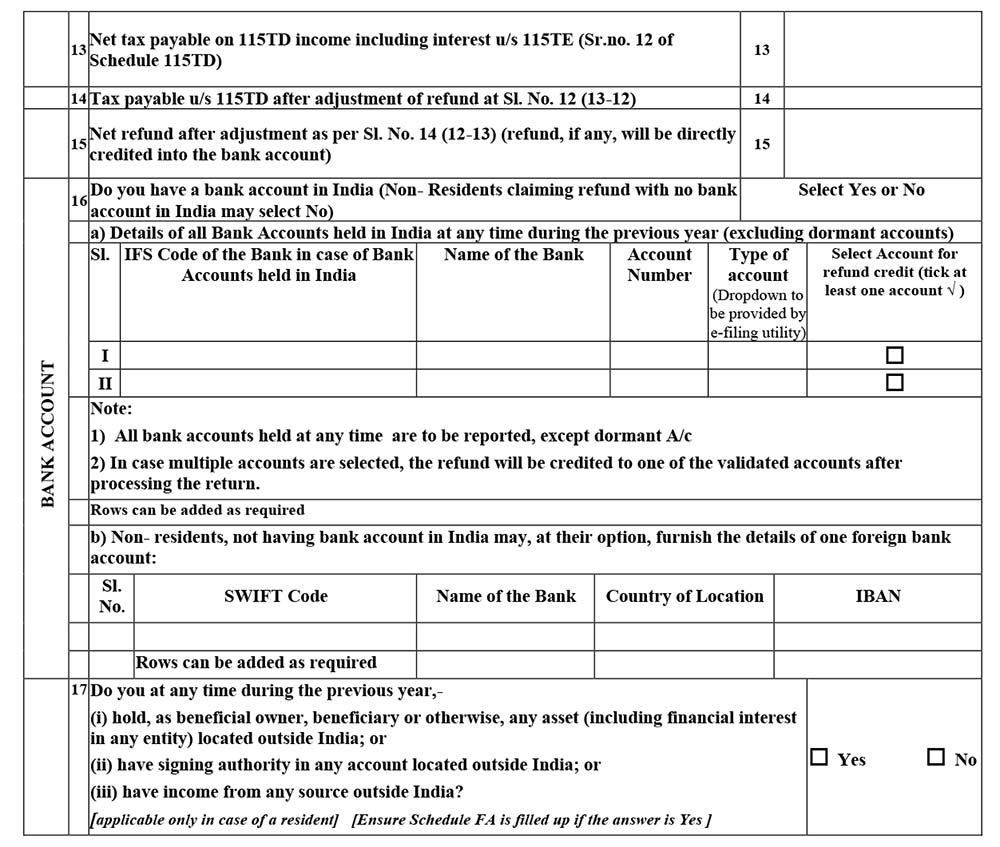

Schedule 115TD

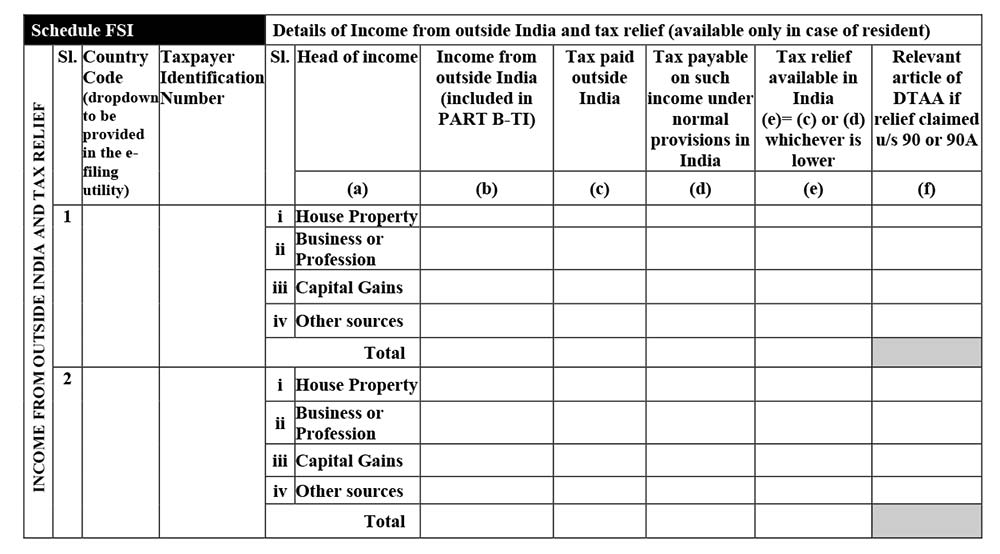

Schedule FSI

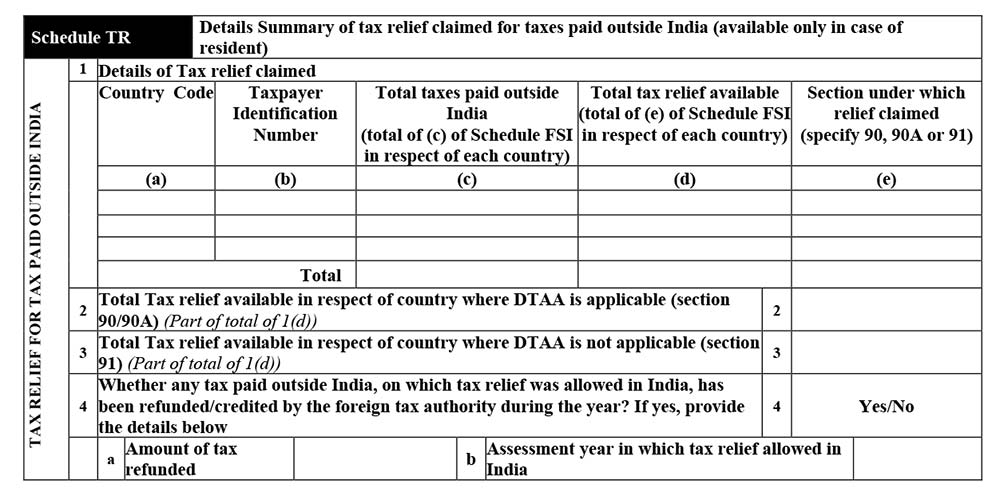

Schedule TR

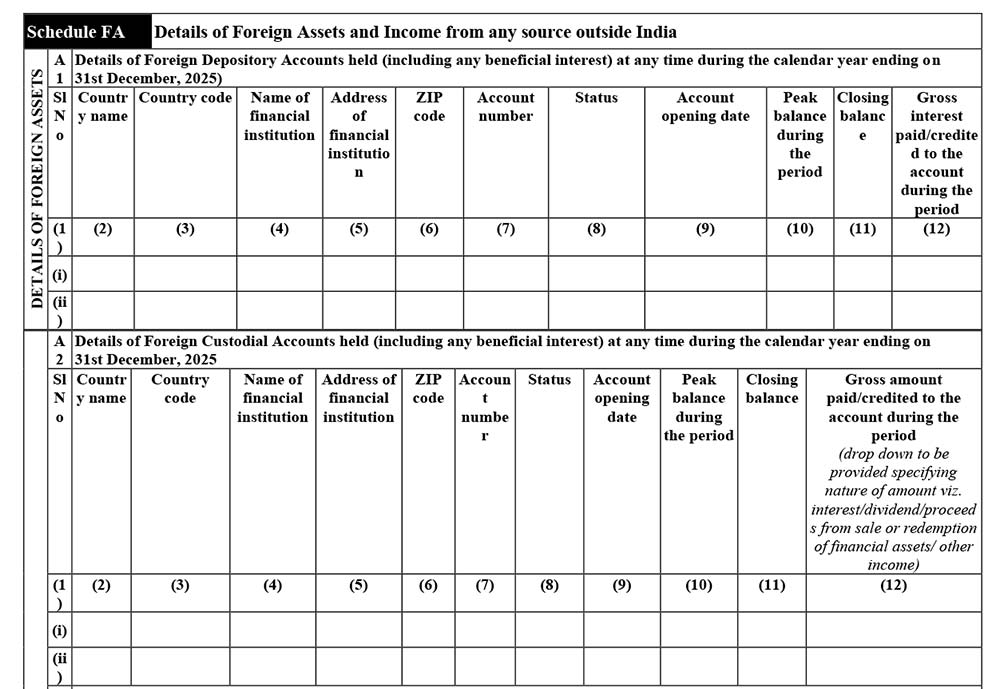

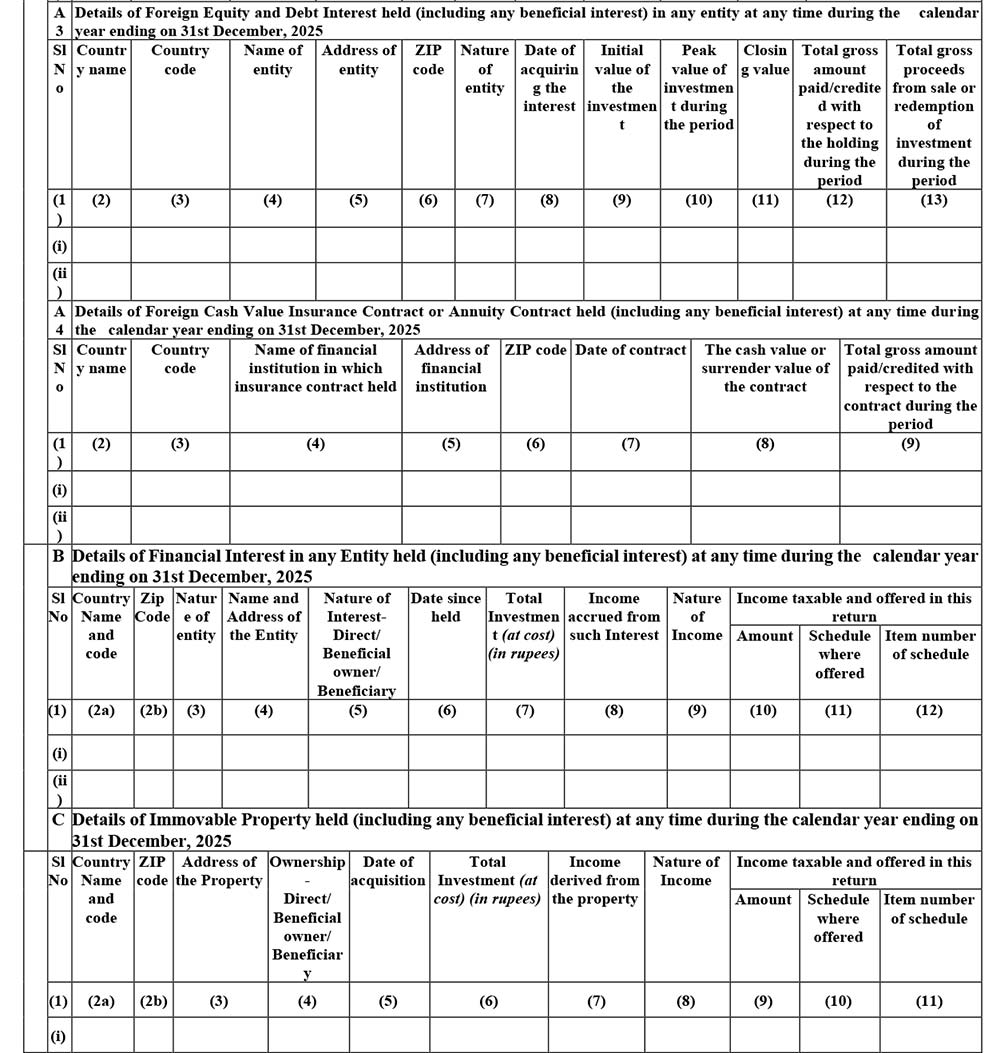

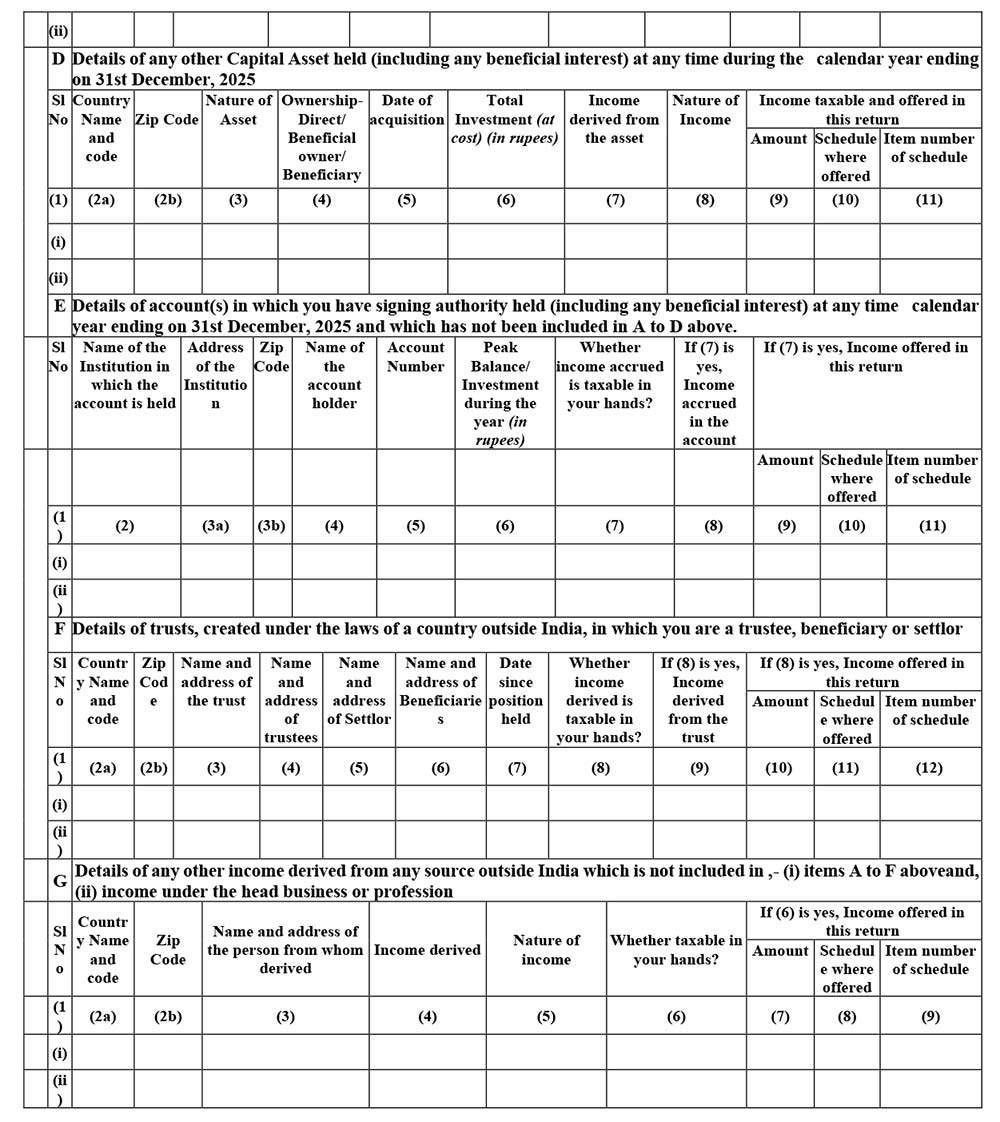

Schedule FA

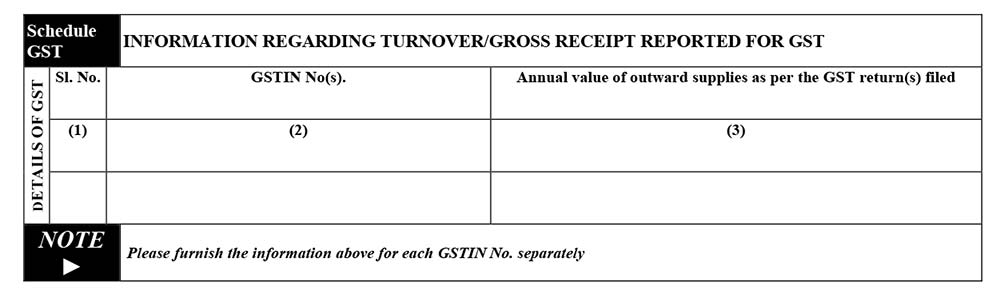

Schedule GST

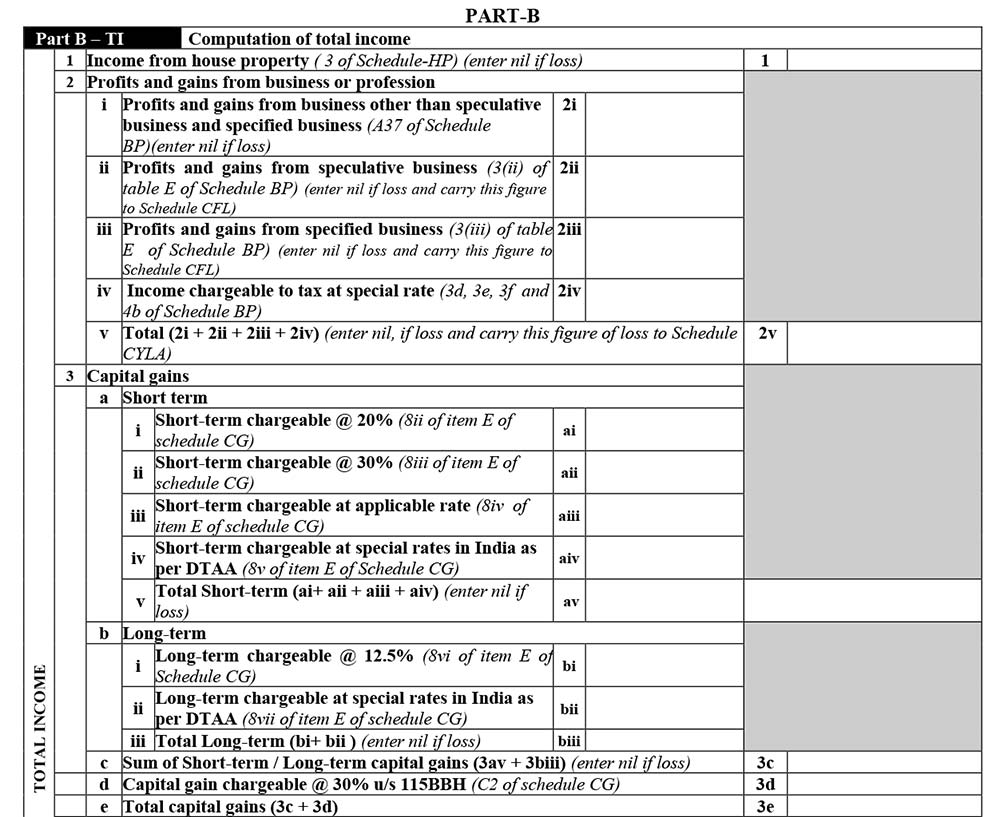

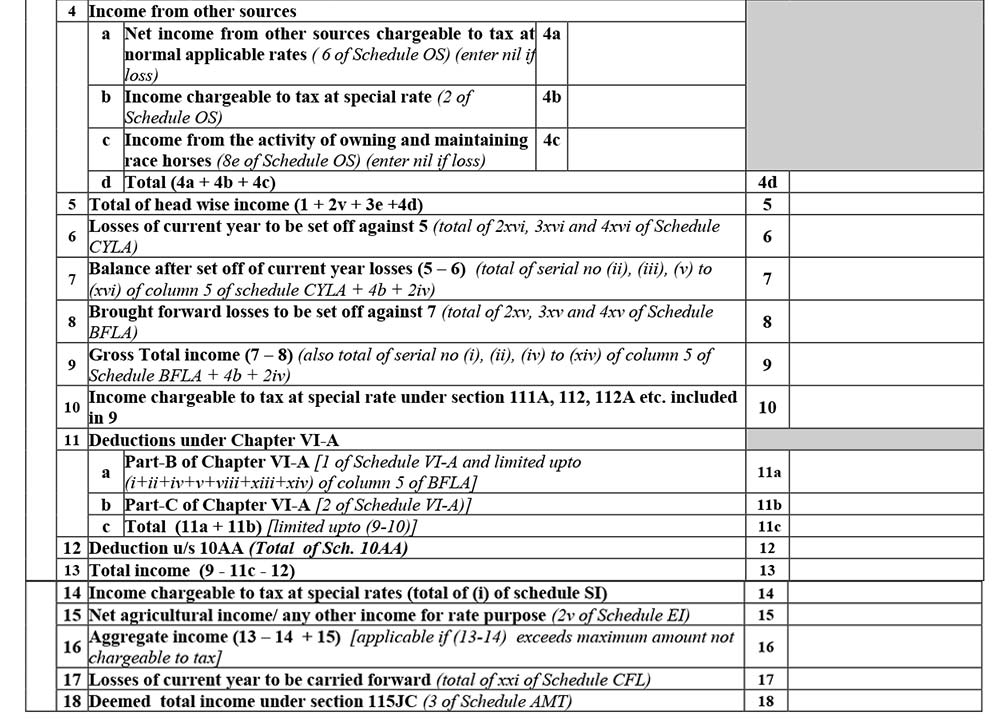

Part-B-TI

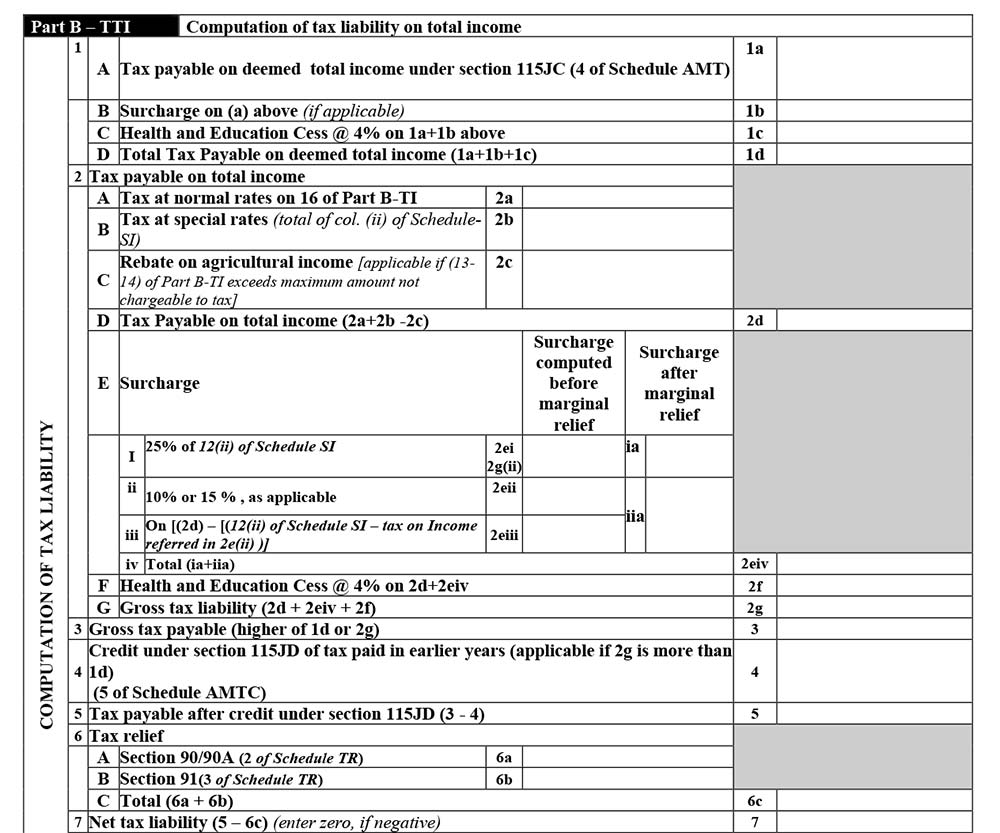

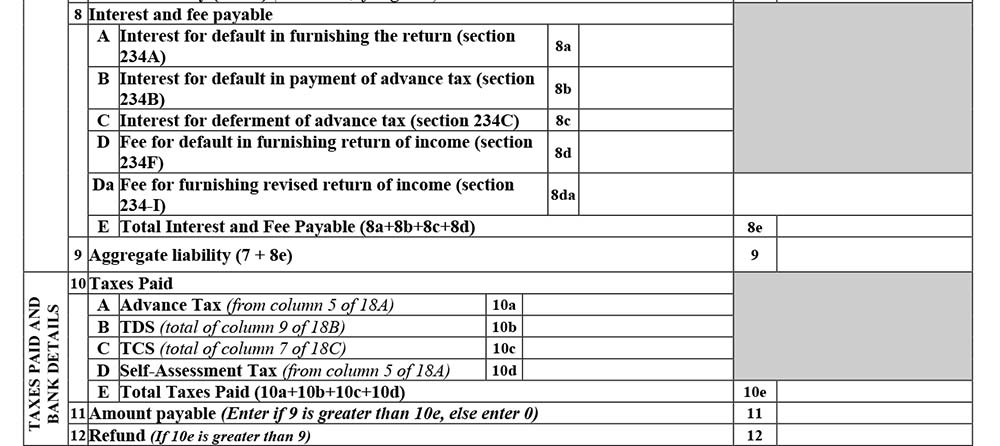

Part-B-TII

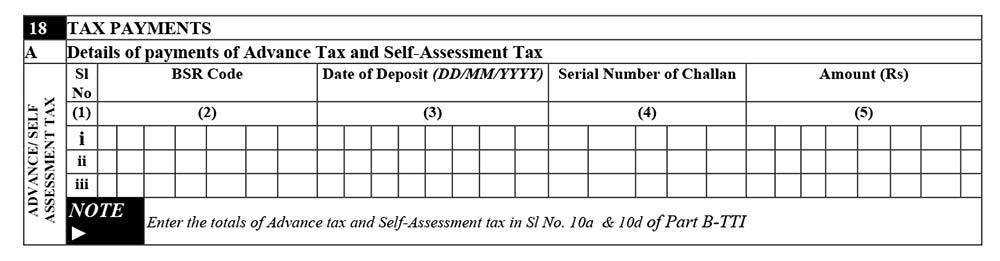

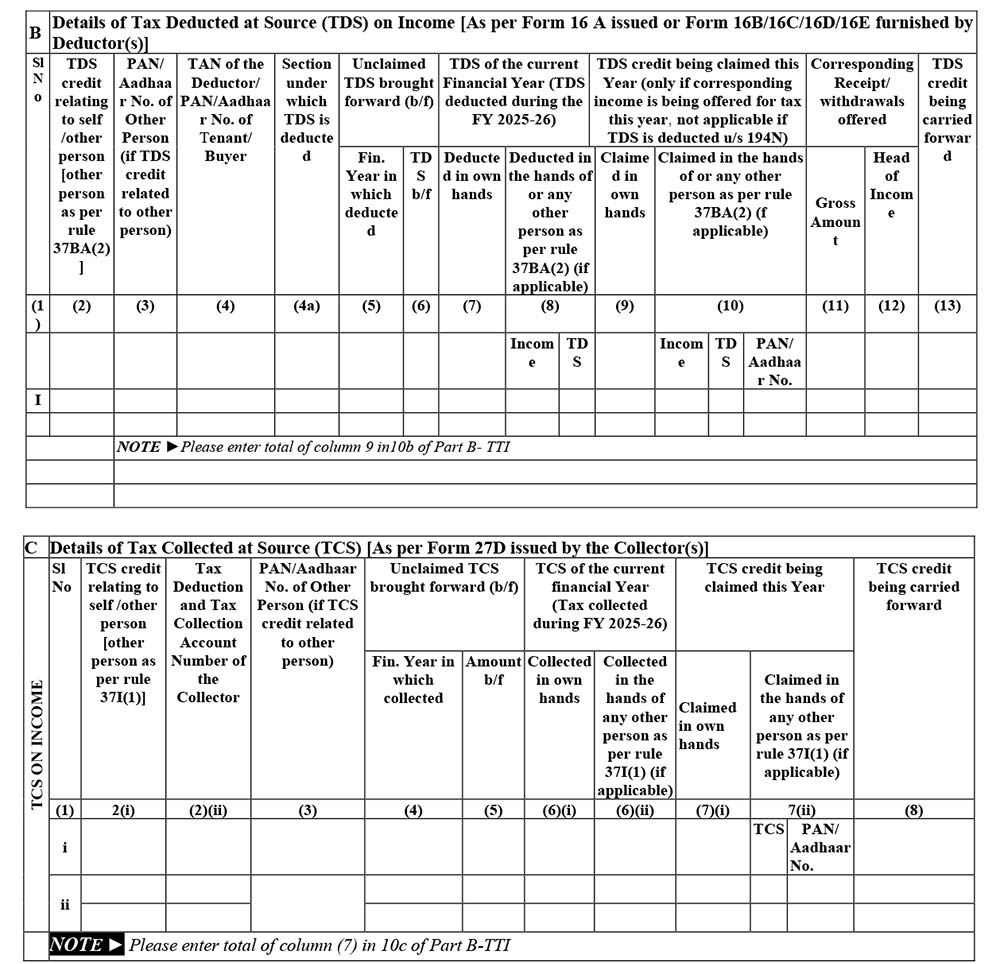

Tax Payment

Verification

There are many technical glitches in itr 5 utility for example audit turn less then one crores column answer is in protected sheet with secret code only CPC know the code

i am unable to validate the ITR-5 as because the loss shows is not equal to the loss of carried forward loss in BTI and CFL. The ITR-5 is filed as belated return where the loss may not be carried forward. pls help in getting the ITR-5 validated and varified before e varify and upload,