If you are a regular goods and services tax (GST) registered taxpayer, then you must submit your GSTR-3B monthly return, including invoices for the applicable tax period. However, if you file bills of the previous month late in the current month of GSTR-3B, then, as per section 50, you need to submit the interest.

When you file a return for an earlier period in a later year, interest is imposed under Section 50. The same takes place when you file the invoices from a previous month or quarter in the Form GSTR-3B return for a subsequent month.

The Goods and Services Tax Network (GSTN) implemented a system change to GSTR-3B for the February 2026 tax period to monitor such late reporting. But, after the same update, the taxpayers encountered a technical issue on the portal as the system needs all the GST-registered taxpayers, as well as those without any late invoices, to open the tax liability breakup tab and validate the same by tapping save.

The issue has been recognised by the GSTN, and it has recommended an interim fix.

In submitting the Form GSTR-3B, taxpayers are encountering issues as the GST portal currently requires confirmation of the tax liability breakup, as applicable,’ tab even in cases where no obligation of earlier tax durations is reported.

It has consequences in unwanted compliance measures and confusion at the time of filing the return. GSTN, as an interim measure, suggested that taxpayers must open the tab and tap SAVE to move with submitting GSTR-3B till the portal issue is solved.

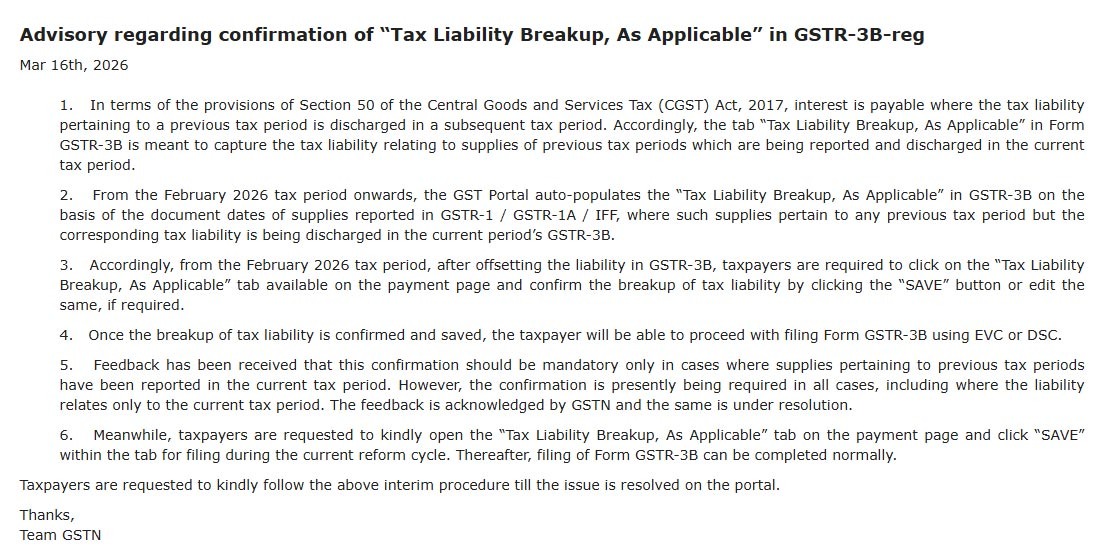

GSTN New Advisory for Confirmation of “Tax Liability Breakup, As Applicable” in GSTR 3B Form

GSTN, in an advisory dated February 16, 2026, specified the following:

As per the provisions of Section 50 of the Central Goods and Services Tax (CGST) Act, 2017, interest is to be paid where the tax obligation related to the previous tax period is released in a subsequent tax period. Subsequently, the tax “Tax Liability Breakup, As Applicable” in Form GSTR-3B is directed to capture the tax obligation of the supplies of previous tax periods that are being reported and released in the existing tax duration.

The GST portal from the February 2026 tax period onwards auto-populates the “Tax Liability Breakup, As Applicable” in GSTR-3B as per the grounds of the document dates of supplies notified in GSTR-1 / GSTR-1A / IFF, where such supplies related to any previous tax period but the related tax obligation is being released in the existing GSTR-3B period.

Subsequently, from the February 2026 tax period, post offsetting the obligation in GSTR-3B, taxpayers must tap on the “Tax Liability Breakup, As Applicable” tab available on the payment page and confirm the breakup of tax liability by clicking the “SAVE” button or edit the same, if needed.

After confirming the tax liability breakup and when it gets saved, then the taxpayers shall be allowed to move to file Form GSTR-3B using EVC or DSC.

Feedback has indicated that this confirmation should be mandatory only for cases where supplies from previous tax periods have been reported in the current tax period. However, at present, confirmation is required in all cases, including instances where the liability pertains only to the current tax period. GSTN acknowledges this feedback, and the issue is currently being addressed.

Important: How GST Software Adjusts the Negative Liability Ledger

Taxpayers must open the “Tax Liability Breakup, As Applicable” tab on the payment page and click “SAVE” within the tab for filing during the current reform cycle. Afterwards, filing of Form GSTR-3B can be completed normally.

GSTN mentions that “Assessee are invited to kindly follow the above interim process till the problem is fixed on the GST portal.”

Read GSTN Advisory