There are various rules and regulations which have emerged in the GST refund process. The GST refund will be needed to maintain under the GST as even a slight delay in the refund process will impact the working capital and cash flow of the manufacturers and exporters. In the current scenario, there is a delay in refunds extending for months, by making refunds available to the concerned manufacturers and exporters, and to get the refunds, it is a challenge as there are strict rules and regulations for the processing of refunds.

Latest Update

23rd December 2021

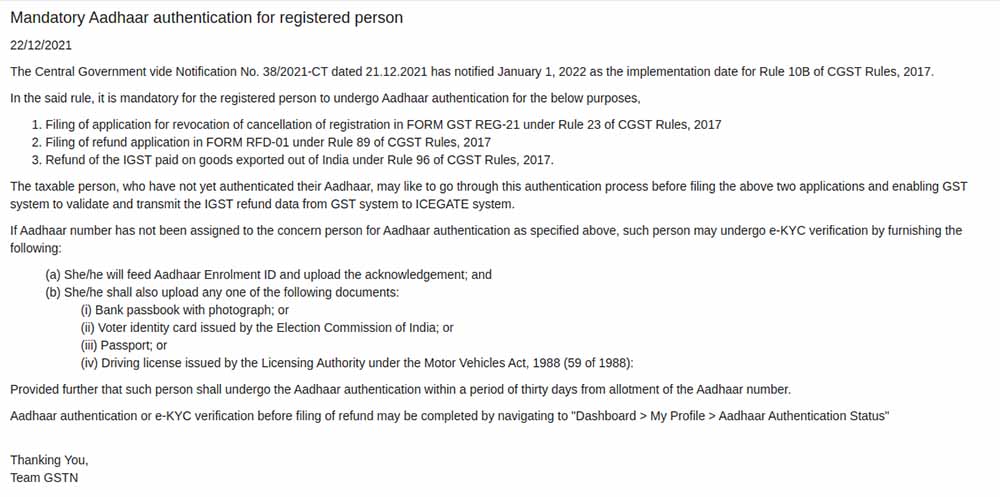

“CBIC has showcased an advisory related to the Aadhaar authentication for filing of GST refund/Revocation of cancelled applications of registration from 1st January 2022. Read more“

9th December 2021

The high court of Madras state prolonged time of limitation and relief to traders on goods and services tax refund claims. read order

18th May 2021

- “Seeks to prescribe Standard Operating Procedure (SOP) for implementation of the provision of extension of time limit to apply for revocation of cancellation of registration under section 30 of the CGST Act, 2017 and rule 23 of the CGST Rules.” Read Circular

Compulsory to Match Invoices for Exporters’ GST Refund Issues

Numerous exporters are facing problems in claiming ITC (Input Tax Credit) as the government made it compulsory to match GST Invoices for the claim. Experts say that the situation is the result of the late fee waiver of certain forms for companies and suppliers. In several cases, exporters were unable to claim ITC as the forms were not submitted. A corresponding invoice is to be uploaded on the GST portal claiming ITC. All the invoices should be reflected in form GSTR- 2A

There are Various Situations for a Refund under GST, like:

- Excess payment of tax accumulated due to a mistake or misinterpretation

- Export (also deemed export) of goods/services within the claim of rebate or Refund of collected input credit of duty/tax when goods/services are exported

- Finalization of provisional assessment

- Refund of Pre-deposit for filing an appeal, assimilating the refund coming in pursuance of an appellate authority’s order

- Payment of duty/tax during the investigation, but no/ less liability arises in the event of finalization of the investigation/adjudication

- Refund of tax paid on purchases made by Embassies or UN bodies

- Credit collection due to output being tax-exempt or nil-rated

- Credit collection due to inverted duty structure i.e. due to tax rate differential between output and inputs

- Year-end or volume based incentives provided by the supplier through credit notes

- Tax Refund for Foreign Tourists

Read Also: How to File GST Refund Claims Manually? Step by Step Guide

There is an Official Refund Process under the GST:

- An Application form to claim a refund can be filed through the GSTN portal

- An acknowledgement number will be given to the applicant by means of SMS or email when the application is filed electronically

- The changes will be made to the return and cash ledger, and decrease the “carry-forward input tax credit” automatically

- Refund application and relevant documents presented must be scrutinized and adhered to accordingly within a period of 30 days of filing the refund application

- The issue of “unjust enrichment” will be analyzed for reach refund application. In the case of non-qualification, the refund would be transferred to CWF (consumer welfare fund)

- If the refund amount stated crosses the predetermined amount of refund, then the file will through the pre-audit process for sanctioning the refund

- Refund will be credited electronically to the account of an applicant via ECS, RTGS or NEFT

- The application for refund can be made after every quarter

- An amount less than 1000 is not eligible for the refund

Trending Topic: Do You Know about GST E-Way Bill and How it Will Generate?

Delay in Refund and Its Process

Subramanian committee suggested along with the defined GST laws and regulations, the refund application must be entertained within the period of 90 days and must be processed within the same time period. If in any case the application could not be processed within the given time framework, there is a 6 percent interest recommended along with the refund amount.

It was also mentioned by Nirmala Sitharaman (finance minister) who cleared that the refund process will be done within the period of 7 days, and if the process gets late for more than 2 weeks, then the refund will be provided along with the interest.

It is speculated that the process of the refund application will be fast and smooth due to its digital dependability. Also, the data will be uploaded electronically, which depicts that the verification and the detailed analysis of the refund application will be quick.

Latest Updates and News on the GST Refund Topic

GST Refund in Hilly Areas Under Scanner

Taxpayers in hill areas and stations are set to approach the court against the revenue department, which has found a reversal of transitional credit benefited by them on account of the cash balance available in the ledger ahead of GST implementation in the country.

The department has not distributed the available GST refunds to producers and manufacturers of hilly states. Previously, before GST implementation, under the area-based exemption scheme, the manufacturers were provided with tax concessions.

The department now mentions that the transitioning provision available under the newly implemented indirect tax regime referred only to the excess credit available to the taxpayers, and it did not apply to the ledger for cash balance.

Furtherly, the finance secretary also mentioned that the Cash credit can not undergo into GST as only Input Tax Credit can be accounted for transition under the GST regime.

GSTN Intends to Launch Online Application for Refunds

The GSTN organization is also under inclusion to launch an online application to process refunds. Chief Executive Officer Prakash Kumar stated that “A separate online app for claiming Integrated GST refunds for August and September would be made available on the GSTN portal.” The application will provide facilities like saving and uploading sales data of the GSTR 1.

The automated process will also be there to assist in which the data will be extracted and will be to the customs department after a digital signature. The details will be validated by the department, and the further refund process will be initiated accordingly.

GST Refund Advice for Taxpayers

| Follow | Not Follow |

|---|---|

| Only browse official GST portal website – www.gst.gov.in for refunds | Beware to reply any fake message of GST refund process |

| Read here to know GST refund status: https://www.gst.gov.in/help/refund | Leave any attachment or hyperlink in the fake message |

| Must Remember that GSTN never call for personal information and GST refund details on email, WhatsApp or SMS | The taxpayers should never fill any personal details and other contact details on other websites |

| Continually browse official GST portal for new updates | Never dial at the phone number that is mentioned in the fake message |

| Any query please use GST helpdesk – 1800-103-4786. | Do not believe other similar design websites instead of the official portal |

General Queries on GST Refund

Q.1 – What in case if taxpayer miss shipping and invoice bill in a month, can he add the details in subsequent month and get a refund?

Yes, a taxpayer can add the details in subsequent month and can get the refund.

Q.2 – Does GSTR 2 and GSTR 3 needs to be filed for claiming refunds?

If the taxpayers have filed GSTR 1 and GSTR 3B than he doesn’t need to fill other forms to claim refunds.

Q.3 – Is the taxpayer eligible to claim refunds on IGST paid on exports of goods if he has filed GSTR 3B?

Yes, the taxpayer is eligible to get the refunds to claim if he has provided the details of export goods details in GSTR 1 Table 6A and has filed GSTR 3B with relevant tax details

{kind=link}

We are the importer of Ferrous, Non-Ferrous and Plastic Scrap materials. While Calculating Custom Duty and IGST, Customs Authority is always taking Higher amount (almost 30%-50%) per unit. For e.g. in case of Import of Plastic Scrap, Invoice Shows material priced as the US $ 375/- per Mt even though Custom Authority considers price as US$ 645/- per MT and accordingly they charged custom Duty and IGST. Also, There is not more 10% of the Value addition in Sales Price hence adjustment of the entire amount of IGST is not possible as a result the good amount of GST is accumulated.

My question as to how we can claim the refund of such accumulated/ non-utilization of GST? This accumulation really hampers our Cash Flow.

Please advice

Thanks and best regards

In the case on inverted duty structure i.e., when the sale price is less than the purchase price and tax paid on the purchase of goods, is more than tax charged on sale then refund of such unutilised credit can be claimed by filing form RFD-01 for such tax period.

WE COULD NOT ABLE TO GET THE REFUND FOR INVERTED DUTY STRUCTURE. CAN ANYBODY HELP US TO PROVIDE THE LATEST CIRCULARS SUPPORTING THE REFUND CLAIM?

Dear Sir/Madam,

It is a very cumbersome process to prepare separate details for Refund Letter, Refund Acknowledgement generated online, Summary of Invoices, etc. Can we get all the forms with Invoices, IGST, etc. details for Refund Application through GEN GST Software itself?

Thanks & Regards,

Jayalakshmi,

In October, We paid the amount in cess instead of CGST, how to refund the amount

You need to file an online application for refund.

You can claim a refund order by logging into your account & avail services options & then refund option. Please note refund amount should be greater than 1000.

Print the refund order copy generated along with supporting like payment voucher from your cash ledger or challans etc, mark self-attestation & submit to your LVO or GST office.

Hi

We filed wrong refund application and the problem is ITC got deducted from ledger for that refund application. Now hoe=w can we delete that application and claim that ITC back in an electronics ledger.

Cancellation is not possible in case of refund application.