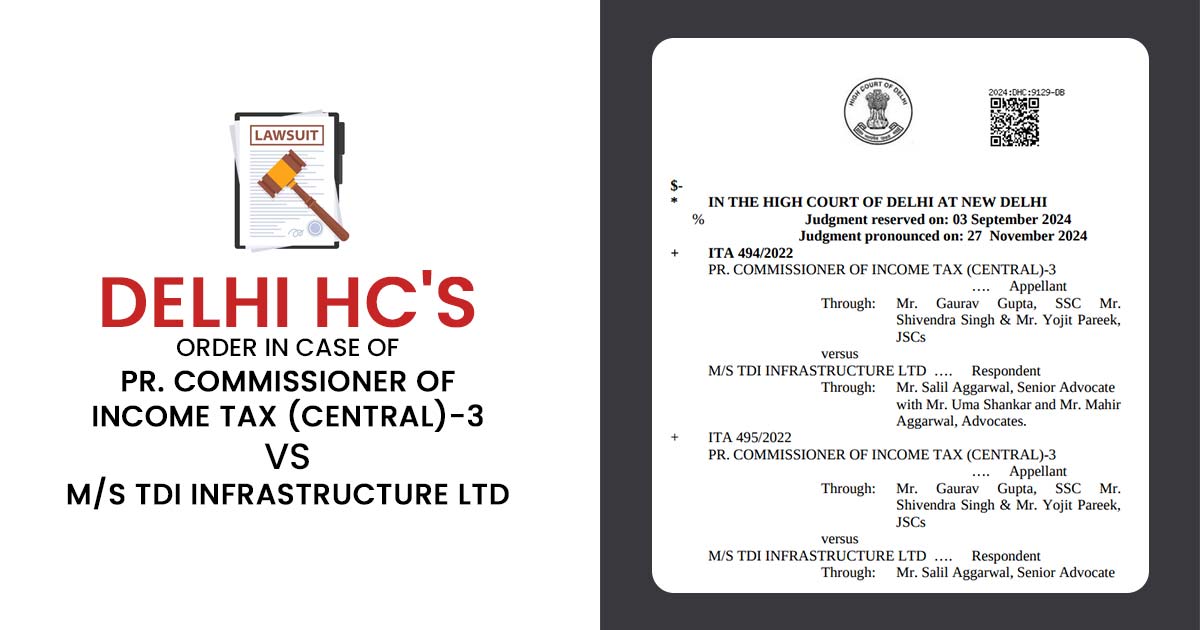

The Delhi High Court has replied in the affirmative to the question that if section 153C of the Income Tax Act, 1961 limits an assessing officer from investigating apart from the considered documents for deriving satisfaction notes for starting assessment/ re-assessment of the ‘other person’.

Section 153C carries a special provision for the assessment of other persons as per the material discovered in the search operations performed u/s 132 on any individual or as a consequence of requisition made under section 132A of the Act.

It provides the authority to the assessing officer of the person investigated to hand over the undisclosed assets records of the other person. If the assessing officer of that other person if satisfied is provided the authority to proceed against these other persons for evading the tax on these undisclosed income.

The proceedings u/s 153C for the case were initiated against the respondent- TDI Infrastructure, under search operations on Taneja-Puri Group.

It is important to mark that the original return for the pertinent assessment year was furnished via the respondent specifying the total income of Rs 46,99,13,140. Though the taxpayer after notice u/s 153C, has incurred other claims of brokerage paid and interest levied through it which was not asserted before.

The Assessing Officer as per the assessment year u/s 153C does not permit the said brokerage and the interest expenses and incurred a specific addition.

ITAT reversed the order based on the additions that were incurred on the grounds of the investigation and the seized documents recorded in the satisfaction note and do not relate to the Respondent. Therefore this appeal.

It was argued by the revenue that the seized documents even when related to or having the information that is of the taxpayer were enough.

Read Also: ITAT Jaipur: IT Section 68 Provisions Do Not Apply to Sale Transactions Already Credited in the P&L

However, it was disagreed by the division bench of Justices Yashwant Varma and Ravinder Dudeja. It mentioned that Pr. CIT v. Dreamcity Buildwell (P) Ltd. (2019) in which the HC carried that the onus was on the revenue to specify that the incriminating material and documents were discovered during the time of search of the taxpayer.

It was carried out that it is not sufficient for the revenue to specify that the documents are either related to the taxpayer or have the data that is of the taxpayer.

Indeed the HC has considered the observations of the ITAT that none of the additions were on the ground of the satisfaction note furnished to start the proceedings u/s 153C.

“None of the additions made in the impugned assessment orders is based on any seized/incriminating material either found during a search or has been recorded in the ‘satisfaction note’ by the Assessing Officer, and therefore, none of these additions can be made in the proceedings u/s. 153C.”

It mentioned that CIT v. Kabul Chawla (2015) where the High Court carried that if there will be no incriminating material discovered in the course of the investigation for the related issue then no addition is to be made concerning these problems in the assessment under Sections 153A and 153C of the Act.

The appeal of the revenue was dismissed as per that.

Appearance: SSC Gaurav Gupta with JSCs Shivendra Singh and Yojit Pareek for Revenue; Senior Advocate Salil Aggarwal with Advocates Uma Shankar and Mahir Aggarwal for Respondent.

| Case Title | PR. Commissioner of Income Tax (Central)-3 vs M/S TDI Infrastructure LTD |

| Citation | ITA 494/2022 |

| Date | 27.11.2024 |

| Counsel For Appellant | Mr. Gaurav Gupta, SSC Mr. Shivendra Singh & Mr. Yojit Pareek, JSCs |

| Counsel For Respondent | Mr. Salil Aggarwal, Senior Advocate with Mr. Uma Shankar and Mr. Mahir Aggarwal, Advocates |

| Delhi High Court | Read Order |