The ITR-3 Form can be filed by those Individuals and Hindu Undivided Families who earn income from a Proprietary business or by practising his/her profession. However, when an individual/HUF earns income as a partner of a partnership firm that is carrying out business/profession, he can file an ITR-3.

File ITR 3 Via Gen IT Software, Get Demo!

Latest Update

- Taxpayers can now download the first version of the Excel-based utility, JSON Schema, and validation for the ITR-3 form. Download Now

ITR 3 Filing Start Date for Tax Professionals

The online filing of ITR-3 is now live on the Income Tax portal from 18th June 2026. Taxpayers can download the latest versions of the utility, schema, and validation tools for Form ITR-3.

Who is Not Eligible to File the ITR-3 Form?

Individuals and HUF who don’t have income from business or profession.

When Should ITR 3 be Filed?

- ITR-3 form is filed when the assessee earns income which falls into the below-mentioned category:

- Income earned from Proprietary Business

- Income gained by conducting a profession

- A person who is Partners in a Firm.

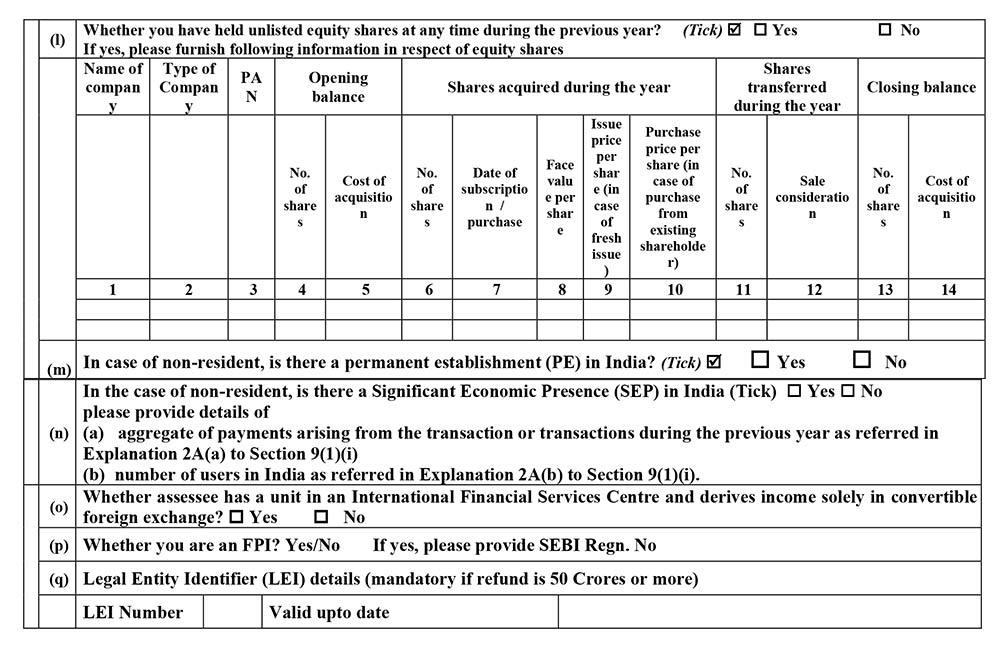

- Individuals who are Directors in a company or who hold unlisted equity shares to file ITR-3

- Income from House property

- ITR-3 is also needed to be filed by a person whose income is chargeable to tax under “profits and gains of business or profession” like, interest, salary, bonus, commission or remuneration.

What is the Due Date for Filing ITR 3 Form?

The due date for filing an income tax return is as follows for individuals and businesses:

| Annual Year | For Non-audit Cases | For Audit Cases |

|---|---|---|

| AY 2026-27 | 31st August 2026 | 31st October 2026 |

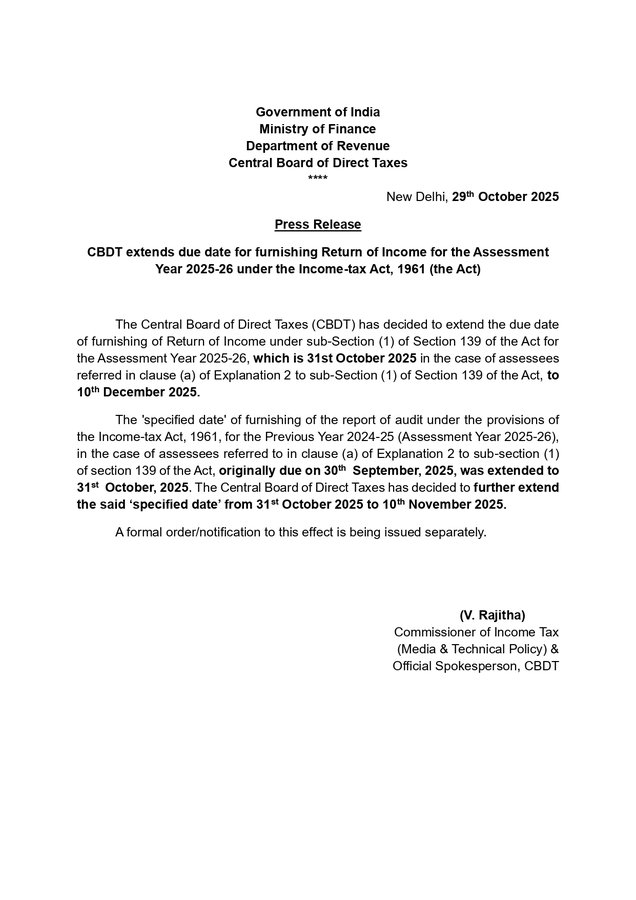

| AY 2025-26 | 31st July 2025( Revised till 16th September 2025, Read Press Release) | 10th December 2025 (Revised) Read PR |

| AY 2024-25 | 31st July 2024 | 31st October 2024 (Revised till 15th November 2024, Read Circular) |

| AY 2023-24 | 31st July 2023 | 31st October 2023 |

What are the Different Methods of Filing ITR-3 Form?

There are the following three methods for filing the Income Tax Return ITR-3 Form:

- By filing a return electronically under a digital signature. (Assesses who need to obtain a tax audit must use this method)

- By conveying the data in ITR-3 form electronically under an electronic verification code.

- By transmitting the data in ITR-3 form electronically, followed by the submission of the return verification in

- Return Form ITR-V to the Income Tax Office via mail. (Taxpayer filing ITR-3 form using this method must complete the acknowledgement in ITR-V.)

Read Also: Complete Process of Filing ITR 1 Online

How an Acknowledgement in ITR-V is Filed Out?

After furnishing all the necessary details, the assessee should print out two copies of Form ITR-V (verification). One copy of ITR-V, properly signed by the assessee, has to be posted to Post Bag No. 1, Electronic City Office, Bengaluru–560100 (Karnataka). The other copy can be retained by the assessee for his record.

Note: ITR-3 form corrigendum via Notification No. 59/2026. Read More

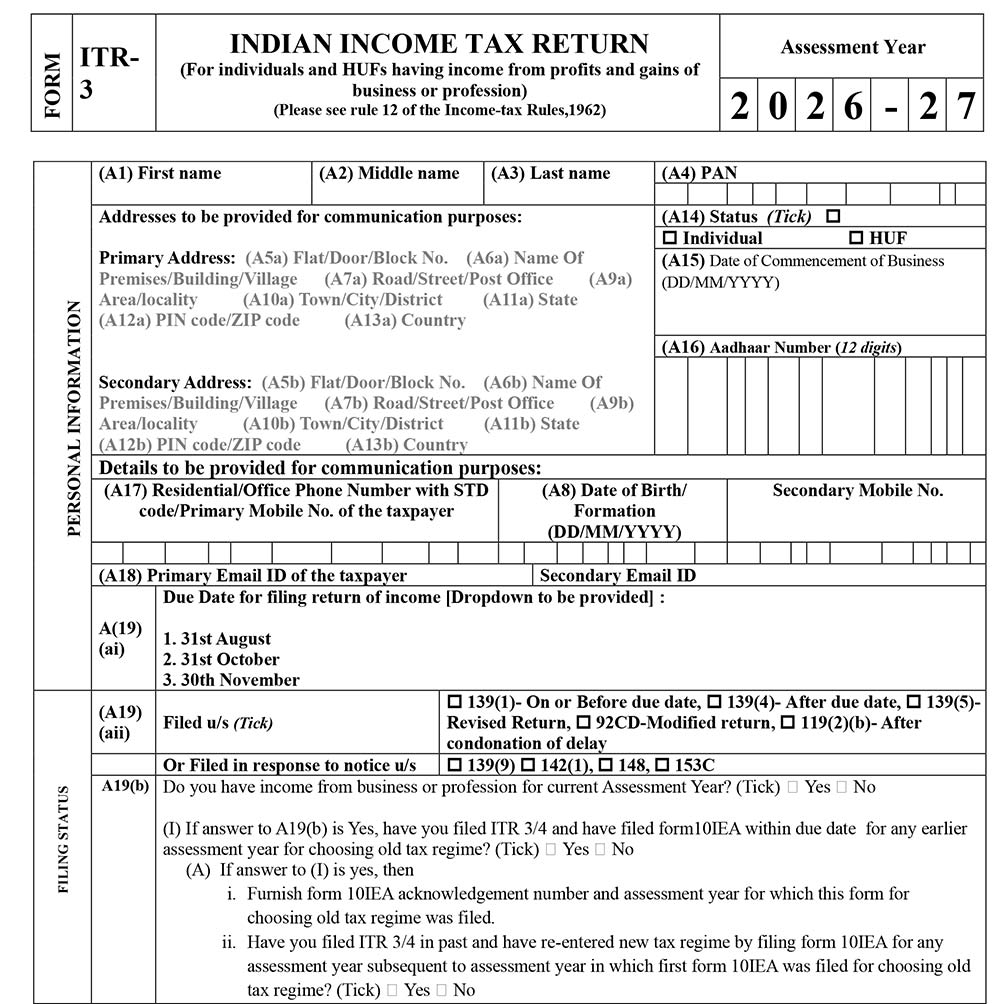

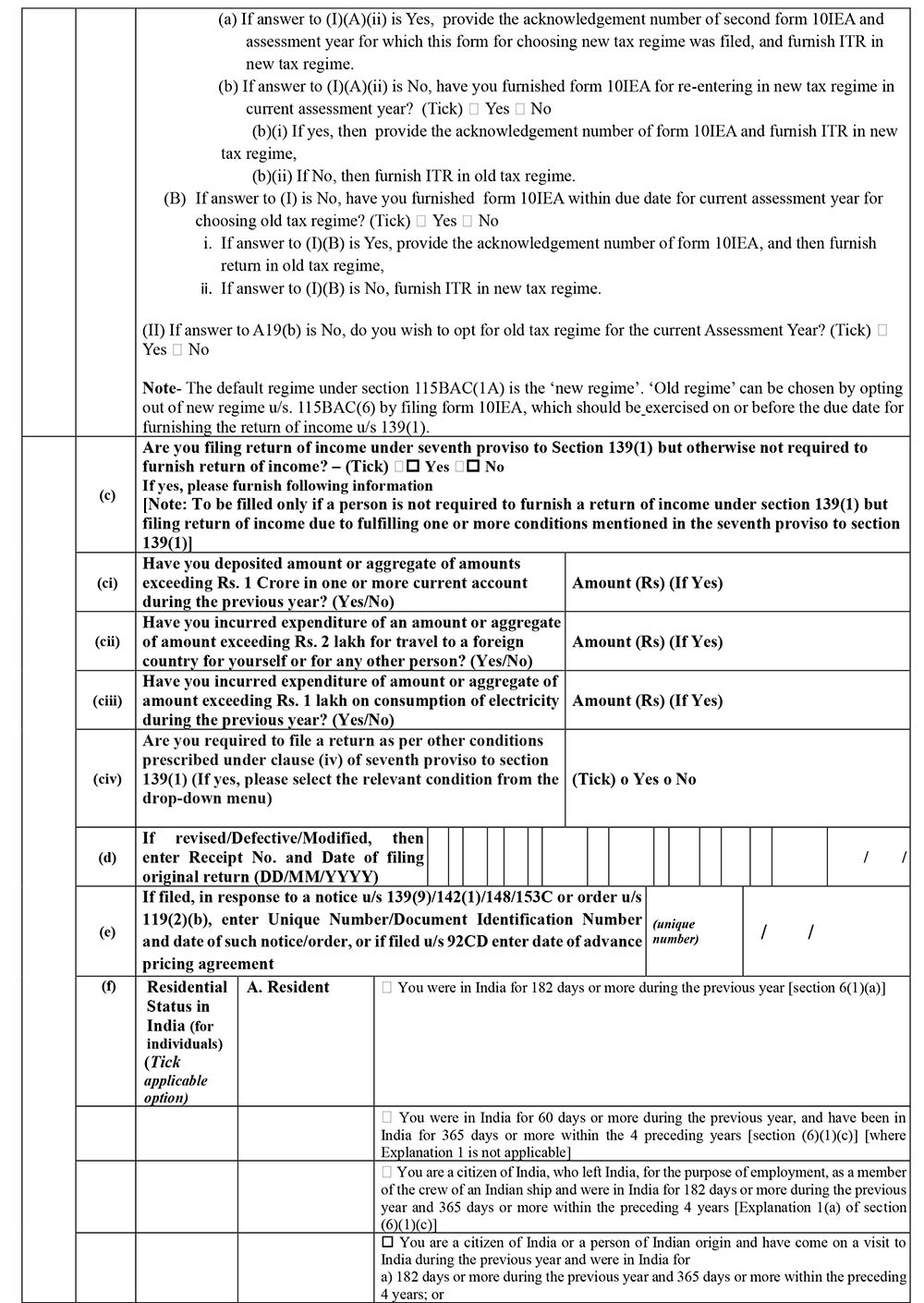

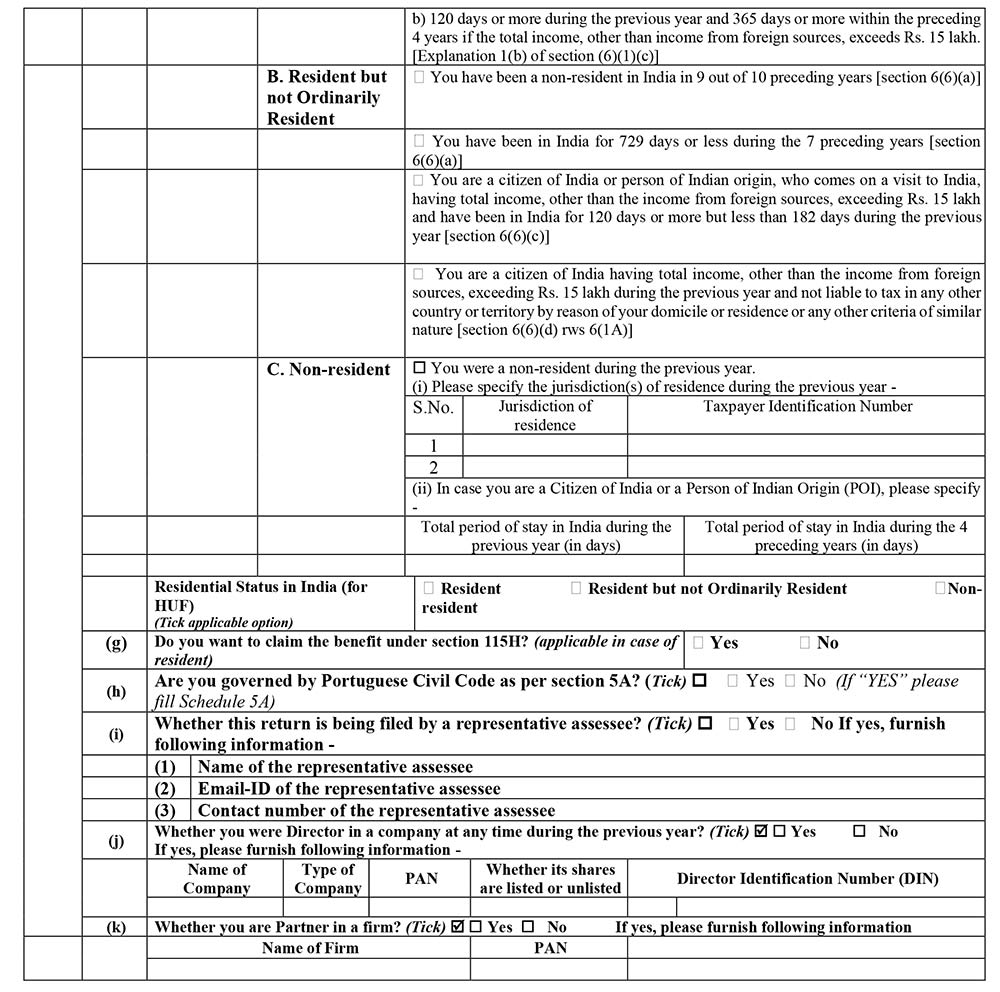

Step-by-Step Process to File ITR 3 Online for AY 2026-27

Part A – GEN General

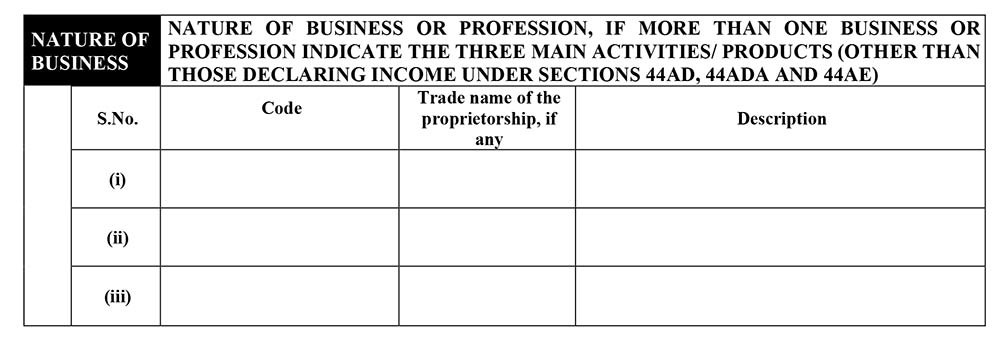

Nature of Business

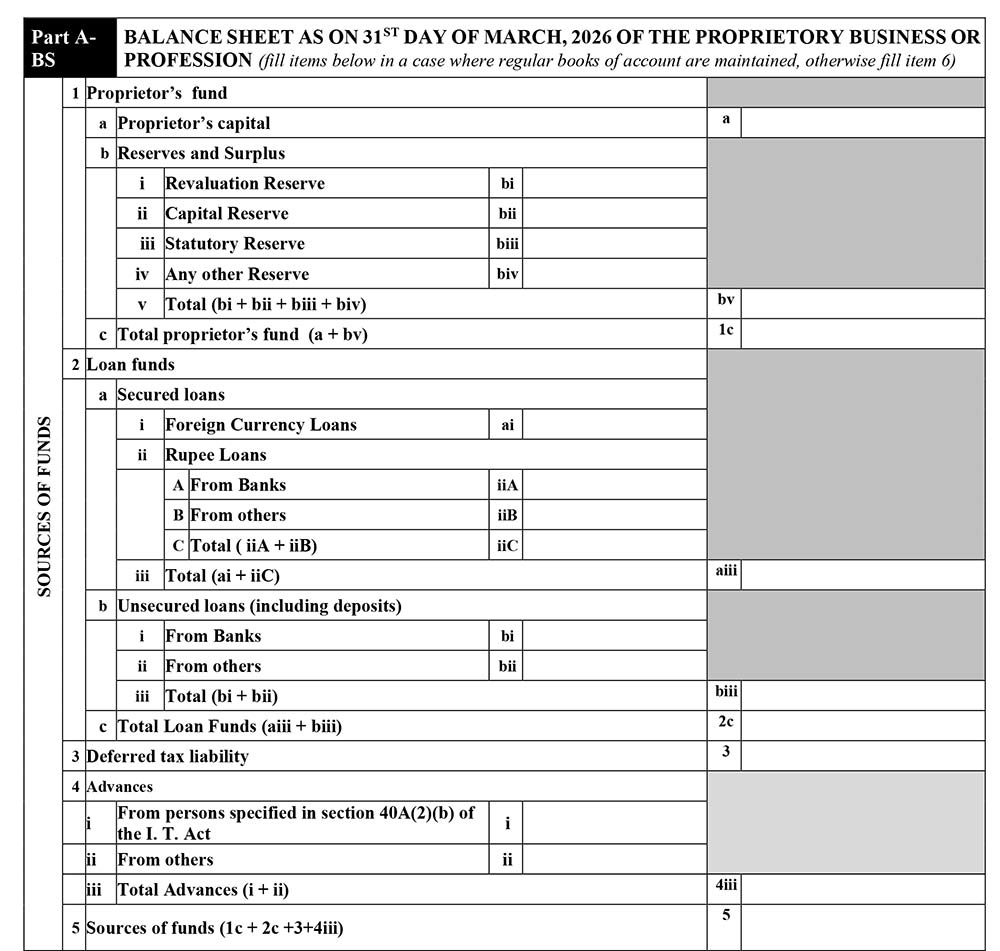

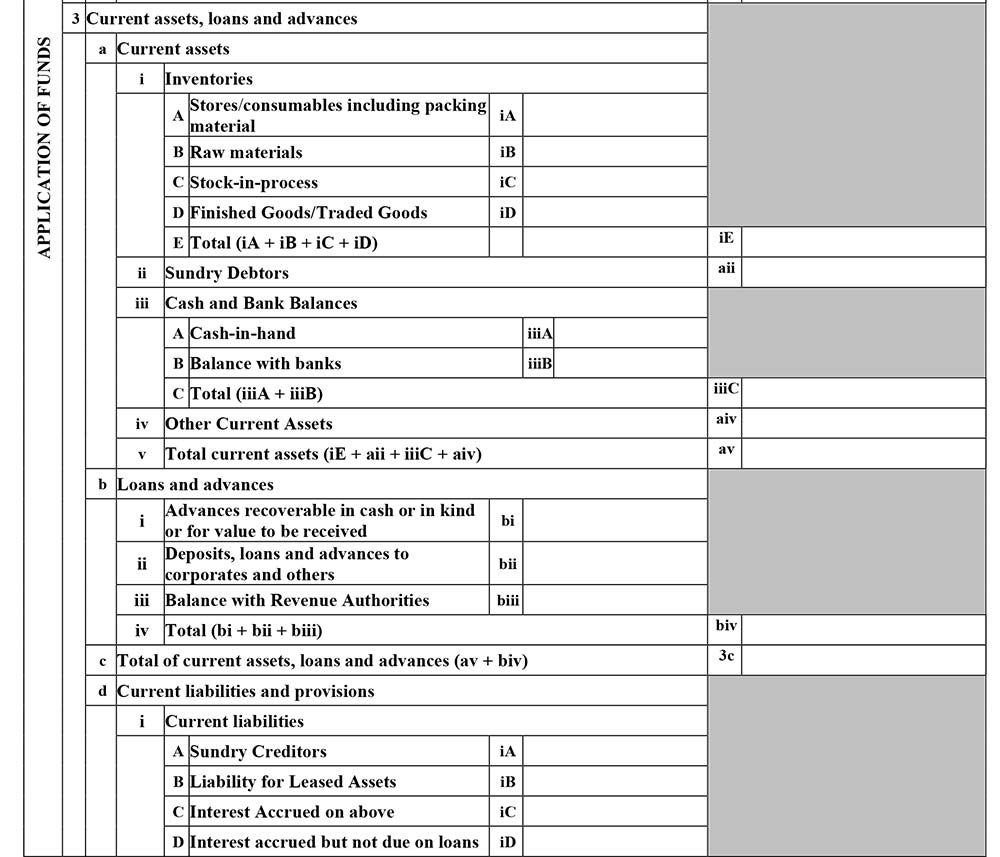

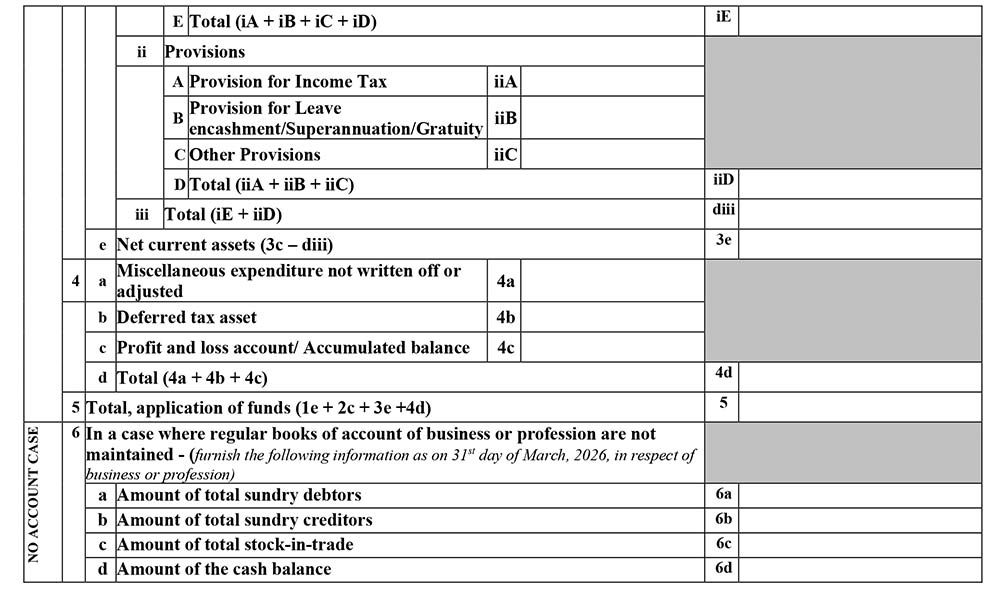

Part-A BS

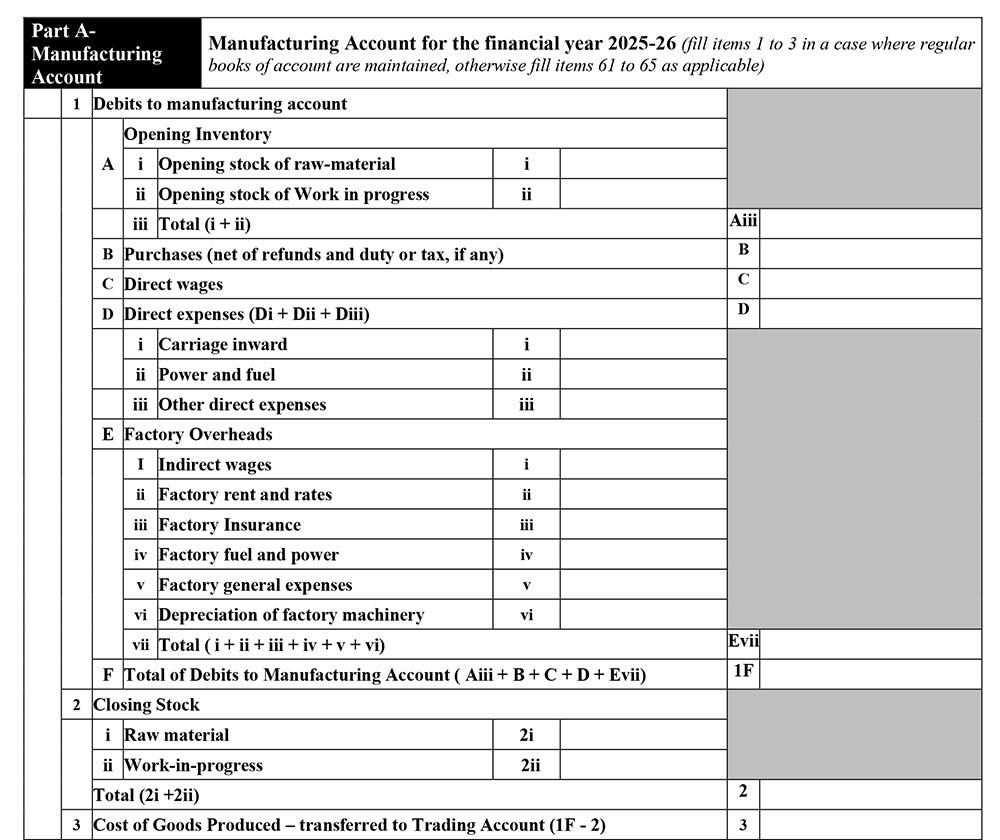

Part A-Manufacturing Account

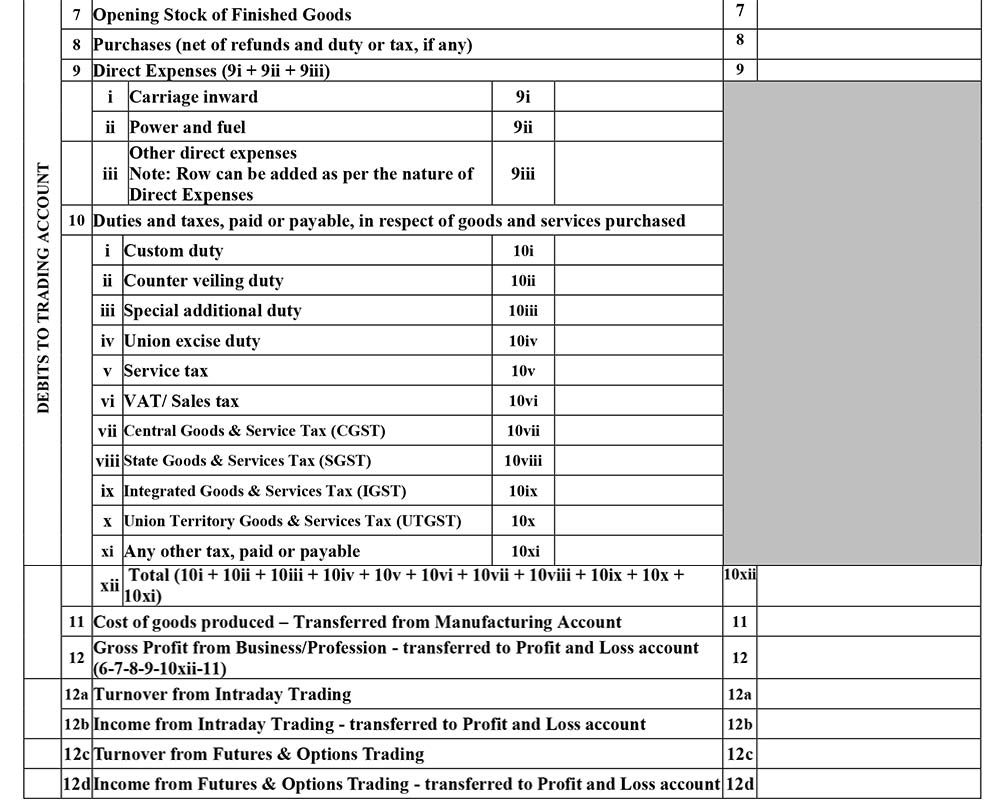

Part A-Trading Account

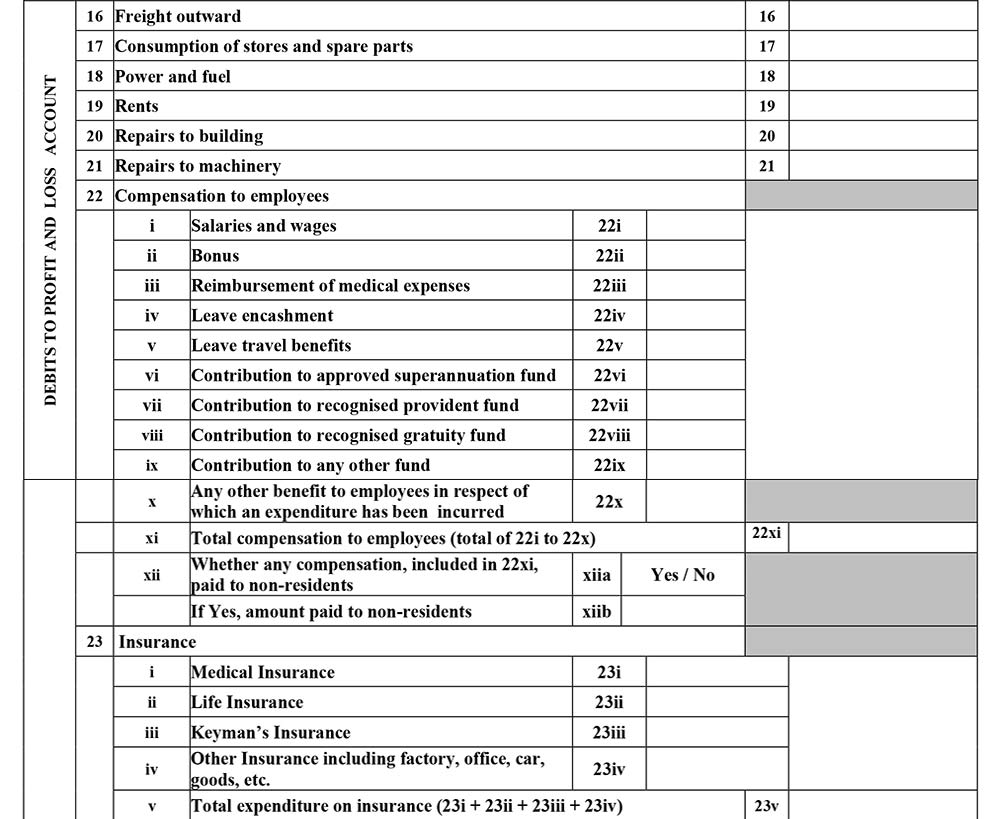

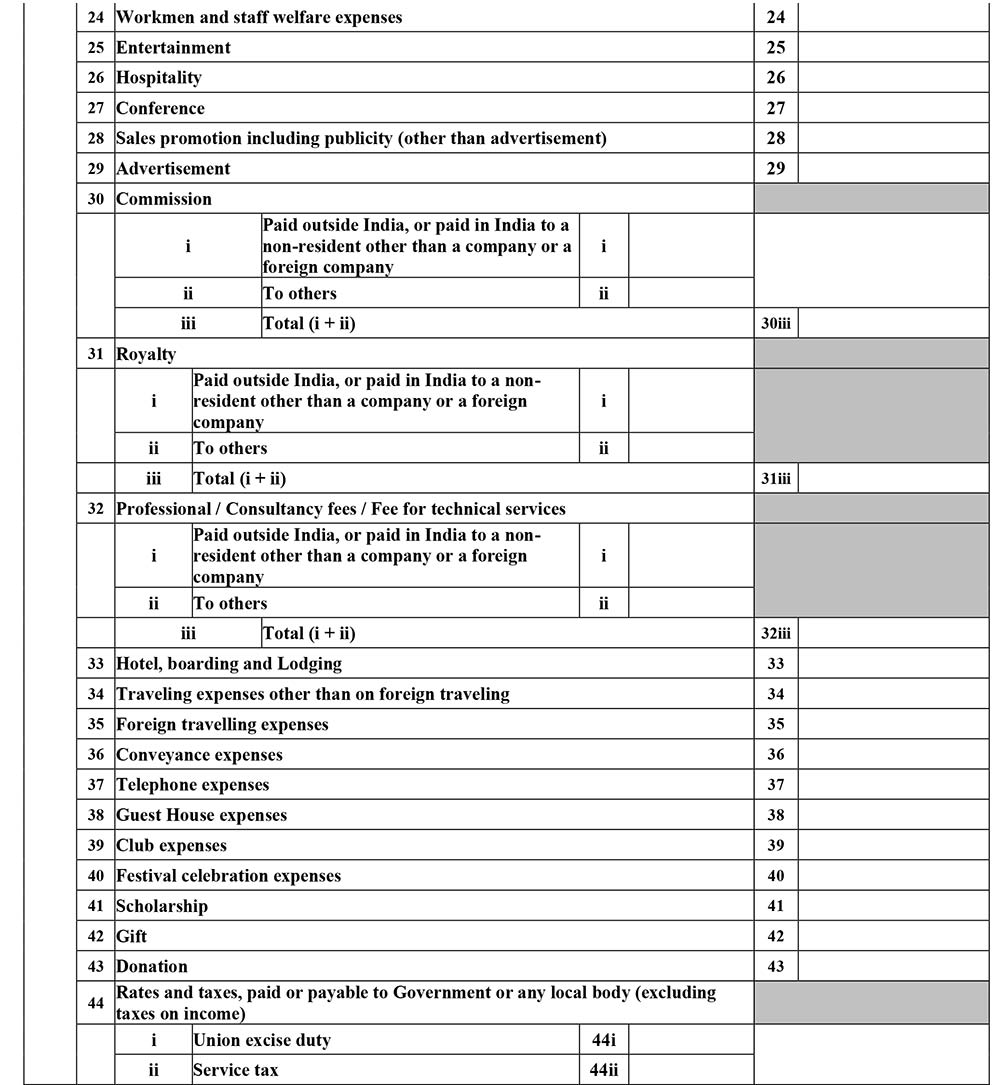

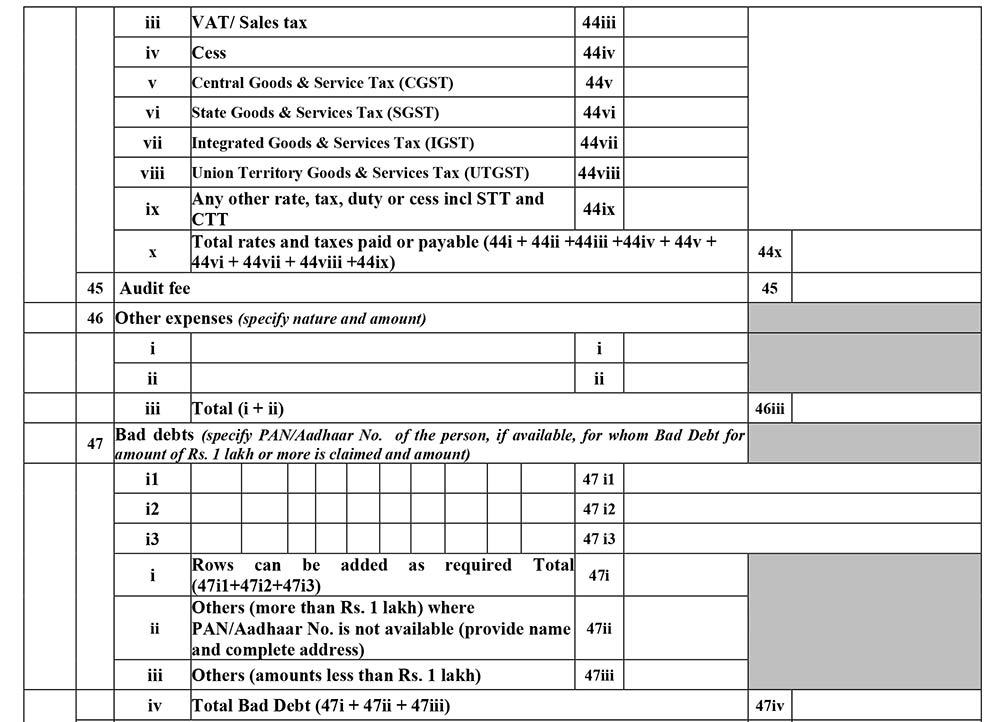

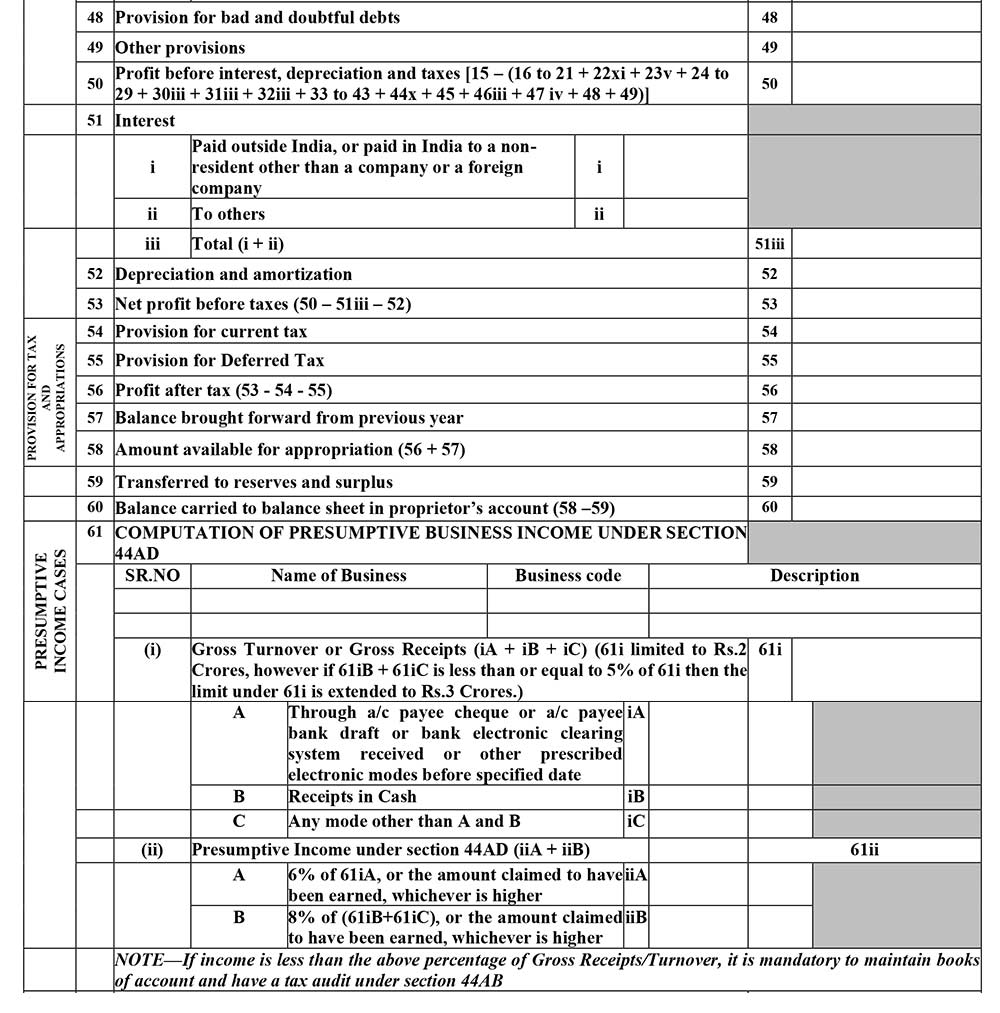

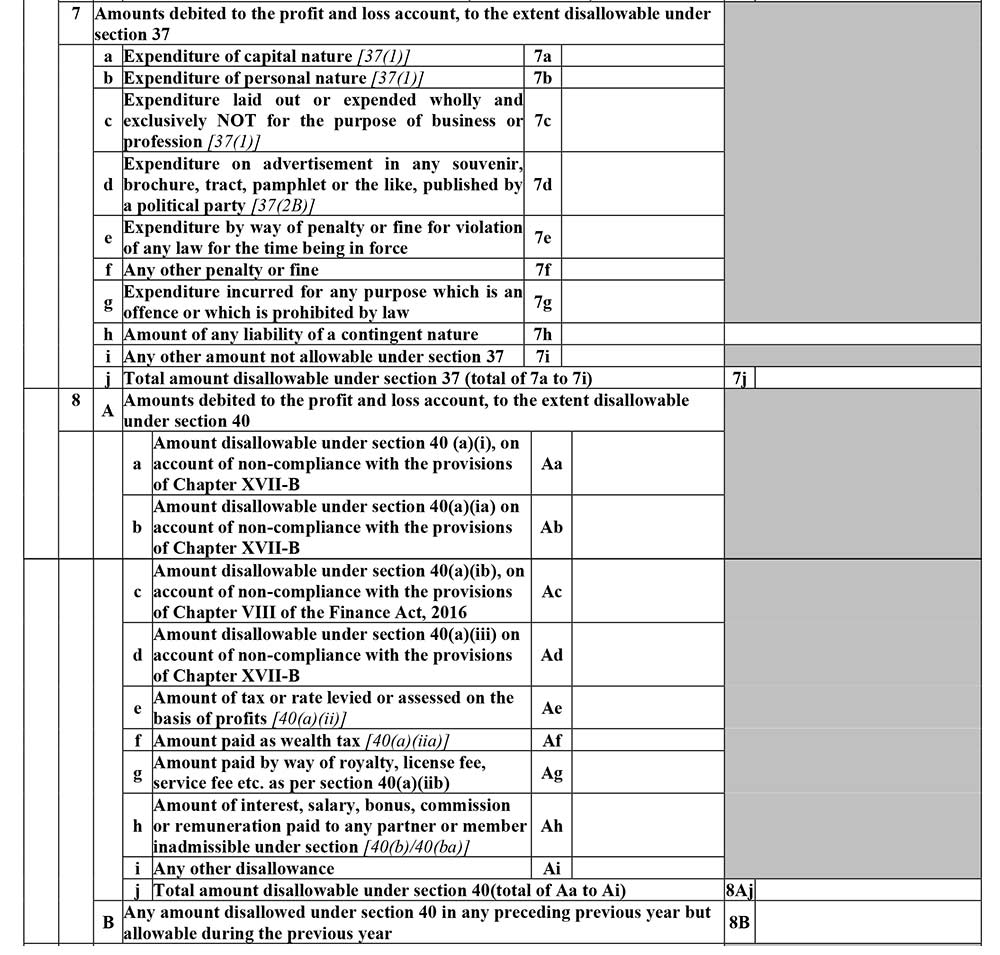

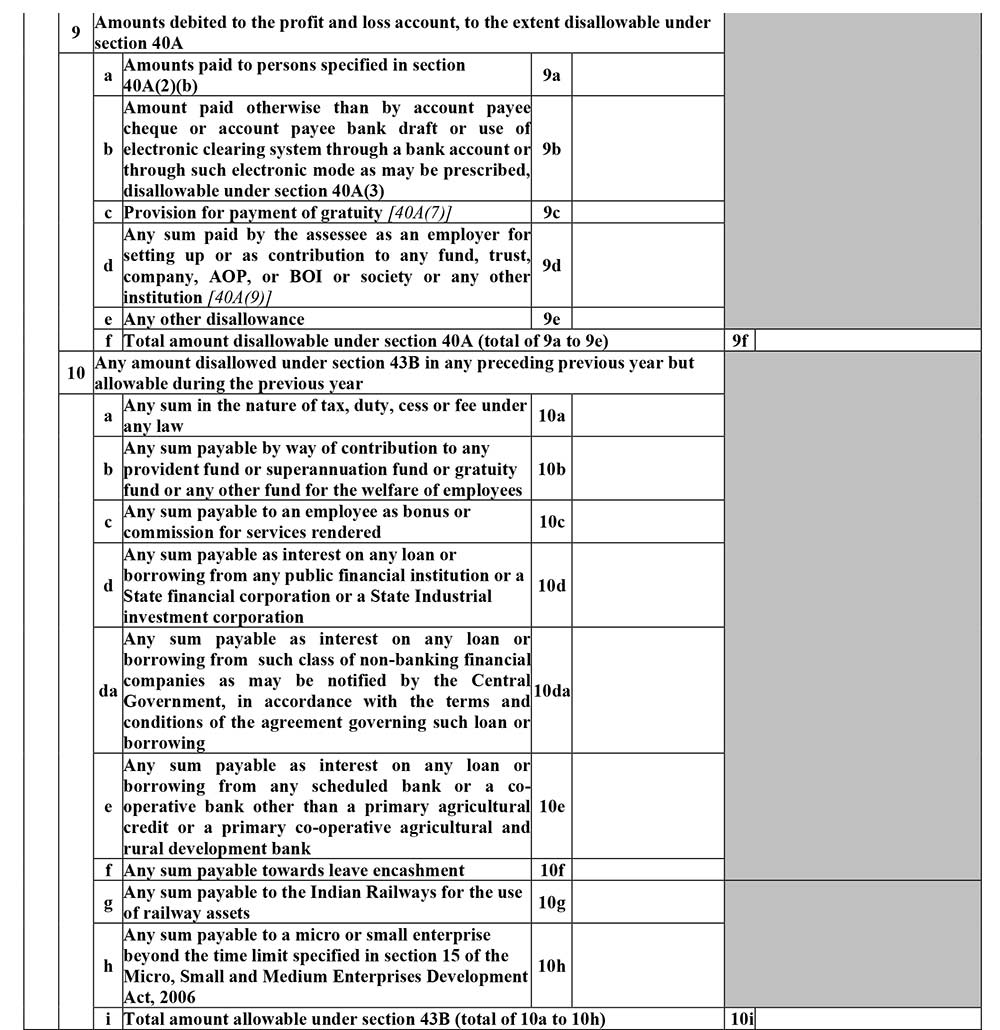

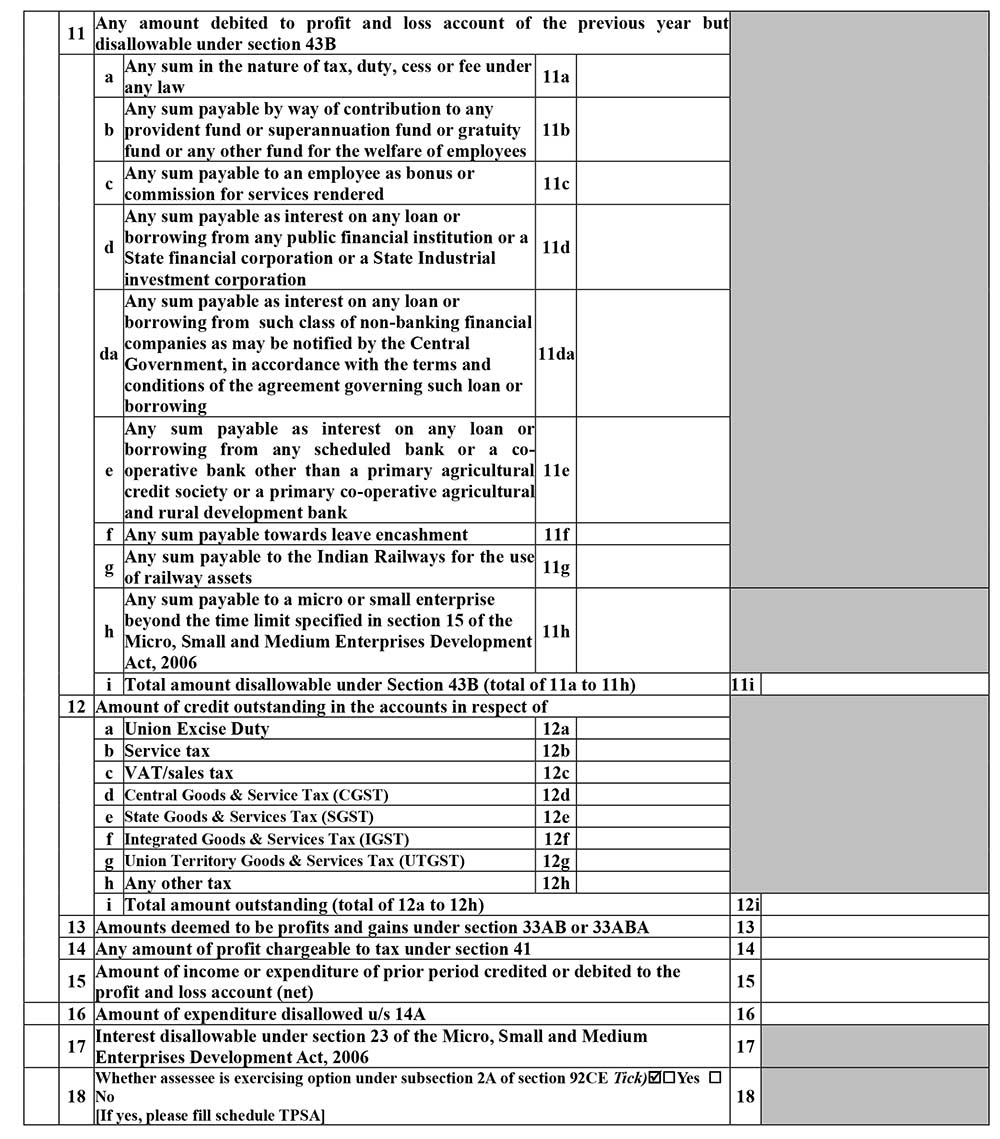

Part A-P&L Account

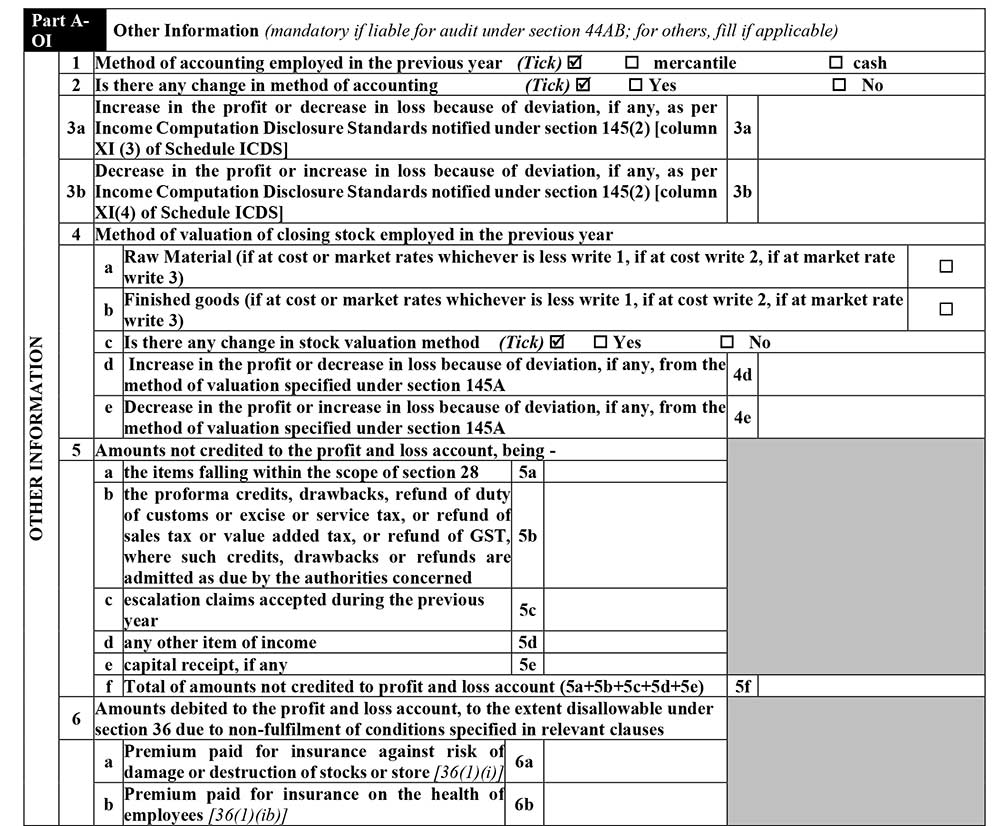

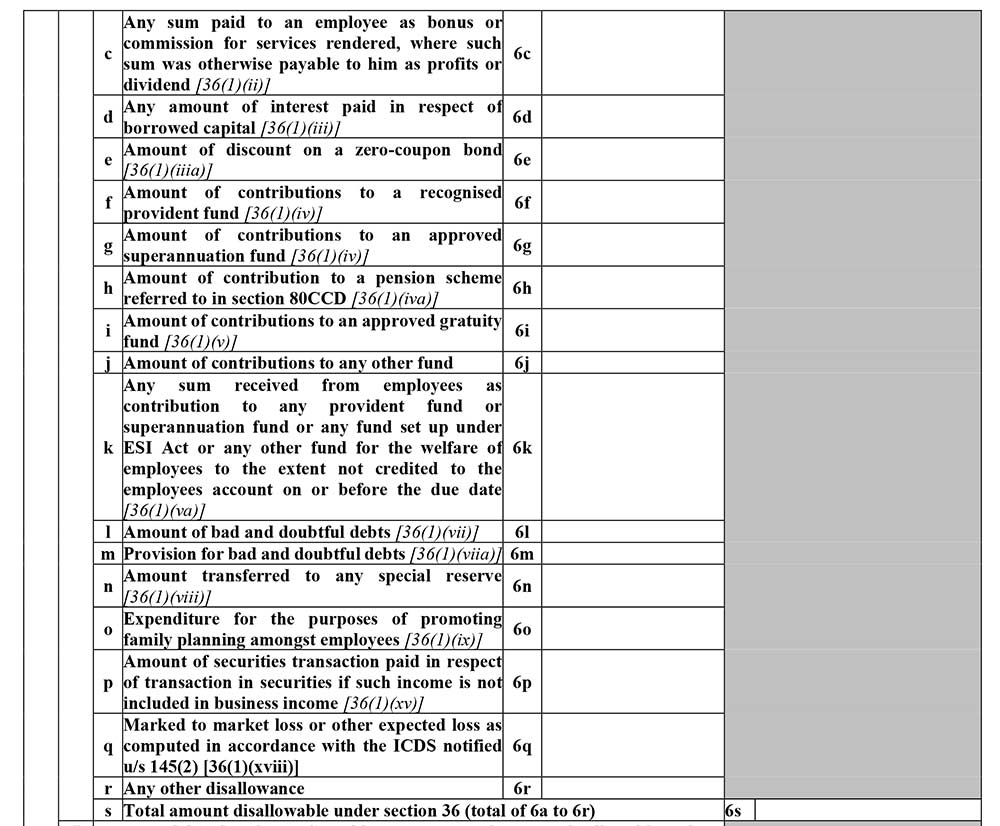

Part A-Other Information

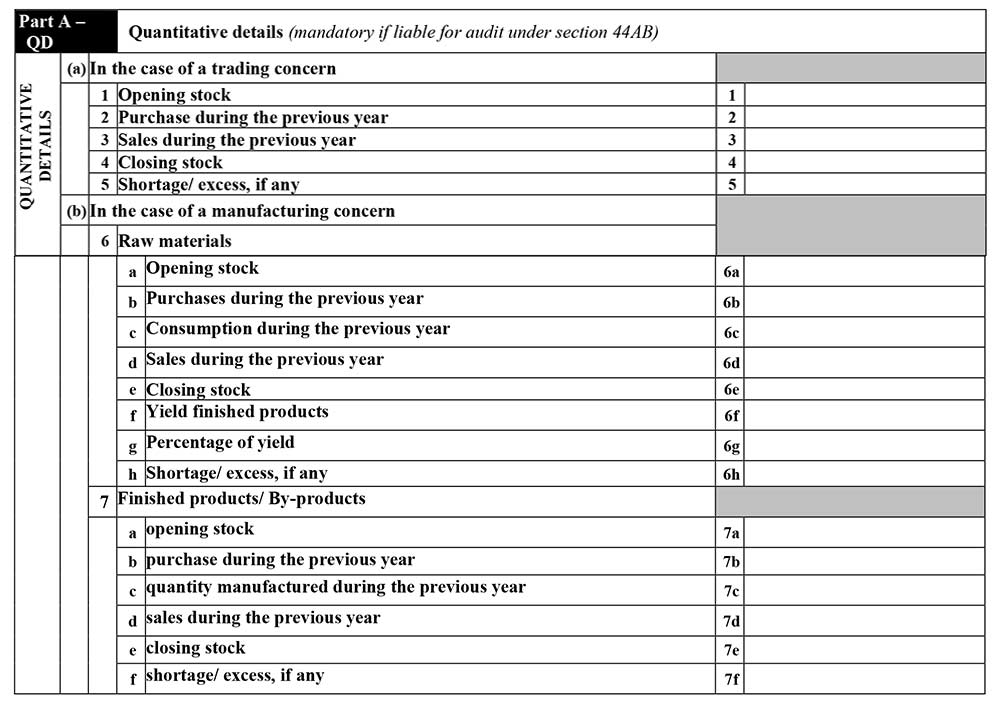

Part A QD

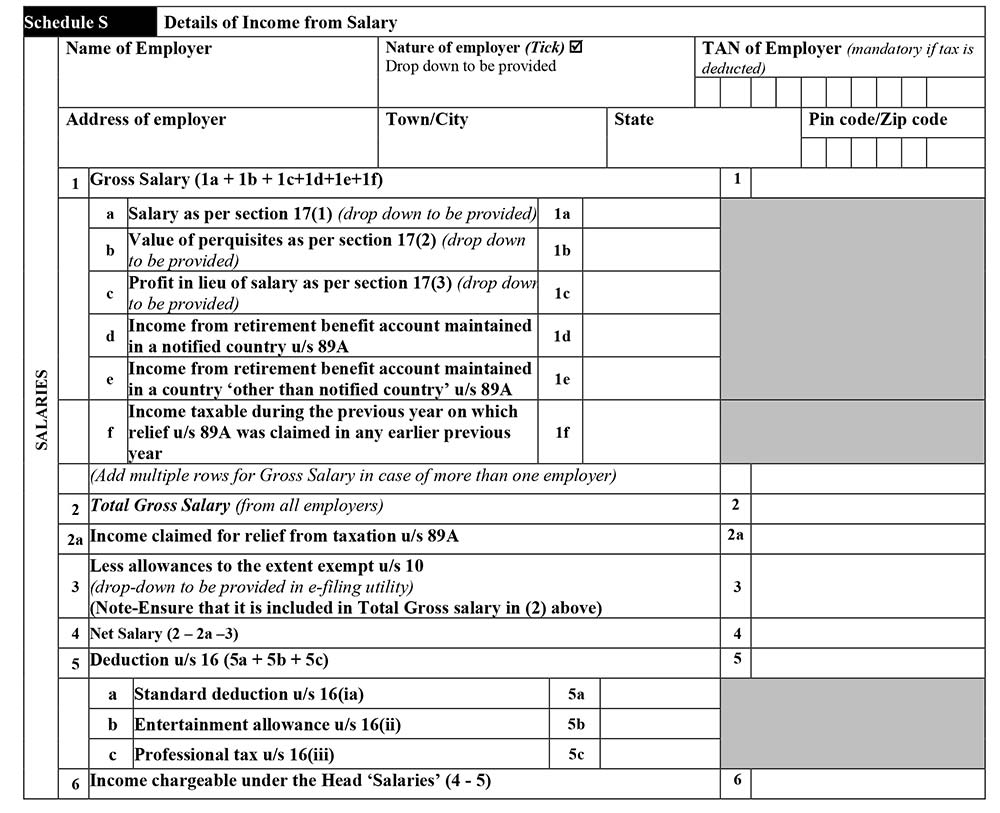

Schedule S

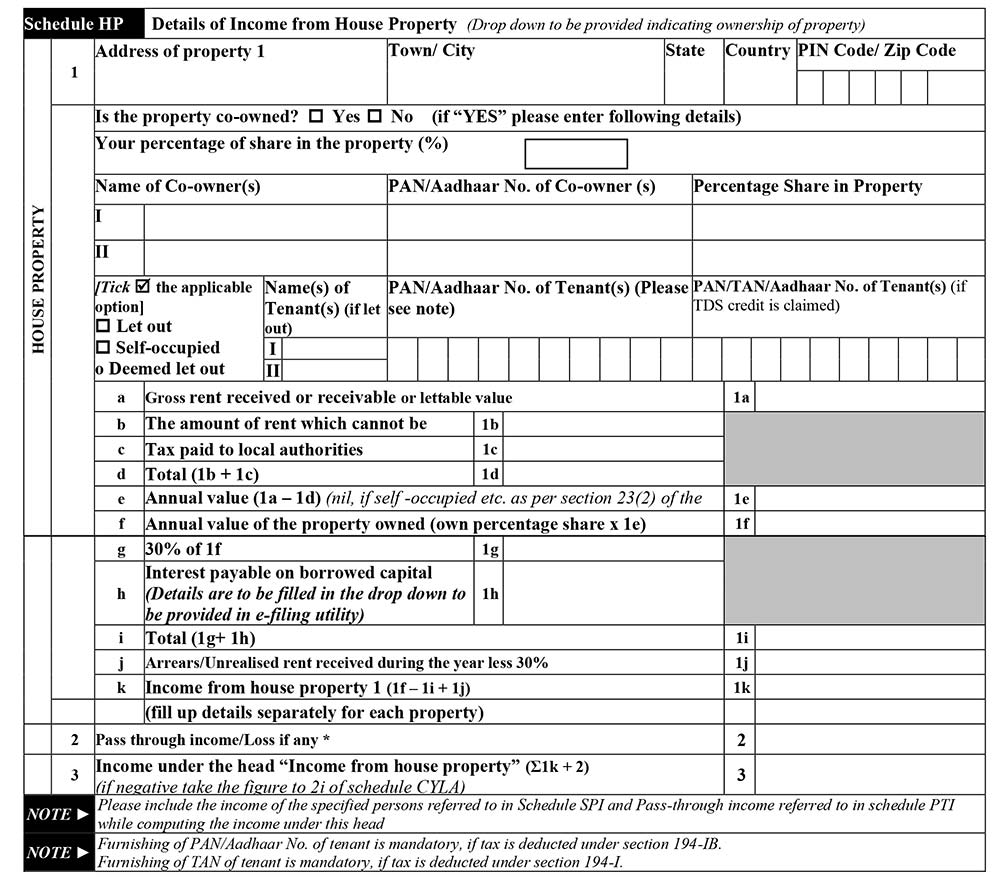

Schedule HP

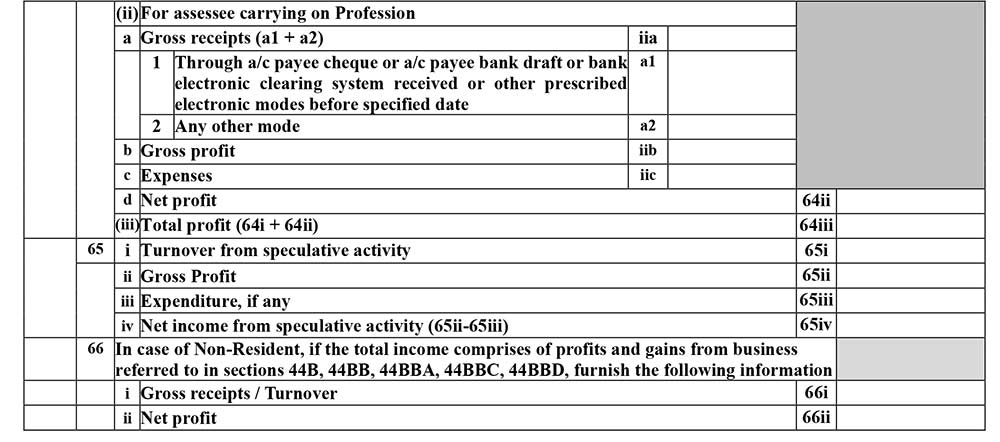

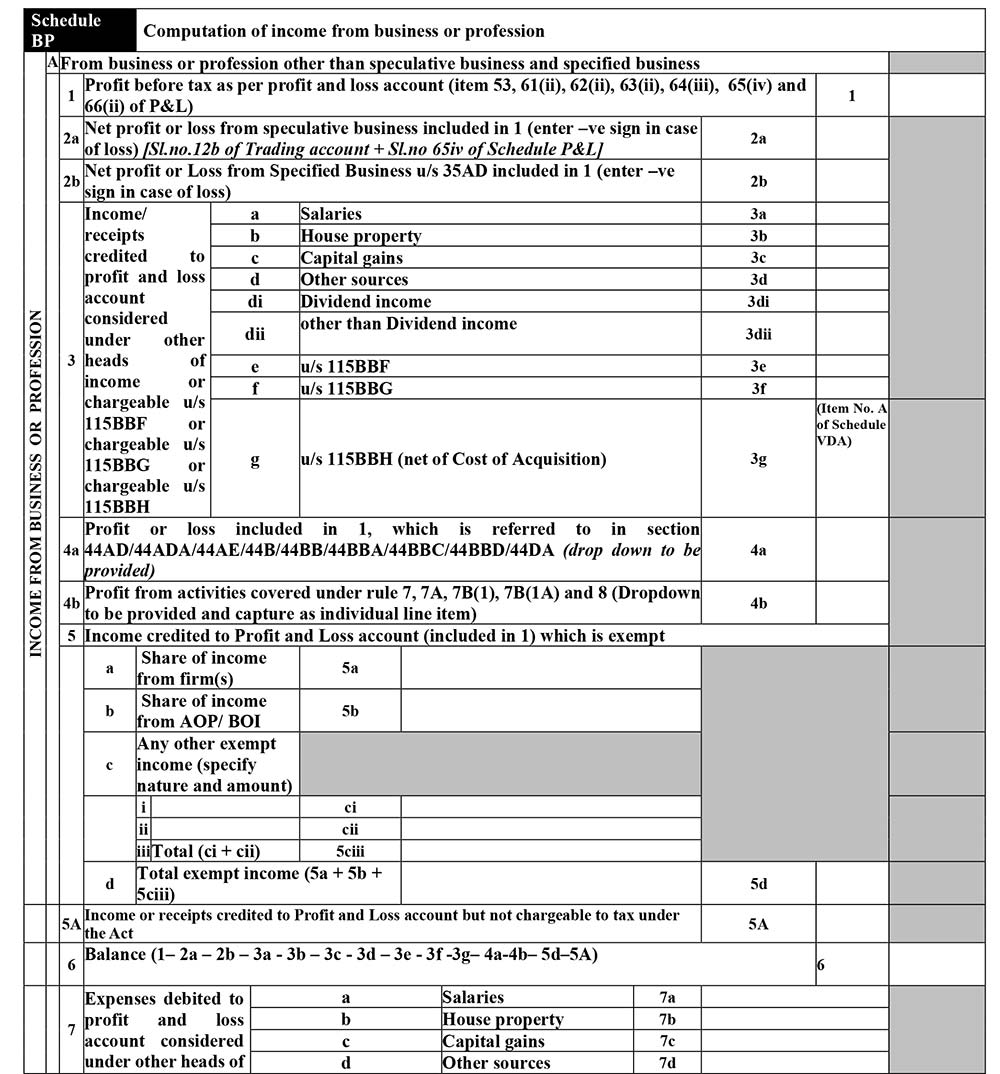

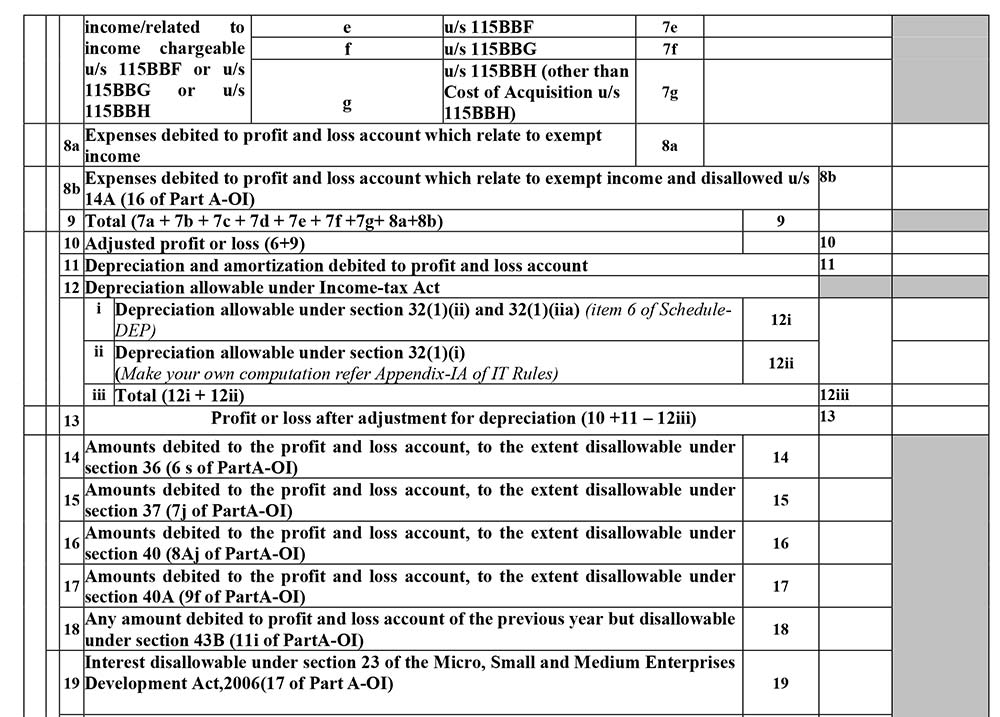

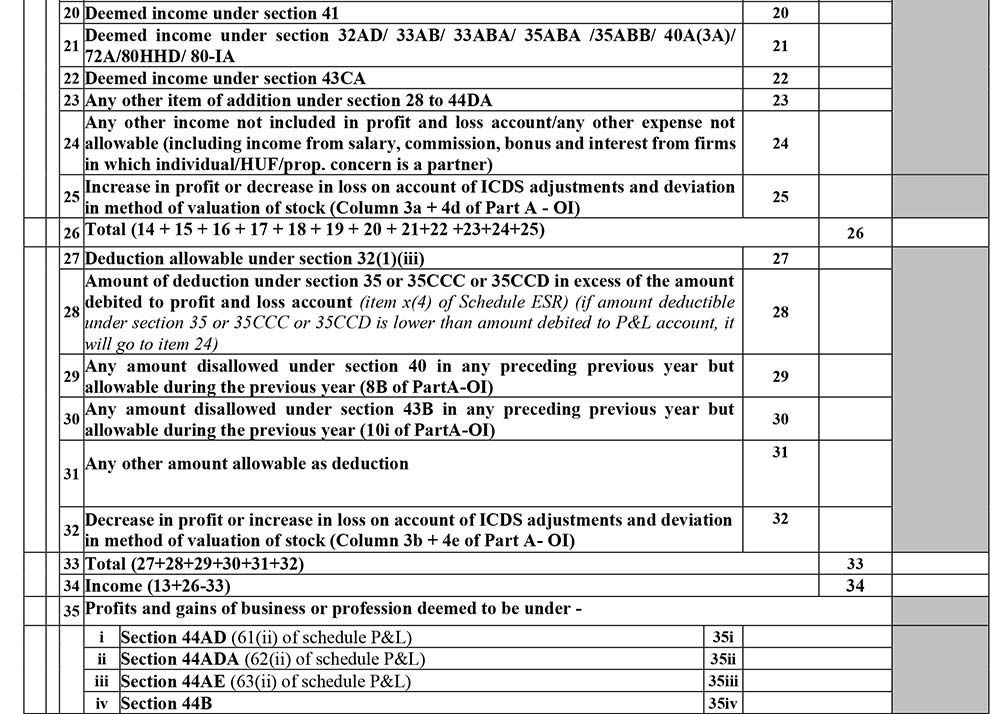

Schedule BP

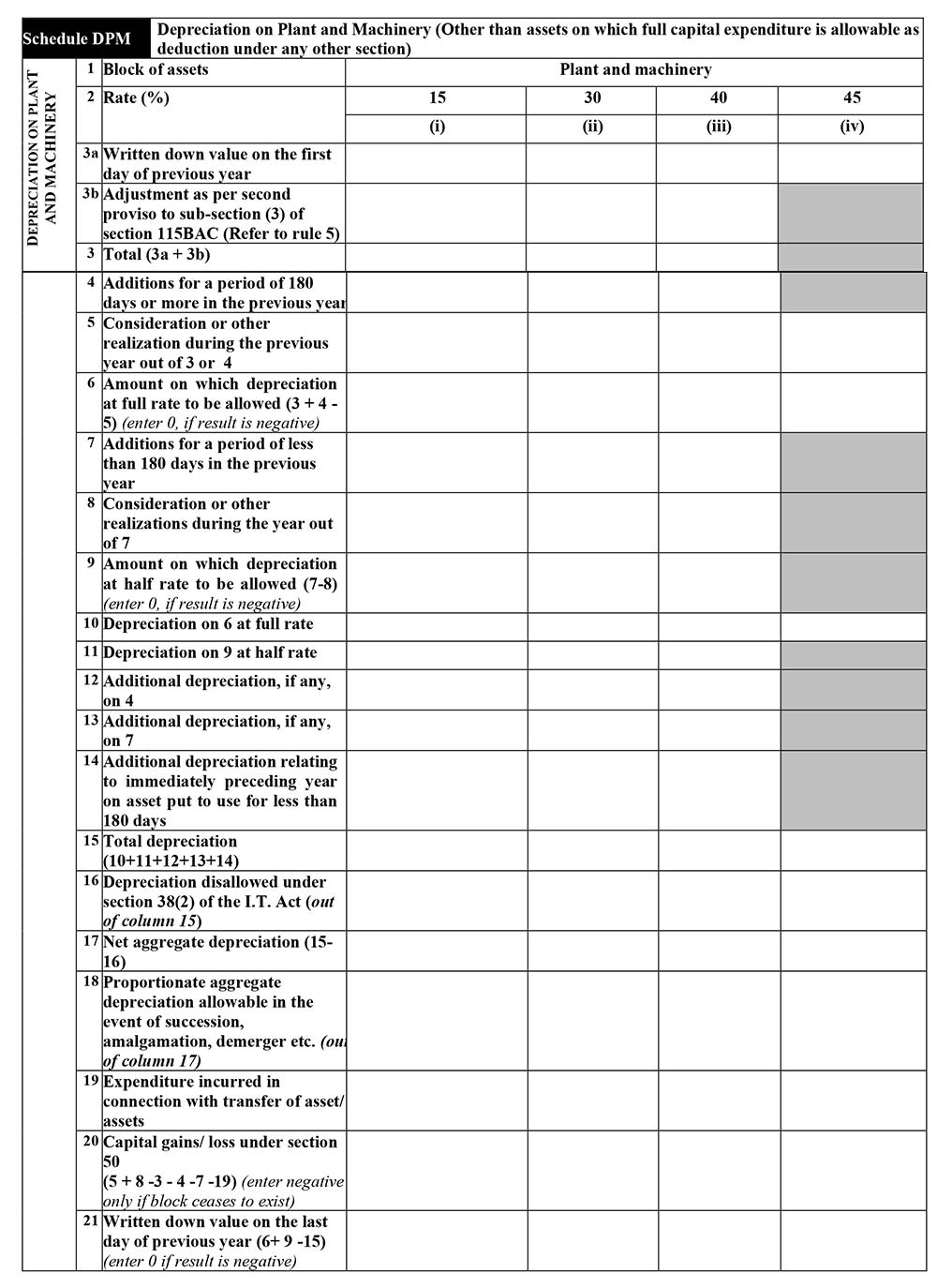

Schedule DPM

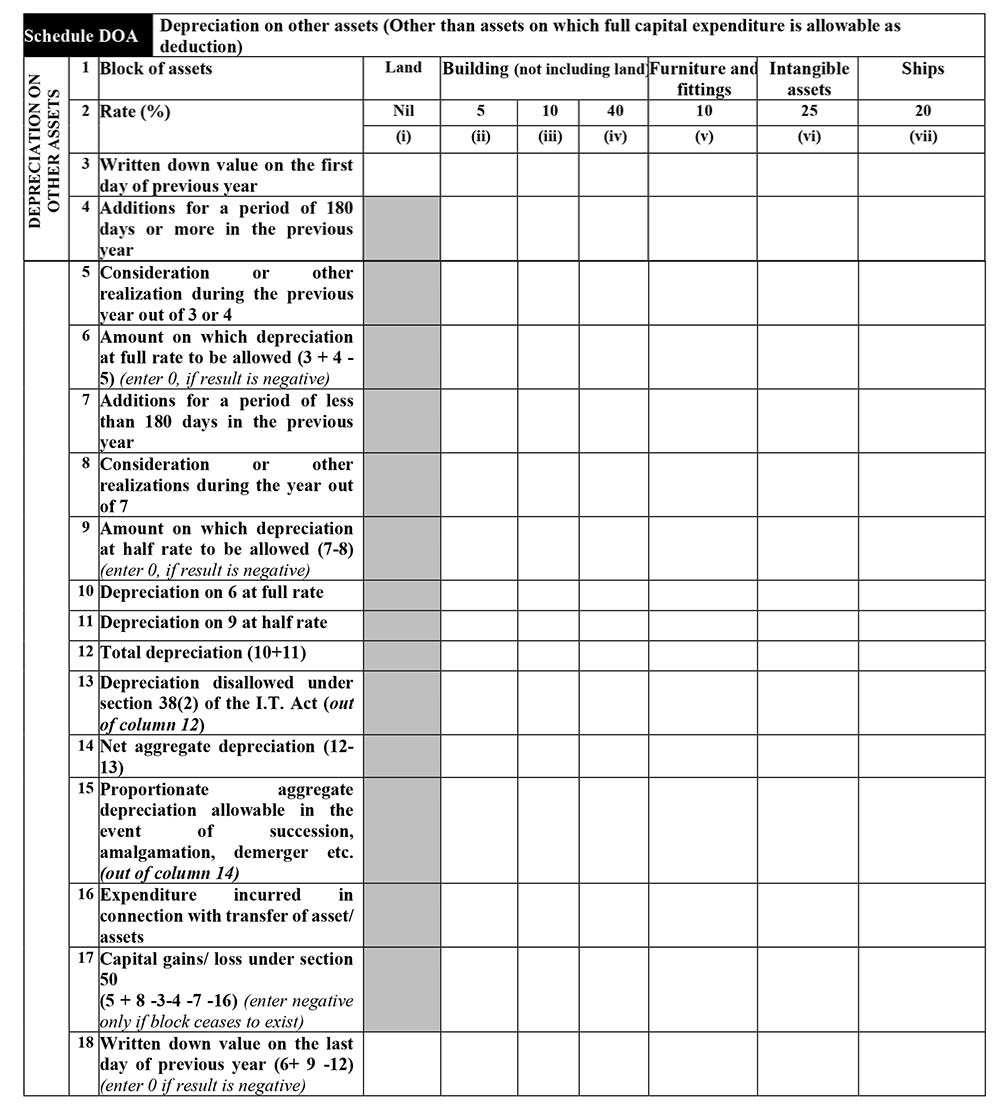

Schedule DOA

Schedule DEP

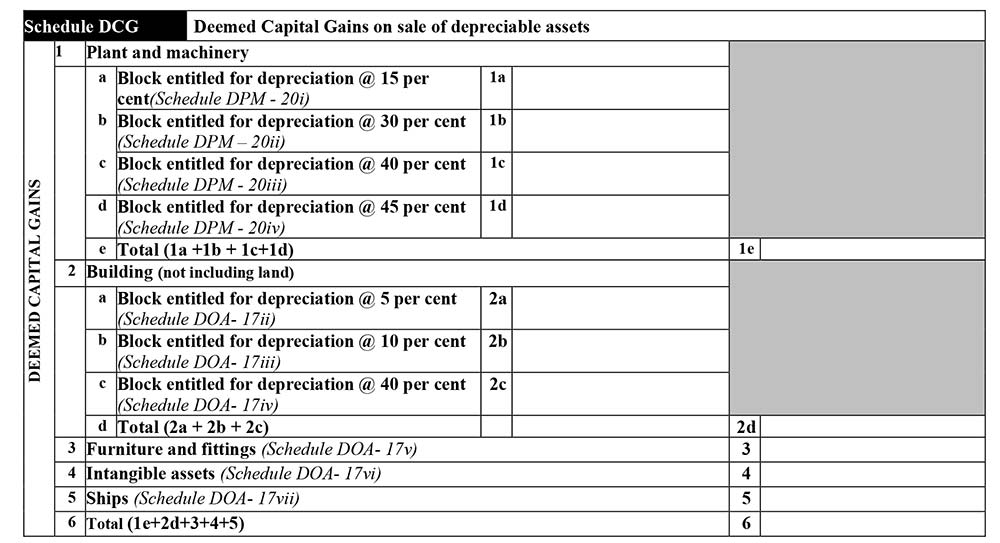

Schedule DCG

Schedule ESR

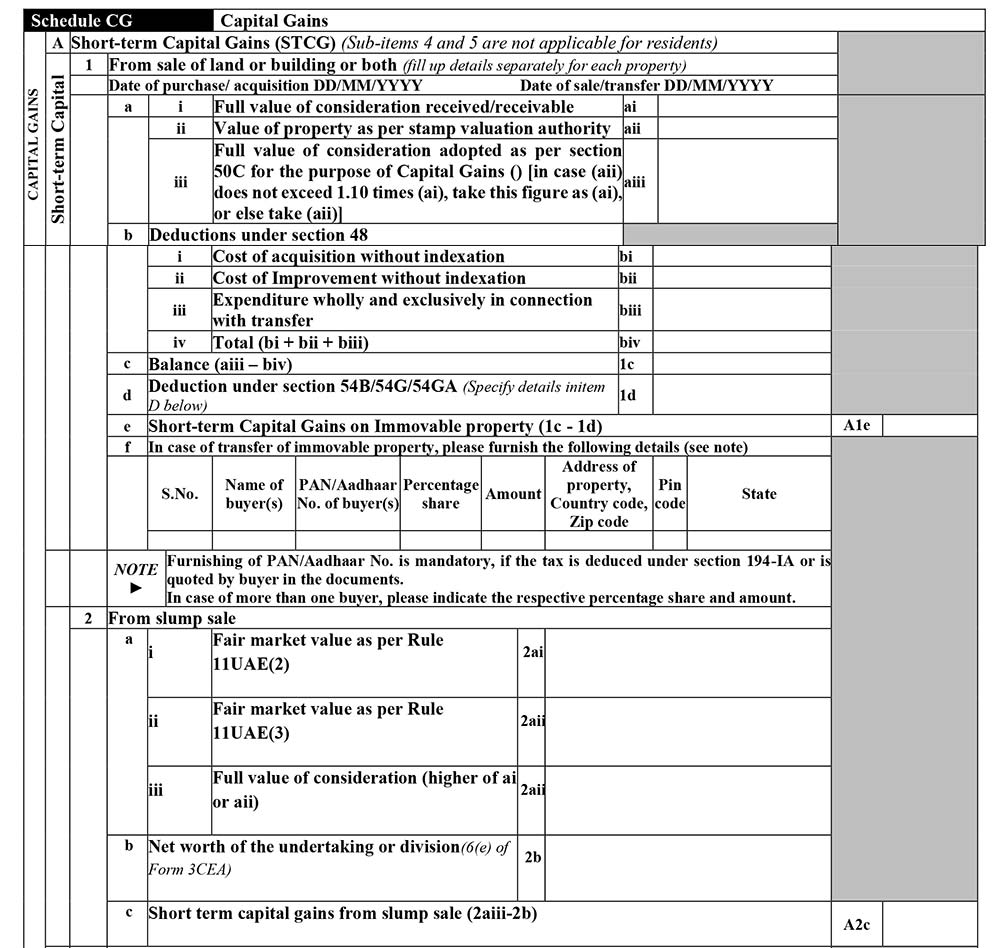

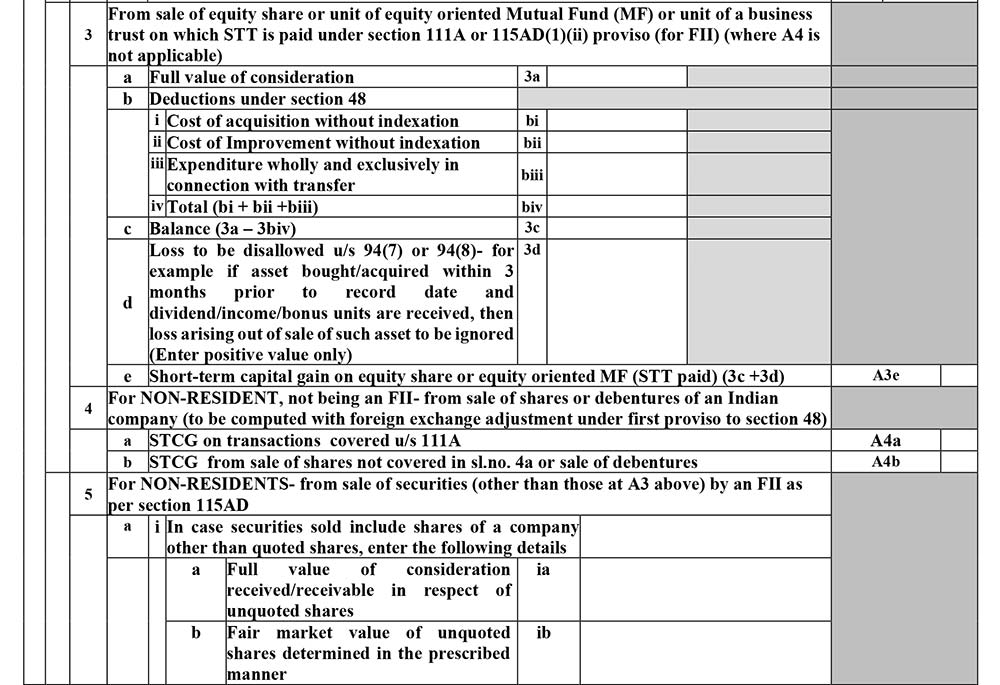

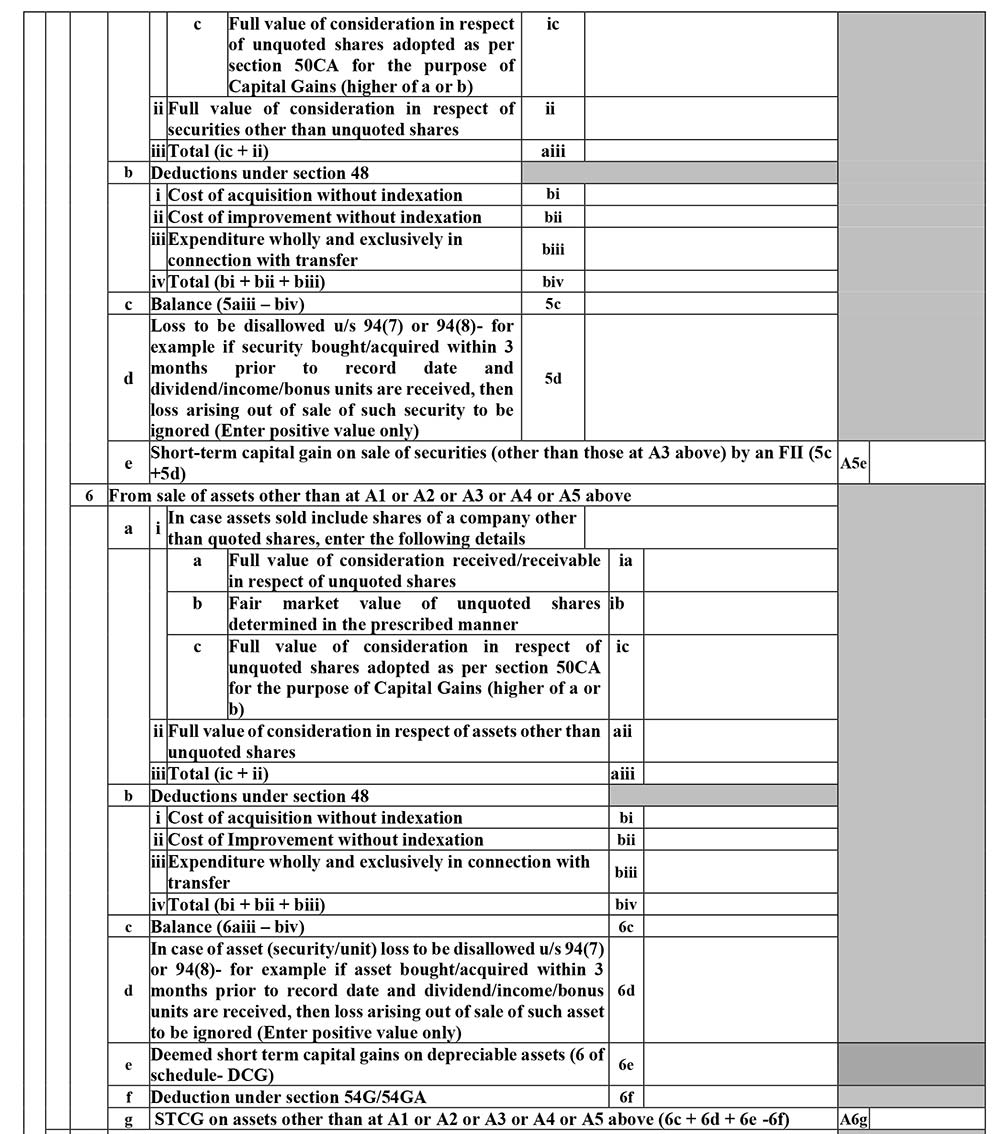

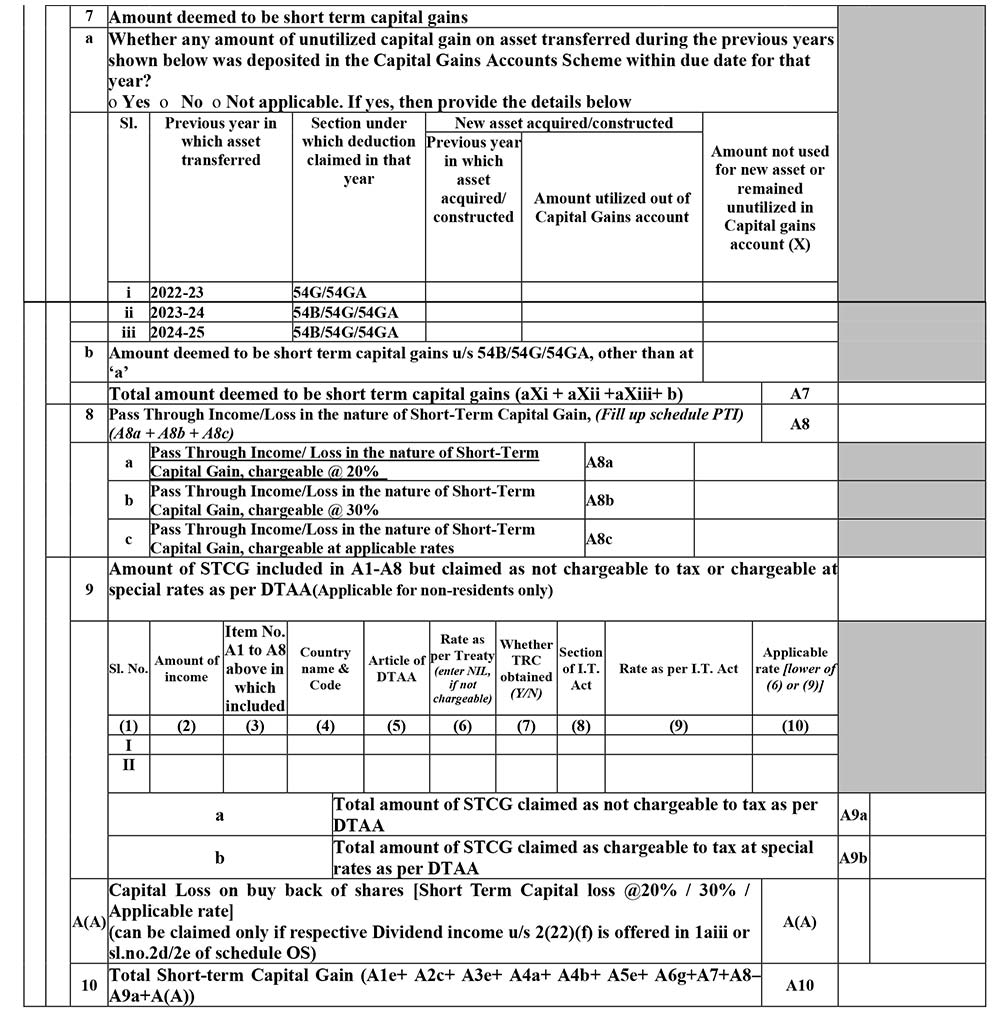

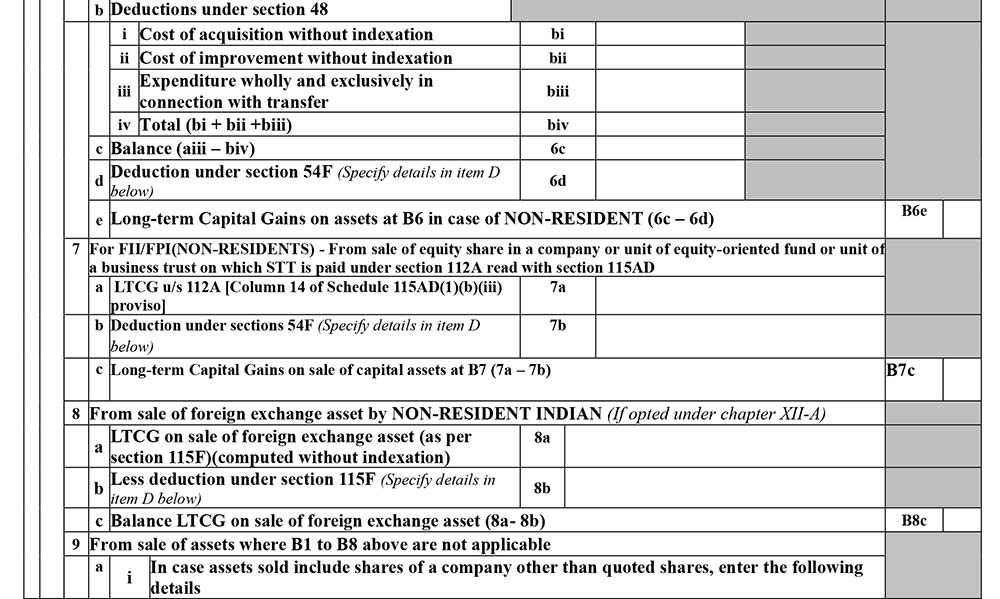

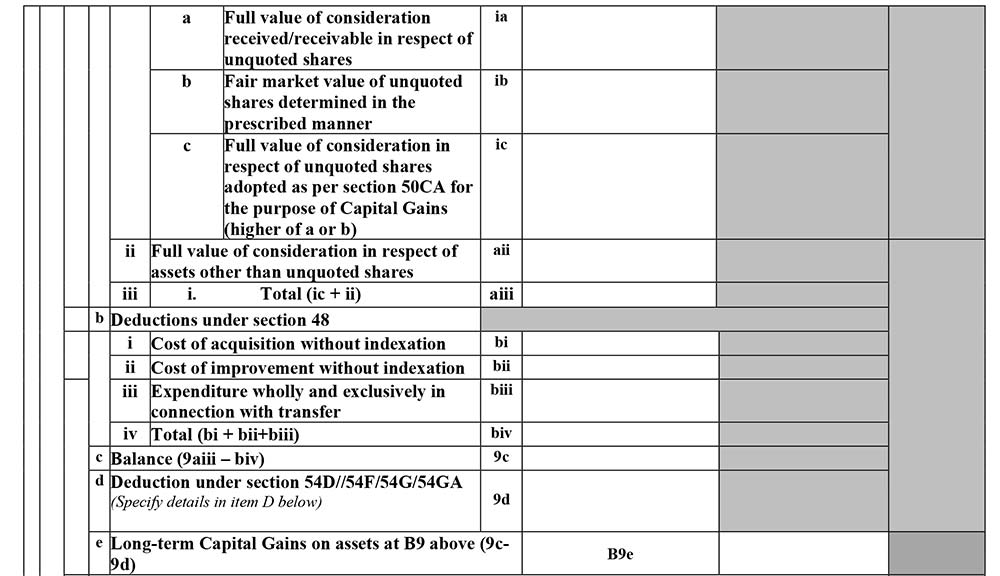

Schedule Capital Gains

A Short-term Capital Gains (STCG)

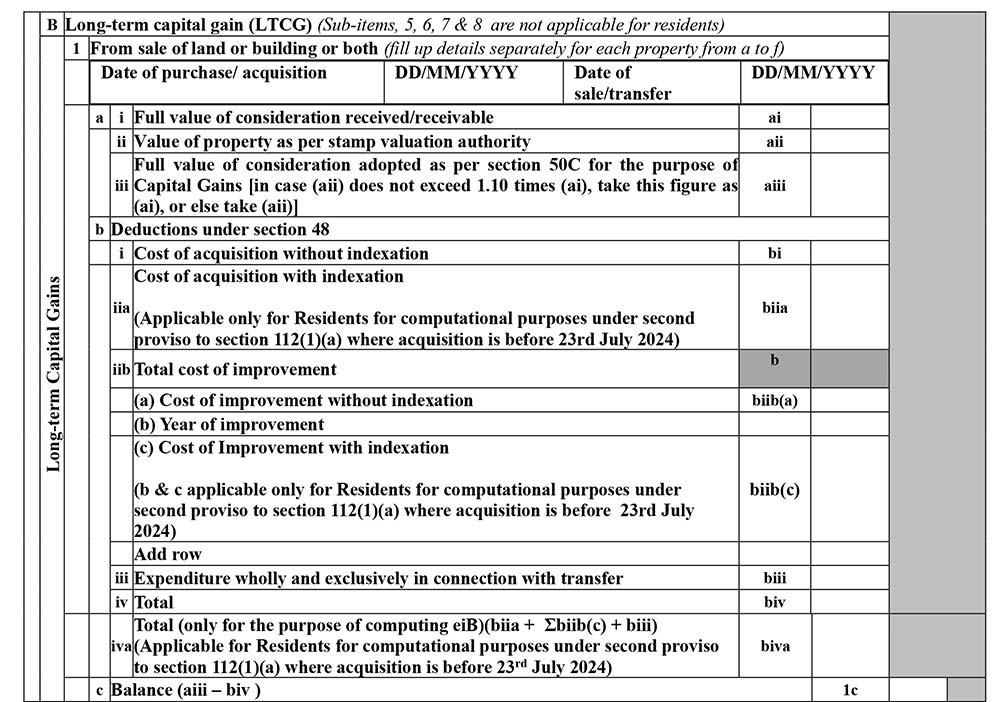

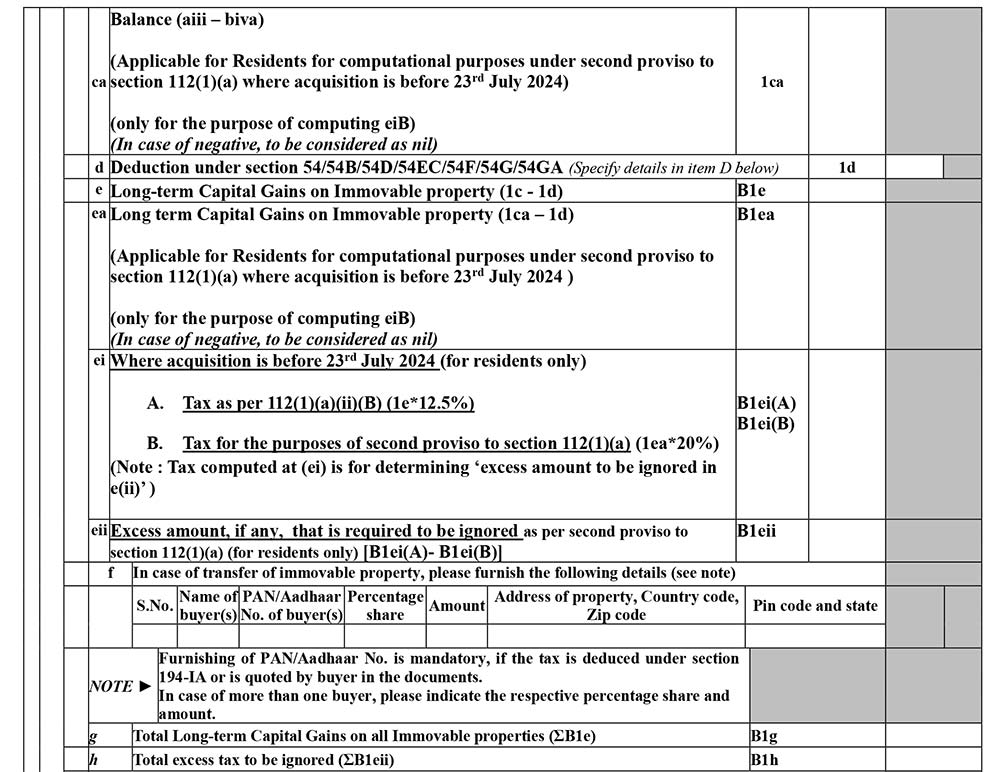

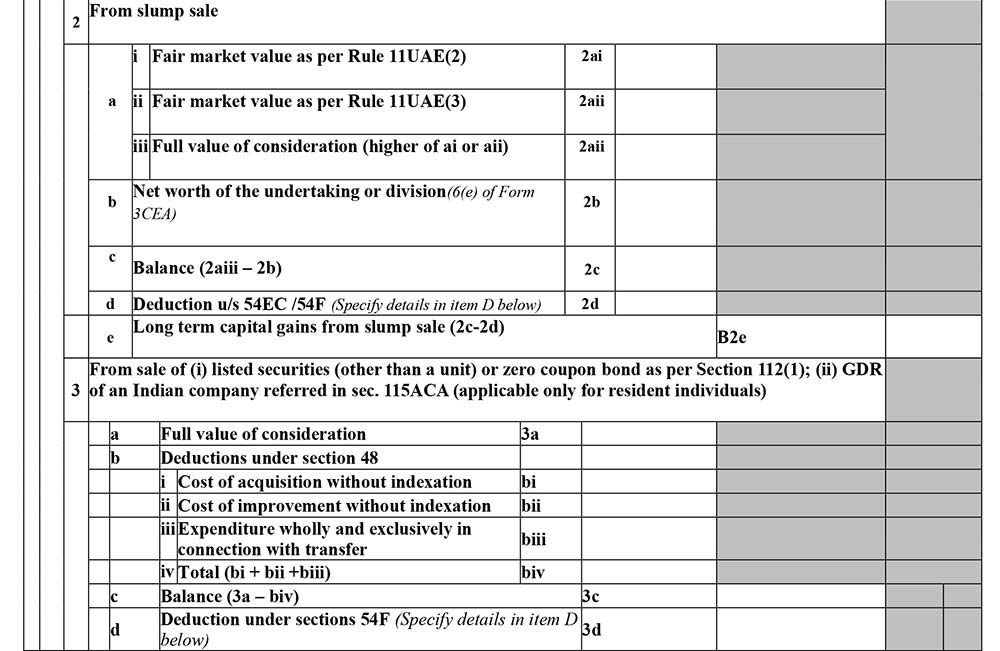

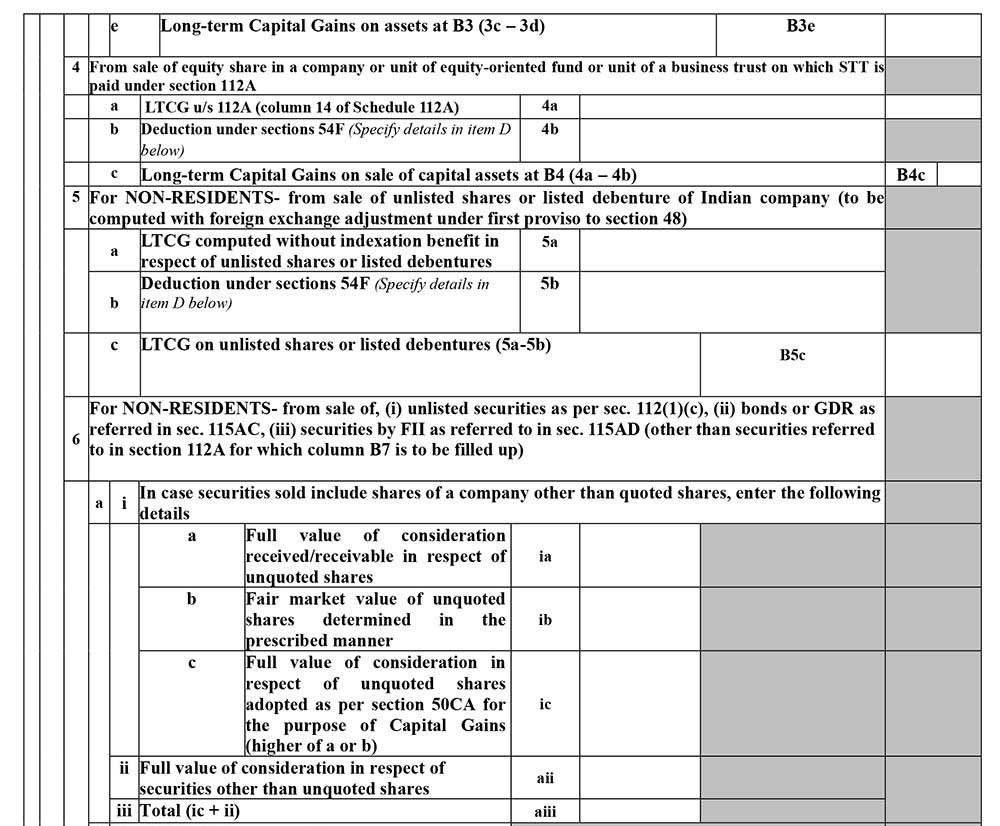

B Long-term capital gain (LTCG)

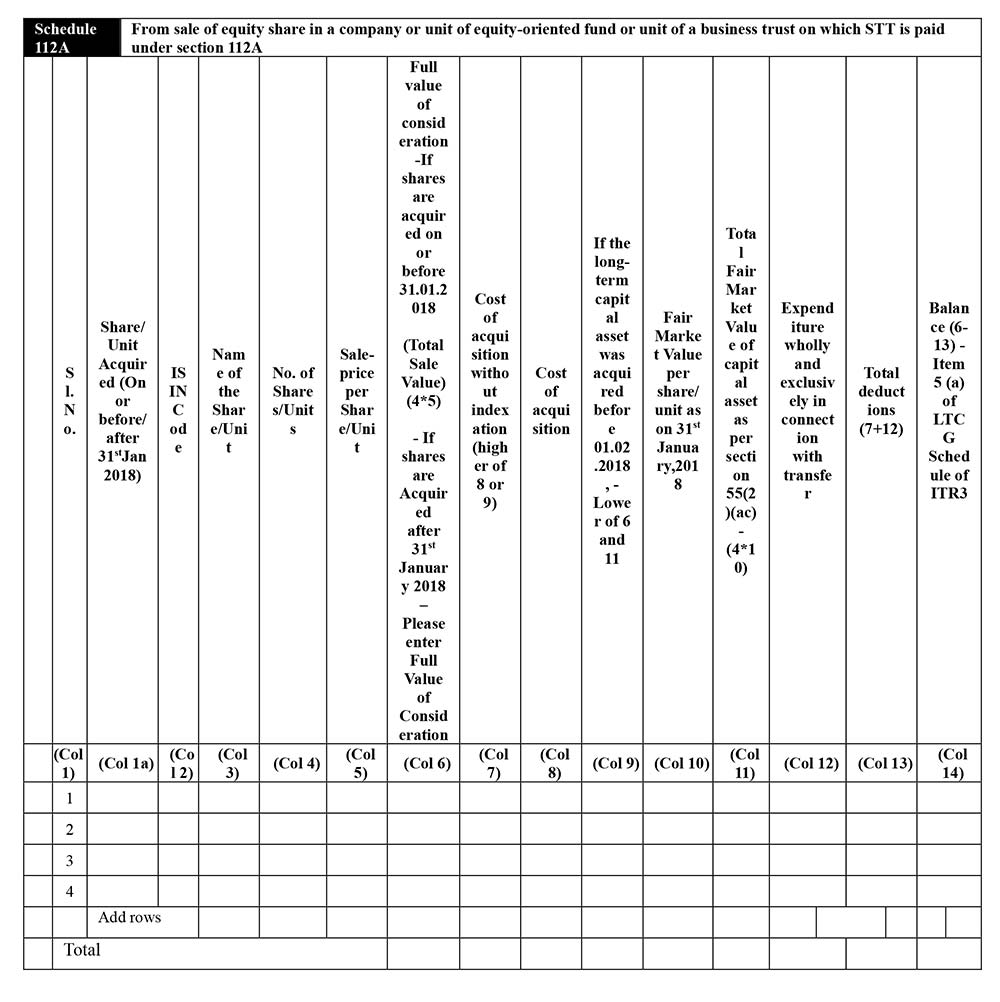

Schedule 112-A

Schedule 115AD(1)(b)(iii) proviso

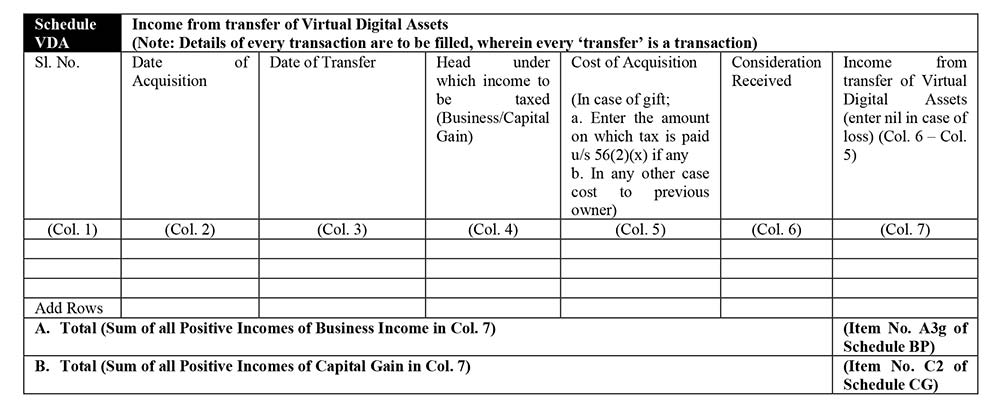

Schedule VDA

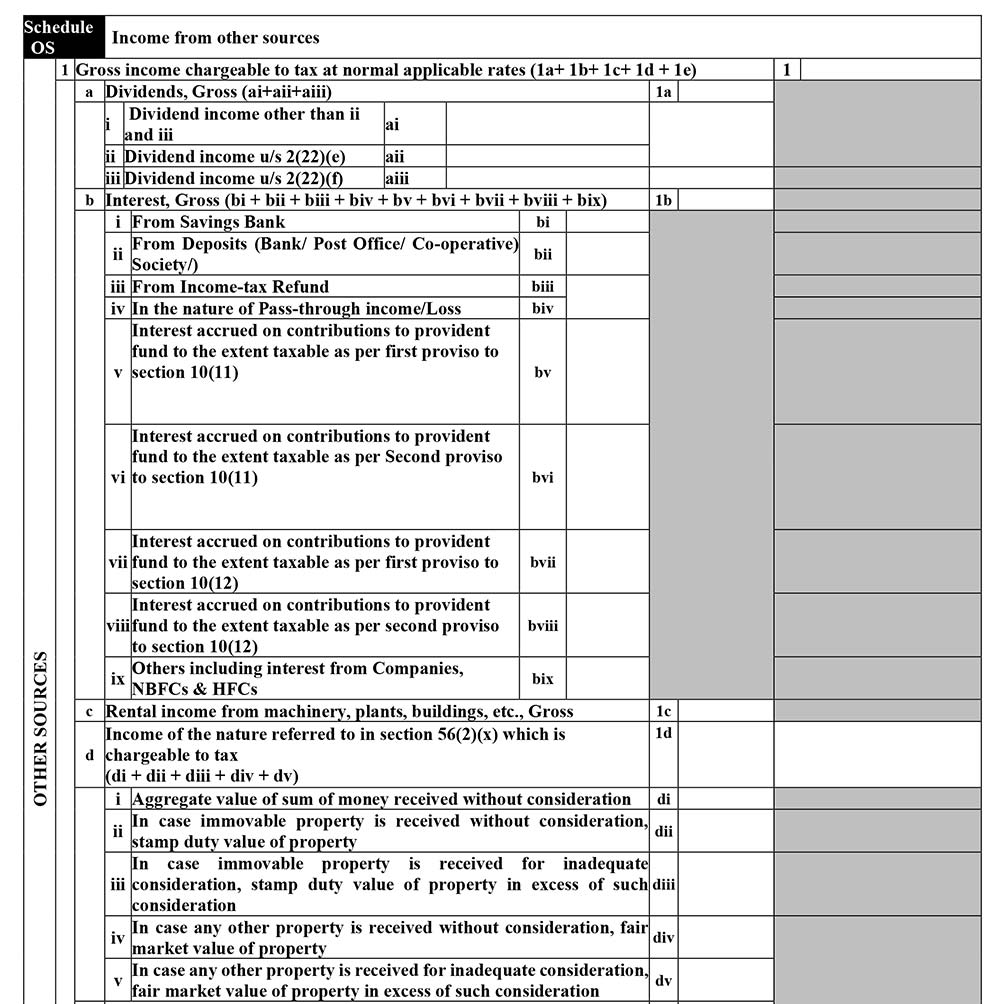

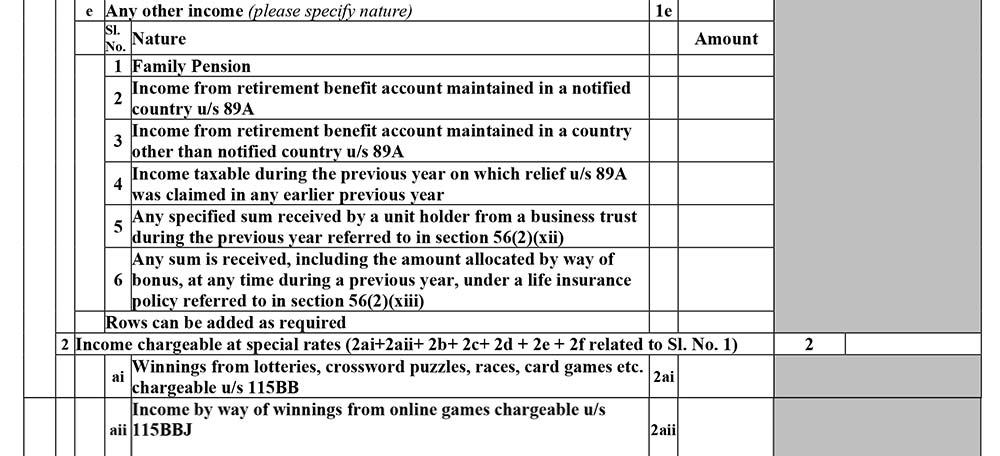

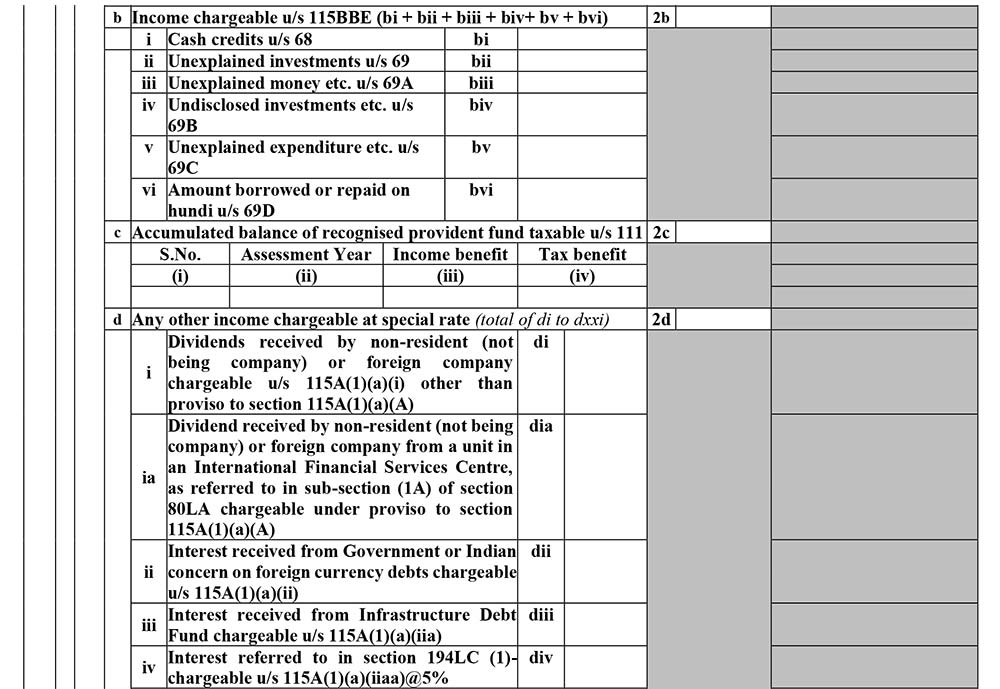

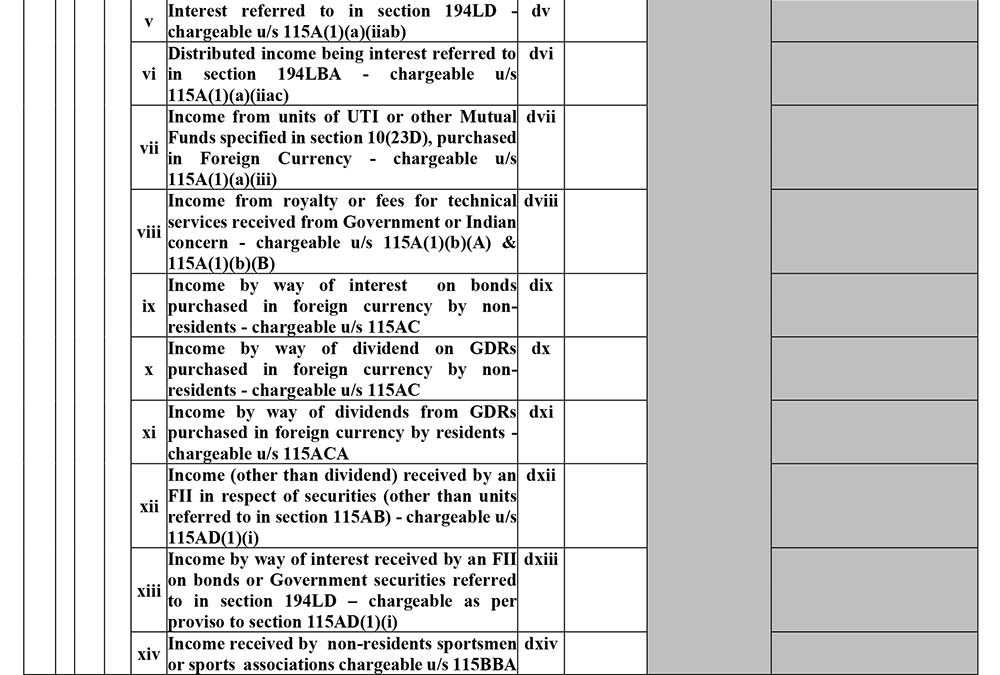

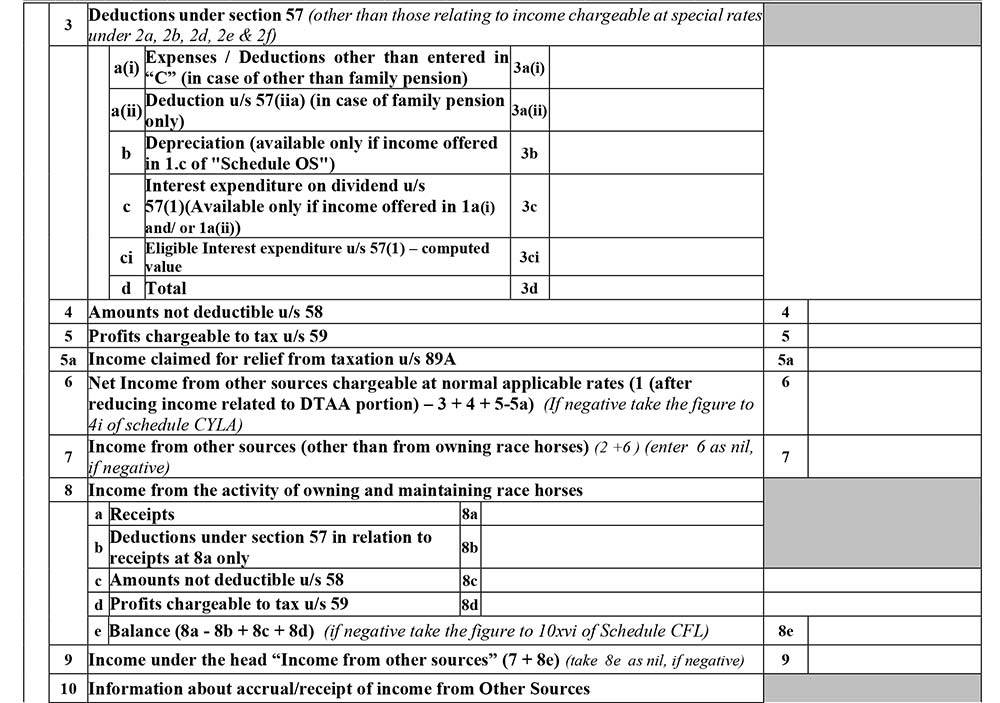

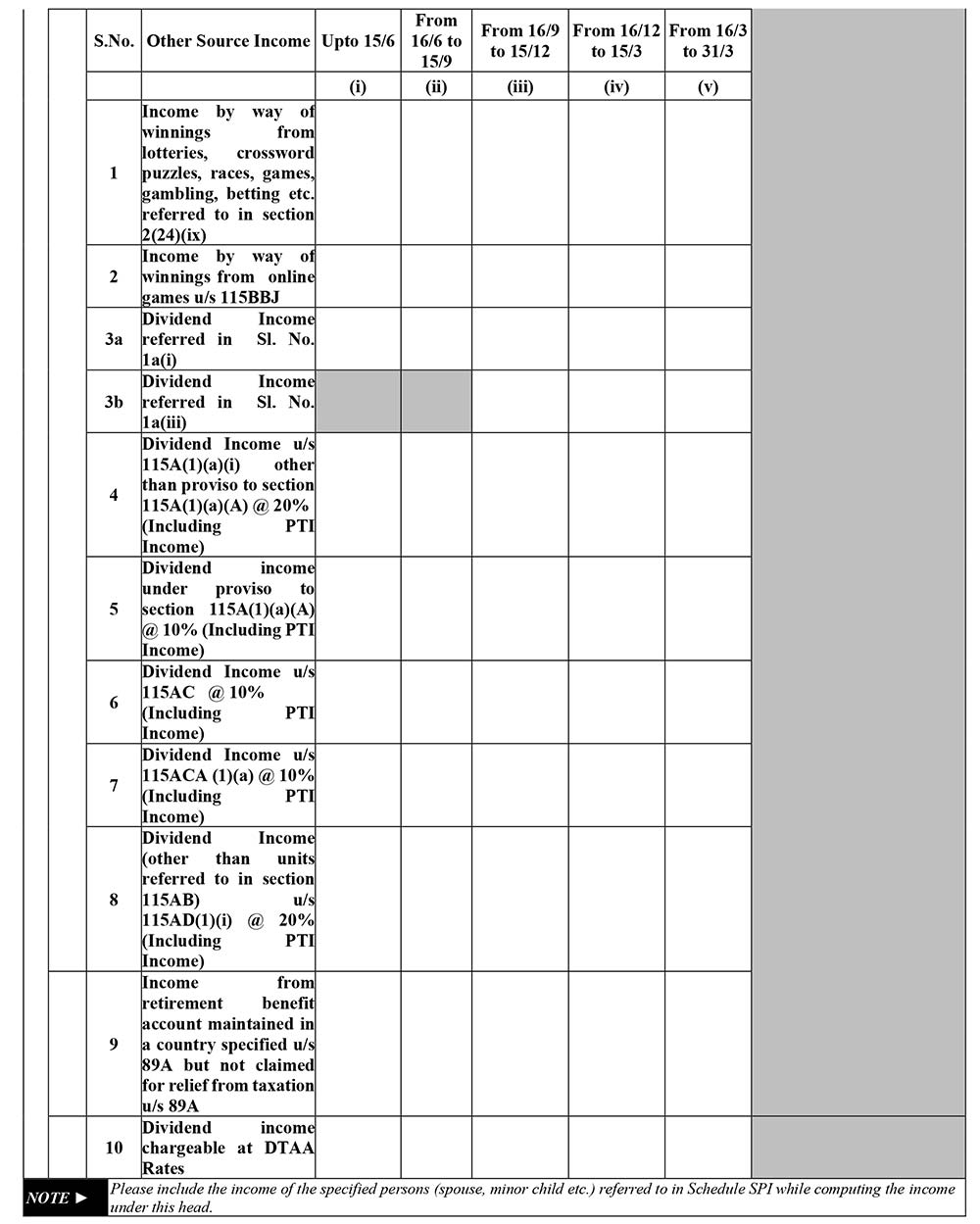

Schedule OS

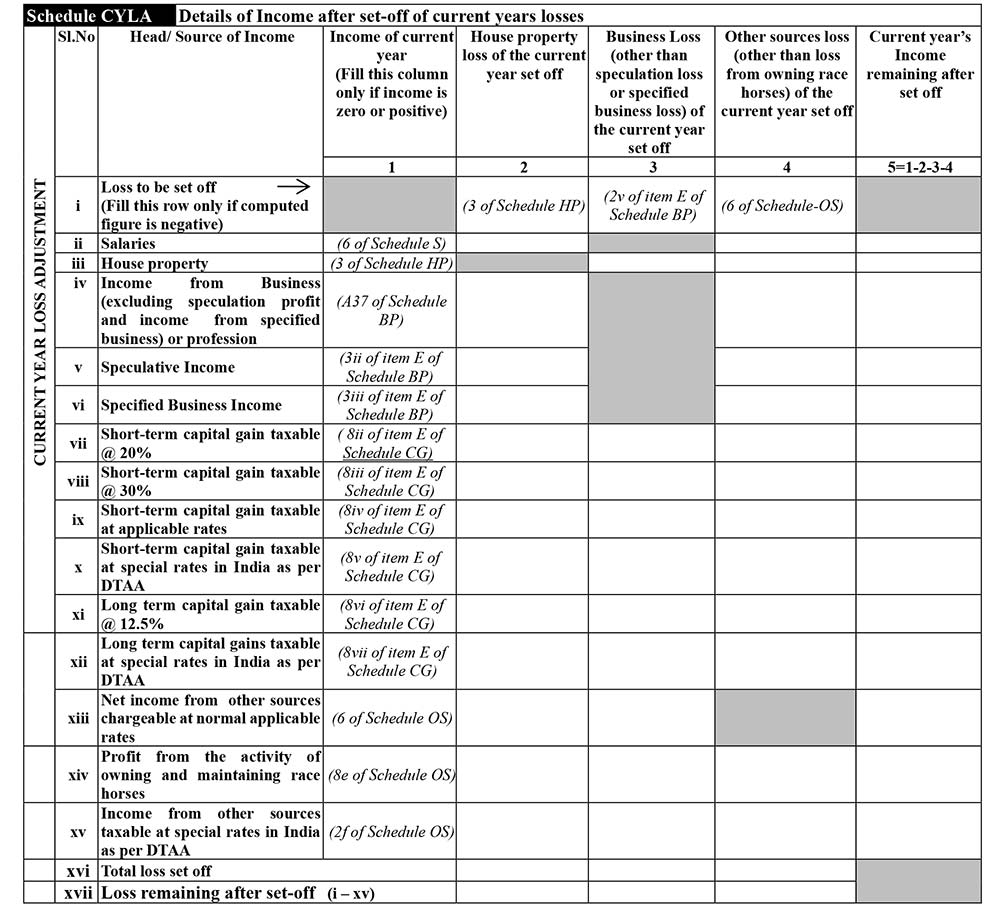

Schedule CYLA

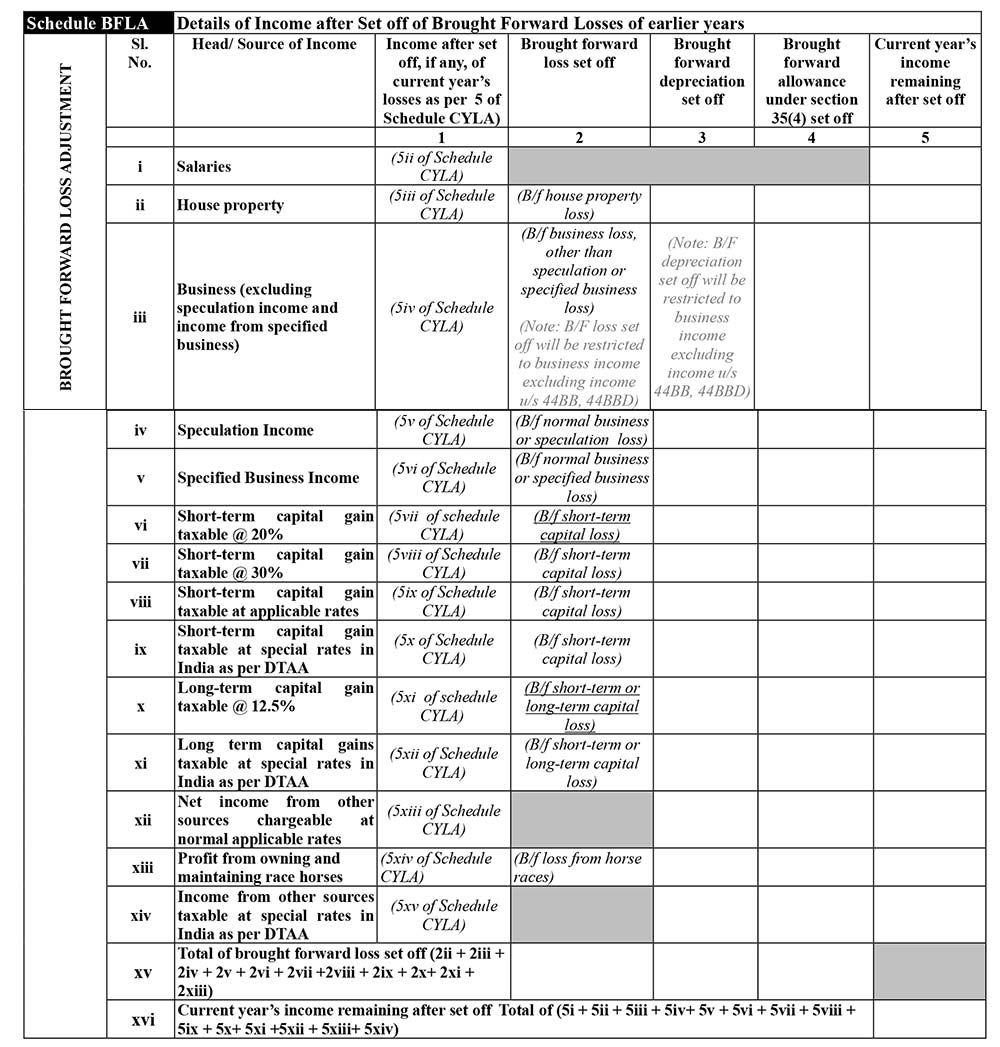

Schedule BFLA

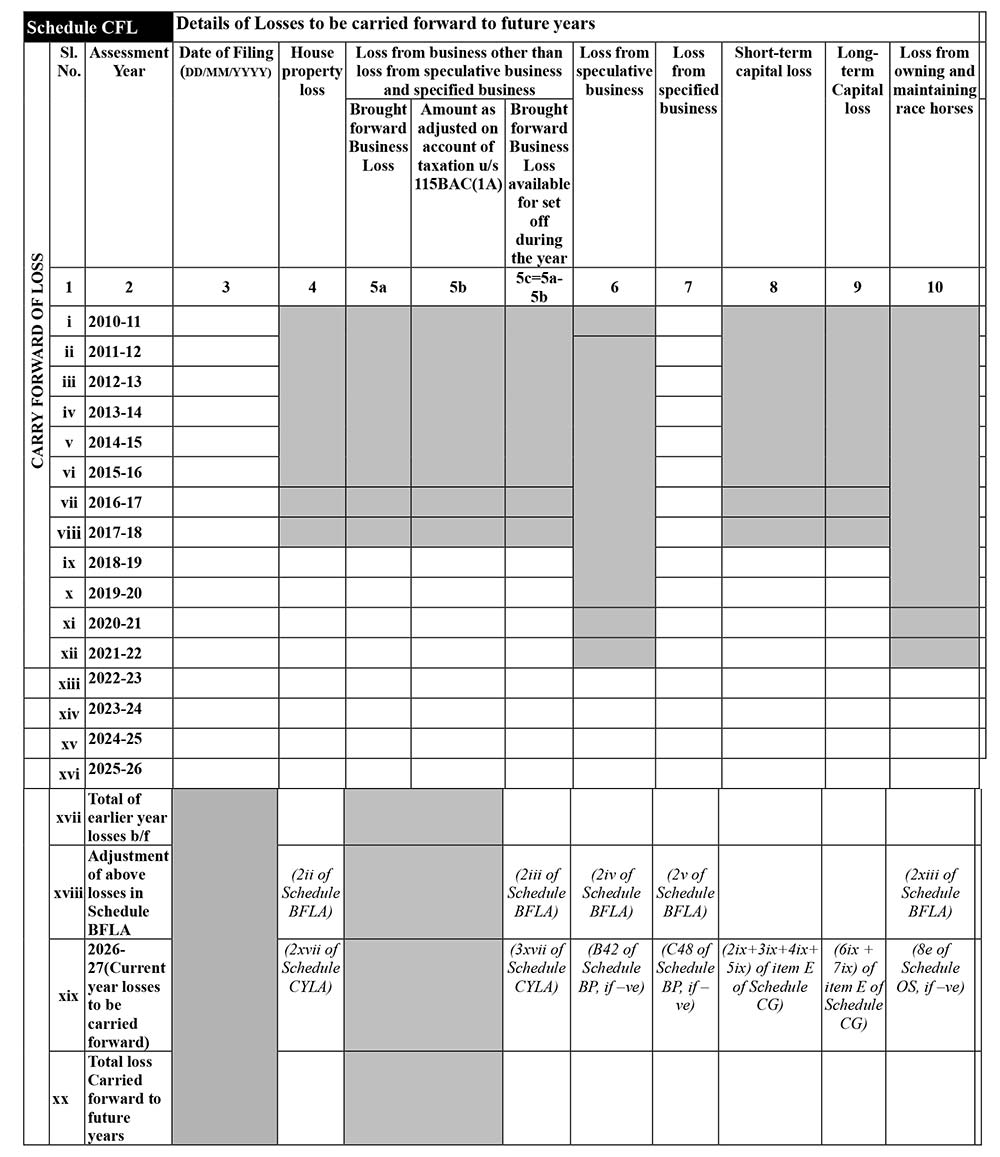

Schedule CFL

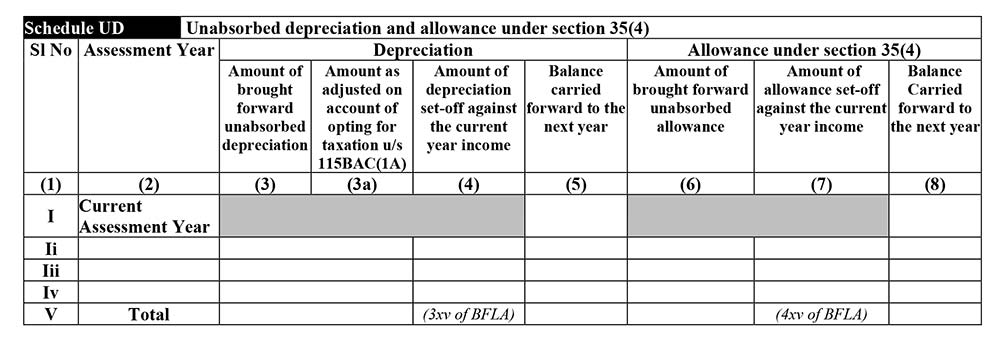

Schedule UD

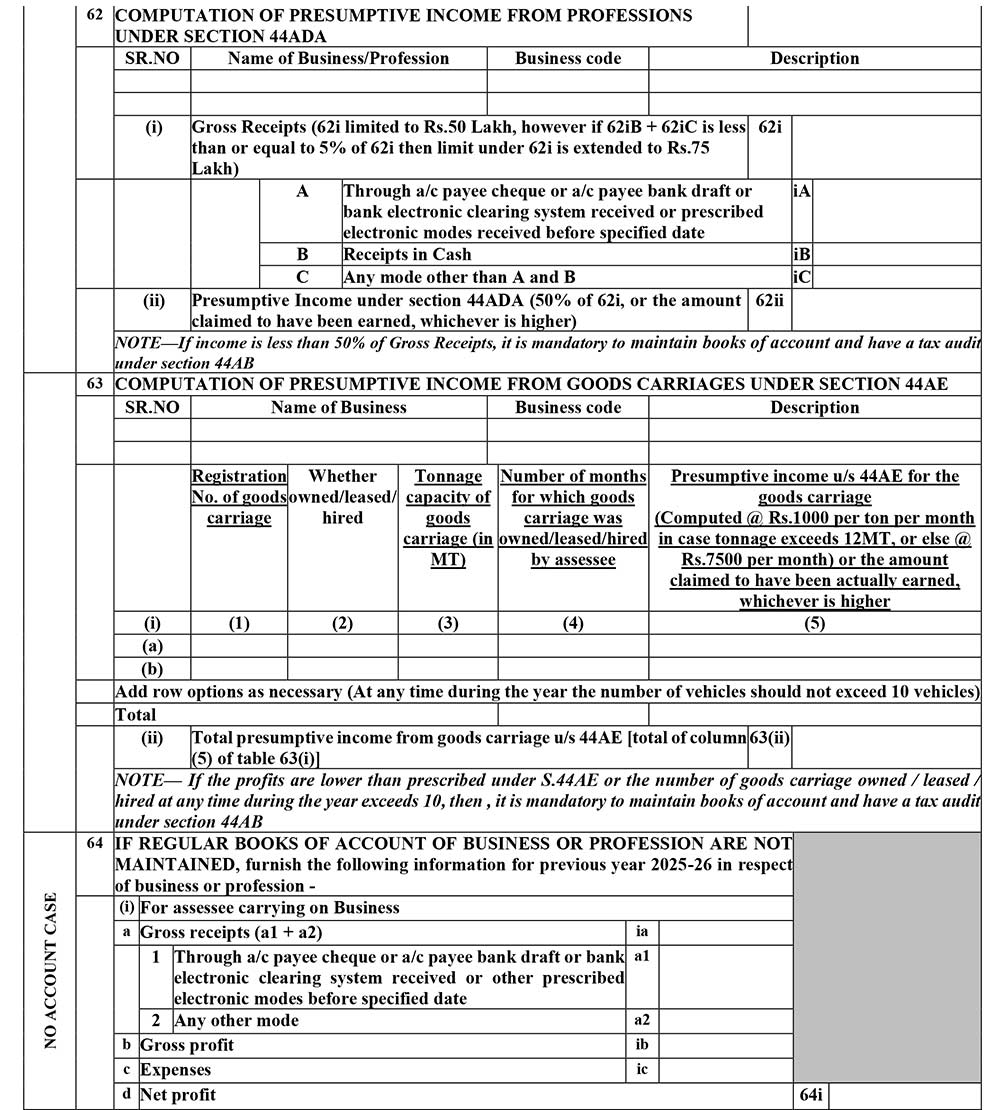

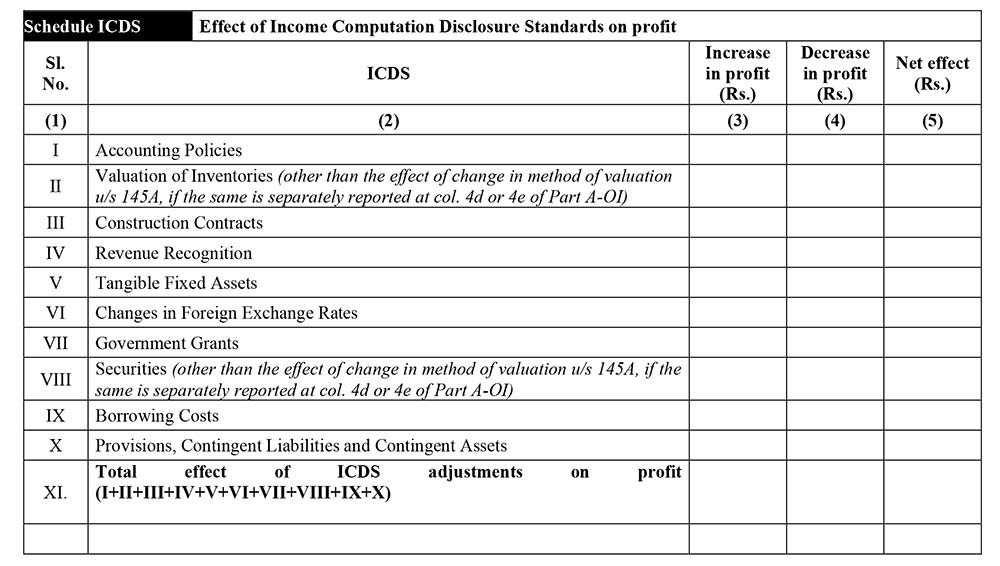

Schedule ICDS

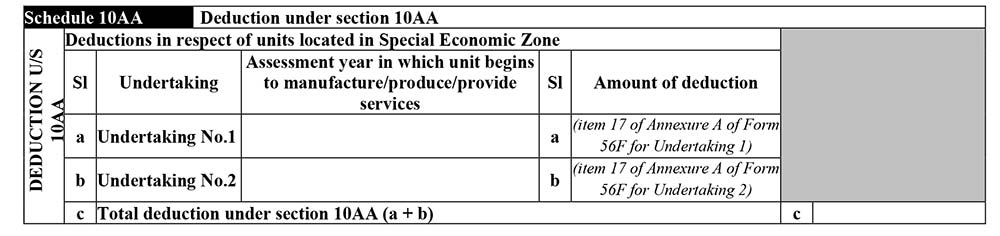

Schedule 10AA

Schedule 80G

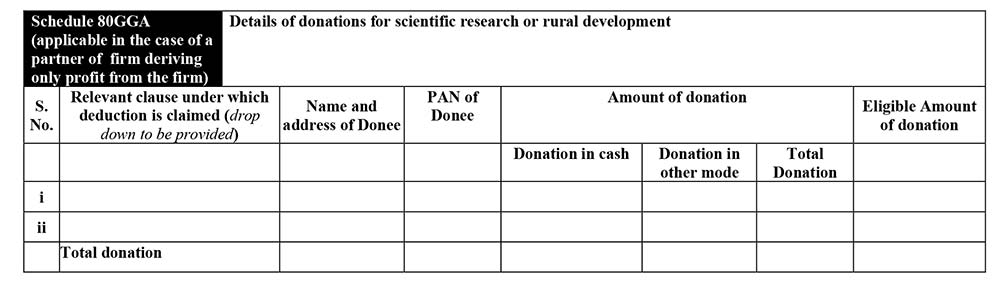

Schedule 80GGA

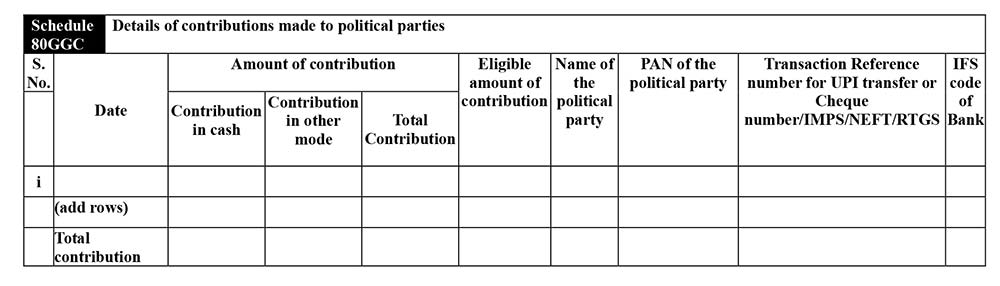

Schedule 80GGC

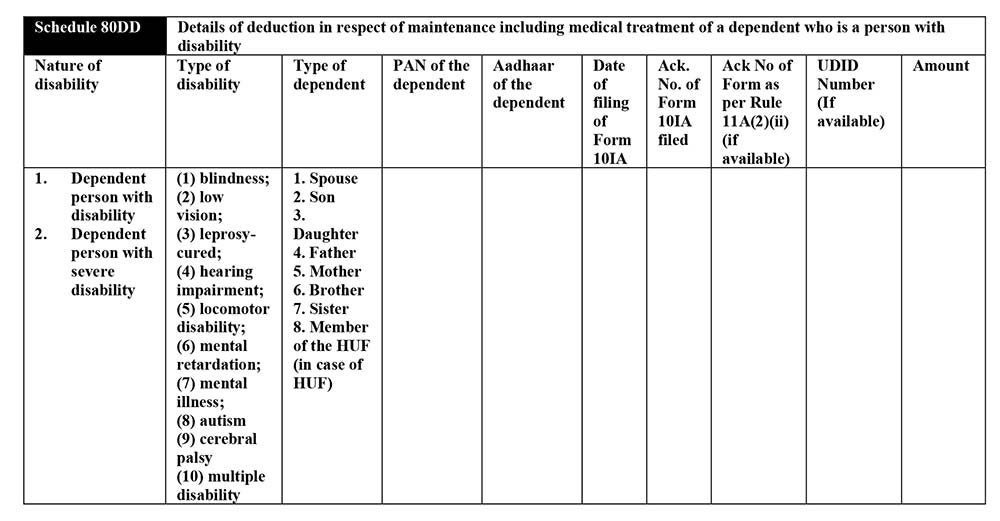

Schedule 80DD

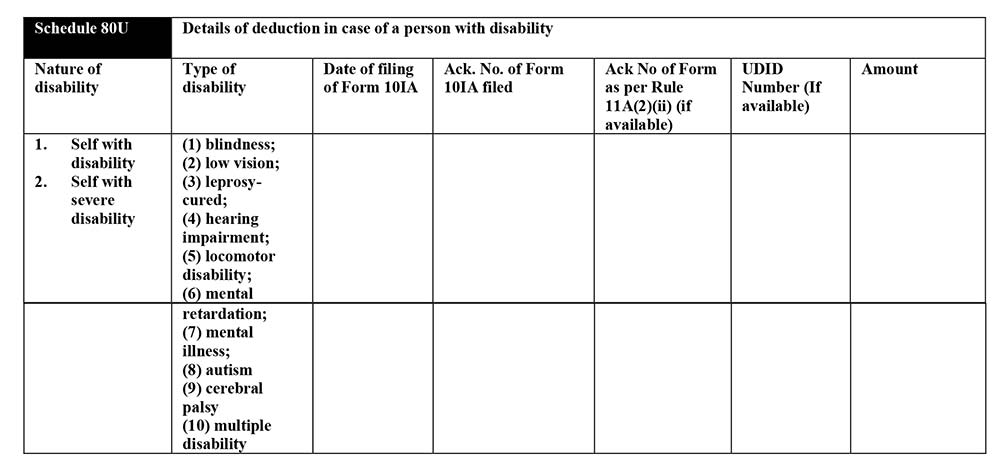

Schedule 80U

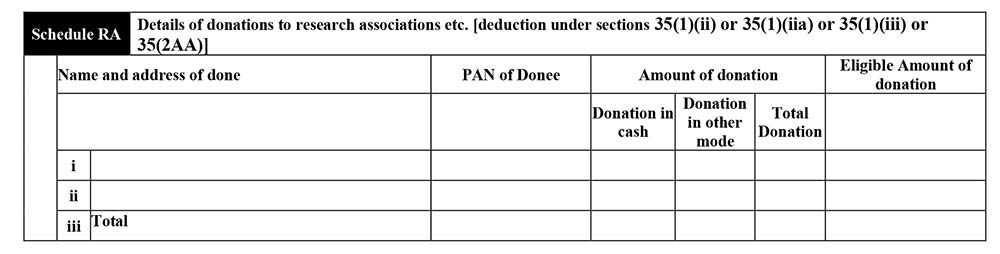

Schedule RA

Schedule 80-IA

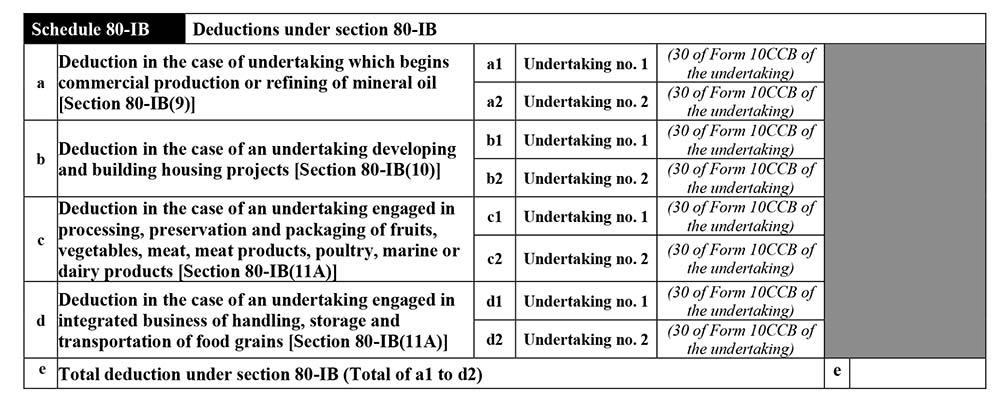

Schedule 80-IB

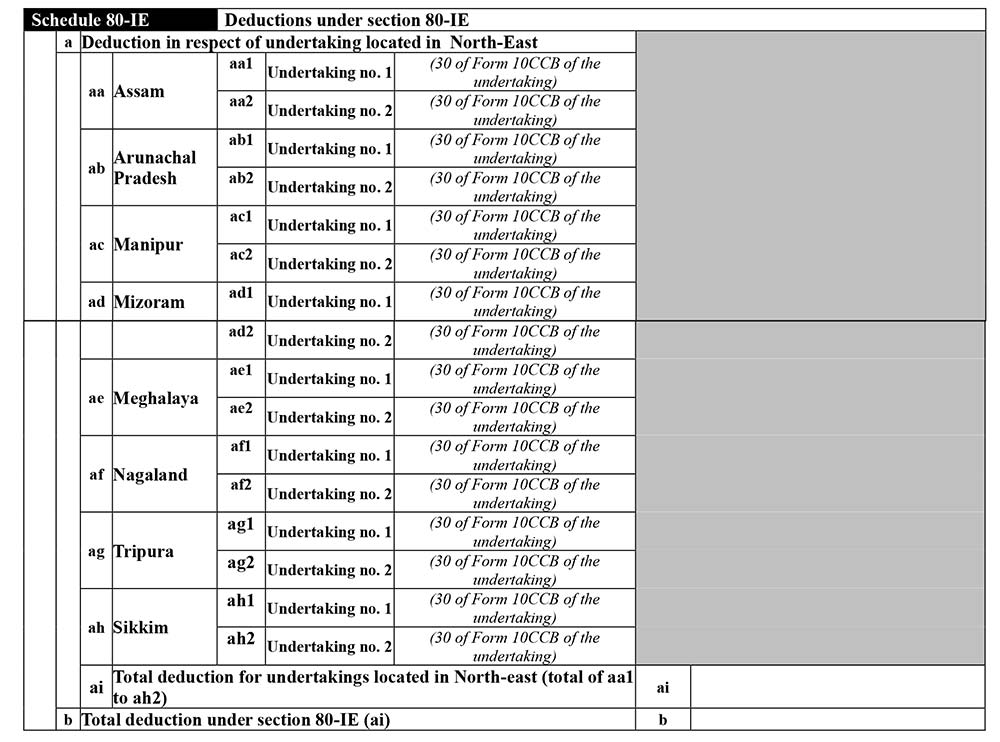

Schedule 80-IE

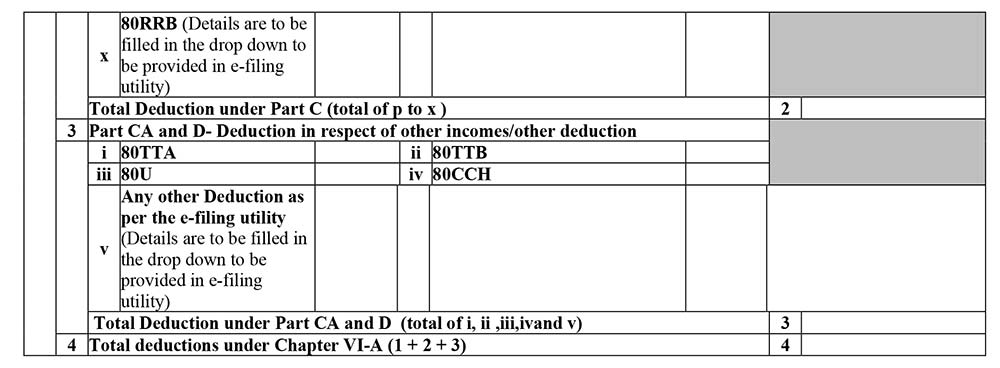

Schedule VI-A

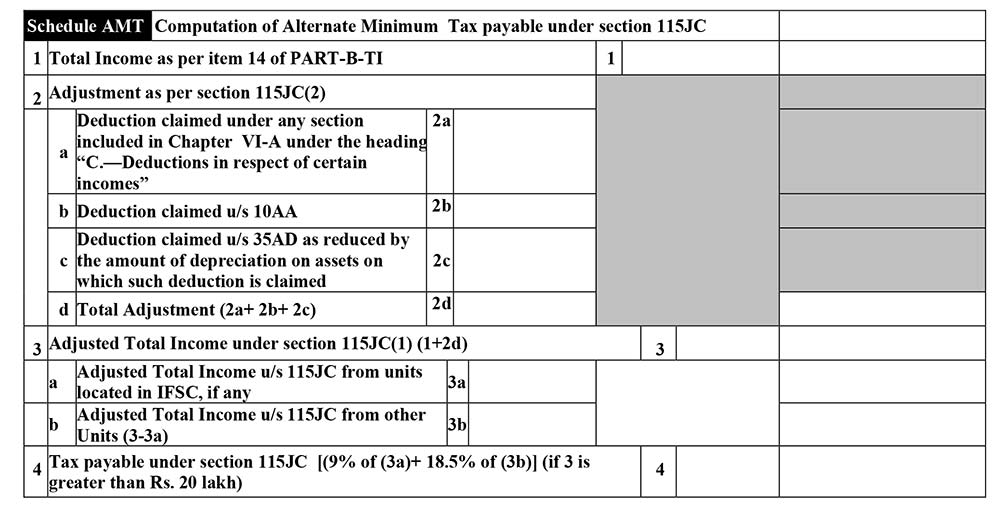

Schedule AMT

Schedule AMTC

Schedule SPI

Schedule SI

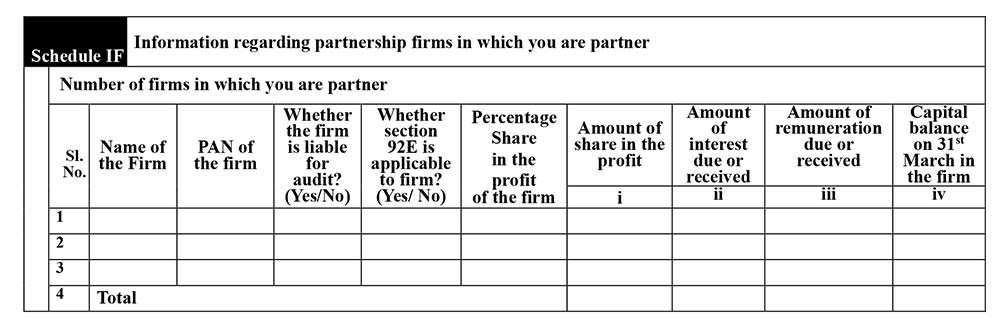

Schedule IF

Schedule EI

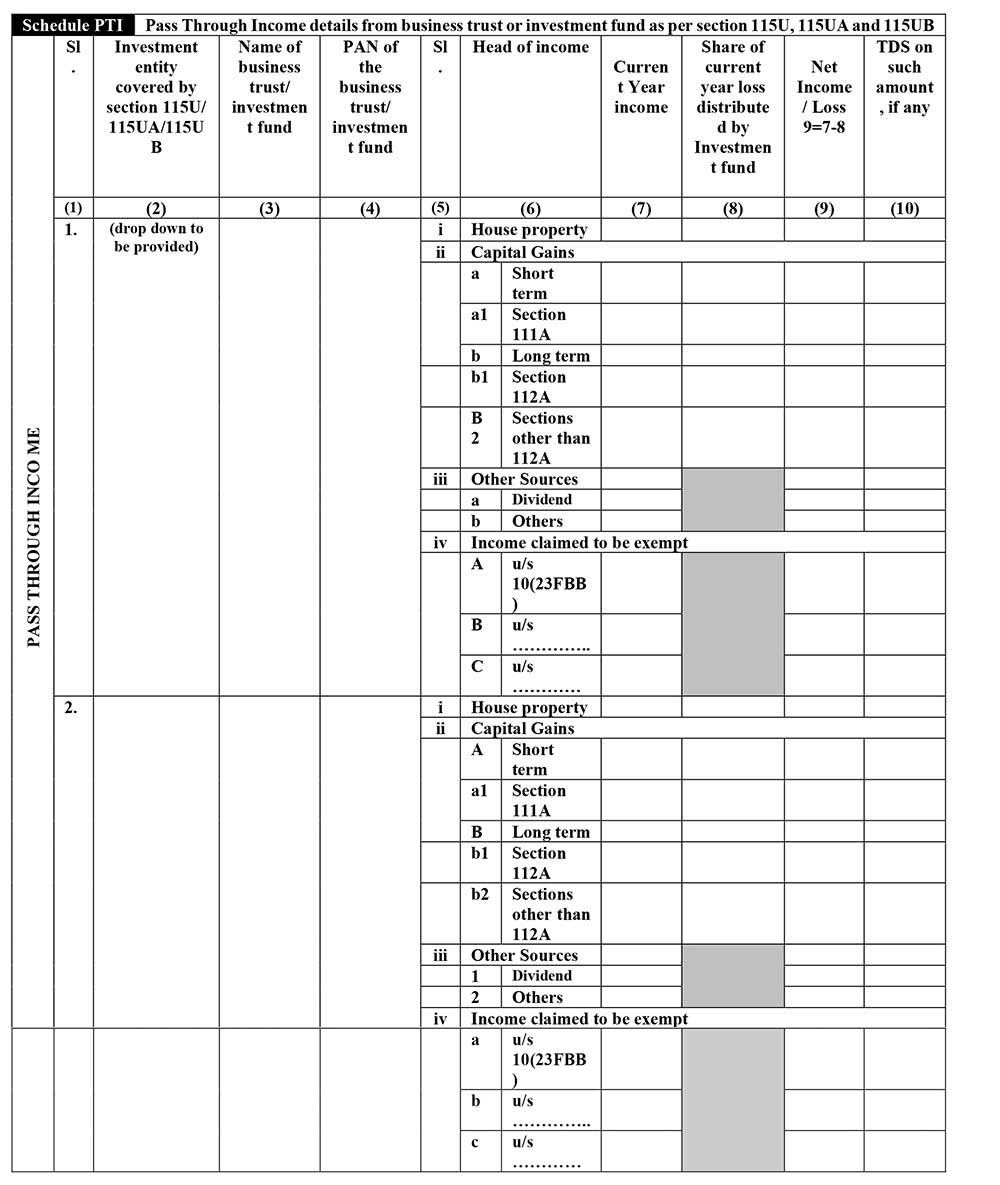

Schedule PTI

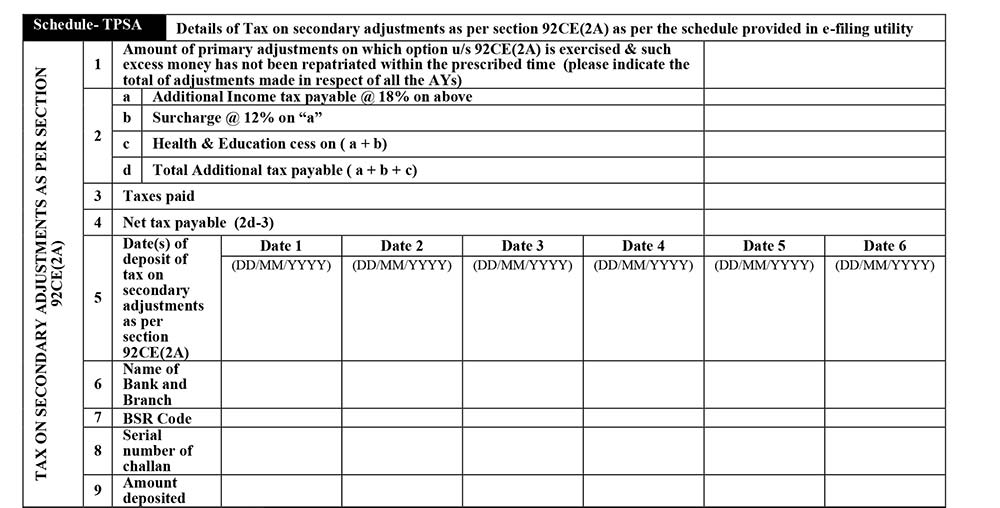

Schedule TPSA

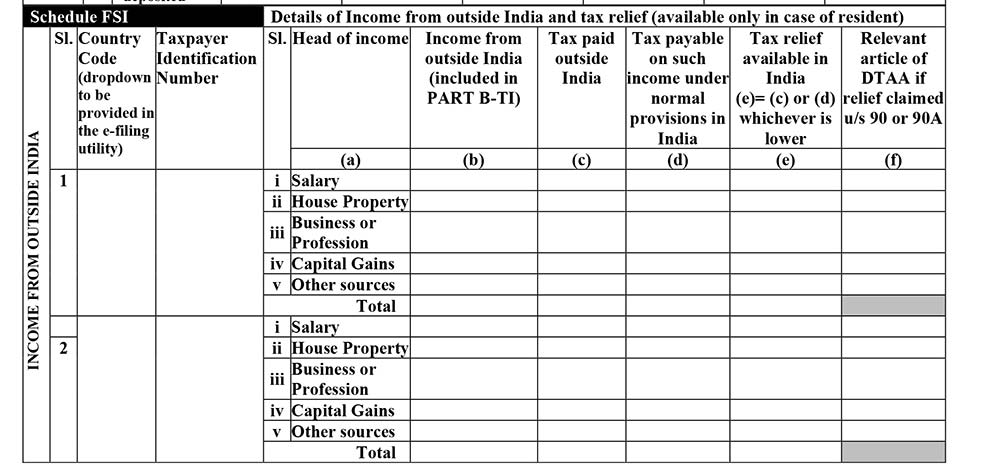

Schedule FSI

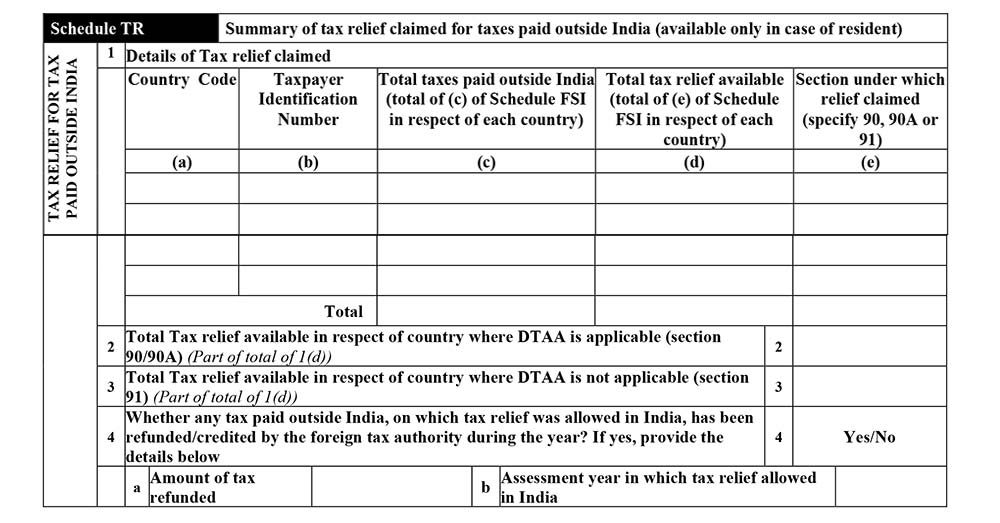

Schedule TR

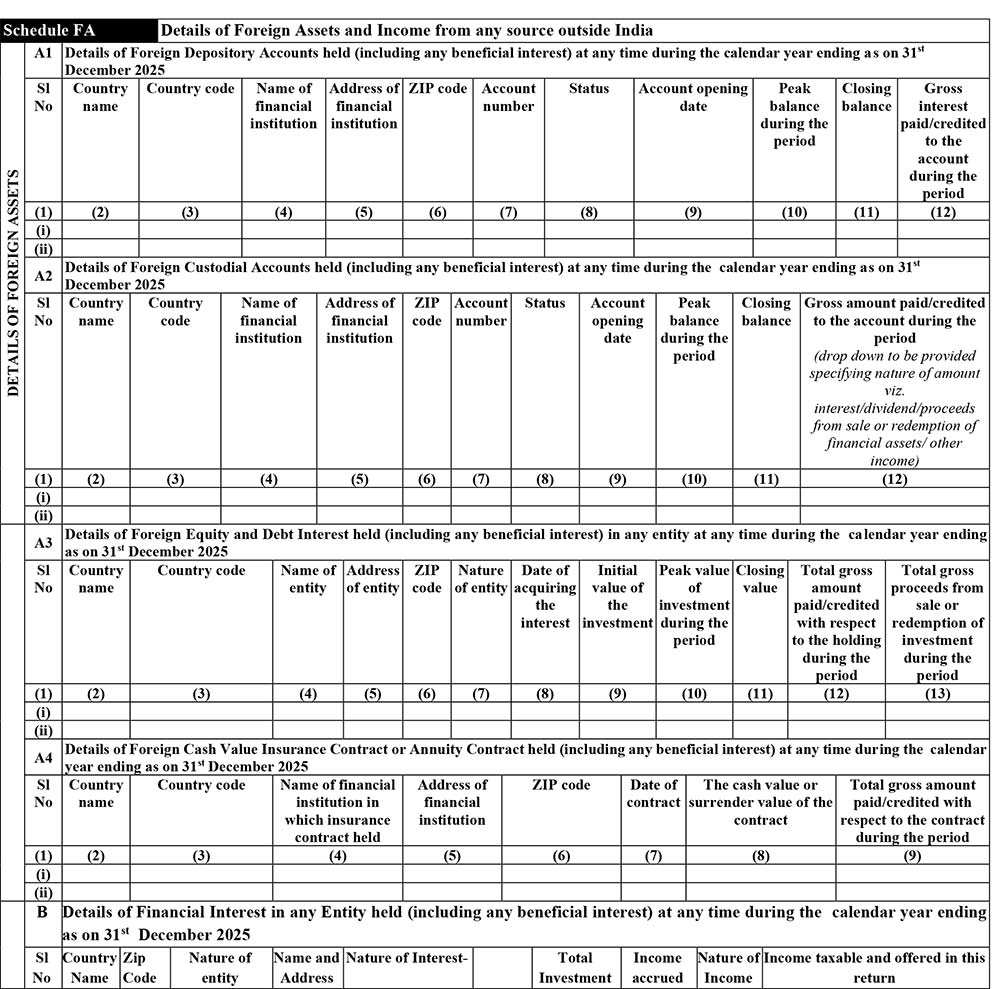

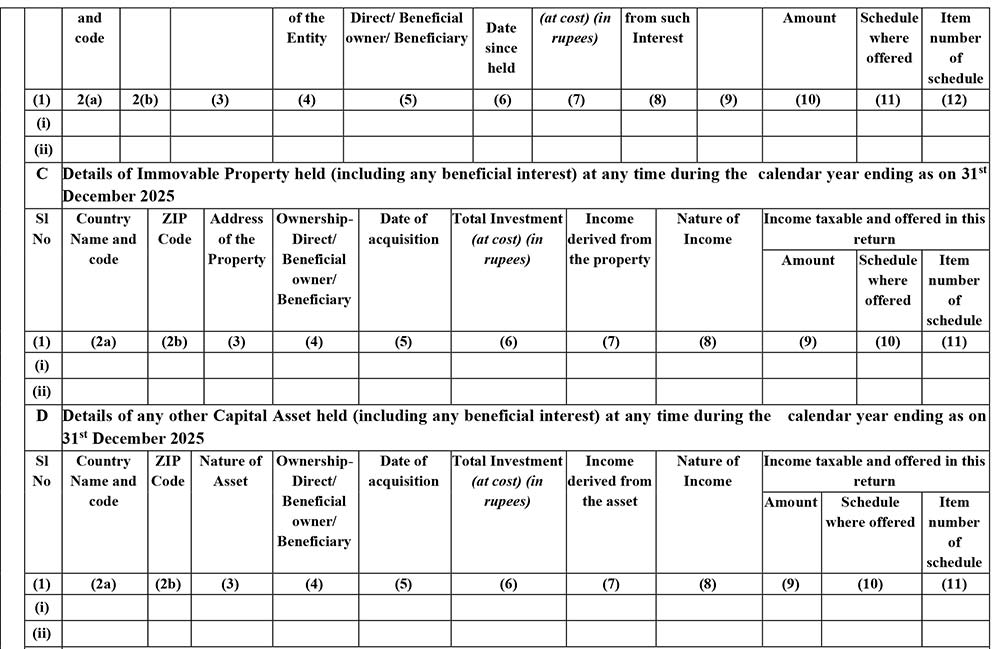

Schedule FA

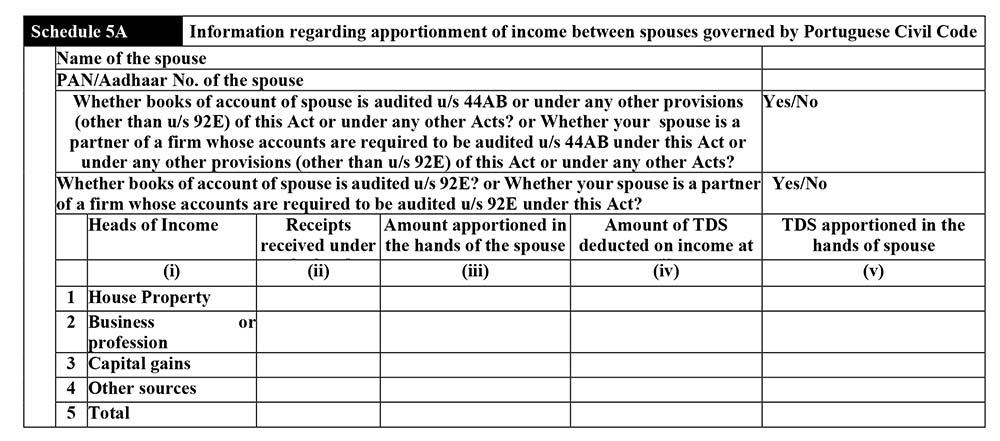

Schedule 5A

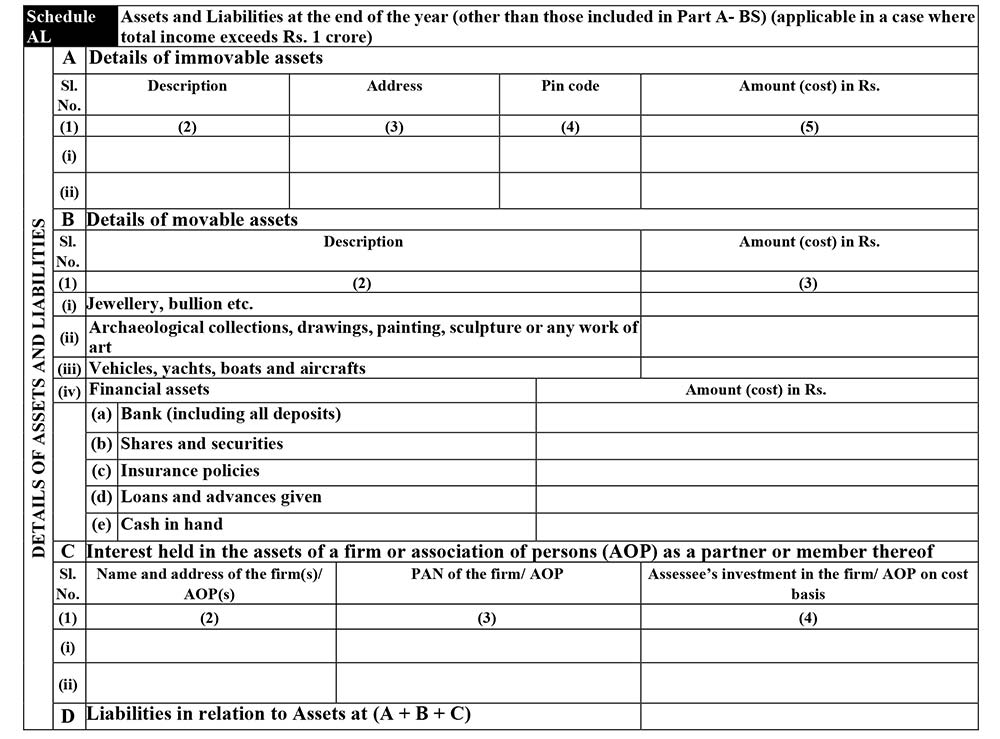

Schedule AL

Schedule GST

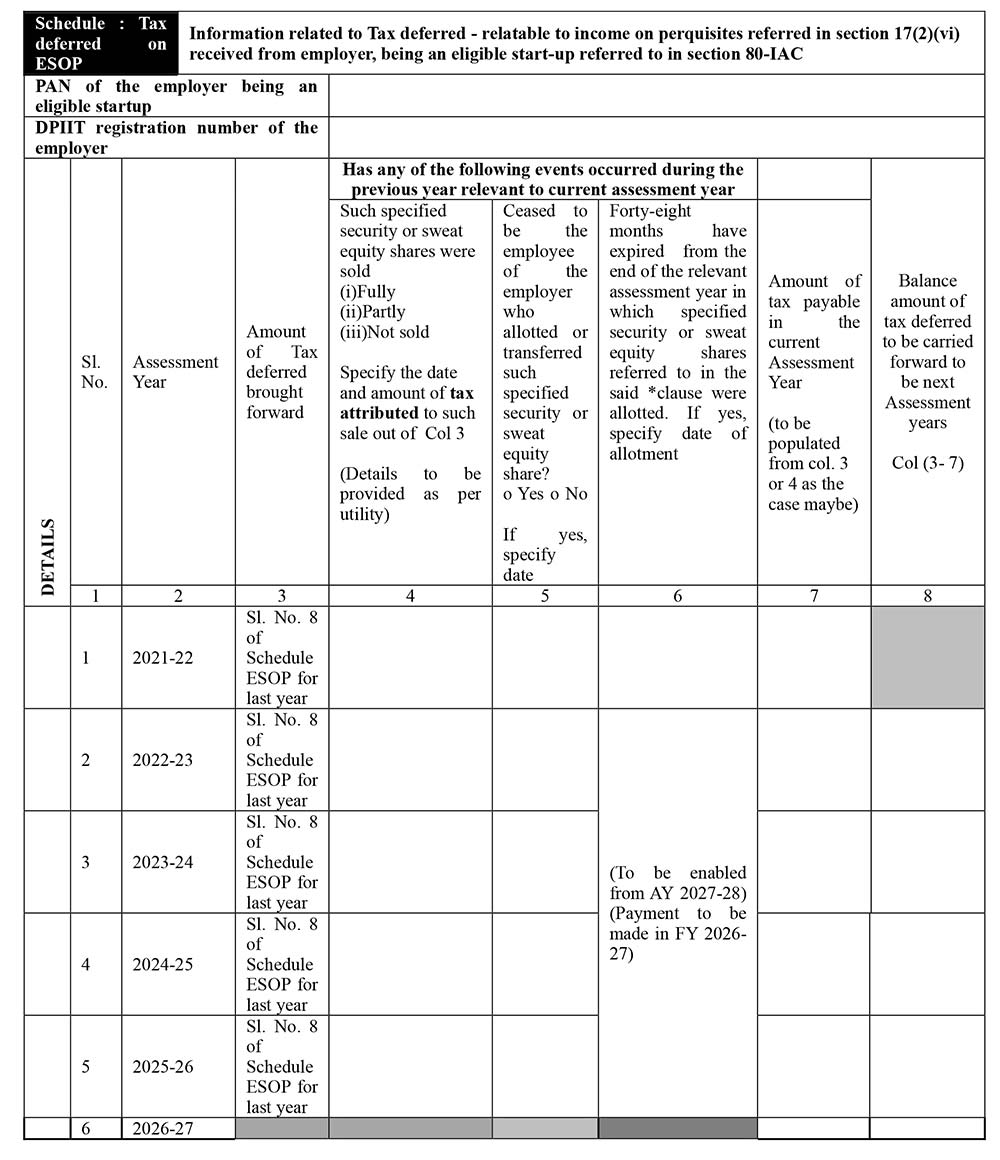

Schedule: Tax Deferred on ESOP

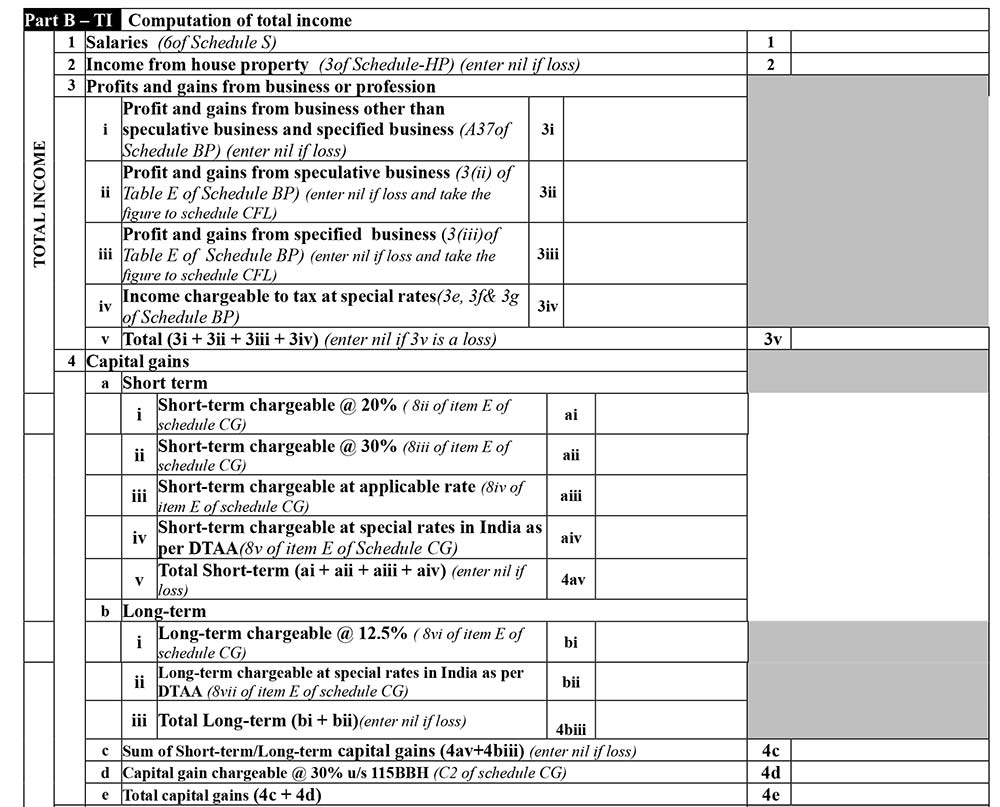

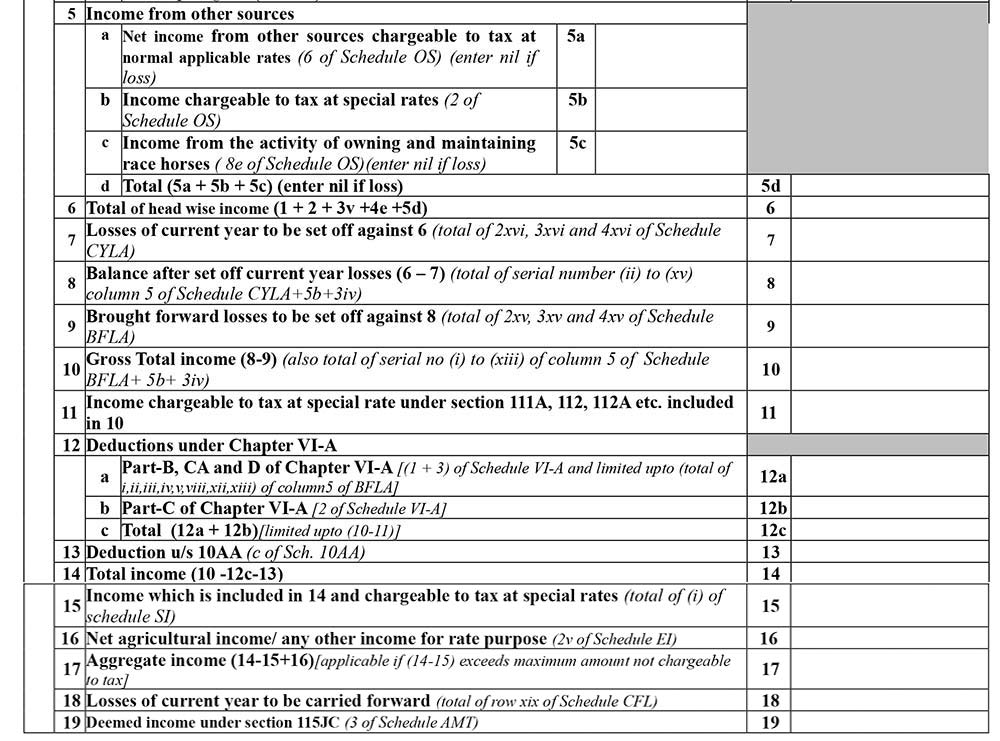

Part B- TI Computation of Total Income

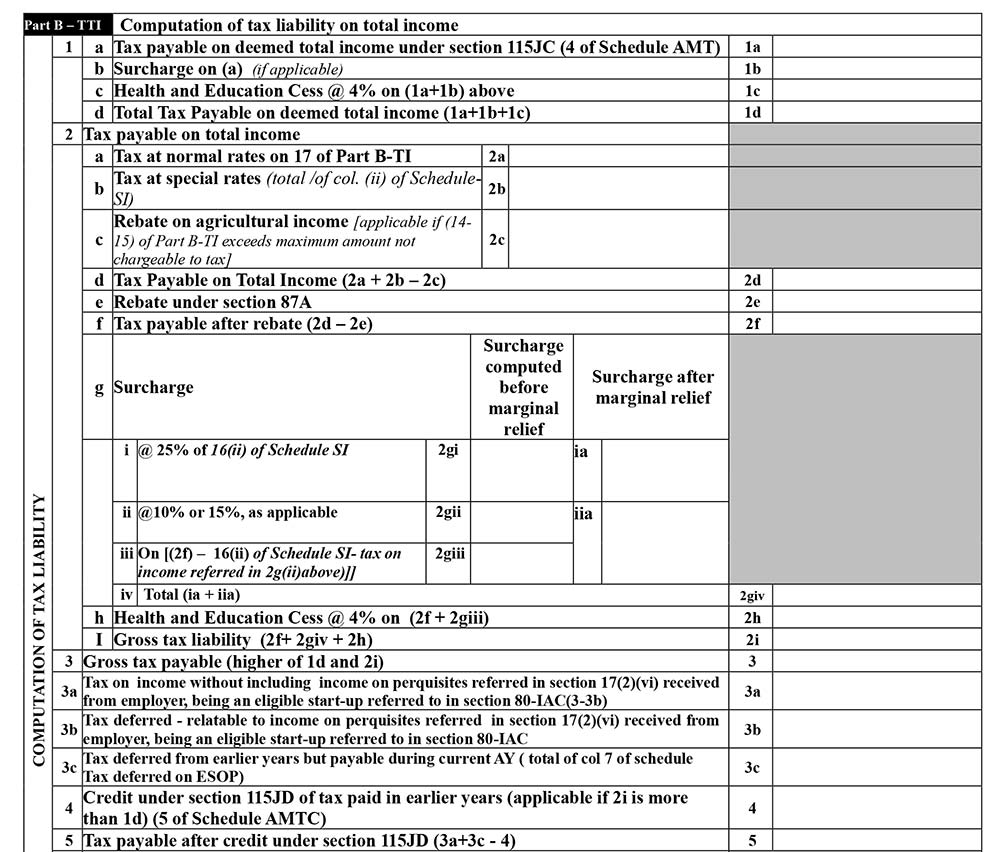

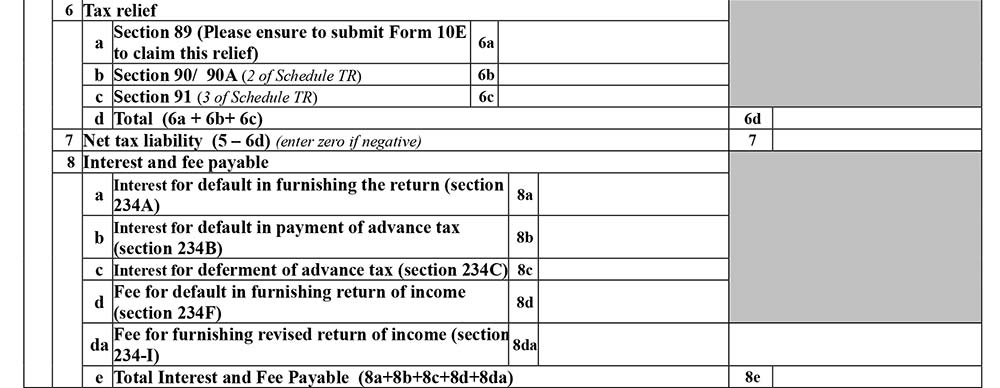

Part B- TII

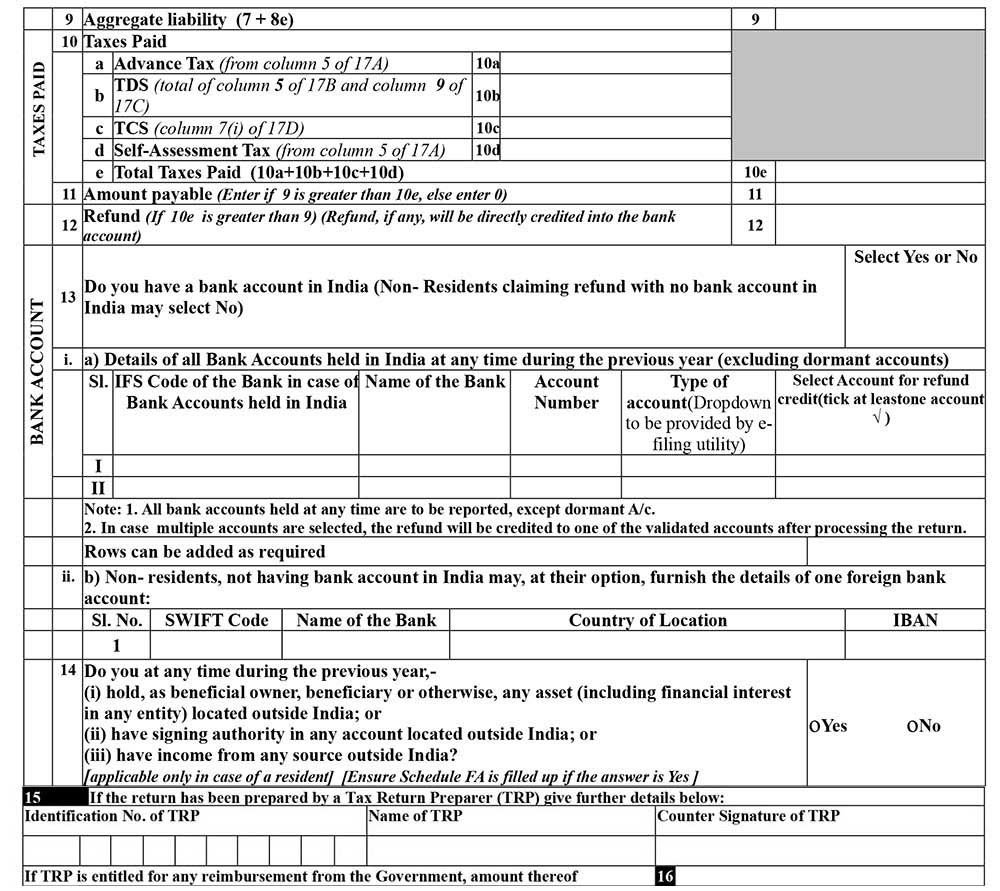

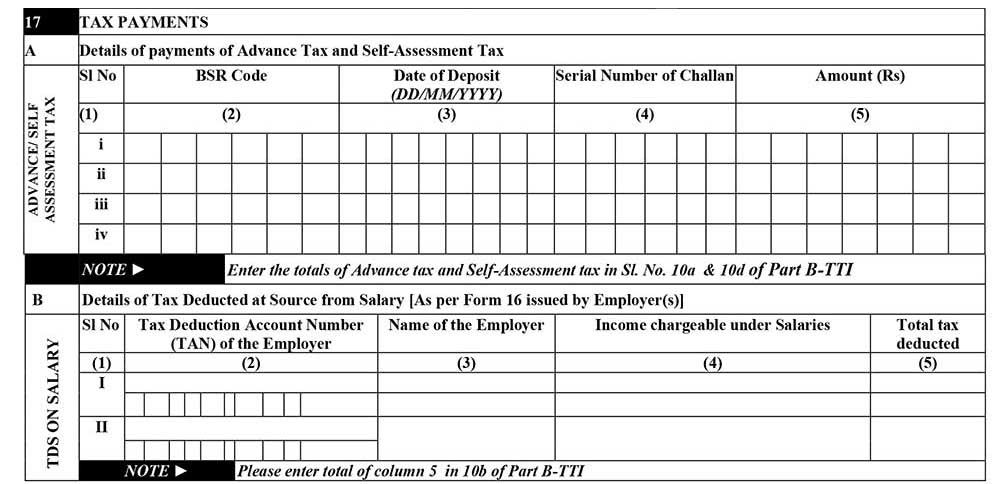

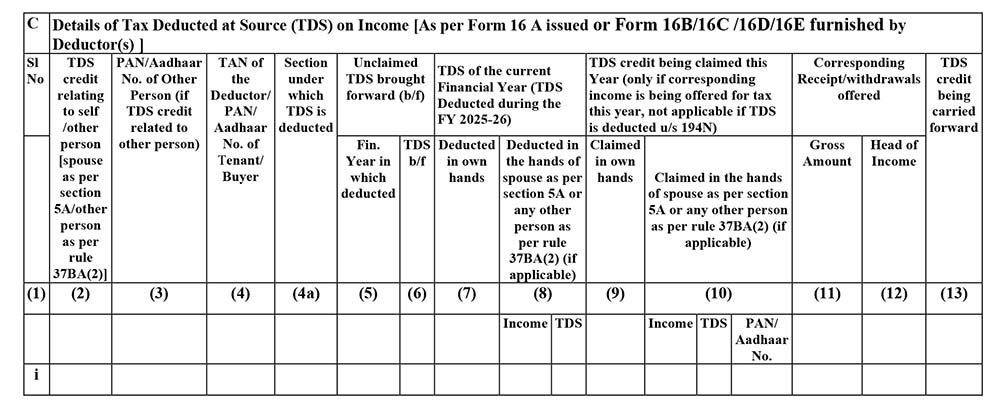

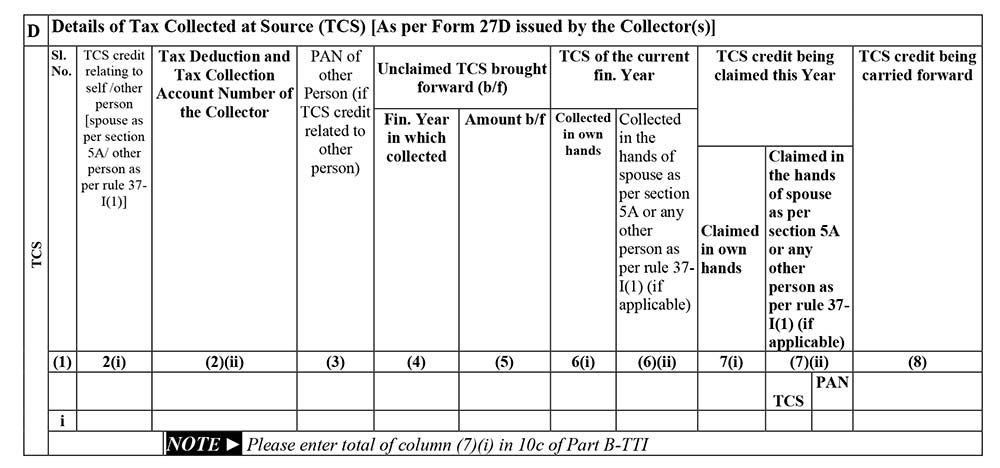

Tax Payments

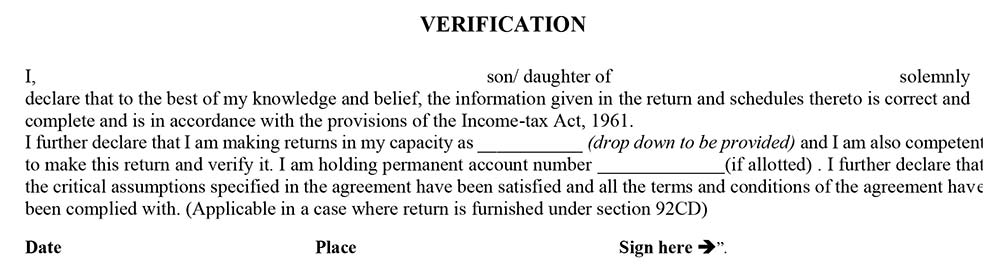

Verification

{kind=link}

Just checking in to see when the ITR-3 filing module for A.Y. 2026-27 will be live in the Genius / Gen IT software? The IT department launched the schema on June 18th, and my local system shows everything is up to date, but I still can’t see the ITR-3 option. Any idea on the exact date or timeframe for the rollout? Got a few clients waiting on this.

Whose ifsc code to mention in sec 80ggc client or political party