The Income Tax Appellate Tribunal upheld the addition of ₹11.14 crore on account of bogus purchases and sustained a 50% disallowance of labour charges, observing that the transactions remained unverified and were not supported by credible documentary evidence. The Tribunal held that the assessee failed to substantiate the genuineness of the claims with adequate supporting records.

With the lower authorities, the tribunal agreed in rejecting additional documents submitted under Rule 46A of the Income‑tax Rules, 1962, observing that the norms for considering these proofs were not fulfilled and that mere reversal entries or self-prepared vouchers cannot specify the genuineness of the transactions.

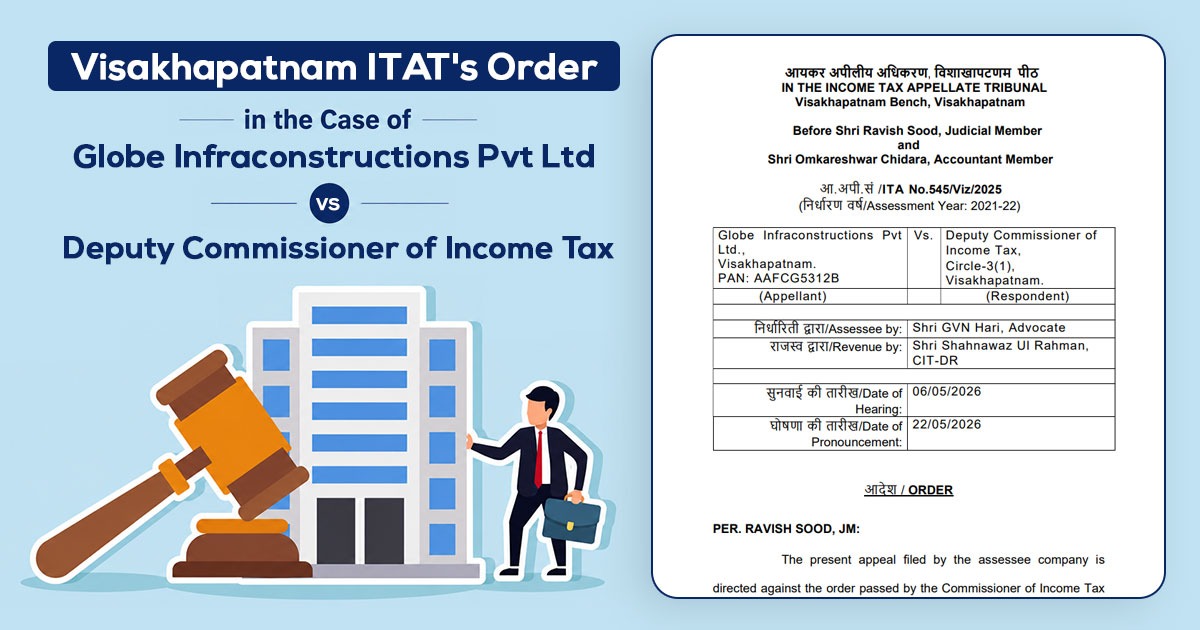

The taxpayer’s firm, Globe Infraconstructions Pvt Ltd, is engaged in the business of infrastructure and commercial construction, and declared an income of Rs 2.04 crore.

At the time of scrutiny, the AO discovered that the company had recorded purchases from 17 suppliers, many of whom had not submitted ITRs or had inactive GST registrations. U/s 133(6), the notices issued showed that most suppliers did not exist or refused any transactions with the taxpayer.

One supplier, Harsha Infra Projects Pvt Ltd, confirmed transactions of Rs 67.74 lakh; the AO considered the remaining purchases of Rs 11.14 crore as fake and added them to the income.

The Assessing Officer (AO) disallowed 50% of the claimed labour charges of Rs 33.53 lakh, mentioning an absence of verifiable records like muster rolls, wage sheets, or PF/ESI details.

The appeal of the taxpayer has not been accepted by the CIT(A) to admit other evidence, marking that the company had various opportunities in assessment but failed to provide the supporting documents.

The explanation for relying on “middlemen” for discounted supplies was deemed unconvincing, as no agreements or correspondence were presented. The disallowance of 50% of labour charges was considered reasonable due to the lack of statutory records and the cash-based nature of the payments.

The taxpayer’s representative, Advocate GVN Hari, claimed that the authorities had misinterpreted the facts and overlooked evidence indicating the reversal of purchase entries and GST input credits. They contended that since the purchases were cancelled and reversed, the addition of ₹11.14 crore as fake purchases was not justified.

Read Also: ITAT Delhi Upholds Deletion of INR 6.80 Crore Addition U/S 69C for Alleged Bogus Purchases

Concerning the labour charges, the taxpayer asserted that payments were made to daily-wage workers hired from local sites who did not possess PAN numbers or formal identification. They argued that the absence of PF/ESI records should not invalidate legitimate expenses supported by vouchers.

The revenue claimed that the taxpayer did not provide documentary proof at the time of assessment, even after repeated notices under sections 142(1) and 143(2).

The revenue also mentioned that mere book entries or reversals without delivery challans, transport documents, or supplier confirmations cannot establish genuineness.

After reviewing the case, the Tribunal confirmed that the Commissioner of Income Tax (Appeals) CIT(A) had correctly dismissed the Rule 46A petition. The Tribunal noted that a “time constraint” was not a valid excuse for the failure to submit evidence.

It was determined that the taxpayer did not meet the burden of proof regarding the validity of the transactions, and therefore, the Assessing Officer was justified in considering purchases amounting to ₹11.14 crore as non-genuine.

The bench, including Judicial Member Shri Ravish Sood and Accountant Member Shri Omkareshwar Chidara, agreed on the issue of labour charges with the decision of lower authorities that payments made in cash to daily‑wage workers without muster rolls, attendance registers, or PF/ESI records were not verified. 50% disallowance of ₹16.76 lakh was considered a reasonable estimate.

Subsequently, the ITAT ruled that the appeal was partly permitted for statistical objectives.

| Case Title | Globe Infraconstructions Pvt Ltd. vs. Deputy Commissioner of Income Tax |

| Case No. | ITA No.545/Viz/2025 |

| Assessee by | Shri GVN Hari |

| Revenue by | Shri Shahnawaz Ul Rahman |

| Visakhapatnam ITAT | Read Order |