One of the best parts of the GST is the Input tax credit (ITC) which has been incorporated in the country as a major change to the tax structure. The same would permit the businesses to diminish their tax load and save money to invest in the development of the businesses. As per the Central Board of Indirect Taxes and Customs (CBIC), the input tax credit would count as a process to prevent the cascading of taxes or tax on tax.

Prior to GST, the credit for taxes charged through the central government was not available as a set-off for tax payments imposed via the state governments, and vice versa. The tax paid at each level may be used as a set-off for the payment of tax at each succeeding stage under the GST, nevertheless, the tax levied by the central or state governments is a component of the same tax system

Input tax credit in GST, As defined by section 2 (57) of the MGL (Model GST Law) and section 2 (1) (d) of the IGST Act, Input tax is related to a taxable entity which means the (IGST and CGST) in respect of CGST Act and (IGST and SGST) in respect of SGST Act is levied on every supply of goods or any services on the entity which is used by it or which is intended to to be consumed in the course of the business and subsumes the tax payable under sub-section (3) of section 7. In a simple way, an input tax credit defines that an entity can reduce the taxes it paid on the inputs at the time of paying the taxes on output.

Latest Update on ITC Under GST

- Budget 2026: Post-sale discounts can now be adjusted in the transaction value even without a prior agreement, provided a credit note is issued, and the recipient reverses the corresponding ITC.

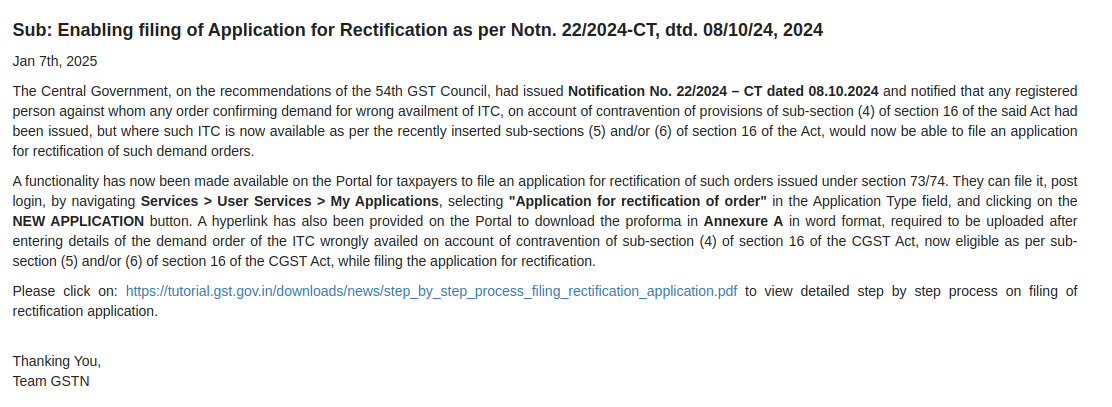

- A new functionality, ‘Application for Rectification,’ has now been enabled for taxpayers on the GSTN portal. [View more | Read PDF]

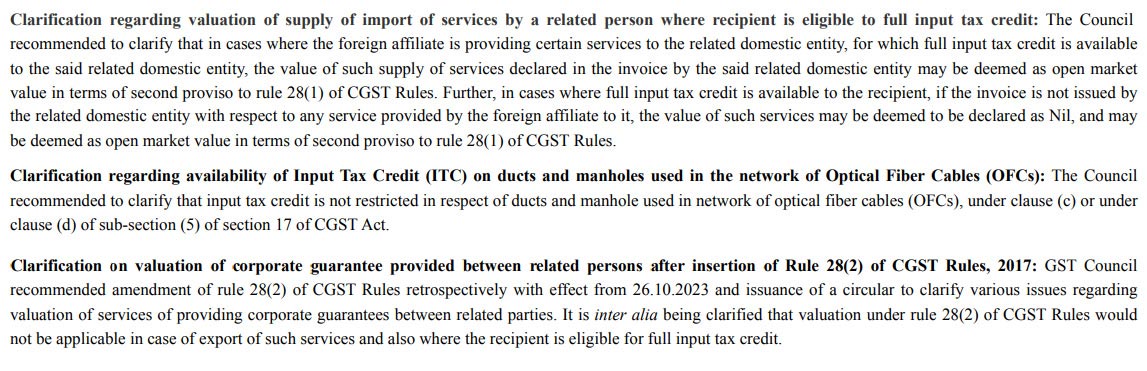

- ITC clarification regarding the supply of imported services, ducts, and manholes used for OFCs, etc in the 53rd GST council meeting. View more

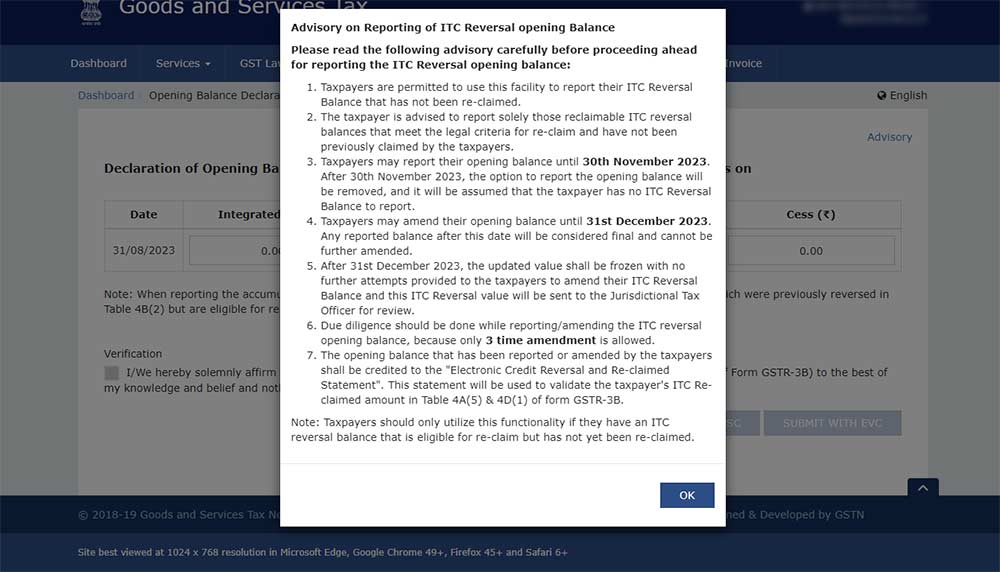

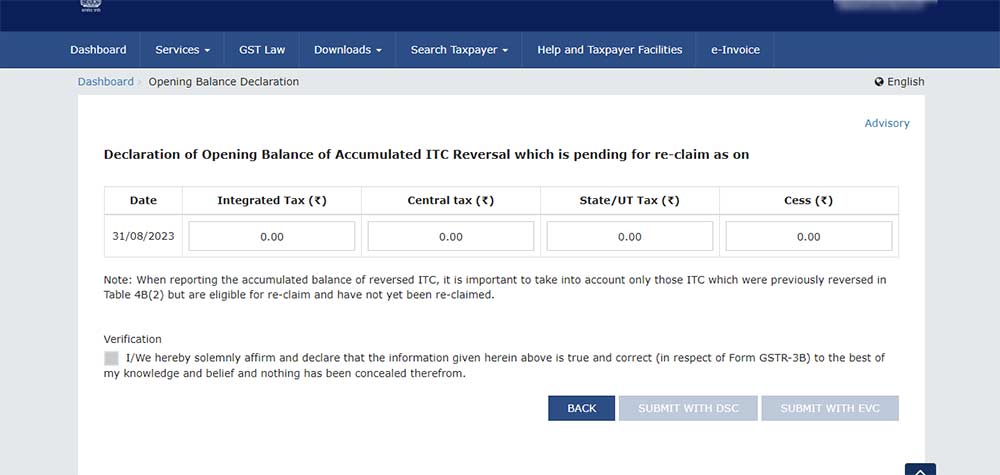

- The GST ITC reversal new advisory on reporting for opening balance is now live on the government portal. Read more, View more

- The Karnataka AAR has published the order for Attica Gold Private Limited. Rent, advertisement expenses, commission and professional expenses are eligible for GST ITC under the marginal scheme. Read Order

- “In sub-rule (4), in clause (b), after the words, ―the details of‖, the words, input tax credit in respect of‖ shall be inserted.”

- “A registered person, who has availed of input tax credit on any inward supply of goods or services or both, other than the supplies on which tax is payable on a reverse charge basis, but fails to pay to the supplier thereof, the amount towards the value of such supply along with the tax payable thereon, within the time limit specified in the second proviso to sub-section(2) of section 16, shall pay an amount equal to the input tax credit availed in respect of such supply along with interest payable thereon under section 50 while furnishing the return in FORM GSTR-3B for the tax period immediately following the period of one hundred and eighty days from the date of the issue of the invoice.”

- “Where the said registered person subsequently makes the payment of the amount towards the value of such supply along with tax payable thereon to the supplier thereof, he shall be entitled to re-avail the input tax credit referred to in sub-rule (1).”

- “In clause (c), for the words, letters and figure, ―and shall be furnished in FORM GSTR2‖, the words, letters and figure, ― and the balance amount of input tax credit shall be reversed in FORM GSTR-3B‖ shall be substituted.” Read More

47th GST Council Meeting Updates

- “Refund of accumulated ITC not to be allowed on flowing goods:”

- Edible oils

- Coal

- “Like CETPs, common bio-medical waste treatment facilities for treatment or disposal of biomedical waste shall be taxed at 12% so as to allow them ITC”

- “Room rent (excluding ICU) exceeding Rs 5000 per day per patient charged by a hospital shall be taxed to the extent of amount charged for the room at 5% without ITC.”

- “Due to ambiguity in GST rates on supply of ice-cream by ice-cream parlours, GST charged @ 5% without ITC on the same during the period 1.07.2017 to 5.10.2021 shall be regularized to avoid unnecessary litigation.”

- “Change in formula for calculation of refund under rule 89(5) to take into account utilization of ITC on account of inputs and input services for payment of output tax on inverted rated supplies in the same ratio in which ITC has been availed on inputs and input services during the said tax period. This would help those taxpayers who are availing ITC on input services also.”

- “Re-credit of the amount in electronic credit ledger to be provided in those cases where erroneous refund amount sanctioned to a taxpayer on account of accumulated ITC or on account of IGST paid on zero-rated supply of goods or services, in contravention of rule 96(10) of the CGST Rules, is deposited by him along with interest and penalty, wherever applicable. A new FORM GST PMT-03A is introduced for the same. 4. This will enable the taxpayers to get re-credit of the amount of erroneous refund, paid back by them, in their electronic credit ledger.”

- “Retrospective amendment in section 50(3) of CGST Act, with effect from 01.07.2017, to provide that interest will be payable on the wrongly availed ITC only when the same is utilized.”

- “Export of Electricity. This would facilitate the exporters of electricity in claiming refund of utilized ITC on zero-rated supplies.”

What Does GST’s ITC Mean?

A GST-registered individual or firm can effectively claim the tax they paid on their inward supplies, inputs, or raw materials as a credit when they are paying taxes on their outward supply or sales of commodities.

What is Net Input Tax Credit (ITC)?

- Net ITC is the input tax credit which is availed by the taxpayer in his ITC ledger or for the month in which the taxpayer has sought. It is the amount of ITC taken by the taxpayer through table 4 of his GSTR 3B returns of the tax period refund is sought.

Now let’s see, how to calculate input tax credit, for example, if a tax payable on the output is INR 450 and the tax paid on the input is INR 300, then the entity can claim an Input tax credit of INR 300 and the remaining amount of INR 150 will be needed to deposit in taxes.

What Method is Used to Compute GST ITC?

For instance, you are an office builder and home furniture and purchase raw materials like wood for Rs 50,000 at a GST of 18%. Rs 9000 will be the tax filed. You sell the furniture that has been made for Rs 1 lakh and charge an 18% GST which amounts to Rs 18000 through your client. Rs 1.18 lakh is the revenue incurred through selling the furniture.

You are authorized to deduct the tax amount that stood at Rs 9000 which has been paid by you during purchasing the raw material. Therefore your total tax liability shall merely be Rs 9000 rather than Rs 18000. The total GST payable minus GST paid is the net GST paid on the raw materials that have been purchased.

How can Input Tax Credits be Claimed under GST?

For claiming an input tax credit, one must occupy a tax invoice or a debit note which is issued by a registered dealer.

The second thing, which must be kept in mind is that one should have received goods and services, and the taxed purchases have been deposited or paid to the government authority by the supplier in form of cash or by claiming the input tax credit.

For Claiming the GST ITC What Documents Would be Needed?

Invoice, debit note, and bill of supply from the supplier, the invoice issued identical to the bill of supply if the sum is less than Rs 200, bill of entry or other pertinent papers, and document from input service distributor are documents needed to file ITC.

Who Will be Qualified for the GST ITC?

Beyond registering with GST and filing taxes the businesses should secure the tax invoice or debit note from the supplier. As mentioned under section 41 of the GST Act, the input tax must be needed to get paid. The individual must be needed to file for the returns mentioned under section 39 of the GST Act, invoice payment should have been incurred within 180 days, GSTIN of supplier and recipient, and definition of goods and services. All the goods or services must be obtained by the individual.

No ITC on Warehouse Construction for Rent

Recently The Authority for Advance Ruling (AAR), Madhya Pradesh stated that the input tax credit will not be available on the goods and services taken and used on the construction of warehouses and the same are deployed for rent as per the Section 17(5)(d) of CGST Act, 2017.

Then, it must be ensured that the supplier has filed for the GST returns.

How to Avail the Input Tax Credit via Different Routes?

- For making payments to IGST: Take input tax credit from the SGST, CGST and IGST which is paid on the purchases.

- For making payments to CGST: Take input tax credit from the CGST and IGST which is paid on the purchases.

- For making payments to SGST: Take input tax credit from the SGST and IGST which is paid on the purchases.

Note: As per the current notification, the govt has modified some ITC set of rules under which the ITC for IGST is first used completely then the CGST & SGST will be used i.e.

- For making payments to IGST: Take input tax credit from the IGST and then CGST & SGST.

- For making payments to CGST: Take input tax credit from the IGST & CGST

- For making payments to SGST: Take input tax credit from the IGST and SGST.

Here is Shown a GST Input Tax Credit Example Which Will Clarify in a Simple Manner:

Assume that there is a seller Mr A and he sold his goods to Mr B. Now here Mr B which is a buyer will be eligible to claim the input tax credit on purchases based on the invoices. So,

Step 1: Accordingly, Mr A will be uploading the details of all the tax invoices issued in GSTR 1.

Step 2. All the details in accordance with the sales to Mr B will auto-populate in GSTR 2A, and the same data will be taken when Mr B will file GSTR 2 (i.e. details of inward supply). (Currently, the GSTR 2 is suspended and not available on the portal, therefore, Mr. B can avail credit in the GSTR- 3B)

How GSTR Forms Operate & How They Reconciled?

The GST Council has appointed 2 types of forms which are mandatory to be filled in every month, namely GSTR 1 for all the sales done and GSTR 2 for all the purchases done. (Currently, GSTR 2 forms are not available on the portal)

The GSTR 1 form will have to be filled on the 10th of every month includes all the details regarding the sales done by the business unit. There is also GSTR form 1A (Currently, GSTR 1A forms are not available on the portal) included which is majorly for the importance of reconciliation.

Basically, Details of outward supplies as added, corrected or deleted by the recipient in Form GSTR-2 (Currently, GSTR 2 forms are not available on the portal) will be made available to the supplier. The due date for the particular form is 20th of succeeding month.

Recommended: GST Forms: Return Filing, Registration, Rule, Refund, Challan, Invoice

Coming to the GSTR 2 form, it is for the details of inward supplies of taxable goods and/or services for claiming the input tax credit. Additions (Claims) or modifications in Form GSTR-2A should be submitted in Form GSTR-2.

On the basis of this, a form GSTR 2A is available which emerges with Auto-populated details of inward supplies made available to the recipient on the basis of Form GSTR-1 furnished by the supplier. The due date of this form is On 11th of the succeeding Month.

Post-GST era, the government allowed business entities to file their GST returns on a self-assessment basis in the starting two months. GSTR 3B is a return form for filing returns under the Goods and Services Tax Regime, TRAN I is the form in which business entities will be required to furnish all the information details of credit that they are claiming for the payment of taxes they had already paid before the implementation of the new tax regime.

According to Finance Minister Arun Jaitley, “Transitional forms (TRANS 1) for claiming input tax credit is now available at GSTN portal, under the Goods and Services Tax Regime.

A senior official of the revenue department said, The transitional form is almost ready and we are working to upload it by 21st August so that businesses can start filing TRAN 1.” All normal taxpayers registered in the new tax regime are required to file July month returns by 25th August which was passed out.

What is the Method to File the Input Tax Credit?

- Log in to the GST portal http://www.gst.gov.in and tap on Services > Returns > ITC Forms

- In the GST ITC-01 box, tap on the ‘Prepare Online

- Choose your relevant section from the claim made under the drop-down list.

- Fill in the information for creating the invoice like GSTIN, Invoice number and date, and item details including goods type, description of inputs, unit quantity code, quantity, value, and amount of ITC claimed; and click on ‘Save’

- Tap on ‘Preview’ to preview the form’s draft and then tap on ‘Submit’

- Tap on ‘Proceed’ on the pop-up alert

- Prior to filing the submitted form you shall need to update your Chartered Accountant (CA)/Cost Accountant information and upload the CA/Cost Accountant certificate on the GST Portal for the ITC claimed exceeds Rs 2 lakh.

- Insert the information of CA like the name of the firm, CA’s name, membership number, and date of issuance of the certificate, and upload his certificate in JPEG format; and tap on ‘Save CA Details’

- For the declaration select the checkbox

- In the Authorised Signatory drop-down list, choose the authorized signatory. The same shall enable the two buttons – ‘File ITC with DSC or File ITC with EVC’

- For filing the form with Digital Signature Certificate choose the DSC button or the EVC button to file through the Electronic Verification Code.

- For filing through DSC tap on the proceed, choose the certificate, and tap on the sign.

- For filing through EVC insert OTP sent on the email and mobile number of the authorized signatory who is registered at the GST portal and tap to verify.

- Post filing the Acknowledgment reference number (ARN) would get generated and shared with the assessee.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

ITC FAQs After GST Implementation for Traders & Consumers

Q.1 – Does the GST paid for motor vehicles used for office purpose is eligible for ITC?

ITC is eligible for all the goods and services which are used within the business operations and course of furtherance, However, there are cases in which the ITC on goods and services has been restricted. And going by the laws the ITC is only permittable when the motor vehicle is acquired for resale or for transportation of passengers/ goods or for imparting training. Only the aforementioned causes make eligible for the ITC else all the causes may be dismissed for the ITC.

Q.2 – Ready-made garments attracting 5% and polyester yarn at 18% GST. How much credit will be available?

Polyester Yarn will grant whole 18% tax credit.

Q.3 – Can a refund be claimed from the duty-free shop?

There is no provision for ITC in the exempt free shops.

Q.4 – A manufacturing company providing canteen services to the workers. WIll it provide input tax credit?

Section 17-5 of ITC does not provide input tax credit for such transactions

Q.5 – Will credit be available for the imported stocks available until 30 June?

If all the documents are there of the stocks, then the credit can be claimed.

Q.6 – A raw material trader can get ITC for the transportation of goods?

The tax paid on transportation services can be availed for Input tax credit.

Q.7 – How to avail ITC on old stocks of medicine?

If documents are complete than the ITC will be available but if in case, the documents are not there, then the product category with 18-28 percent will provide 60 percent CGST, while 5-12 percent tax items will give a CGST rate of 40 percent

Q.8 – Do business with manufacturing and distribution will have to register again for the input distribution?

Yes, there will be a separate registration for the ISD services.

Q.9 – Who will pay the GST of loading trucks GST which is capped at % percent?

Whoever claims the goods will be paying the GST, and if in case he is unregistered dealer he may have to pay the GST to the transporter and will have to submit the GST to the reverse charge mechanism.

Q.10 – If in case, the registrant takes one PAN for two registration with two different verticals. will be there any tax on the transactions in between?

Yes, the registration of both will be considered two separate entities so there will be a tax on the transaction on them. While there will be applicable for credit also.

Q.11 – What is the limitation for the registered dealer in transactions with the unregistered dealer?

A registered dealer can transact with the unregistered dealers with the maximum limit of INR 5000 per day with one or more dealers.

Q.12 – If a composition dealer purchases from an unregistered dealer, will it have to pay under RCM?

Yes, the reverse charge mechanism is applicable to the composition dealers also.

Q.13 – Will there be Cess input tax credit available?

The credit of cess will be available but it can only be used in paying the Cess

Q.14 – What if 75 percent of apartment building work was completed before the GST. Is GST still applicable at the paid amount to the builder?

The GST will be applicable on the amount paid after 1st July, still, the builder must reduce the further amount as the input credit benefits will be available to him

Q15 – Is there input tax credit available for the furniture and AC purchased for office purpose?

Yes, there will be input tax credit available for all the purchases made for the office purpose.

Q.16 – When there is HSN code mismatch but the tax rate is similar, so is there any effect on input tax credit?

No, there will be no difference in the input tax credit.

Q.17 – What if a hotel doing business under 10 lakh turnover, has contracts with online hotel booking portals which require GSTN number for further business?

Yes, the registration is necessary to deal with registered online portals as it will affect their input claims further. It is also necessary to file taxes and necessary return on time.

Q.18 What is the time limit for holding old stocks, and is there any GST applicable on it?

There is no time limit for keeping old stock but if input tax credit is to availed on that old stock than there is a time limit of six months

Q.19 What if trader operates in other states even when its turnover is less than 20 lakh limit?

The trader has to register under GST, as it is doing operations in other states also. He cannot opt for composition scheme either with all the invoice rules to be properly followed. But one can claim input credit if he pays input tax

Q.20 What is the case in bearing supply, as sometimes there is no issuance of invoice?

There is an issue regarding the B2B supplies, as the invoice is a must for it. While it is also important to the input tax credit claim which requires an invoice. The invoice must also contain GST number and CGST SGST details.

Q.21 Garments industry input is effected as INR 25 input gives only INR 15 output. Will there be any refund of remaining INR 10?

No, according to the GST act refund provisions, there is no refund on the input. But the credit can be used elsewhere in the transaction chain

Q.22 Do single state transportation of goods with turnover less than 20 lakh requires GST number to be given to the transporters?

No, there is no requirement of GST number.

Q.23 As a retailer with 50 lakh turnover, Which scheme must be taken under GST?

Composition scheme seems to be more feasible for a retailer as it has a very less compliance in front of the general scheme. In a composition scheme where a retailer has to file 1 return in 3 months, the general scheme has 3 tax returns in one month. Also, there is no need to give invoice details, but in the composition scheme you cannot charge taxes and cannot take input credit.

Q.24 What is the final date to apply for composition scheme?

The government has extended the application of composition scheme till 16th of August.

Q.25 Can a dealer opt for a composition scheme if he has old stock of inter state purchase?

No, a dealer cannot ask for composition scheme if he has an interstate purchased stock.

Q.26 How to obtain input tax credit in GST if GSTN number is not mentioned on the invoice?

There must be GSTN number mandatory on all invoices regardless of mistakes.

Q.27 Is there any provision to claim input tax credit and depreciation, if the office furniture and machine are purchased?

One can claim input tax credit but cannot claim depreciation.

Q.28 In an imitation jewellery business, is there a concept of claiming input tax credit?

Yes, one can take input tax credit after paying all the due taxes.

Q.29 Is there input tax credit available on the office stationery purchase?

Yes, there is a provision of input tax credit on all the purchases of office stationery.

Q.30 When a product is purchased on the basis of RCM and the due tax is duly deposited on 10th of August, so when will input credit be claimed?

It can be claimed in July Returns But the returns to be filed before 20th of August.

Q.31 What is the GST on cars?

GST of 28% is levied on the cars while it also depends on Engine capacity and length of the cars. Less than 4 meters and engine capacity of 1200 cc is levied with 1% cess and an engine capacity of 1500 cc is having a 3% cess. While SUV and luxury cars will be applicable with 22% cess totalling 28% GST + 22% cess.