The Supreme Court has quashed a Special Leave Petition (SLP) contesting an assessment order passed u/s 74 of the CGST Act, making crucial observations on electronic communication of GST orders and the limits of writ jurisdiction.

The Court said that uploading an assessment order on the GST electronic portal is a valid communication. The court dismissed the claim that the taxpayer’s lack of awareness of the order uploaded to the portal could nullify the proceedings, stating there’s no valid basis to ignore legal electronic service.

The Bench, including Justice Joymalya Bagchi and Justice Vipul M. Pancholi, observed that the applicant had admitted becoming aware of the proceedings in 2024 but still approached the High Court only in 2025. By that time, the statutory appeal u/s 107 had become time-barred. The court ruled that a writ petition is not a suitable alternative for an appellate remedy that was not exercised within the stipulated limitation period.

The applicant, section 74, was incorrectly invoked, claiming there was no fraud, wilful misstatement, or suppression of facts. ITC claimed for October 2017 was voluntarily reversed in the November 2017 returns, and thus, no intent to evade tax was shown. Reliance was also placed on another pending Supreme Court matter involving similar issues.

The Supreme Court analysed the SCN on September 8, 2023, and the assessment order on November 7, 2023, and discovered that the tax authorities had earlier dealt with the factual matrix in detail.

The Court, CGST Act, furnishes a clear appellate remedy under section 107, which the applicant was not able to use within time. Once that remedy was lost because of limitation, the attempt to contest the order via writ jurisdiction was not maintainable.

The court has not accepted the appeal for lack of awareness of the order. Also, it repeated that GST portal uploads constitute sufficient notice. The court differentiated the referenced pending case, pointing out that it dealt with a challenge to a show-cause notice, while the current case involved a finalised assessment and an appeal that had passed its deadline.

The Supreme Court did not find any merit and dismissed the SLP and all the due applications, supporting that regulatory remedies should be pursued within limitation and that GST electronic communications carry complete lawful effect.

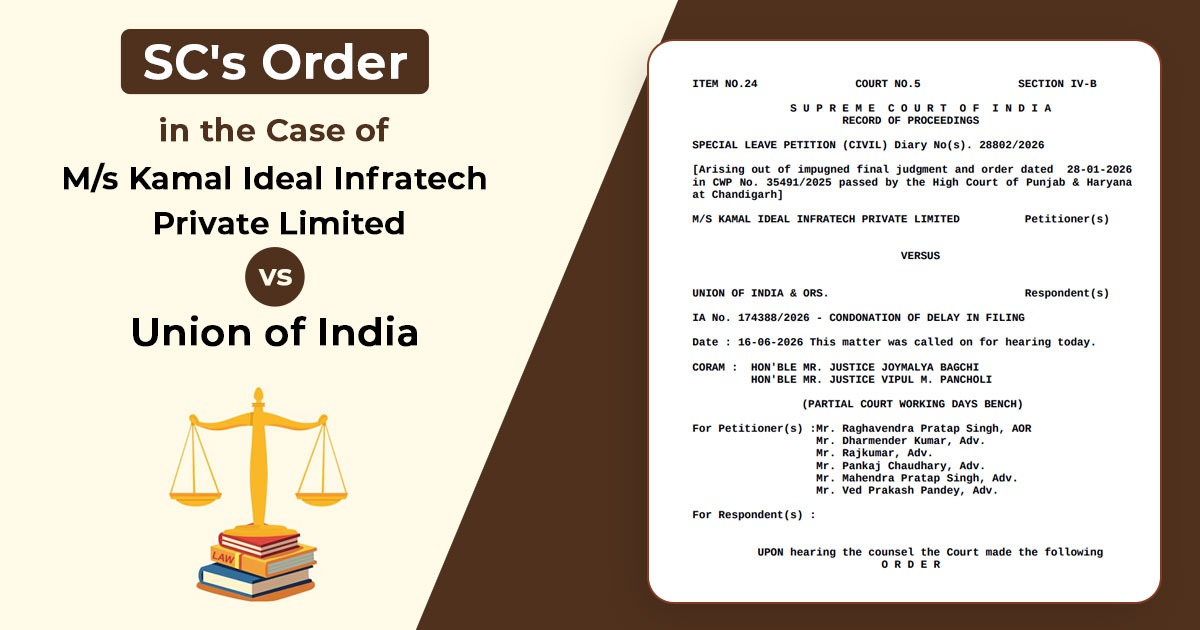

| Case Title | M/s Kamal Ideal Infratech Private Limited Vs Union of India |

| Case No | Special Leave Petition (Civil) Diary No(s). 28802/2026 |

| For Petitioner | Mr Raghavendra Pratap Singh, Mr Dharmender Kumar, Mr Rajkumar, Mr Pankaj Chaudhary, Mr Mahendra Pratap Singh, Mr Ved Prakash Pandey |

| Supreme Court Order | Read Order |