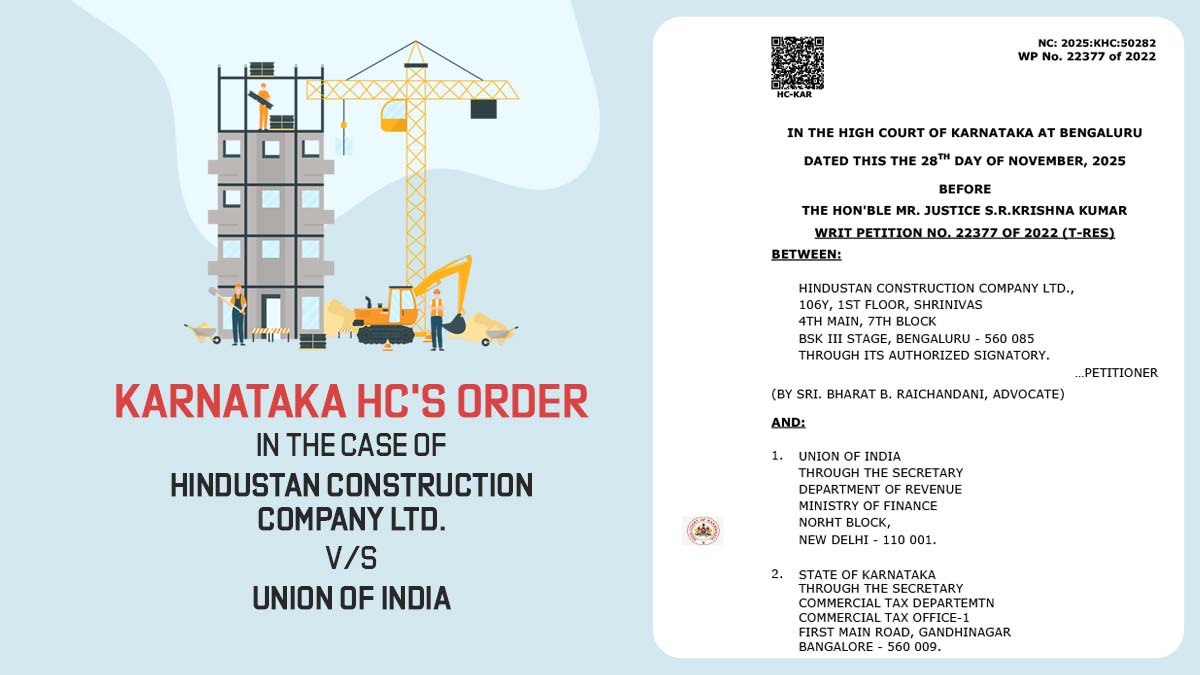

The Karnataka High Court in Hindustan Construction Company Ltd. v. Union of India, decided in Writ Petition No. 22377 of 2022, analysed whether bona fide errors committed by the taxpayer at the time of filing GSTR-3B returns can explain the initiation of the proceedings u/s 73 of the CGST/KGST Act.

The case was heard and decided by Justice S.R. Krishna Kumar, who reaffirmed the principle that genuine and unintentional mistakes in GST returns are capable of rectification and cannot automatically be considered as tax evasion or suppression warranting penal action.

The applicant, Hindustan Construction Company Ltd., a works contractor, contested a show cause notice via the Assistant Commissioner of Commercial Taxes, claiming that even after having rectified the errors via the GST portal, the department proceeded u/s 73 on the premise that these rectifications were not allowable.

The ruling is significant since it repeats a consistent judicial approach chosen via the Karnataka High Court and aligns with the direction of the Supreme Court to re-examine timelines and provisions of the rectification of bona fide errors in GST returns.

The applicant is in the works contract services and has submitted its GSTR-3B returns for the initial GST period from July 2017 to March 2018. Thereafter, the applicant observed errors in the returns, which were admittedly bona fide and inadvertent in nature.

The applicant has accidentally declared specific outward supplies as B2C rather than B2B. Then the applicant considered that during reporting the turnover, it had considered the value as inclusive of GST at 18%, but the appropriate rate was 12%. These errors result in the wrong reporting of turnover numbers, but no dispute was pertinent to tax payment or revenue loss.

The applicant, on noticing such mistakes, corrected the errors dated 06.05.2019, and the GST portal allowed these rectifications. Even after the same, the Assistant Commissioner of Commercial Taxes had issued an SCN under section 73(1) of the KGST Act, alleging that the applicant was not qualified to make the same rectifications and proposing tax proceedings.

The applicant is dissatisfied with the issuance of the SCN and approached the Karnataka High Court, asking to quash the proceedings and a direction to the department to accept the revised returns.

Statements By Applicant

The applicant said that the errors committed in the GSTR-3B returns were clerical and bona fide, and does not hold any intention to evade tax or suppress turnover. It was claimed that the GST regime is still evolving, particularly at the time of the initial period of its execution, and minor mistakes were inevitable.

On the ruling of the Karnataka High Court in Orient Traders v. Deputy Commissioner of Commercial Taxes (Audit), the applicant put reliance where the court’s categorisation that GSTR-3B returns rectification must be allowed when it does not prejudice revenue or disrupt the GST input tax credit (ITC) chain. It was found that the existing matter was covered under the mentioned decision.

Reliance was placed on Wipro Limited India v. Assistant Commissioner of Central Taxes, where the Court had taken a similar opinion and allowed rectification of errors in GST returns, acknowledging the intricacy of the GST system and the need for a practical approach.

The petitioner highlighted that the GST portal itself allows for corrections, indicating that the system is designed to facilitate the rectification of genuine mistakes. Once corrections are made and accepted on the portal, the department cannot later argue that such corrections are impermissible.

Additionally, it was pointed out that Section 73 of the CGST/KGST Act is meant to address instances of unpaid tax, short payment, or erroneous refunds resulting from fraud, willful misstatement, or suppression of facts—none of which were present in this case. Therefore, initiating proceedings under Section 73 for honest errors was deemed arbitrary, unjust, and contrary to the intent of the statute.

Respondents’ Arguments

The respondents, represented by the department counsel, desired to explain the issuance of the SCN under section 73. They said that the statutory framework sets timelines for the rectification of returns, and once these timelines lapse, the taxpayer cannot revise the returns on their own.

The department contended that allowing rectification outside the stipulated period would open the door to manipulation of returns and undermine the certainty and finality of self-assessment under the GST regime. The respondents stated that the applicant had surpassed the permissible window for corrections, and thus, the revised returns could not be accepted.

Additionally, it was furnished that the issuance of an SCN u/s 73 was merely a preliminary step, and the applicant would have the chance to explain their position during the adjudication process. Thus, judicial interference at this stage was not justified.

High Court Analysis

The factual matrix has been analysed by Justice S.R. Krishna Kumar, who cited that no allegation of fraud, suppression, or wilful misstatement against the applicant was made. The errors of classification of supplies and the wrong calculation of turnover due to an inadvertent application of a wrong tax rate.

The court put reliance on its earlier decision in Orient Traders, wherein it had been ruled that allowing rectification of GSTR-3B returns shall not cause prejudice to the revenue nor disrupt the GST credit chain. The Court noted that this case had even stronger grounds, as the GST portal had already permitted the corrections.

The Bench referred to Wipro Limited India, where identical rectification was allowed, supporting the principle that procedural technicalities must not override substantive justice, especially when revenue interests are not adversely impacted.

A crucial aspect of the ruling was the reference of the court to the direction of the Apex court to the CBIC to re-examine provisions and timelines for rectifying bona fide errors. HC said that the same direction specifies judicial recognition of the practical issues encountered by taxpayers under the GST regime and the need for a practical approach.

The claim of the department has been refused by the court that the expiry of timelines automatically disentitles the taxpayer from correction, holding that such an interpretation would be unduly harsh and inconsistent with the objective of GST as a facilitative tax system.

Karnataka High Court Judgment

The Karnataka High Court stated that bona fide errors in GSTR-3B returns are rectifiable and cannot, by themselves, form the basis for initiating proceedings u/s 73 of the CGST/KGST Act. The Court concluded that the impugned SCN was not sustainable in law.

Subsequently, the court permitted the writ petition and issued the directions-

- The respondent department was asked to accept the revised GSTR-3B returns submitted via the applicant, including the required rectifications.

- Under Section 73(1) of the KGST Act, the SCN issued was rendered untenable in the facts of the case.

- The judgment supports the principle that tax administration should differentiate between genuine mistakes and intentional non-compliance, and that penal provisions cannot be invoked mechanically.

| Case Title | Hindustan Construction Company Ltd. Vs. Union of India |

| Case No. | Writ Petition No. 22377 of 2022 (T-Res) |

| For Petitioner | Sri. Bharat B. Raichandani |

| For Respondent | Sri. Prathibha, Sri. K. Hema Kumar |

| Karnataka High Court | Read Order |