The Delhi High Court has responded to a request from the GST Appellate Tribunal Bar Association in Delhi. They are challenging a deadline set for June 30, 2026, the last day to submit appeals regarding tax decisions communicated before April 1, 2026.

The Bar Association is requesting an extension of at least three months beyond June 15, 2026, when the process for filing appeals online was fully explained to all involved.

Although the Court refused to provide an interim relief at this phase.

A vacation bench of Justices Mini Pushkarna and Vinod Kumar said that it shall acknowledge the issue after obtaining responses from the respondents.

A bench said, “I am not granting any interim relief. Let them file a reply; we’ll see. In case it is to be done, we’ll see that.”

Important: GSTAT Sets Up Help Desks at Delhi, Surat, and Jodhpur Benches to Assist Taxpayers

The court issued notice to the Union of India represented through the Ministry of Finance and the Central Board of Indirect Taxes and Customs (CBIC). It asked the respondents to submit their responses and provided the applicant with the liberty to submit a rejoinder afterwards. On July 27, 2026, the case had been listed before the roaster bench.

The applicant’s counsel said that although section 112 of the CGST Act has furnished a right of second appeal since 2017, the GSTAT started operations in Delhi only on April 2, 2026, and the process for e-filing appeals was formally explained in a National Workshop conducted on June 15, 2026. Stakeholders had just 15 days to submit appeals that had accumulated over several years because of the non-functioning of the Tribunal.

The counsel, referring to the challenge raised in the writ petition, placed reliance on the appeal that, “The time allowed for filing of appeal up to 30th June 2026 is palpably unjust, unfair and unreasonable having regard to the complicated procedure adopted by the GSTAT.”

The petition further states that “practically only 15 days time is available to the stakeholders and professionals to file appeals which have been piled up over the years on account of non-functioning of GSTAT.”

The applicant then claimed that the GSTAT e-filing procedure remains inconvenient and prone to technical issues. GSTAT had considered issues encountered by appellants in e-filing via a communication dated May 14, 2026, and asked for an extension of the filing period by at least three months from June 15, 2026, apart from other consequential reliefs.

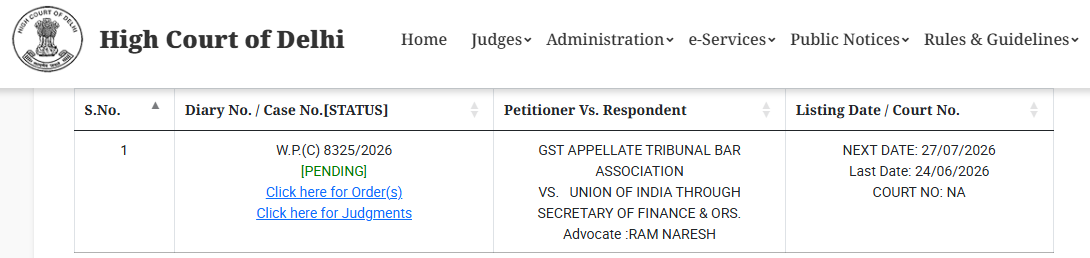

| Case Title | GST Appellate Tribunal Bar Association V/s Union of India Through Secretary of Finance & ORS. |

| Case No. | W.P.(C) 8325/2026 |

| Delhi High Court | Order Pending |

{kind=link}