The proceedings arose from a complaint filed by homebuyers against M/s Ahmedabad East Infrastructure LLP. The complainants alleged a violation of Section 171 of the CGST Act, claiming that the developer failed to pass on the proportional benefits of Input Tax Credit (ITC) received after the implementation of GST in relation to the “Arvind Uplands I” project.

After finding prima facie evidence, the Standing Committee on Anti-Profiteering directed the Directorate General of Anti-Profiteering (DGAP) to carry out a detailed investigation into the alleged profiteering.

DGAP: Analysed the time span from 01.07.2017 to 31.05.2025 and stated that there was an additional claim of ITC via the respondent in the GST portal.

However, the ratio of ITC was 8.64% before the implementation of GST, which surged to 9.95% after the rollout of GST, therefore giving rise to an increase of 1.31%. The same rise was computed to be Rs. 1,07,78,857 plus GST Rs. 1,293,463, which amounts to Rs. 12,072.

The issue: Is the respondent benefiting from not passing additional Input Tax Credit (ITC) benefits to homebuyers u/s 171, which warrants a refund with interest and penalties?

Decision of Tribunal: The Tribunal upheld the opinion of the DGAP, stating that there was an additional gain in Input Tax Credit (ITC) after the implementation of the GST, which was not passed on to homebuyers. As a result, the offender is responsible for an offence u/s 171 of the CGST Act.

The Appellate Tribunal has ordered the Respondent to repay the total profit of ₹12,072,320, along with interest at a rate of 18% per year, calculated from the date of collecting the profit until the amount is refunded.

Read Also: Delhi (PB) GSTAT Dismisses GST Profiteering Case After ITC Benefit Found to Be Nil

U/s 133(3)(b), the interest of 18% per year is obligatory in nature and comes under the regulatory mandate of passing the benefit on making the supply.

Concerning the penalty, it was stated that section 171(3A) is applicable to the case since the period of breach was after 01.01.2020. Although no penalty was levied on the Respondent, if the profit is deposited in the account of the Government within 30 days from the order date.

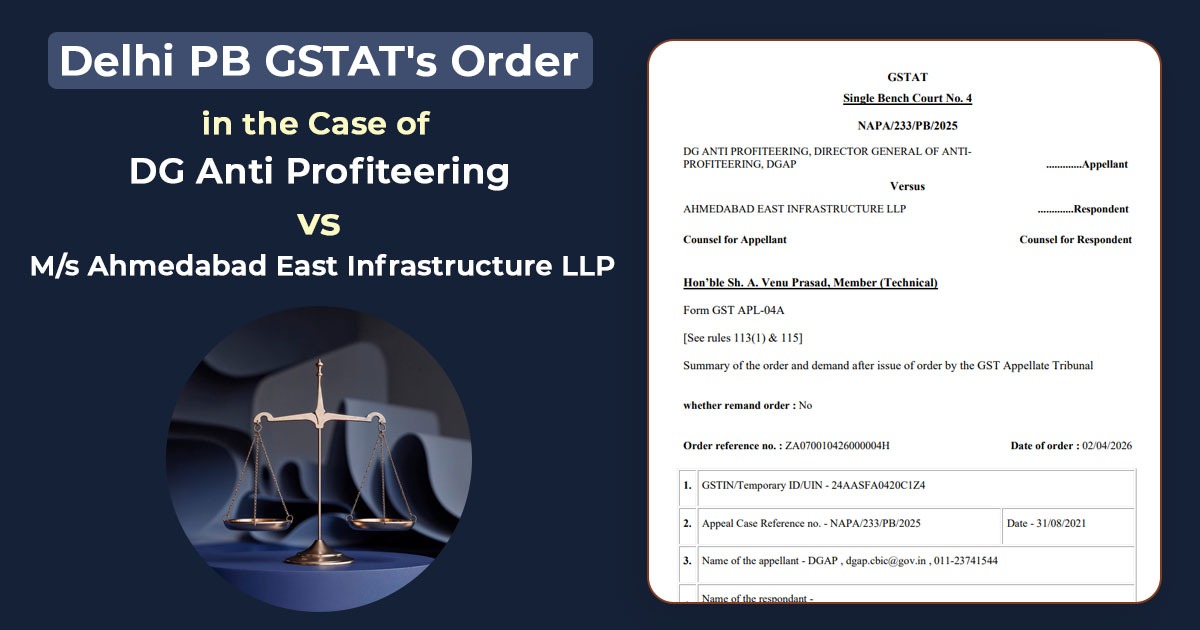

| Case Title | DG Anti Profiteering vs. M/s Ahmedabad East Infrastructure LLP |

| Appeal Case Reference No. | NAPA/233/PB/2025 |

| GSTIN | 24AASFA0420C1Z4 |

| Date | 02.04.2026 |

| Delhi PB GSTAT | Read Order |