What is the ITR 2 Form?

The ITR-2 is filed by individuals or HUFs not having income from profit or gains of business or profession and to whom ITR-1 is not applicable. It includes income from capital gains, foreign income, or any agricultural income of more than Rs 5,000.

- What is ITR 2 Form

- Eligibility File ITR 2 Online AY 2026-27

- File ITR 2 Via Gen IT Software

- ITR 2 Due Date for AY 2025-26

- Structure of ITR 2 Filing

- ITR 2 Form Filing Online and Offline Mode

Latest Update

- Now, taxpayers can download the Excel-based utility, JSON schema, and validation for ITR-2 AY 2026-27 from the official e-Filing portal. Download now

ITR 2 Filing Start Date for Taxpayers

The Income Tax Department has not yet started online filing for the ITR-2 form.

Eligible Taxpayers for Filing ITR 2 Online AY 2026-27

The taxpayers who are eligible for filing the ITR-2 form are the persons whose source of income is as mentioned below:

- A resident having any asset located outside India or a signing authority in any account.

- A non-resident or non-ordinary resident.

- Taxpayers who earn agricultural income above Rs. 5000/-.

- Income from winnings of a lottery, horse race, gambling, etc., under the head of other sources.

- Both short and long-term capital gains/losses from the sale of property/investments/securities. (if there is only long term capital gain exempt u/s 10(38) then ITR-1 can be filed)

The taxpayers who are not eligible to file the ITR-2 form are as follows:

- Taxpayers who earn from a business or profession

- Taxpayers who are eligible to file an Income Tax Return 1.

File ITR 2 Via Gen IT Software, Get Demo!

Due Date for Filing ITR 2 Online AY 2026-27

| Financial Year | Due Date |

|---|---|

| FY 2025-26 (AY 2026-27) | 31st July 2026 |

| FY 2024-25 (AY 2025-26) | |

| FY 2023-24 (AY 2024-25) | 31st July 2024 |

Every year, on or before 31st July, is termed as the last date for filing ITR 2.

Note: ITR-2 form corrigendum via Notification No. 58/2026. Read More

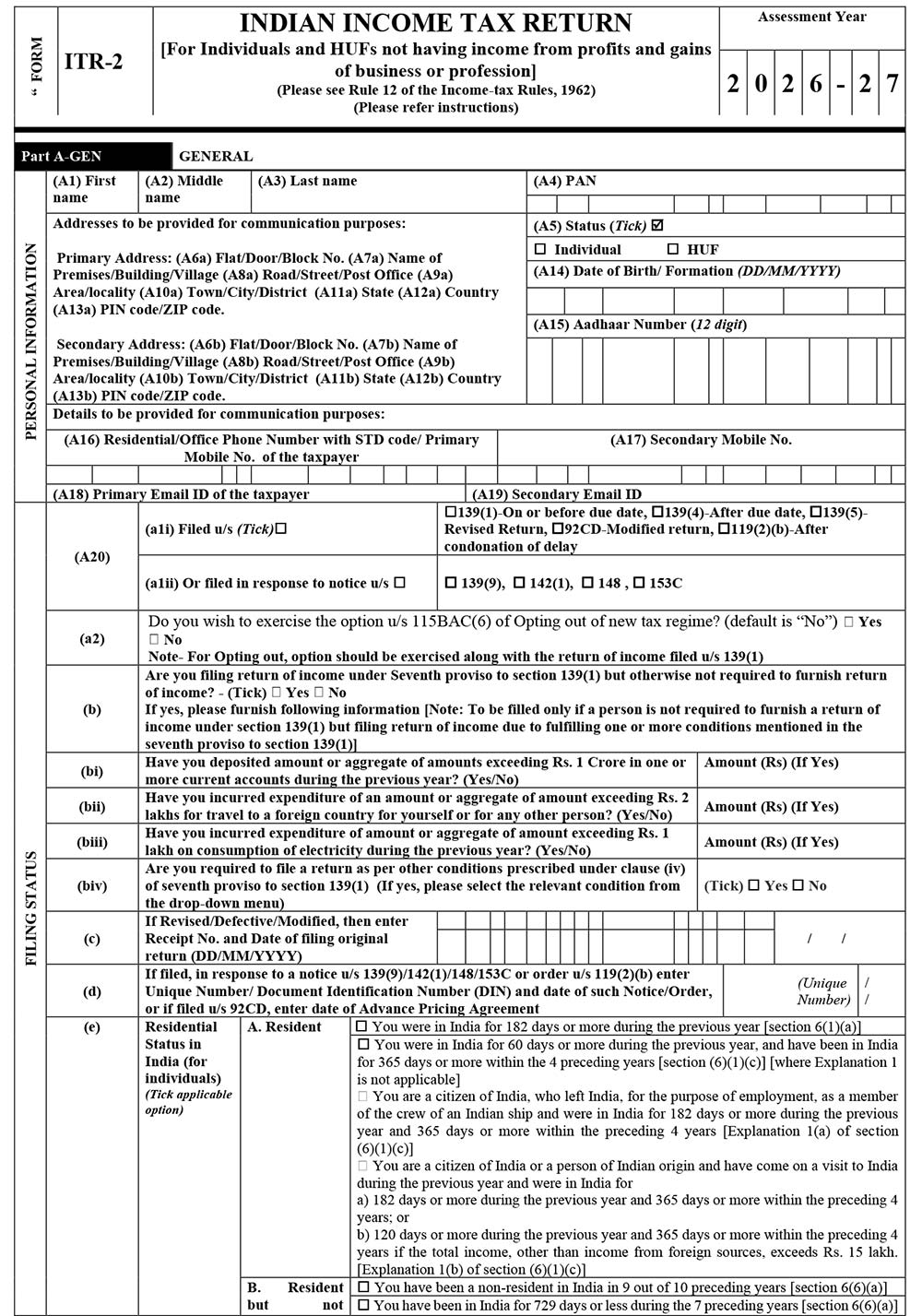

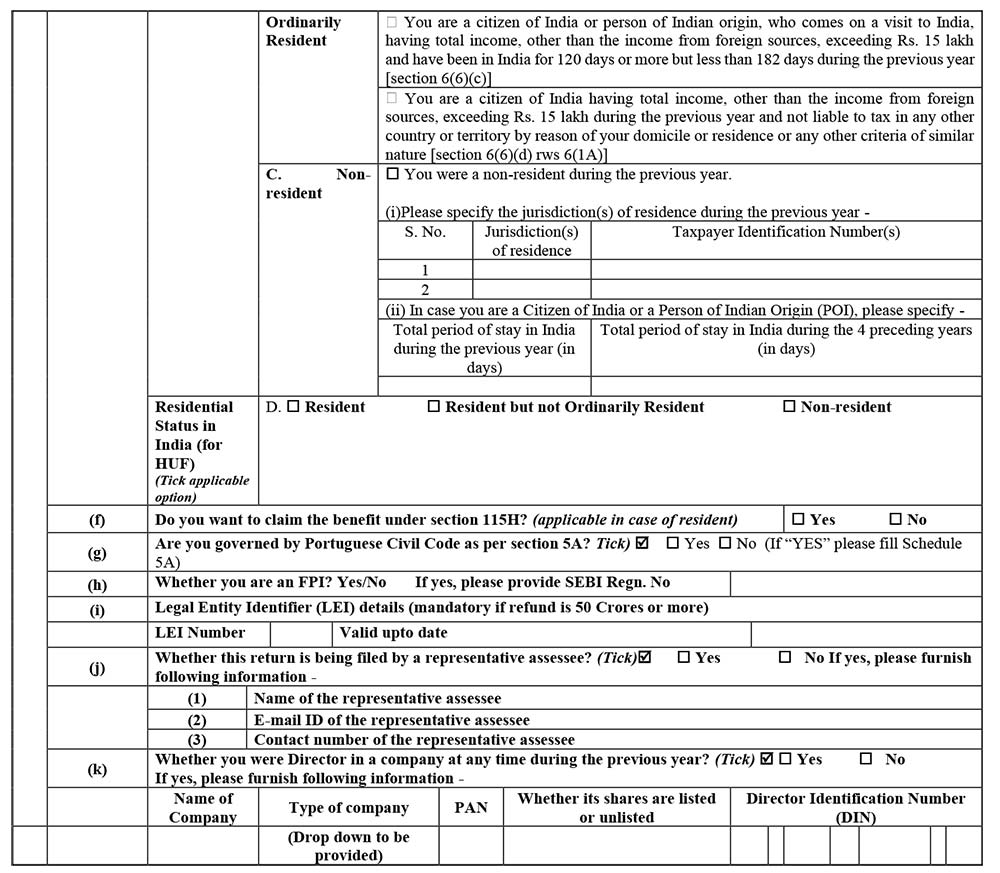

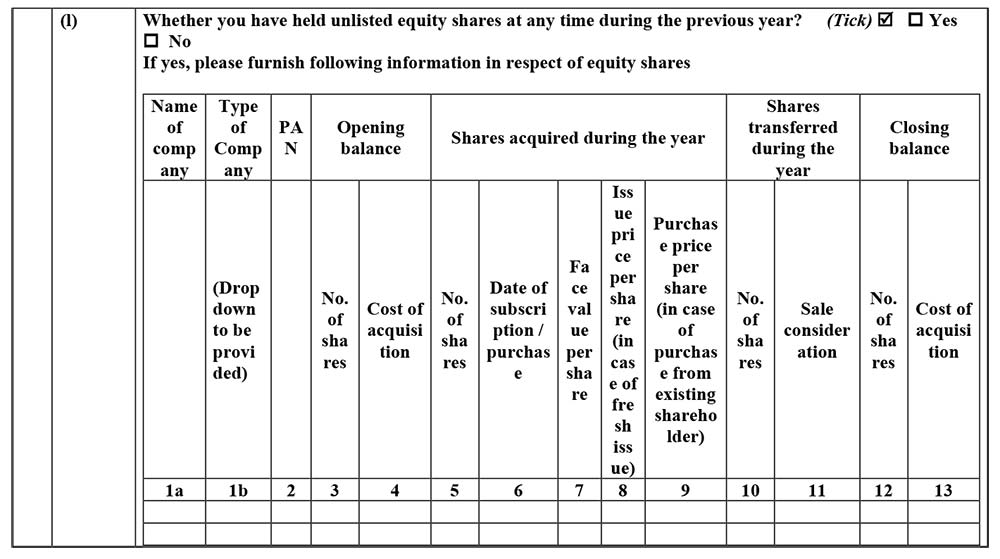

Structure of ITR 2 Filing for AY 2026-27 Online

Part A: General Information

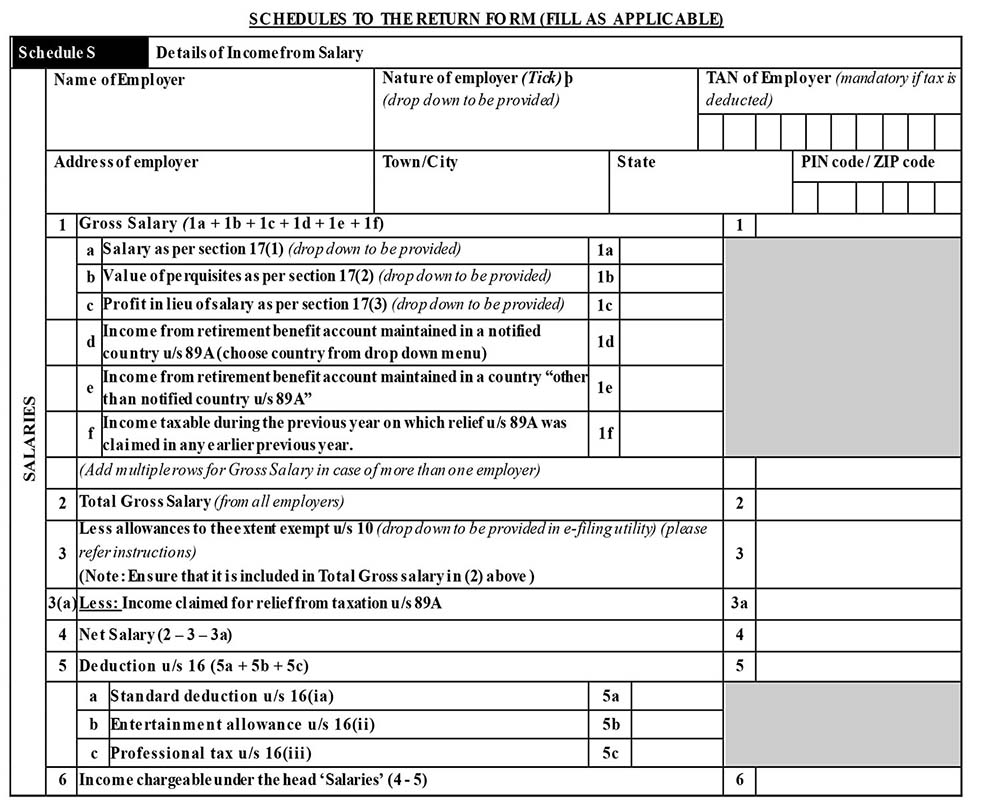

Schedule S: Details of Income from Salary

Schedule HP: Details of Income from House Property

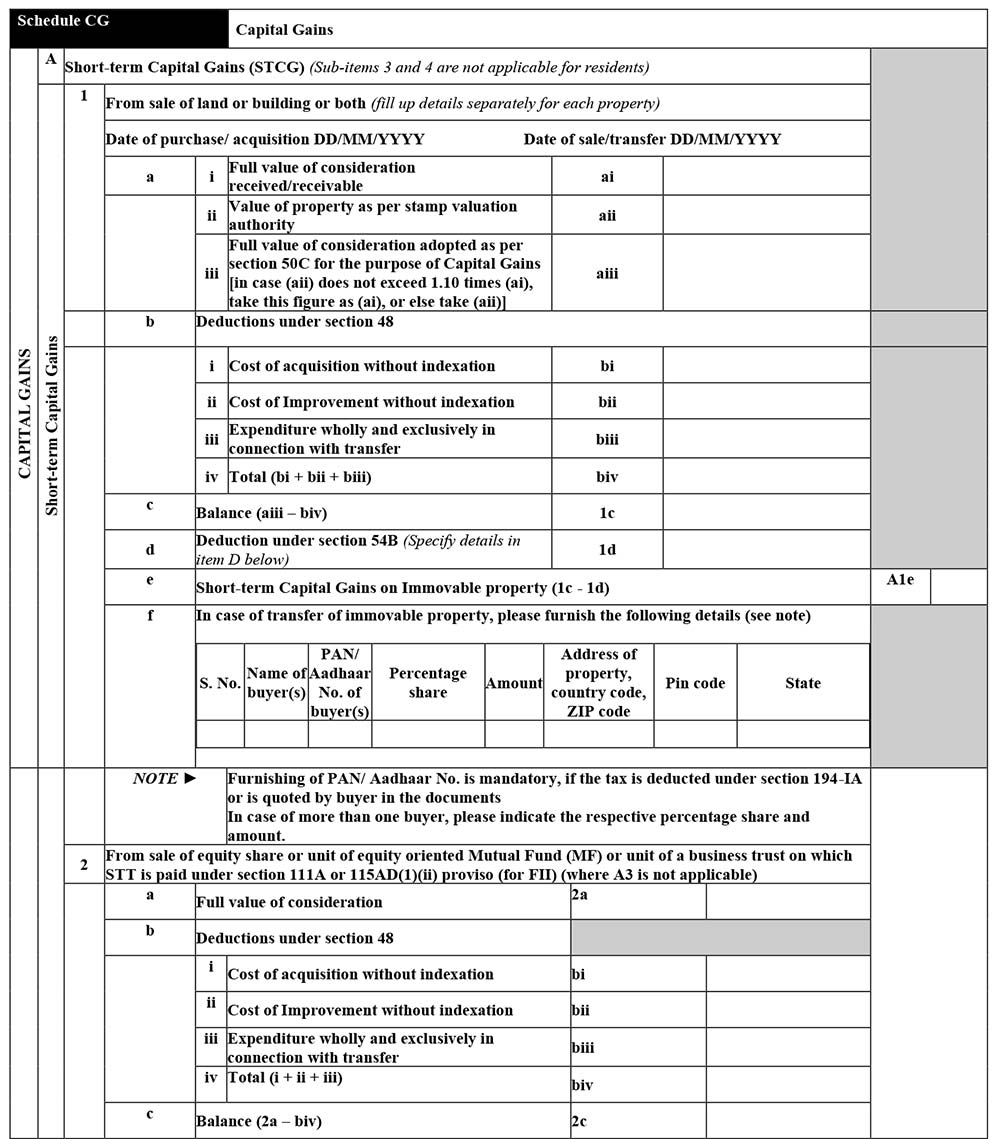

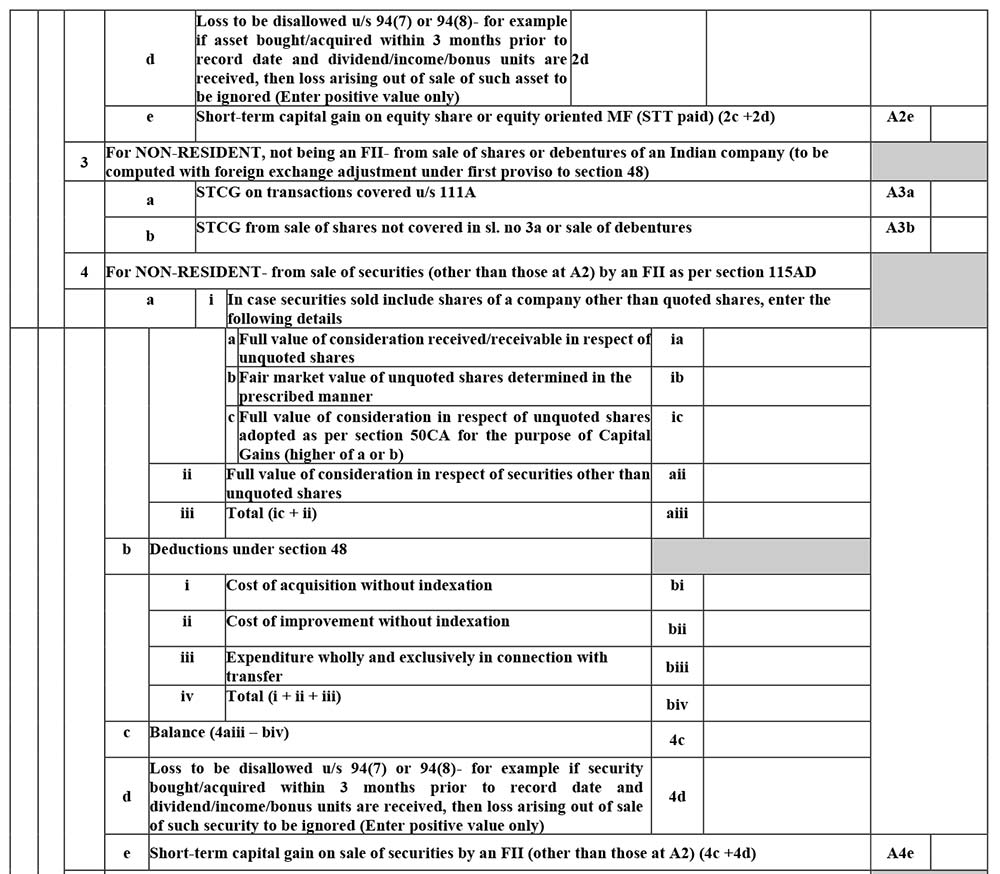

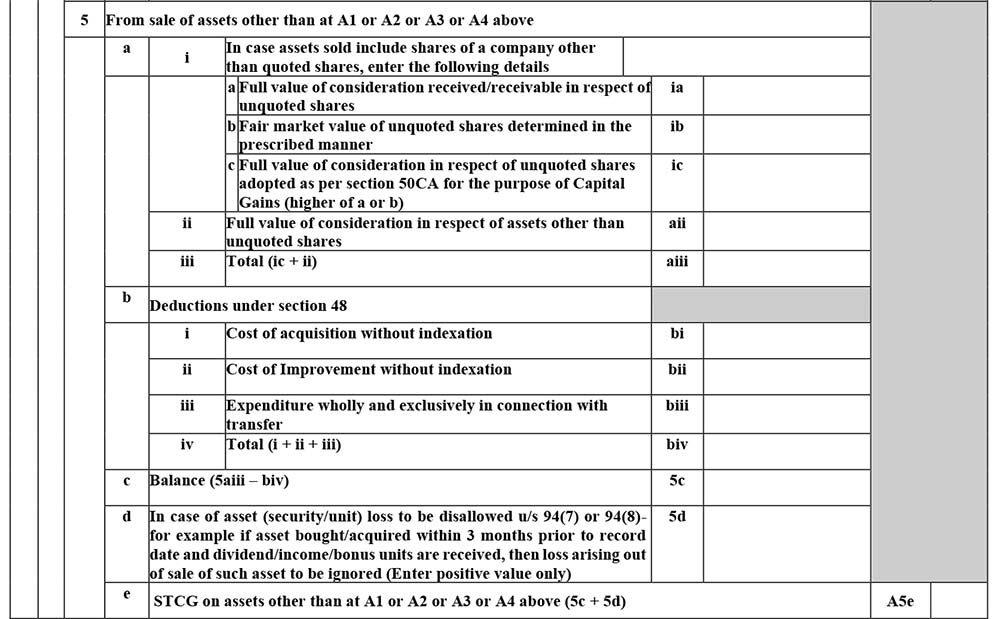

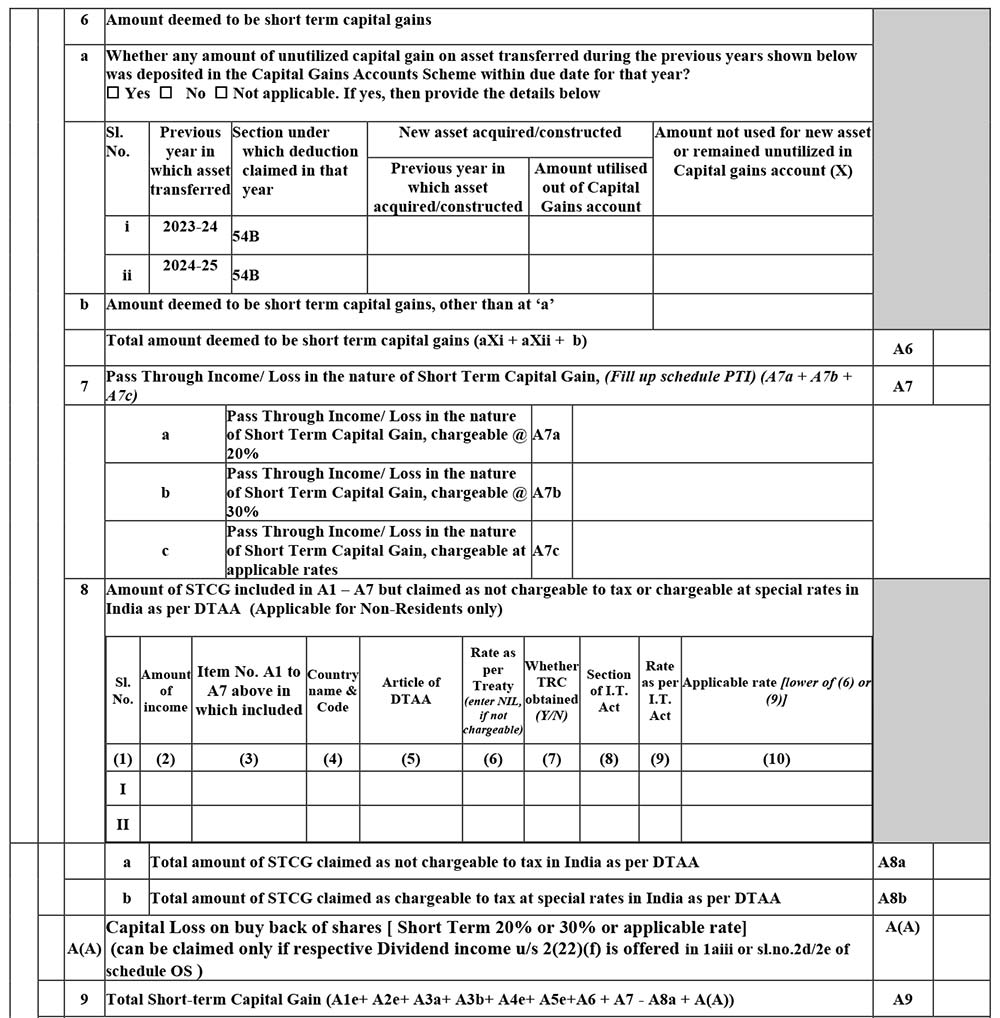

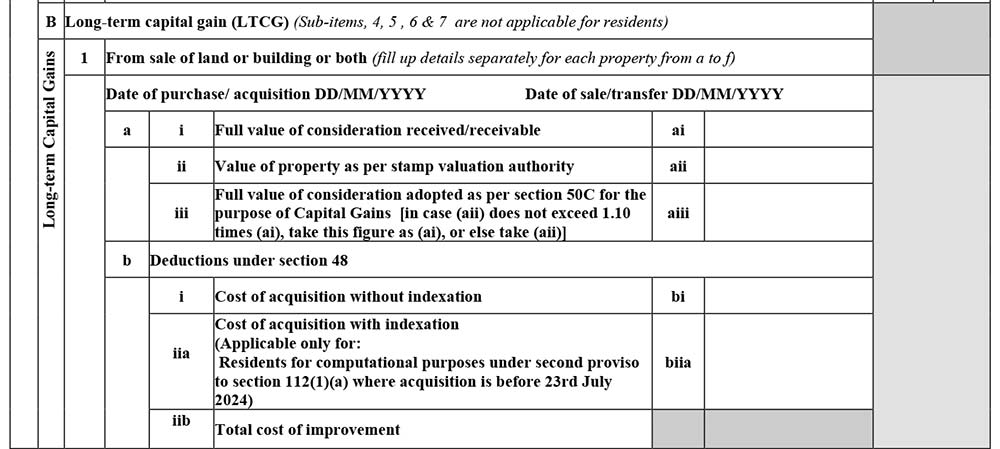

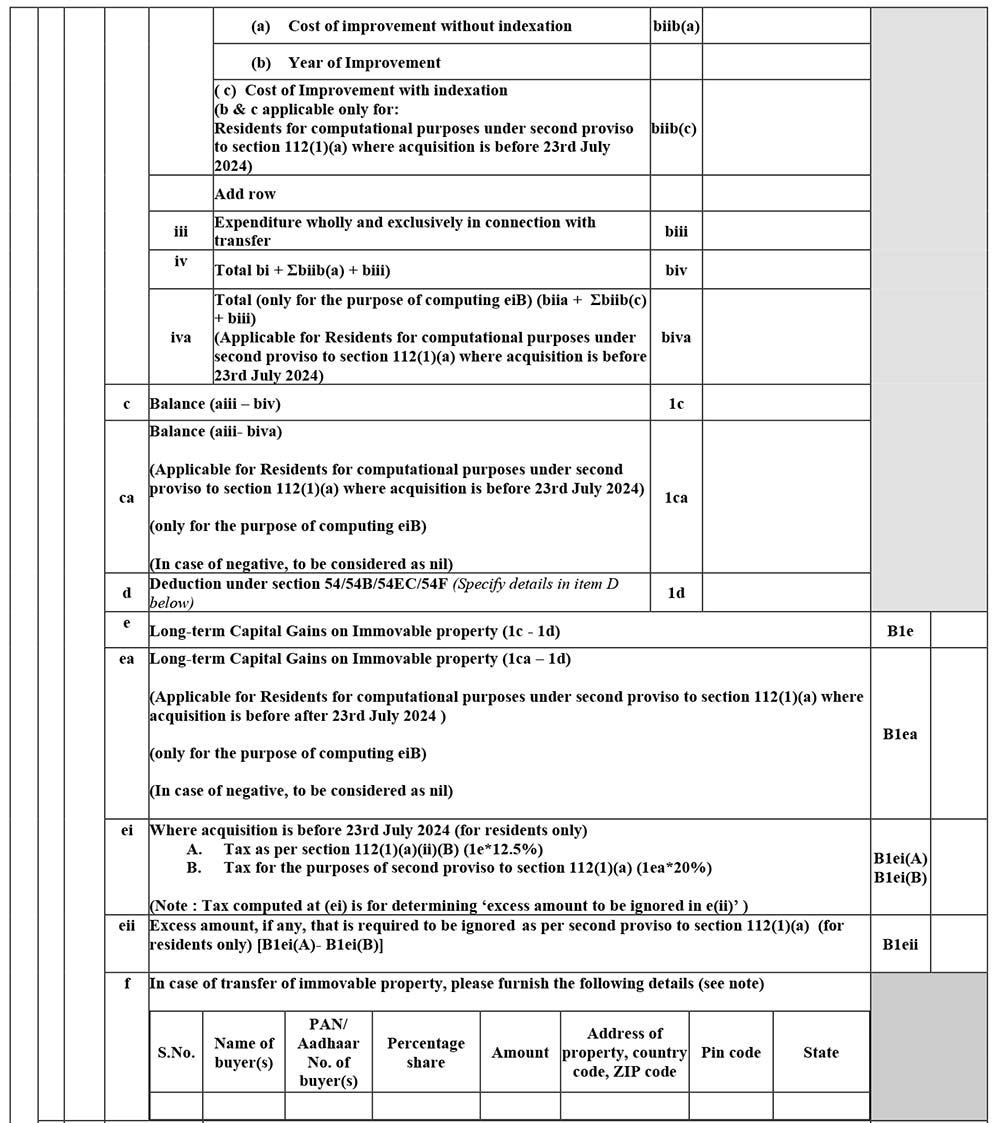

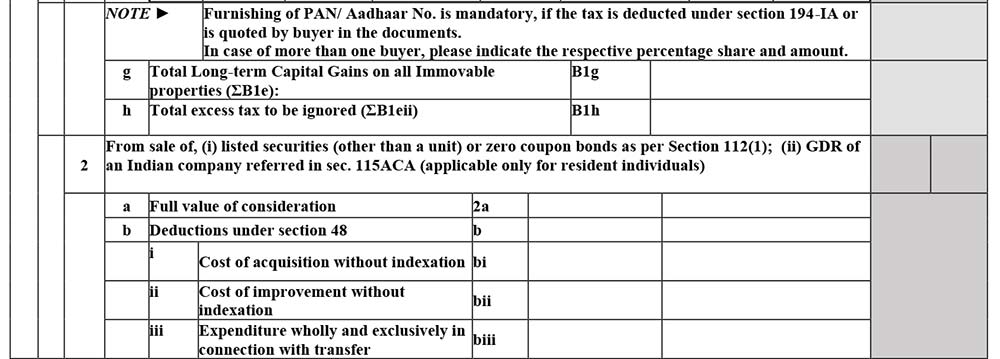

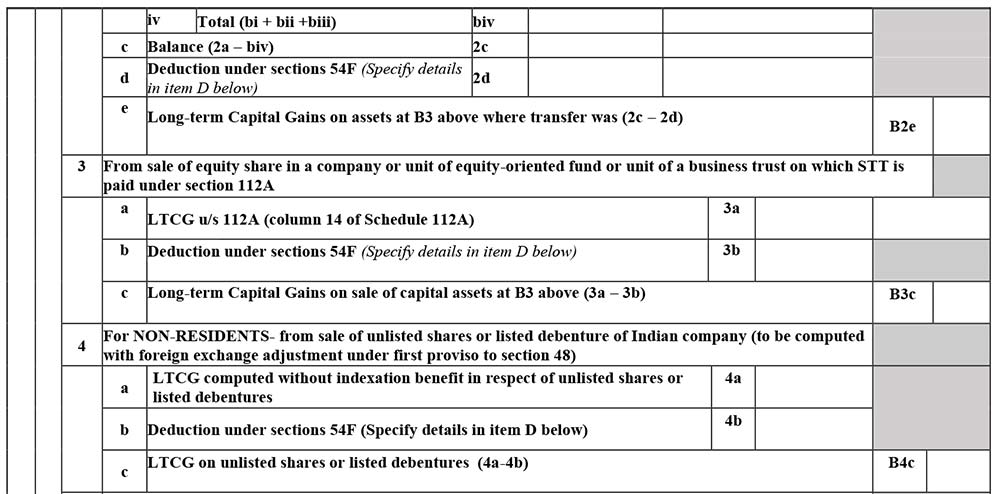

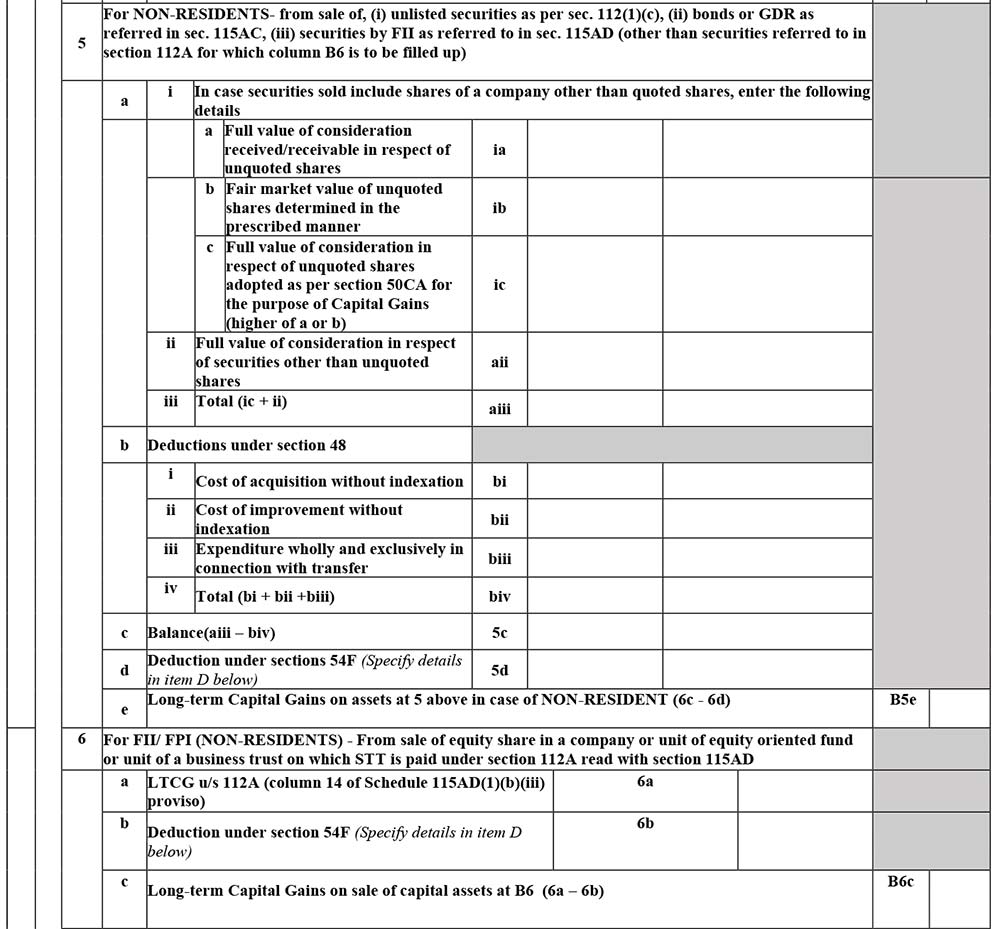

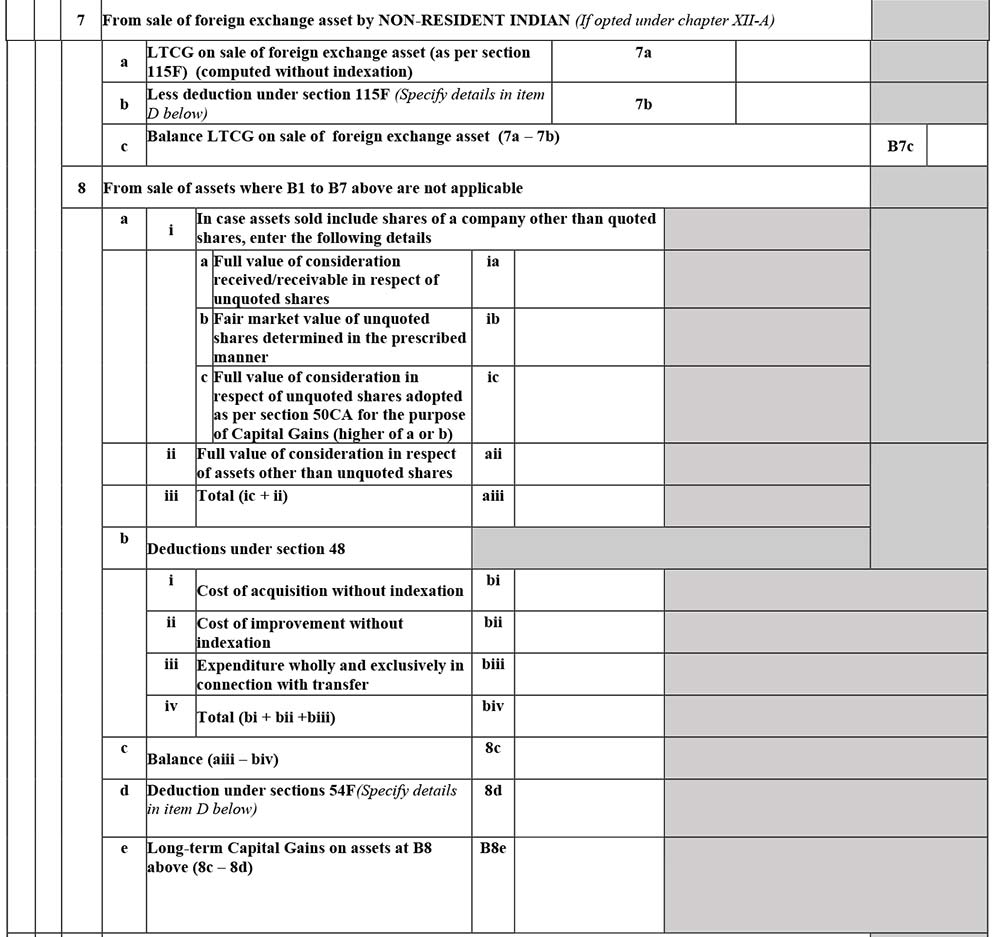

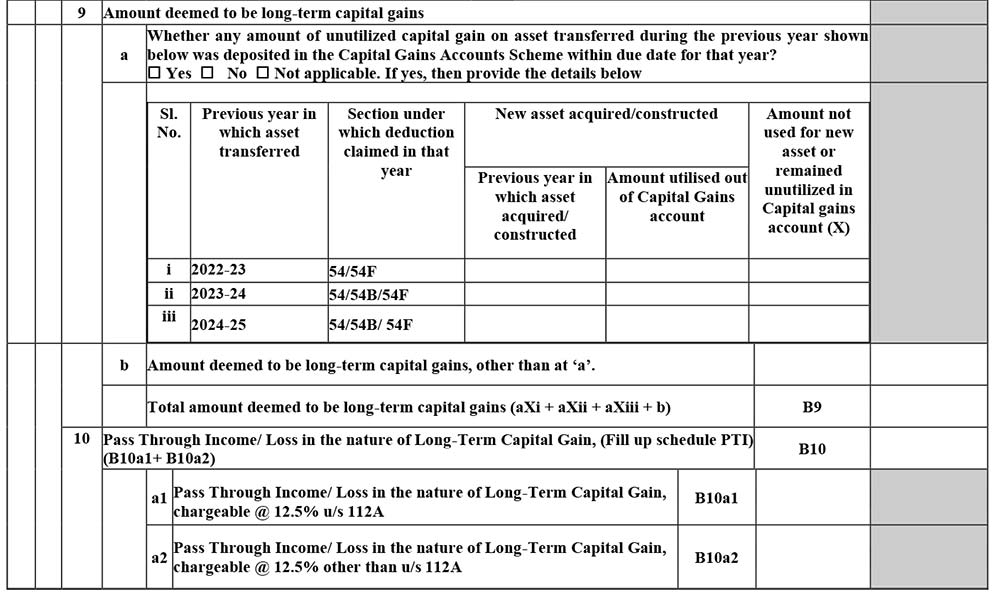

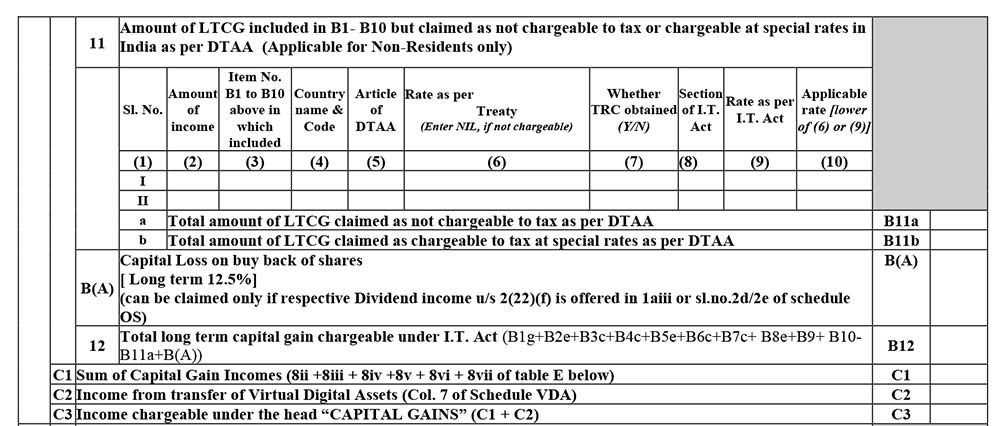

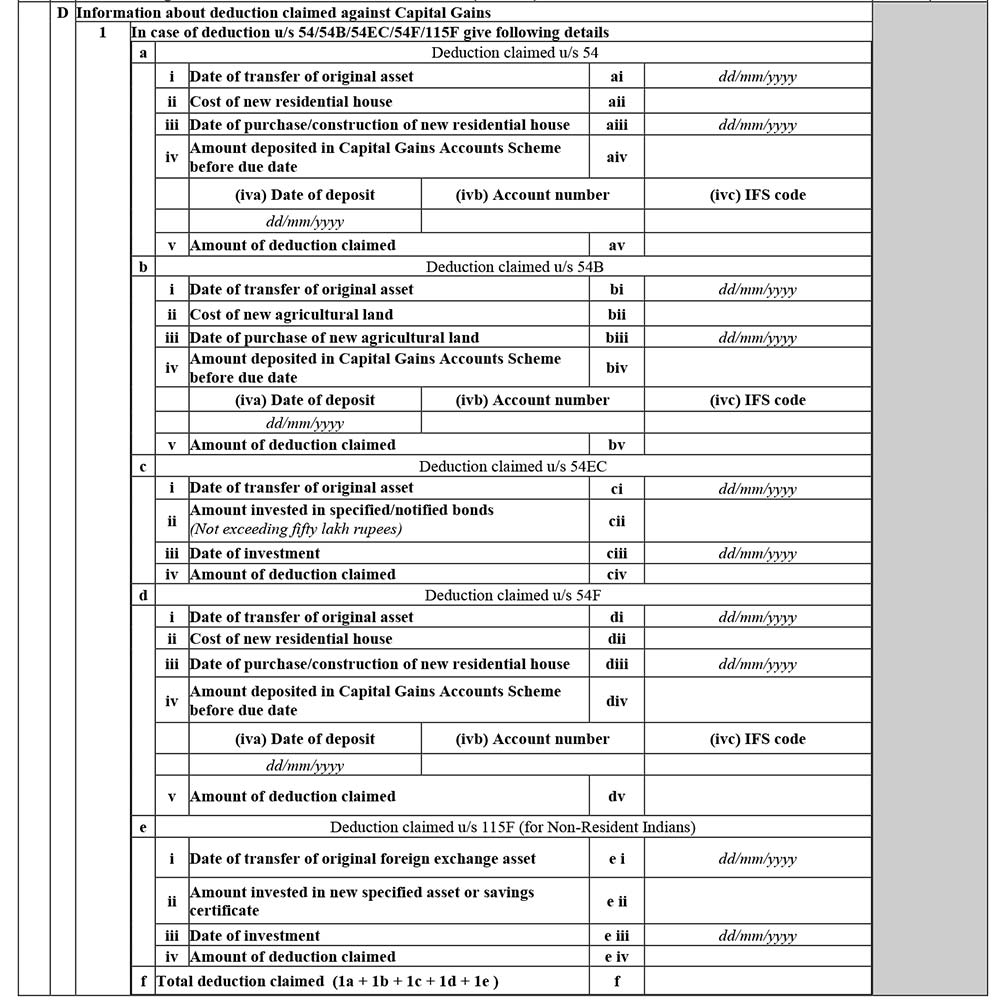

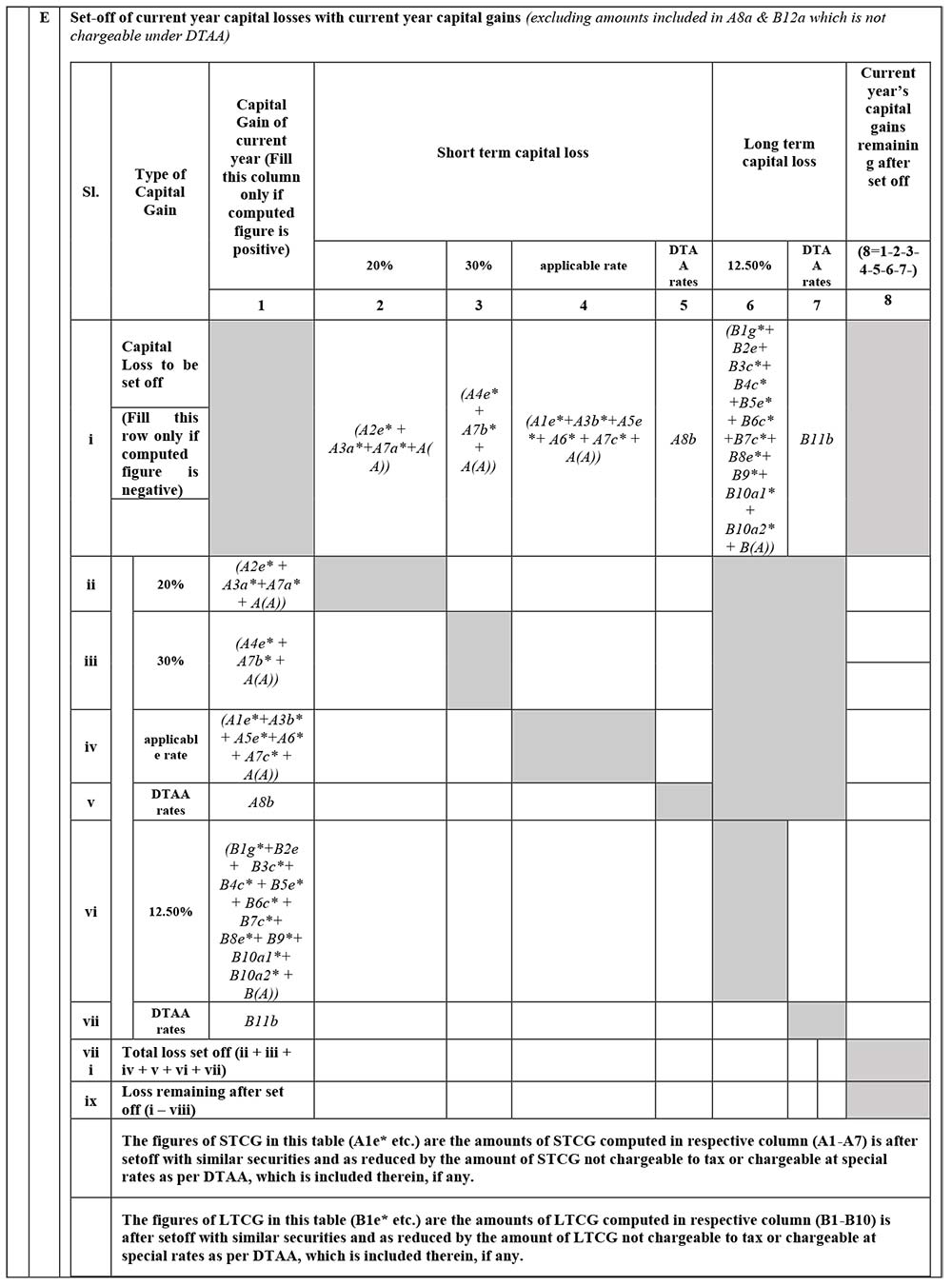

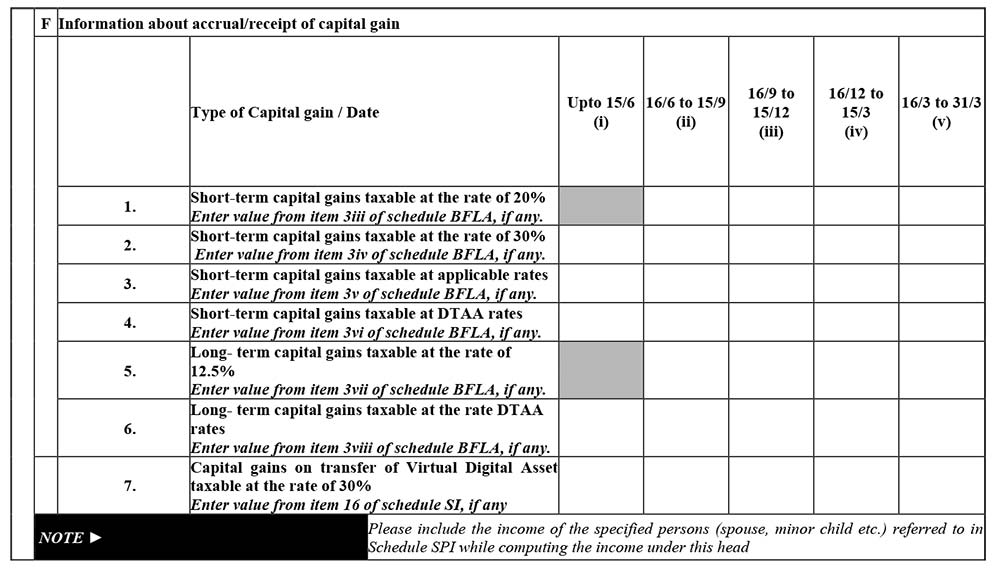

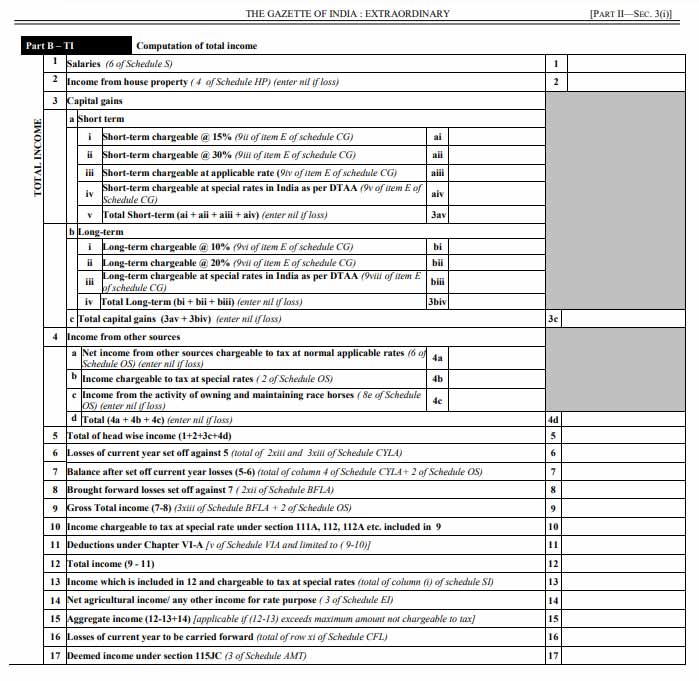

Schedule CG: Capital Gains

The information regarding Capital gains is enclosed with the following details of the taxpayer to furnish:

A. Short-term Capital Gains (STCG)

B. Long-term capital gain (LTCG)

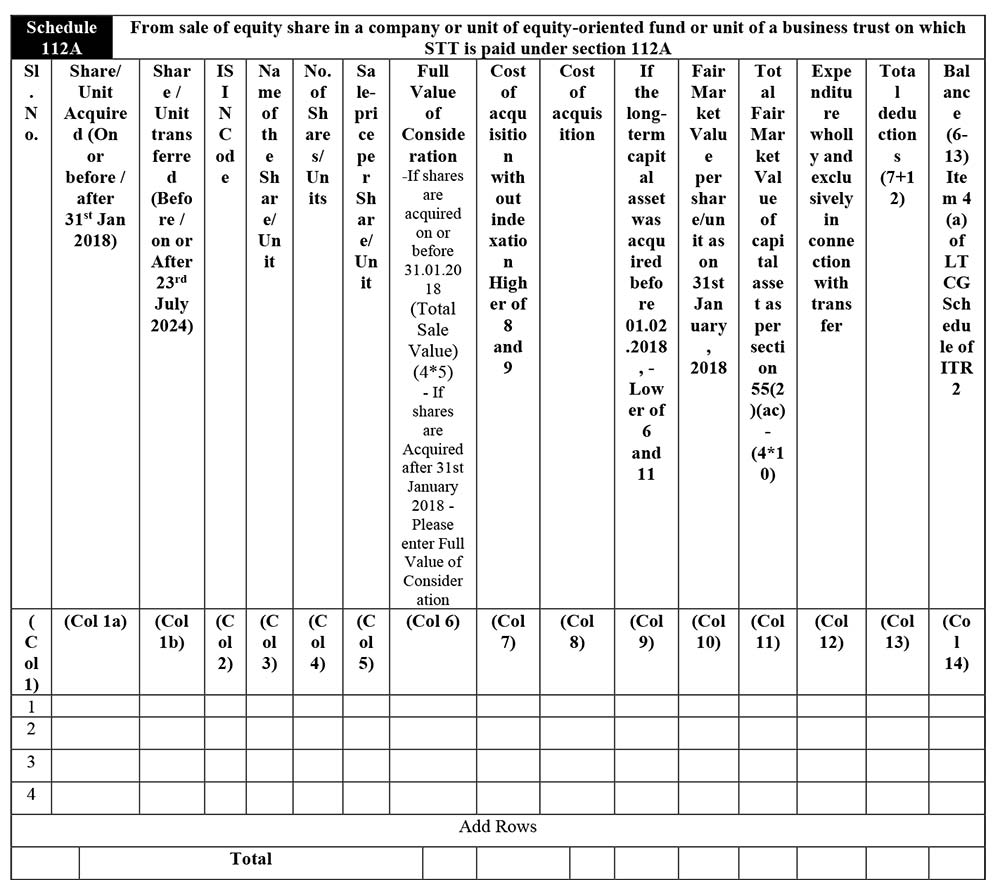

Schedule 112A:

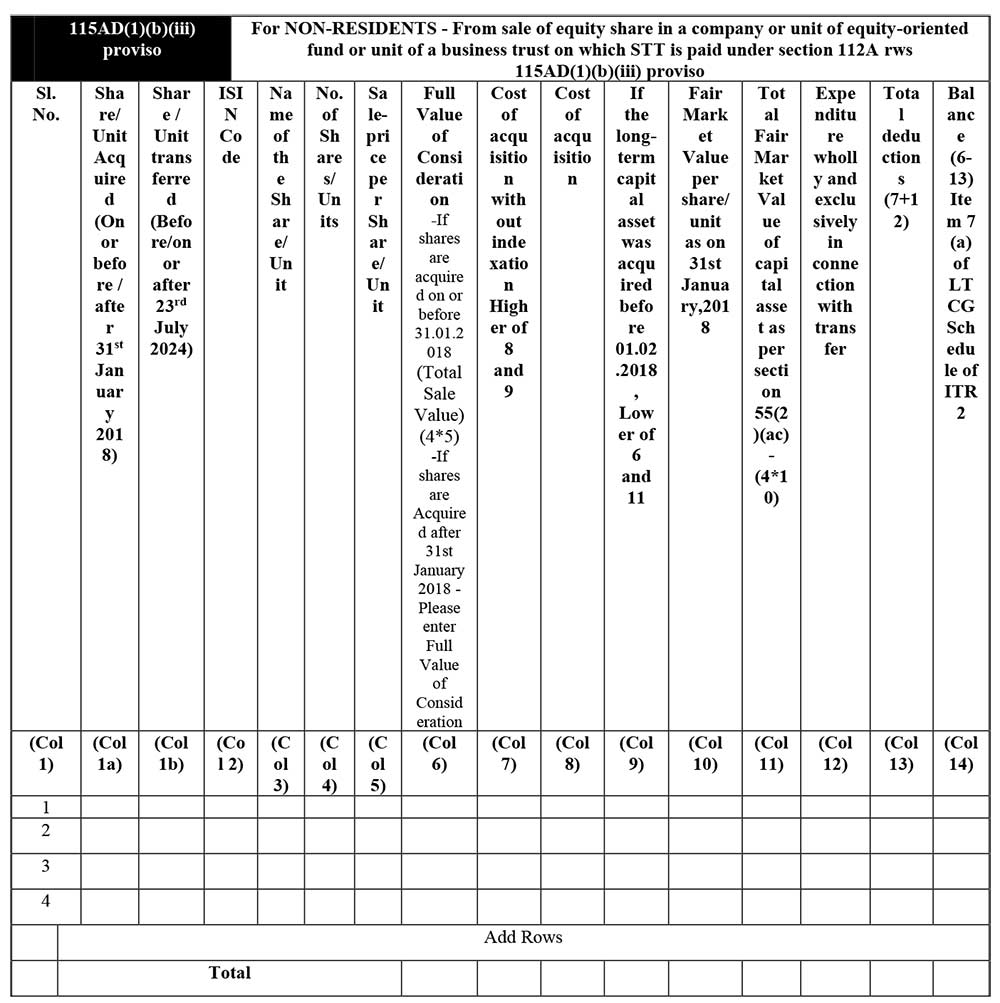

115AD(1)(b)(iii) proviso

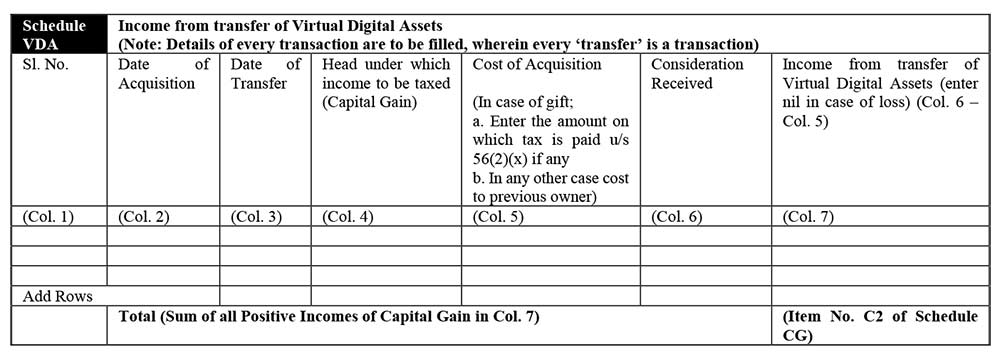

Schedule VDA

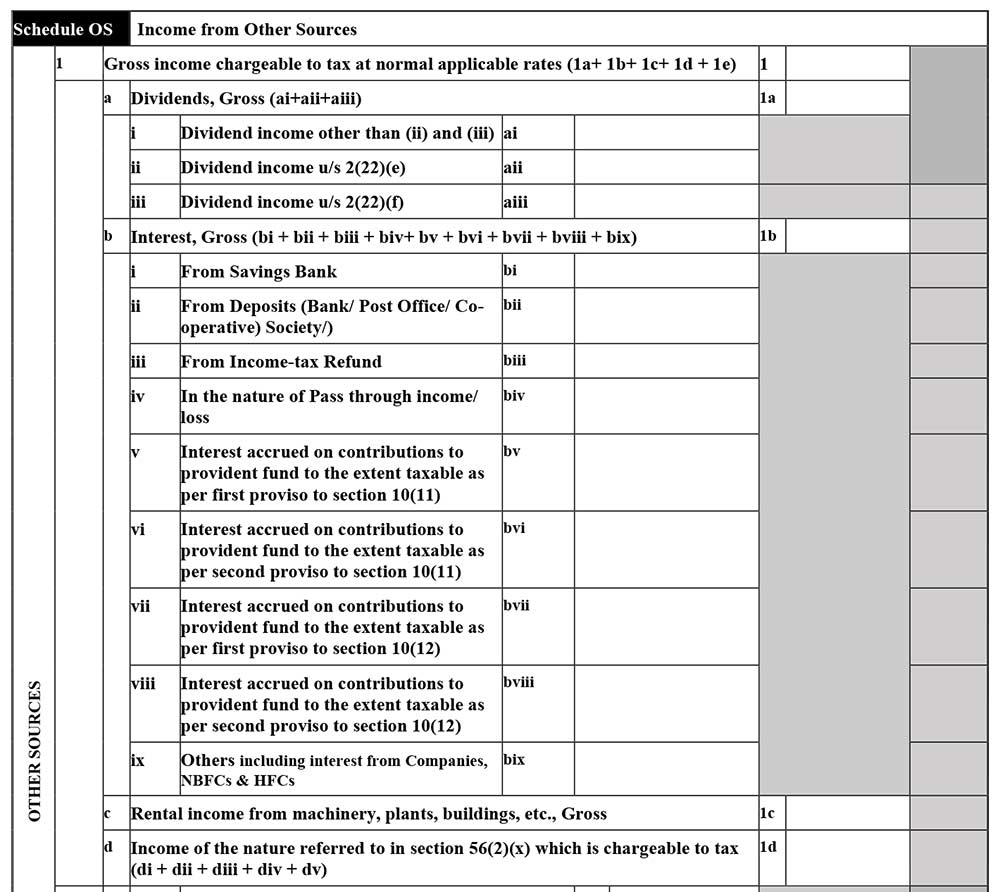

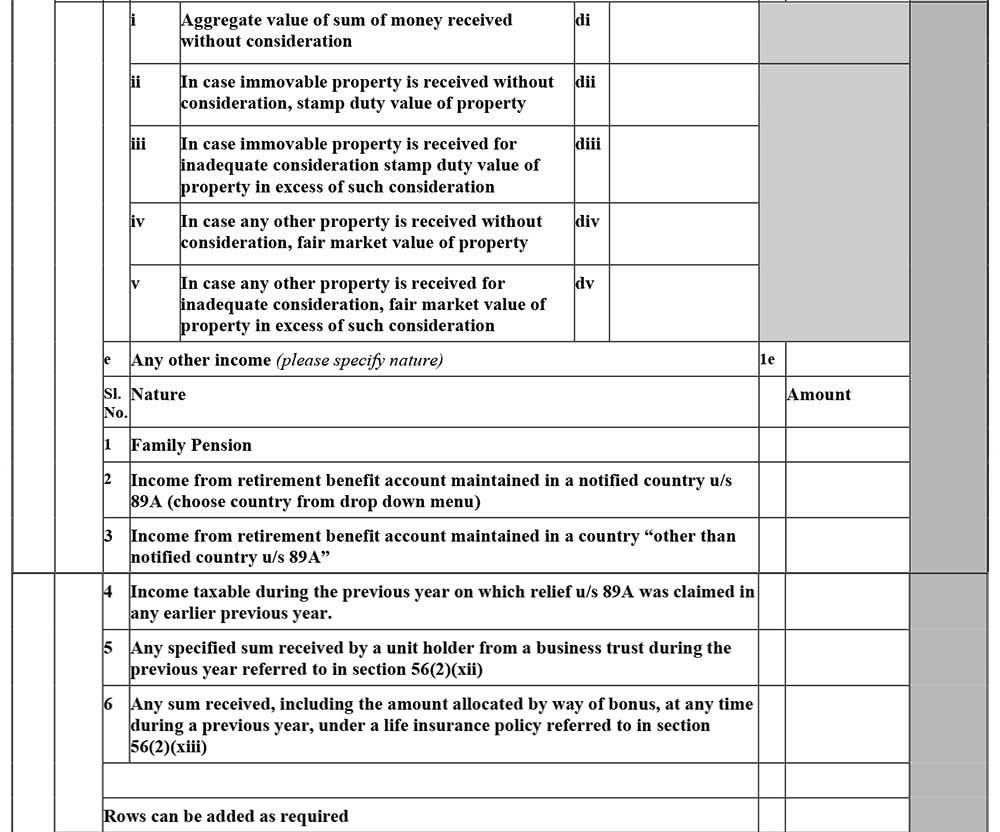

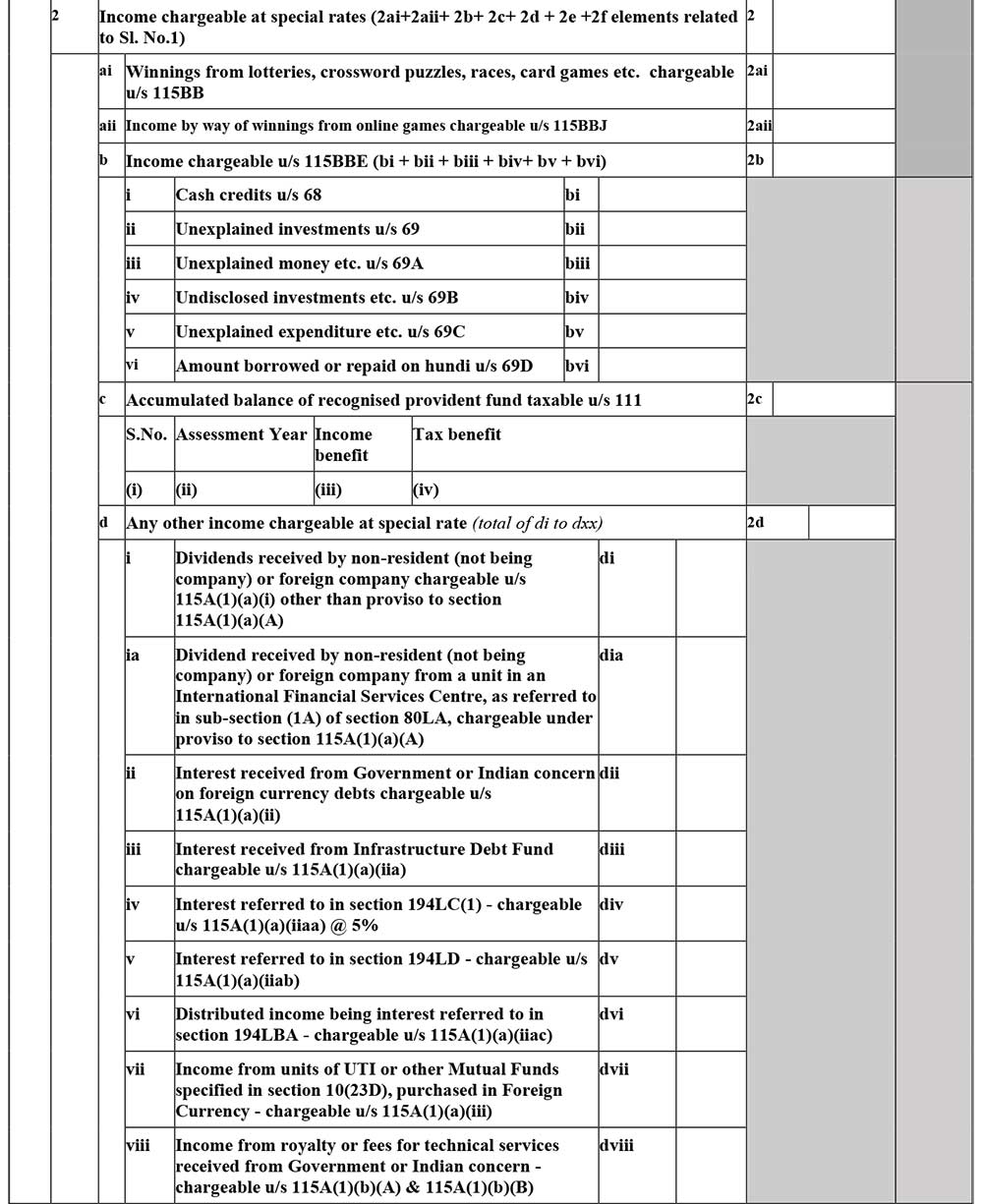

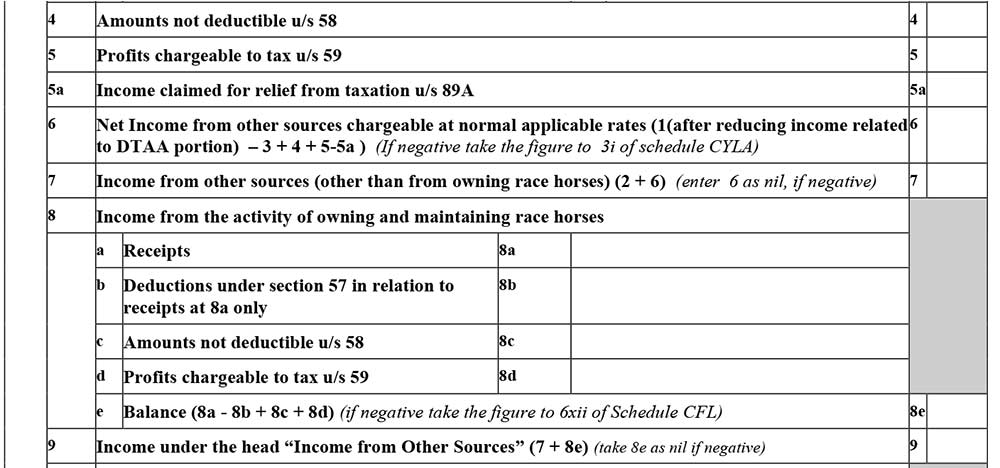

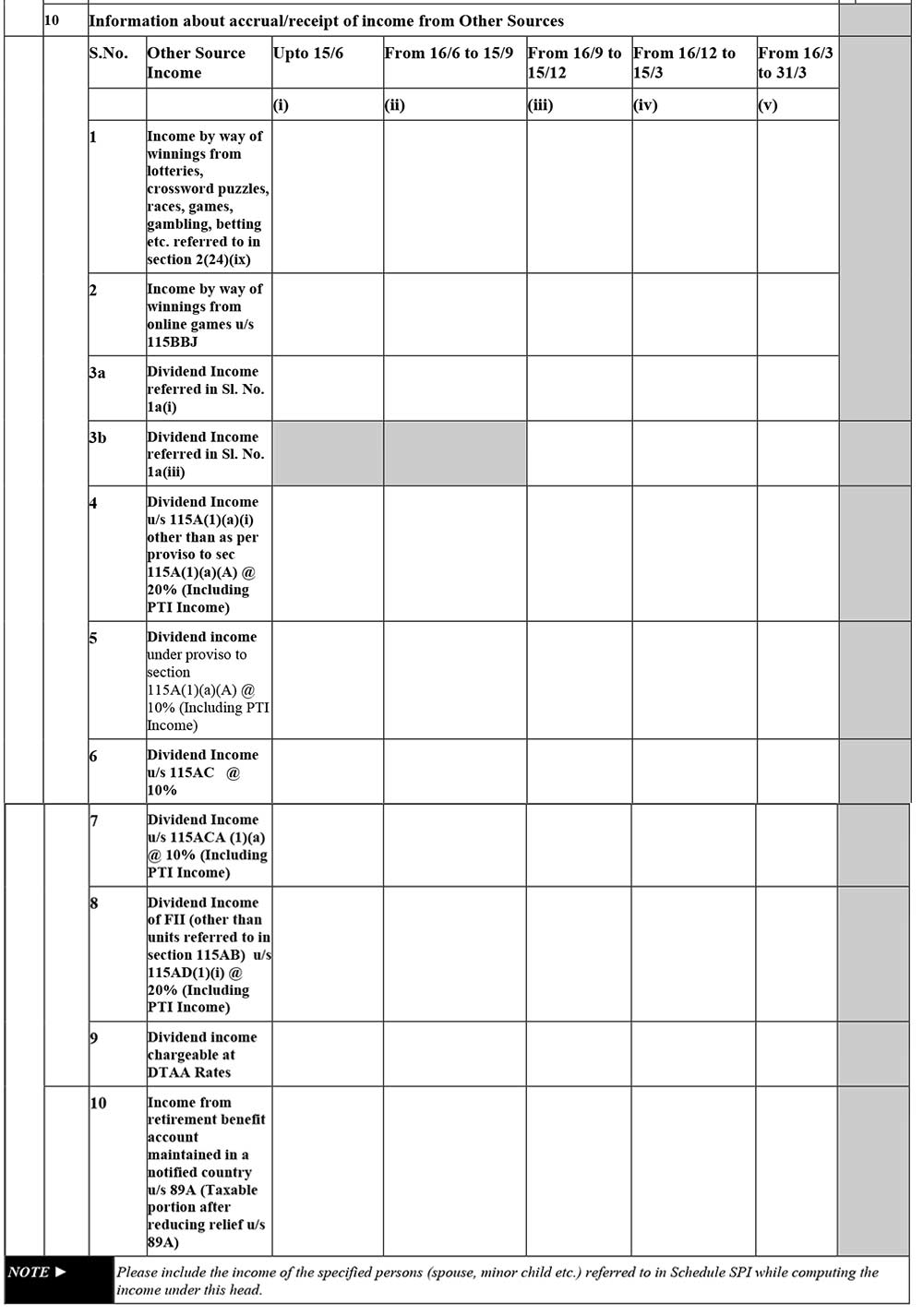

Schedule OS:

- Income from other sources: The information regarding income from other sources is enclosed.

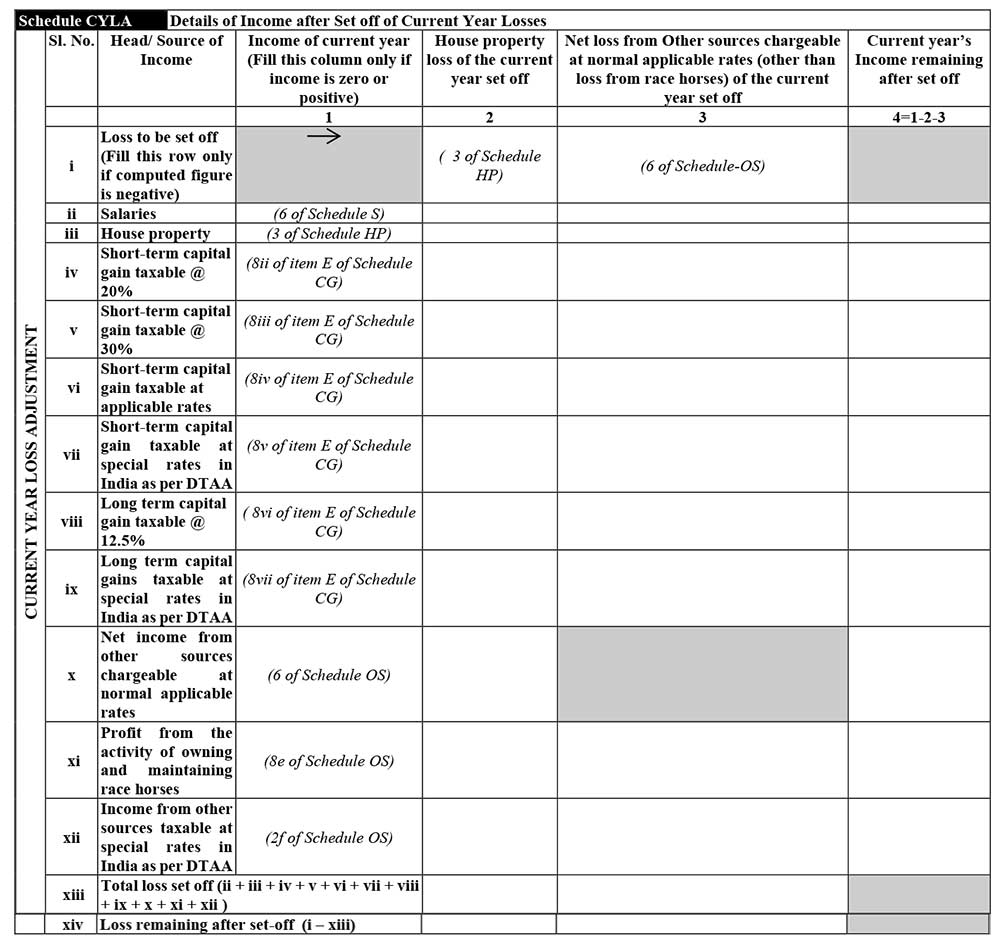

Schedule CYLA:

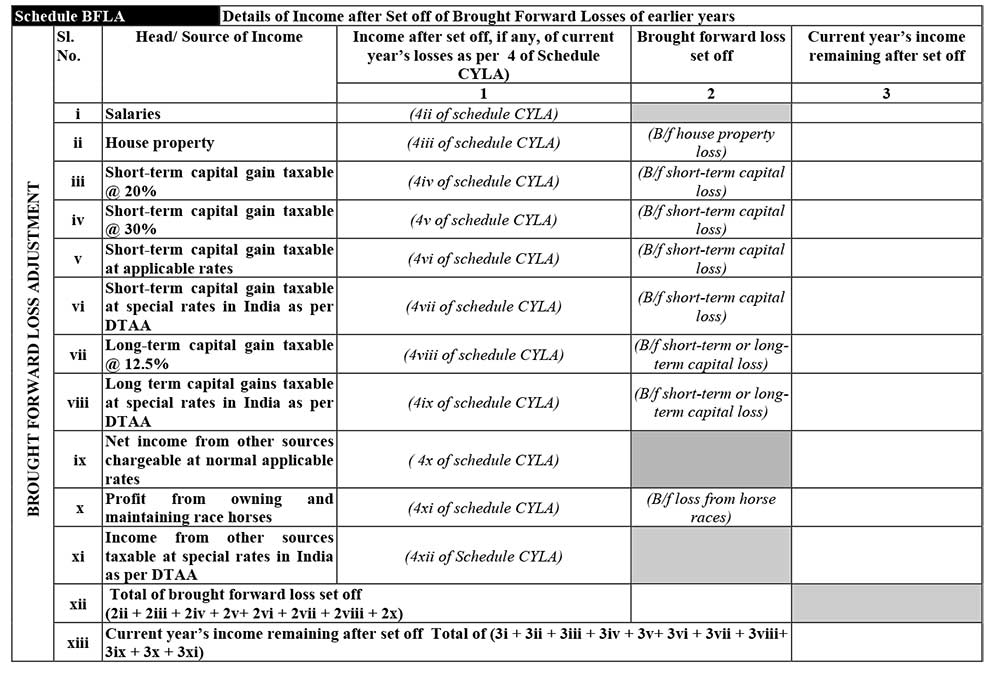

Schedule BFLA:

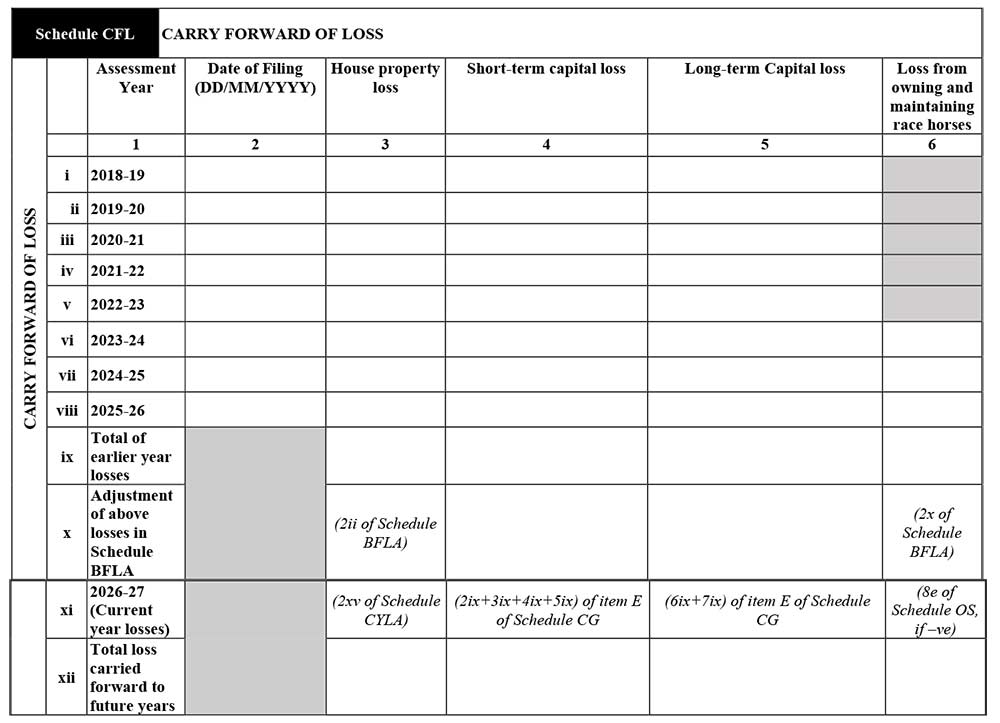

Schedule CFL: Carry Forward of Loss

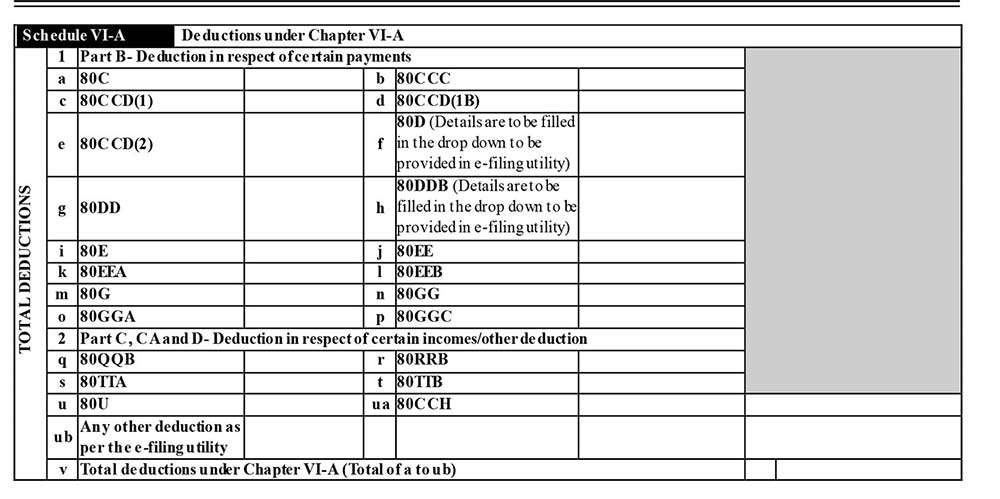

Schedule VI-A: Deductions under Chapter VI-A

Details under this title are enclosed with the following details of the taxpayer to furnish:

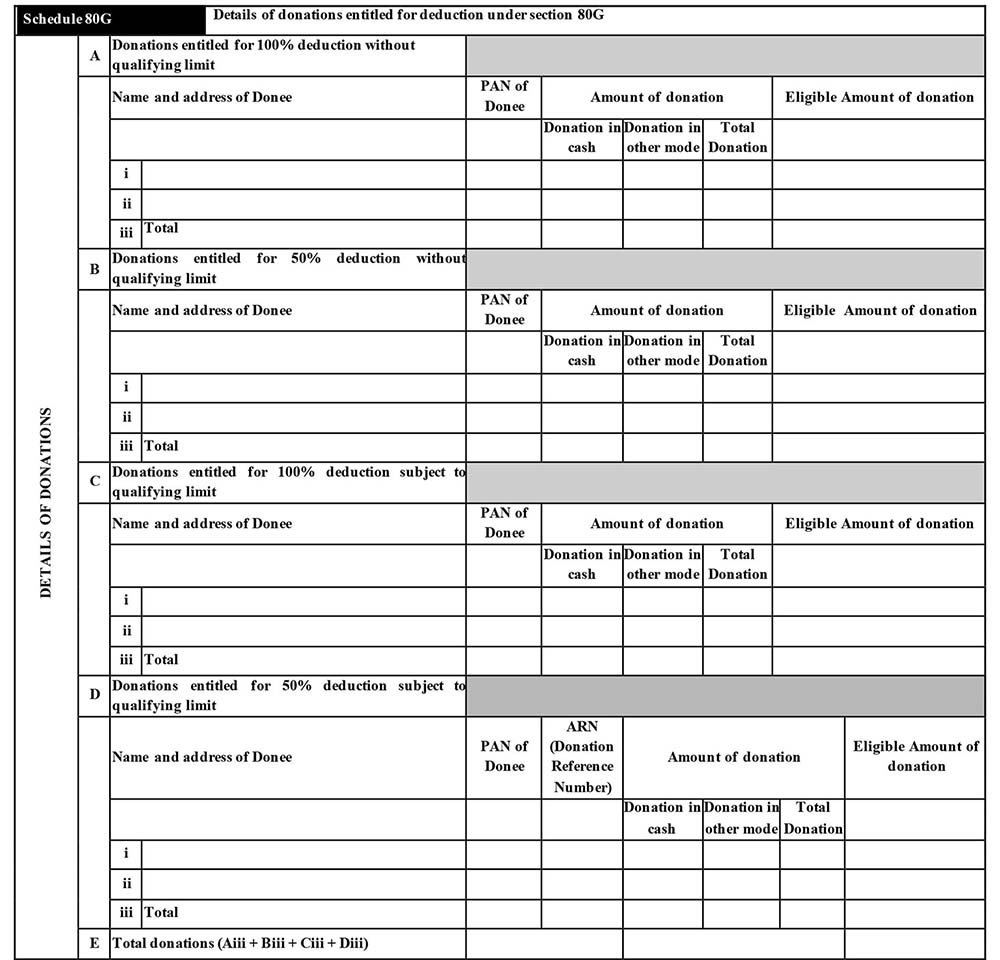

Schedule 80G: Details of donations entitled for deduction under section 80G

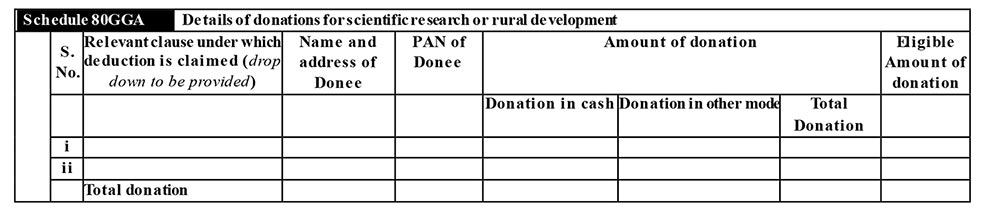

Schedule 80GGA: Details of donations for scientific research or rural development

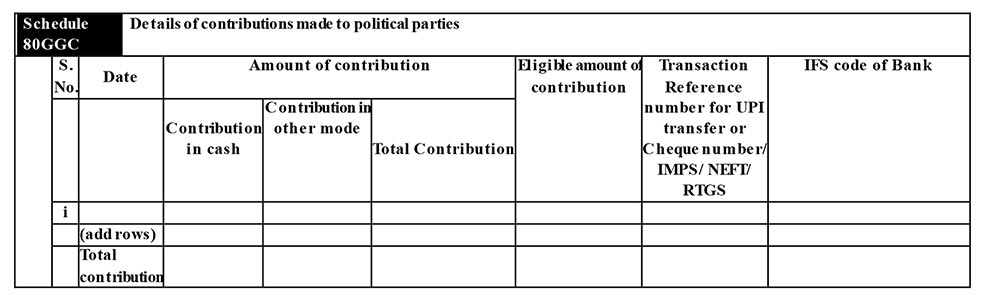

Schedule 80GGC: Details of contributions made to political parties.

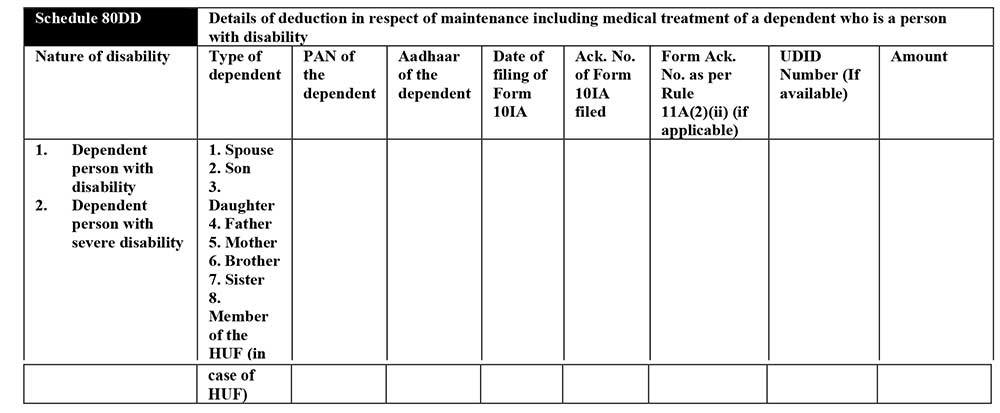

Schedule 80DD: Details of deduction in respect of maintenance including medical treatment of a dependent who is a person with disability.

Schedule 80U: Details of deduction in case of a person with disability

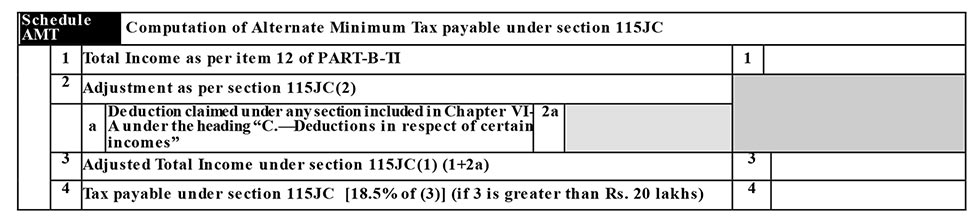

Schedule AMT: Computation of Alternate Minimum Tax payable under section 115JC

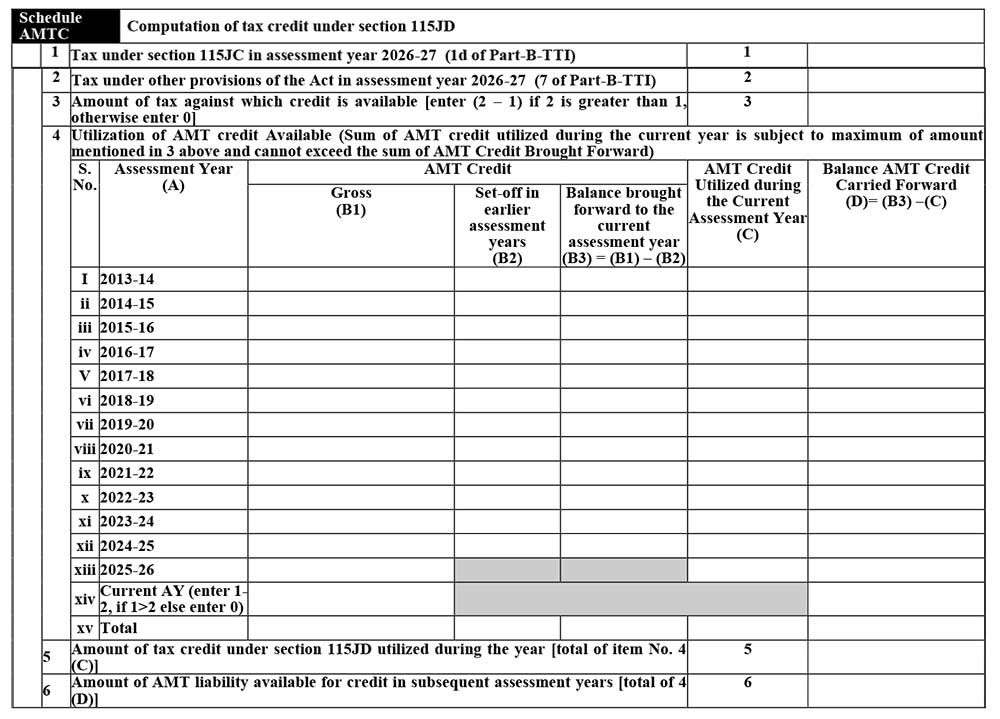

Schedule AMTC: Computation of tax credit under section 115JD

Schedule SPI: Income of specified persons (spouse, minor child etc.), includable in the income of the assessee as per section 64

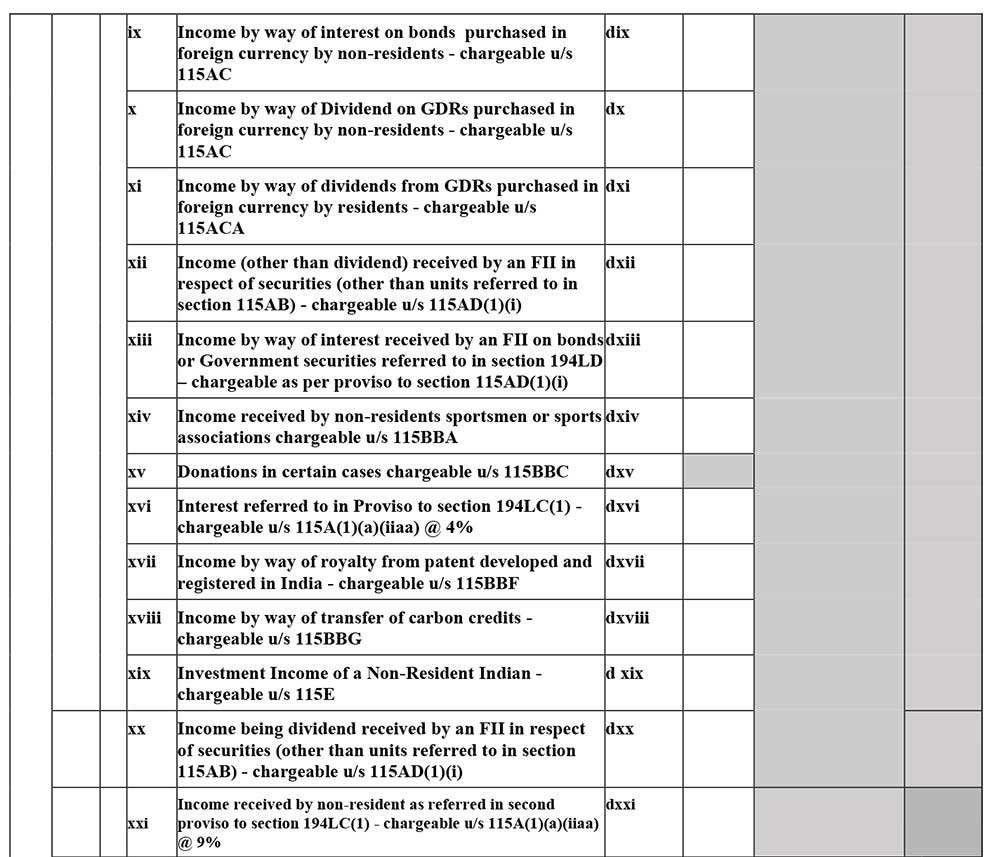

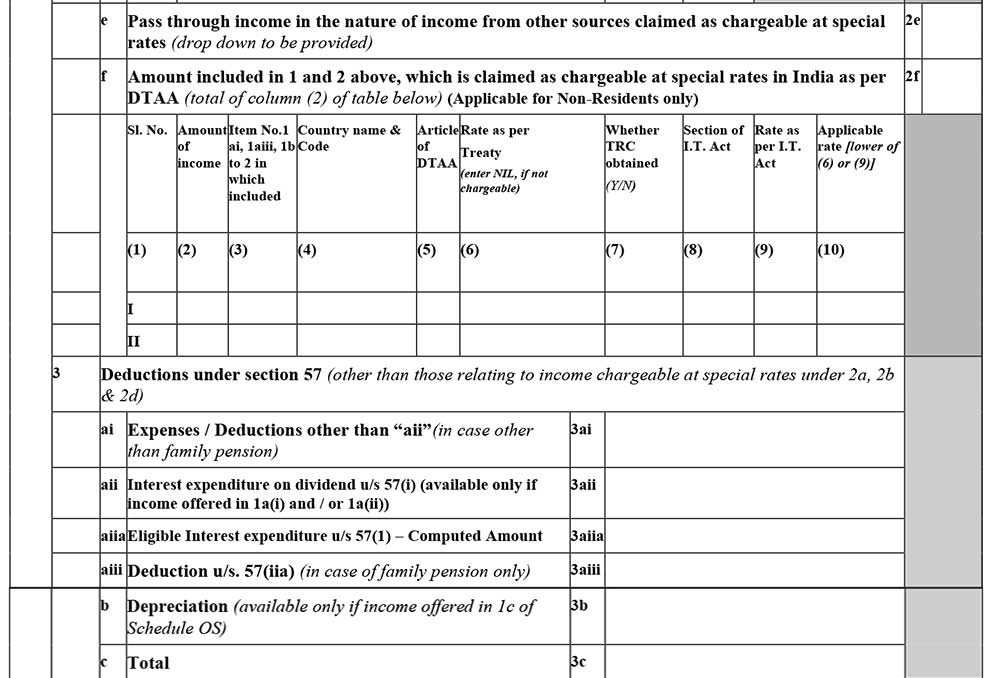

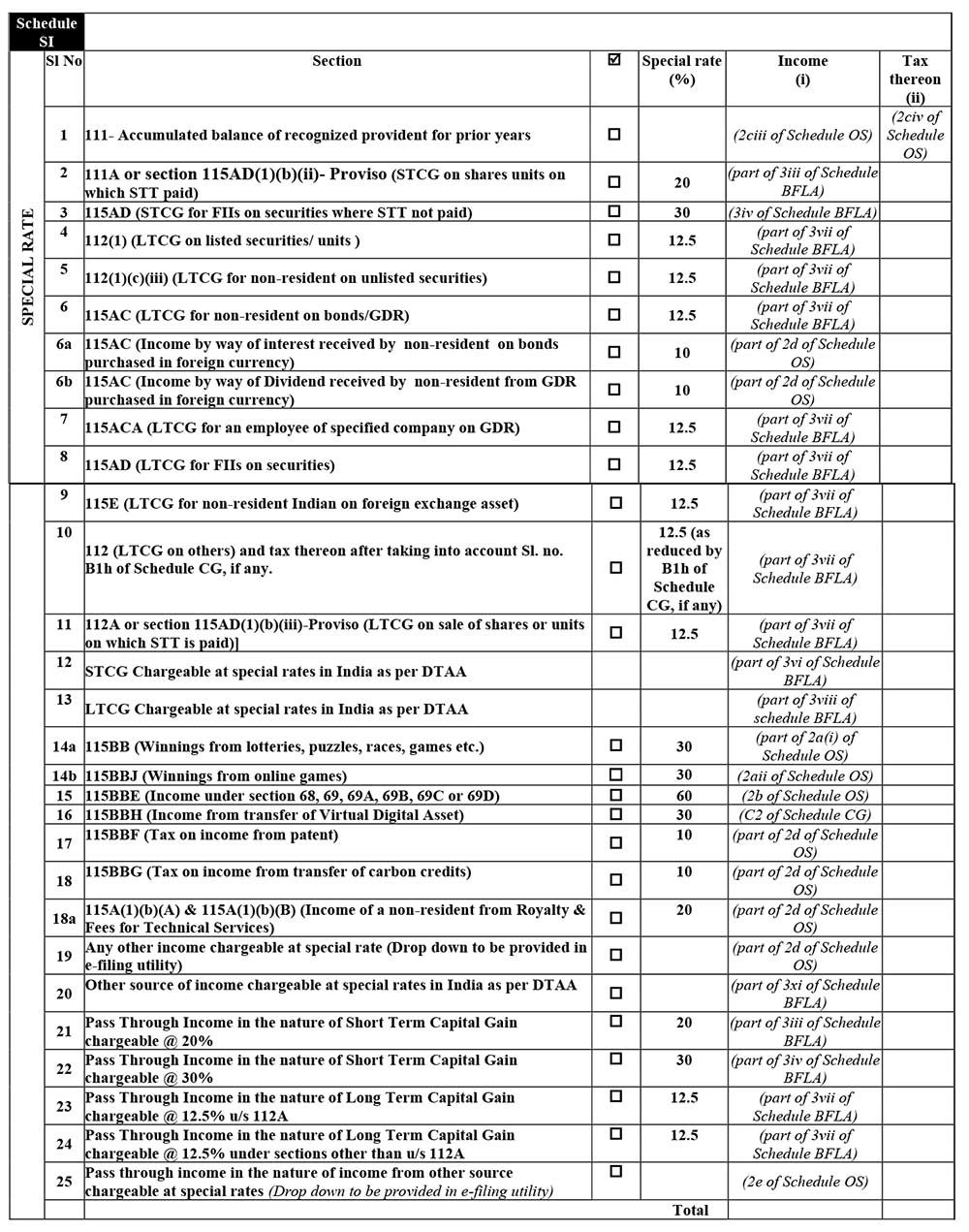

Schedule SI: Income chargeable to tax at special rates

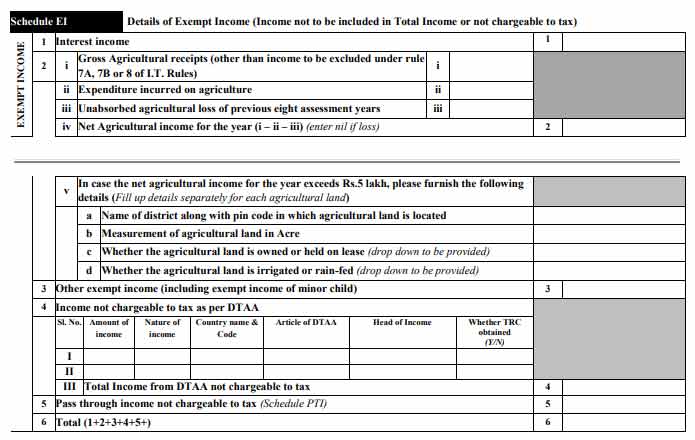

Schedule EI: Details of Exempt Income (Income not to be included in Total Income or not chargeable to tax)

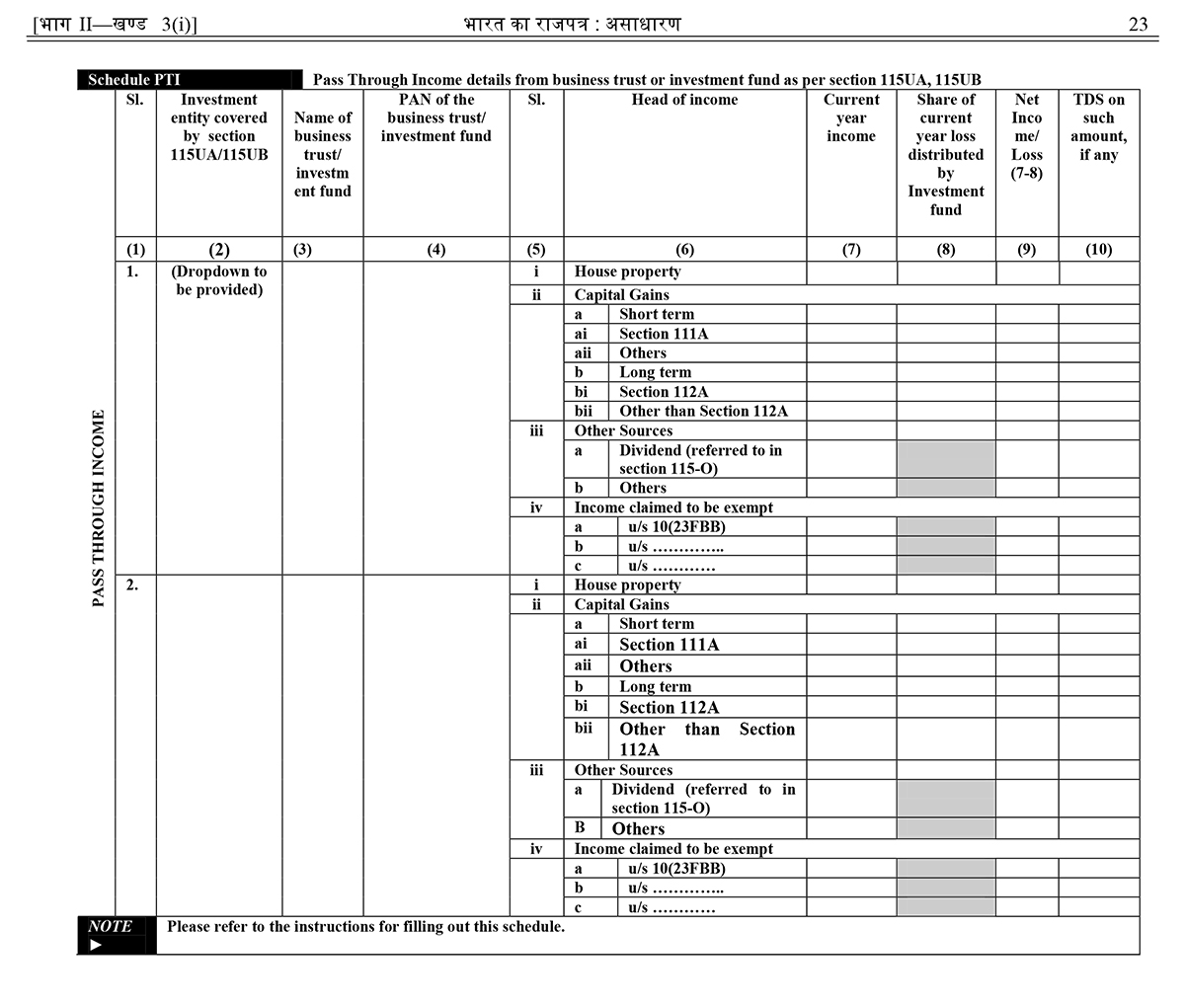

Schedule PTI: Pass Through Income details from business trust or investment fund as per section 115U, 115UA and 115UB

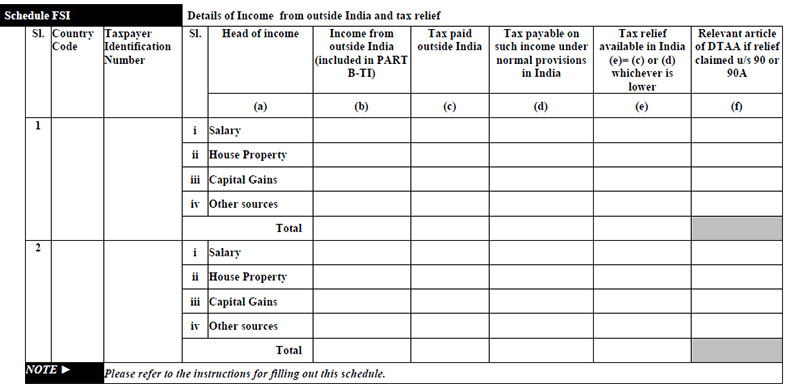

Schedule FSI: Details of Income from outside India and tax relief

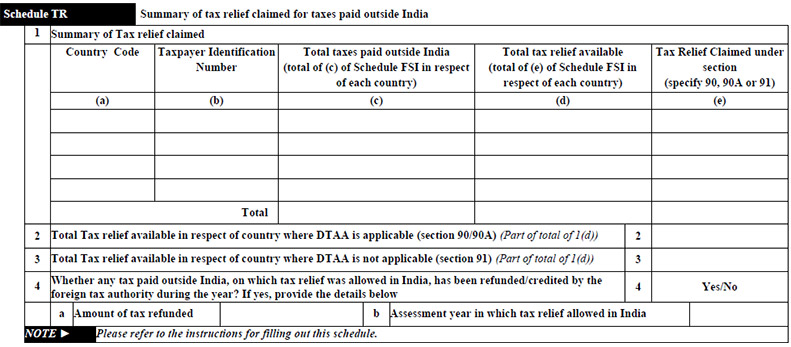

Schedule TR: Summary of tax relief claimed for taxes paid outside India

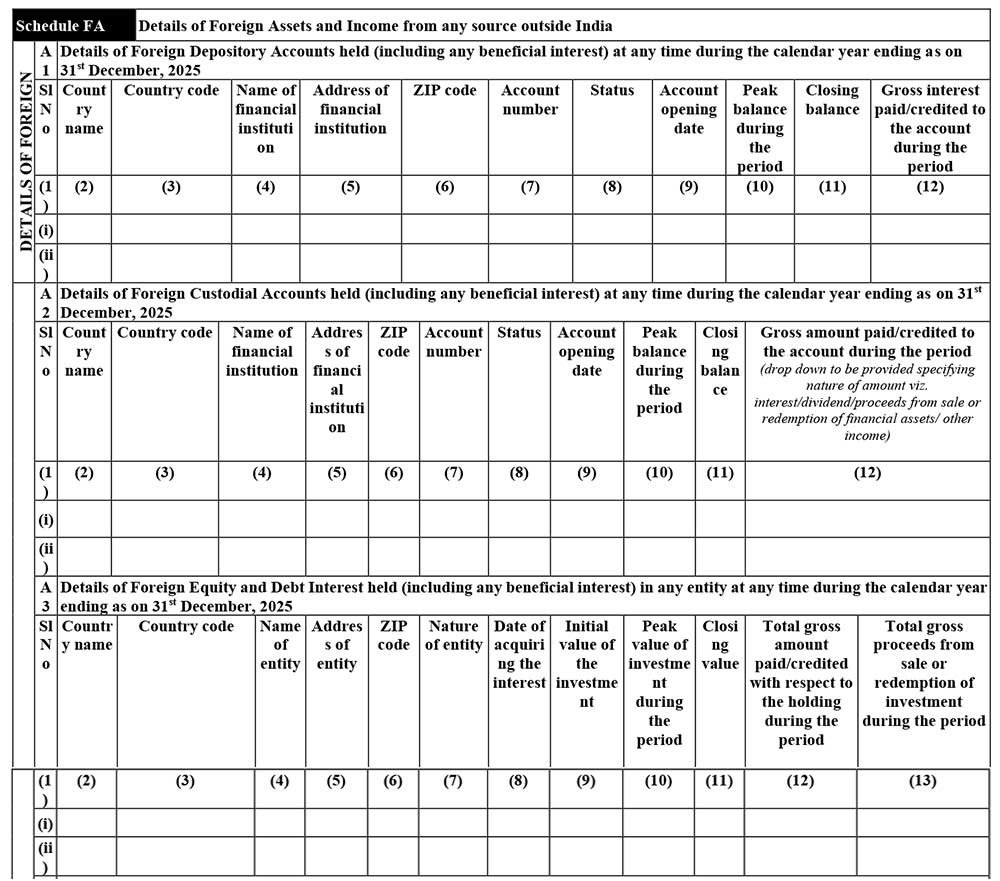

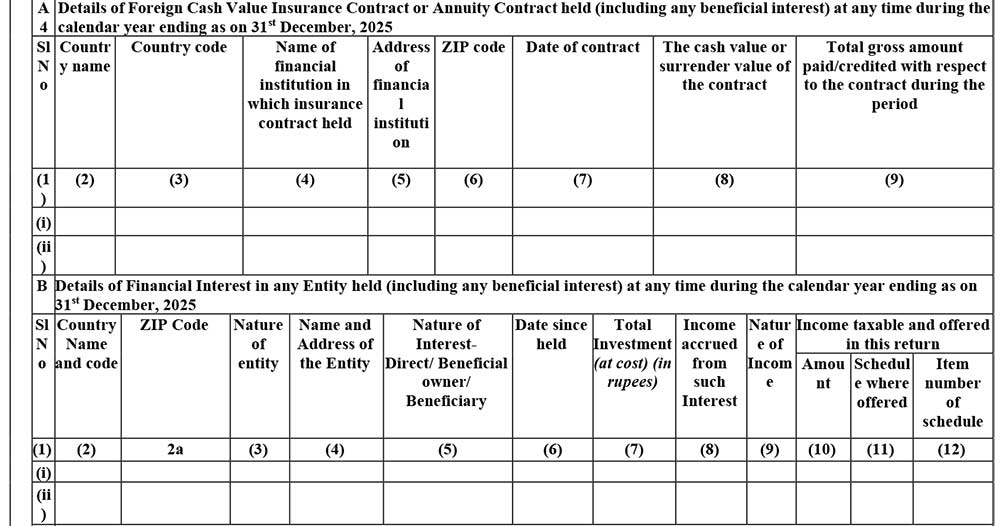

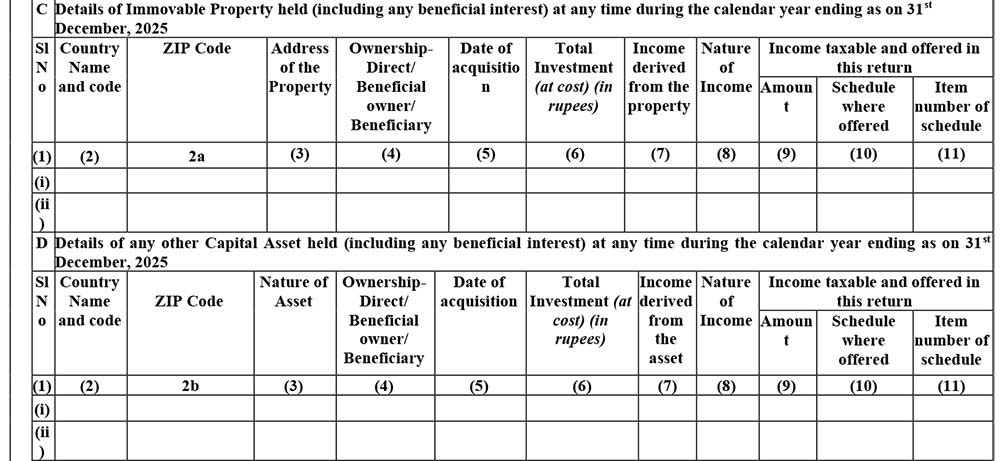

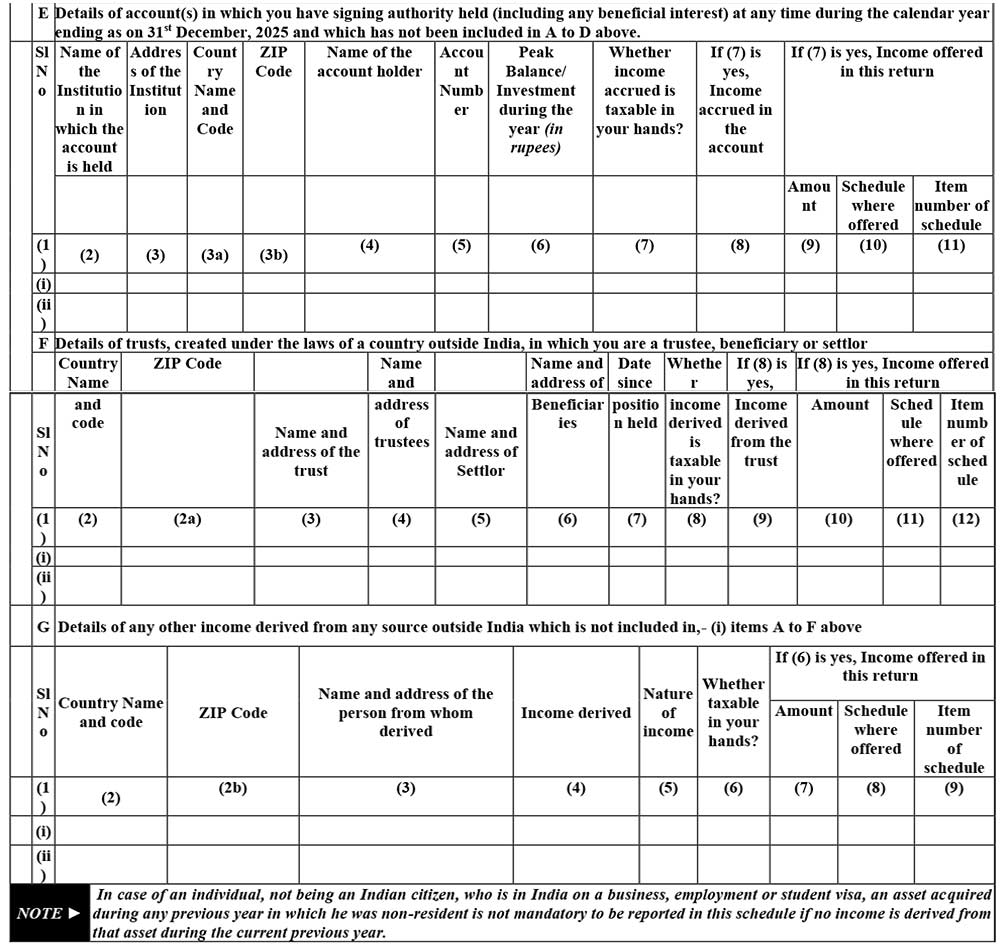

Schedule FA: Details of Foreign Assets and Income from any source outside India

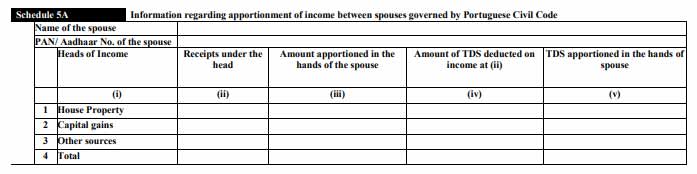

Schedule 5A: Information regarding apportionment of income between spouses governed by Portuguese Civil Code

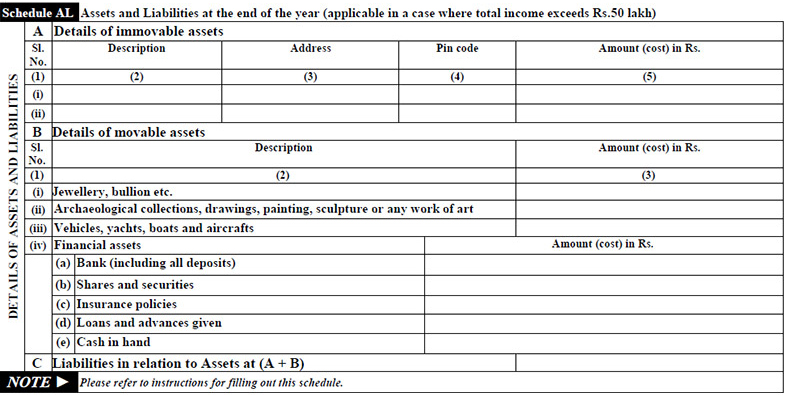

Schedule AL: Assets and Liabilities at the end of the year (applicable in a case where total income exceeds Rs. 1 Crore)

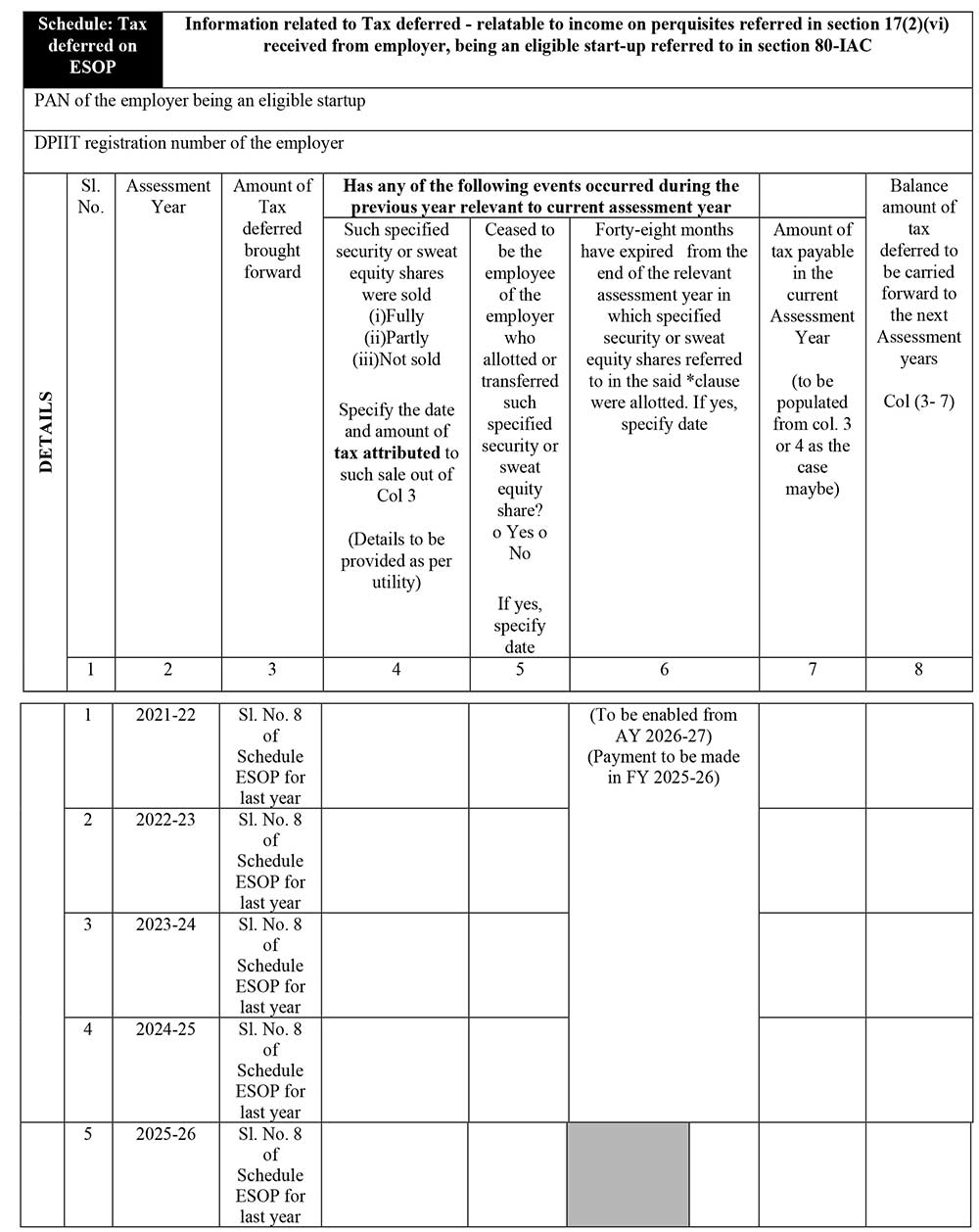

Schedule Tax-deferred on ESOP: Information related to Tax deferred – relatable to income on perquisites referred in section 17(2)(vi) received from employer, being an eligible start-up referred to in section 80-IAC

Part B-TI: Computation of Total Income

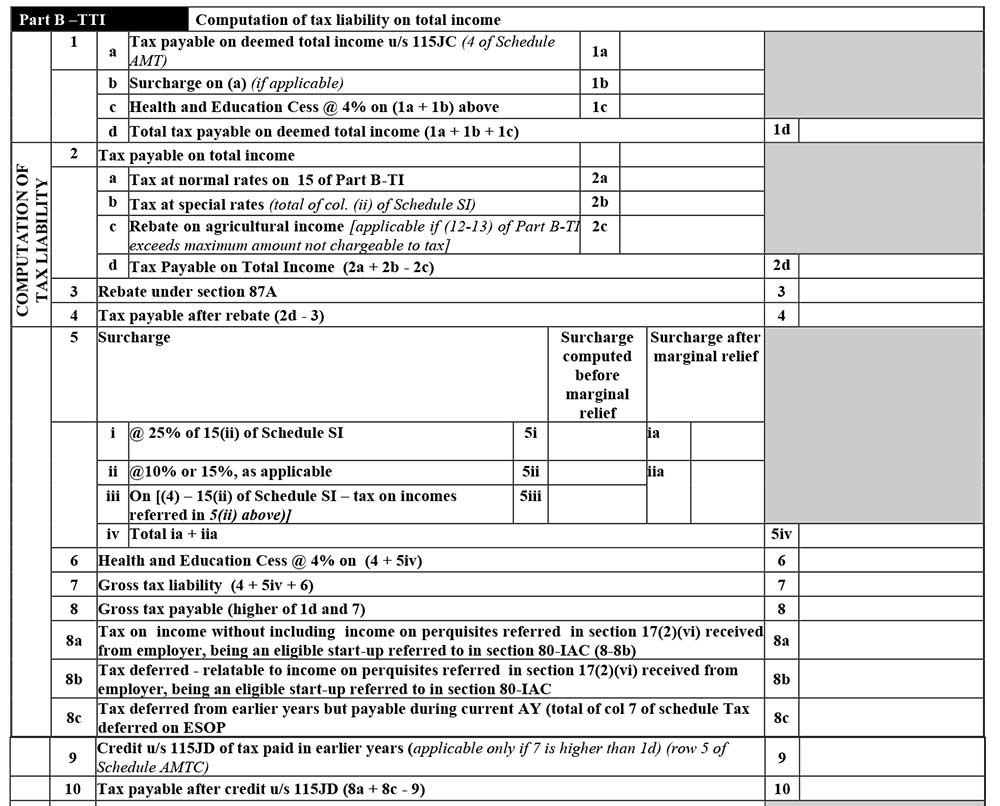

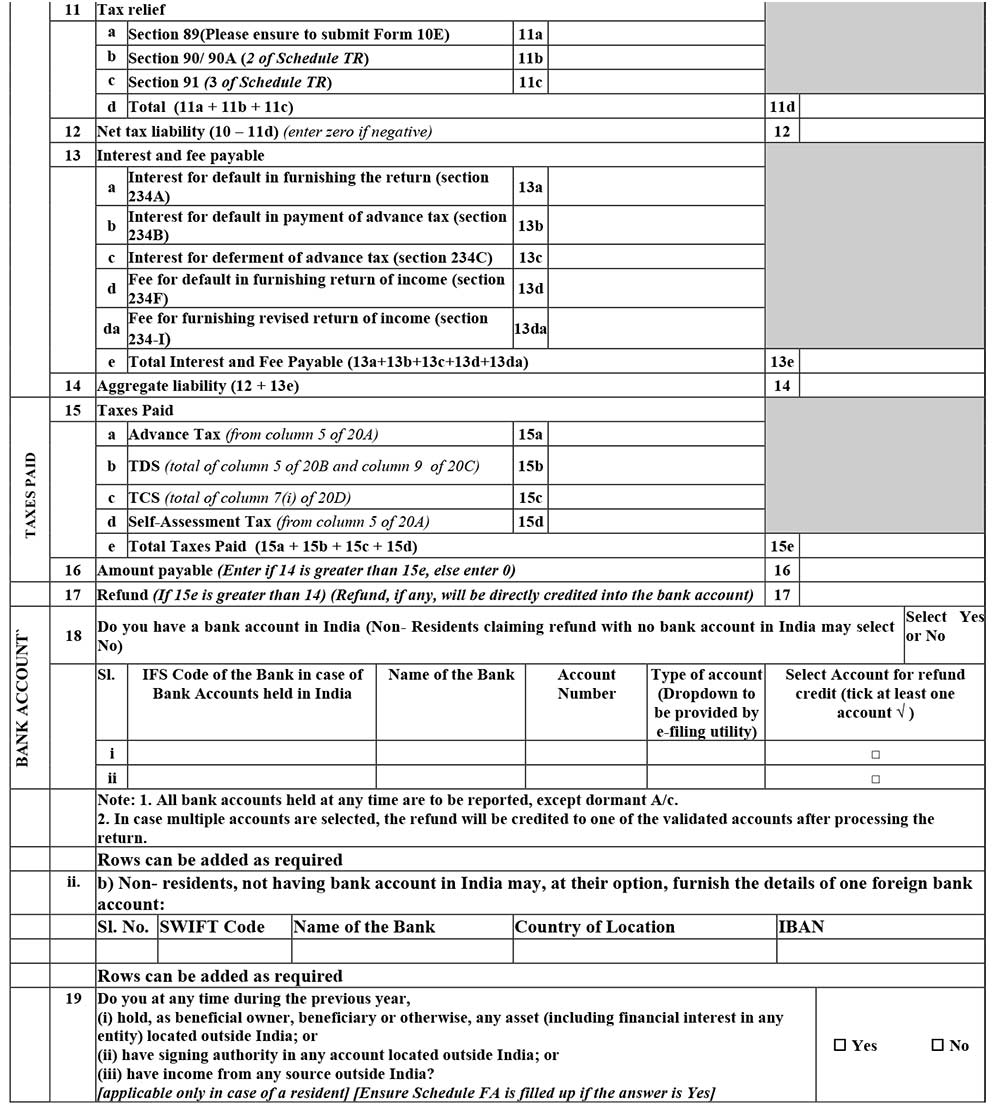

Part B-TTI: Computation of tax liability on total income

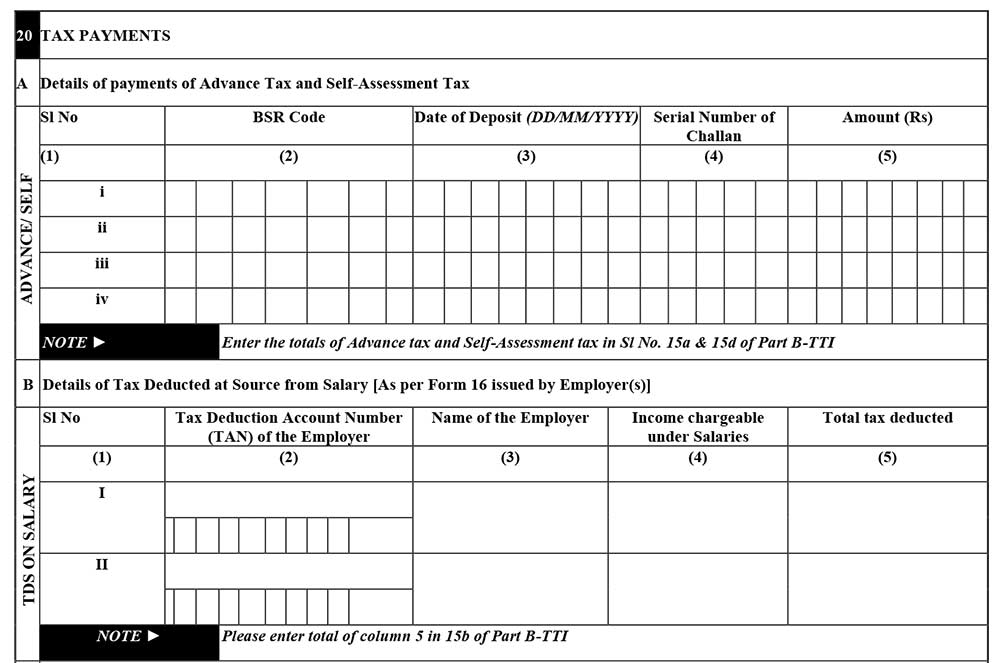

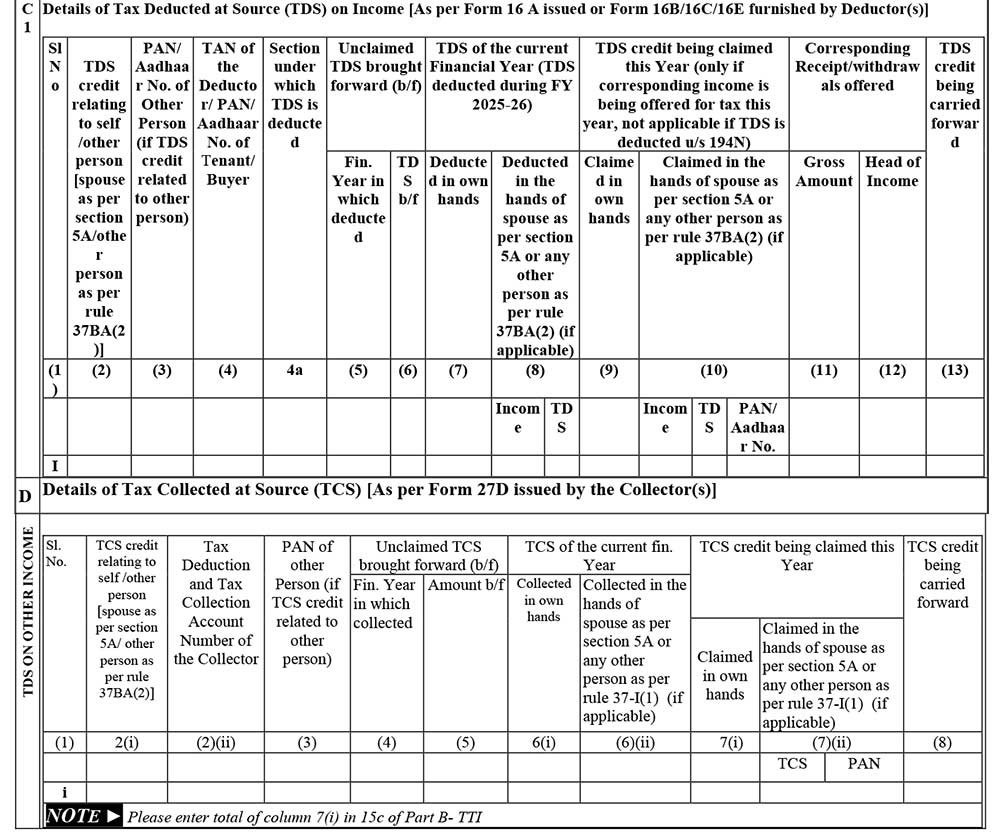

20 Tax Payments

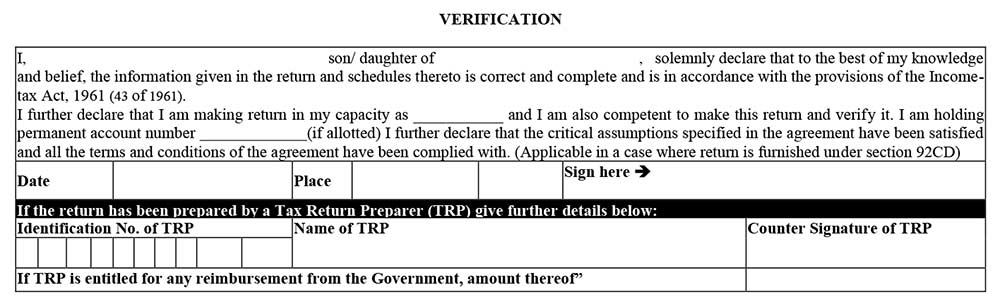

Verification: There will be verification at the end of all the General, Part B TI and Part B TTI, ensuring that the details given are factually correct and self-attested by the taxpayer.

If the return has been prepared by a Tax Return Preparer (TRP), give further details below:

- Identification No. of TRP

- Name of TRP

- Counter Signature of TRP

Income Tax Return 2 Form Filing Mode

An ITR-2 form can be furnished either online or offline. In offline mode, a JSON file (generated via a utility) needs to be uploaded. Alternatively, the user can log in to the portal and select ‘Prepare and submit online’. Data is pre-filled from the AIS, TIS, and Form 26AS. Super senior citizens (80+) may be eligible for paper filing under specific conditions.

Online:

- While furnishing ITR-2 online, feed the details and e-verify the return using EVC via Bank Account/Net Banking/Demat Account/Aadhar OTP or

- 2. Feed the details using an electronic medium and send a physical copy of ITR V to the Centralised Processing Centre (CPC), Bengaluru, through speed post or normal post. When you furnish the ITR-2 return form using an electronic medium, the receipt will be seen in the inbox of the registered email ID. It can also be downloaded from the official income tax website manually. After downloading the acknowledgement, you need to sign the form and then send it to the CPC office, Bangalore, before completing 30 days counting from the e-filing date. On the other hand, it is not required to send the ITR V to the CPC if the EVC/OTP option is used

Offline:

- If the age of the person is 80 or more years during the respective tax period or in the previous year, he/she can opt for offline return filing.

I was an NRI during AY 2020-21 working abroad. Do I have to mention my NR salary income in ITR 2? I am confused about whether my NR salary income is to be mentioned in Schedule EI Exempt income under DTAA. Kindly advise.

If your salary income is taxable outside India then you have to show that income in the salary tab and in the DTAA tab and if it not taxable outside India then it will be shown under the salary tab

Two doubts

1. Schedule 112A – Expenditure wholly in connection with Transfer: Do we have to include both cost of purchase and of Sale or only of sale (Purchase can be stated at total cost). But in the case of Grandfathered cost, if we put the total cost of purchase including brokerage etc, the comparison is made between the exchange-traded price on January 31, 2018, and the actual total purchase cost. Which is the correct model?

2. In the schedule “TDS”, do we have to indicate the details Form 16A – wise or only the consolidated TDS for the year by one Deductor. (earlier we had to enter Form 16A- wise as Form 16A Certificate Number was required to be mentioned – but not now. Can you please clarify.

I have the same doubt regarding……

I too have the doubt number 1 of yours. Did you get any clarification on this? I believe ‘Expenditure wholly in connection with this transfer’ should be both acquisition charges (such as brokerage & STT) and sale charges (Brokerage +STT).

can anyone confirm this?

Expenditure related to transfer means selling expenses. For further clarification please contact to the department.

A pensioner and this year need to file ITR 2 thanks for a small Long Term Capital Gain.The filing process went fine till Calculate tax in TTI where it is struck for validating A8 STCGDTAA which obviously relates to short term capital gain and are told to be MANDATORY fields.No transaction for short term capital gain has been done Asks for Treaty, relevant IT act and all which are not relevant for me. Please anyone guide

IF you have no short term capital gain and it is a mandatory field then fill it as zero.

I have booked one flat jointly with my son. while doing part payment I deducted 1% as TDS (Tax collected and paid in FY2019-20)from the amount to be paid to the builder under 26 QB and deposited with the IT dept immediately. Where and how should I show it in ITR2? This amount reflects in my Form 26AS

You do not have to show this TDS amount in your return as seller will get credit of tds amount not purchaser.

Kindly refer concerned section

Trying to file ITR 2 for AY 21-23. After filling up the form and validation no errors are shown. On clicking proceed to verification getting error as *Col 7, cost of acquisition without indexation should be higher of Col 8 and Col 9″.

This is done automatically by the ITR utility and the values are correct still am getting this error and cannot proceed to verify my returns.

How do I resolve this issue? Any help would be much appreciated.

TIA

I am a salaried person posted and residing in Bangalore. I had a property in Ghaziabad which is rented and rent income is being shown in ITR-1 which I was filing till now.

Last year, I purchased another property in Ghaziabad after arranging 28 lacs as a home loan from the bank. I got the property registered in September 2019 but could not let it out till now because it needs some repairs. Please advise

1. Whether I should file ITR-1 or ITR-2?

2. Whether ITR-2 can be filled in an excel sheet and after converting to XML, whether the same can be uploaded?

3. Should the second property be treated as ‘Deemed let out’?

4. I think interest on loan EMI to be considered as a loss (negative income). Am I right?

5. How the amount paid for buying stamp papers for registration to be treated?

Ans 1. You have to file ITR 2.

Ans 2. You can prepare your return through ITR 2 Excel utility.

Ans 3. Yes, the second property should be treated as Deemed let Out.

Ans 4. Yes, you can take benefit of interest on loan EMI.

Ans 5. You can treat it as transfer Expenses.