The Punjab and Haryana High Court has ruled that suspending Input Tax Credit (ITC) within an assessee’s Electronic Credit Ledger without issuing a speaking, reasoned order directly contravenes Rule 86A of the CGST Rules, 2017.

The Bench emphasised that administrative authorities cannot act on mere suspicion; they must establish objective justification and communicate explicit reasons prior to restricting a taxpayer’s statutory right to utilise credit.

Read Also: P&H HC Quashes GST Assessment Order for Ignoring Assessee’s Reply to SCN in ITC Fraud Case

The bench of Justice Deepak Sibal and Justice Lapita Banerji ruled that authorities cannot freeze an available credit of a taxpayer only via an administrative communication without recording reasons and following the specified procedure under law.

The applicant, Shreyash Retail Private Limited, contested the action of the State Tax authorities in blocking its ITC. As per the petition, the blockage had been communicated via an email on January 13, 2026, without any formal order being passed by the competent authority. The applicant claimed that the same action does not have any statutory backing and breached procedural safeguards under the GST structure.

The scope of Rule 86A of the CGST Rules has been analysed by the Bench. The Court said that the provision grants authority to the commissioner or an authorised officer not below the rank of Assistant Commissioner to block ITC only where there are reasons to assume that the same credit has either been claimed fraudulently or is otherwise ineligible. The use of this authority is limited and needs to comply with statutory conditions.

The Court outlined that the provision of reasons to believe is not a mere formality. These reasons are there before the exercise of power and must be shown in an order passed via the competent authority.

In the same case, it was not disputed that before blocking the applicant’s ITC available in the electronic credit ledger, no order had been passed recording reasons for this action.

The High Court, considering the same procedural lapse, concluded that the impugned action was in breach of Rule 86A. The Bench said that the credit blocking without a formal order and without recording reasons cannot be kept under the law. The Court subsequently held the action to be illegal.

The Court ordered the release of the blocked input tax credit (ITC) of the applicant. But, during granting relief, the Bench mentioned that the tax authorities shall remain at liberty to start fresh proceedings against the applicant, given such action is opted as per the law and after complying with the procedure specified under the statutory structure.

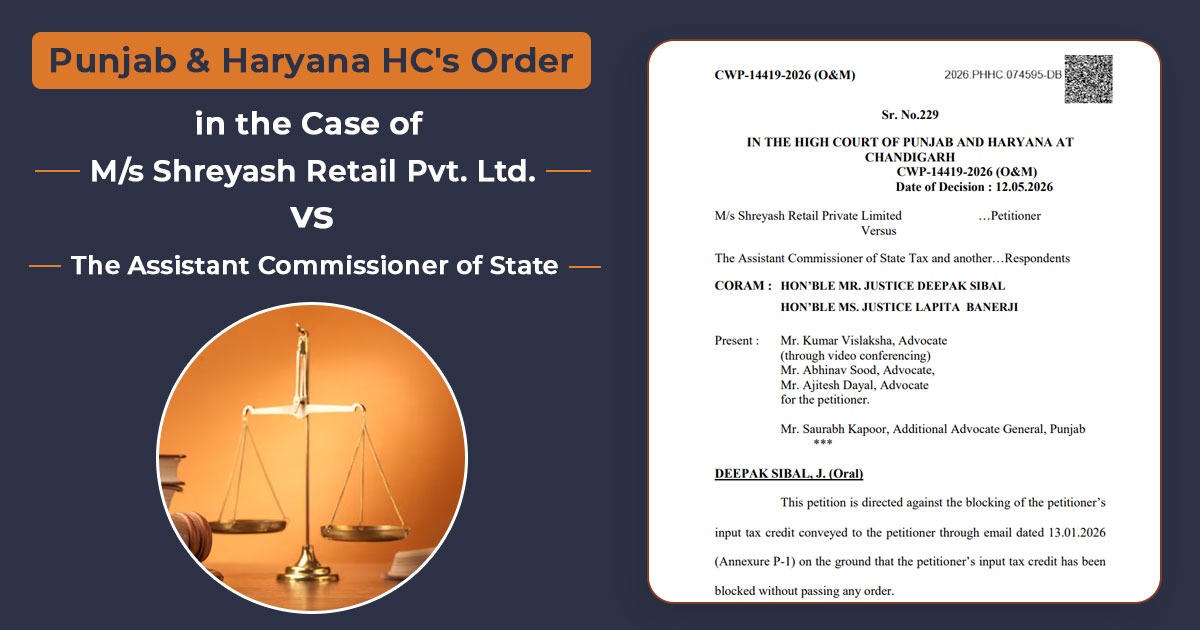

| Case Title | M/s Shreyash Retail Pvt. Ltd. vs The Assistant Commissioner of State Tax and another |

| Case No. | CWP-14419-2026 (O&M) |

| Counsel For Petitioner | Mr Kumar Vislaksha, Mr Abhinav, and Mr Ajitesh Dayal |

| Counsel For Respondent | Mr. Saurabh Kapoor |

| Punjab & Haryana High Court | Read Order |