The Supreme Court, without a valid cause, the Goods and Service Tax (GST) refund from the cash ledger cannot be withheld.

The Union of India’s challenge against a Delhi High Court ruling has been dismissed by a bench comprising Justice Sudhanshu Dhulia and Justice Joymalya Bagchi, which quashed the order of the GST authority staying a sanctioned refund of Rs. 5.5 crore to M/s HCC VCCL Joint Venture, marking a critical development in the interpretation of refund rights under the GST regime.

The case has arrived from a refund order on December 9, 2022, which sanctioned Rs. 5.5 crore, including amounts deducted as Tax Deducted at Source (TDS) by Delhi Metro Rail Corporation (DMRC)—in favour of HCC-VCCL JV. As per the provisions u/s 51 of the Central Goods and Services Tax (CGST) Act, these amounts were credited to the Electronic Cash Ledger (ECL) of the applicant.

Thereafter, under Section 108 of the CGST Act, a revisional authority of the GST Department invoked powers and passed an order on July 5, 2023, staying the refund, claiming it was “erroneous and prejudicial to the interest of revenue.” This stay has been extended by a corrigendum from 6 months to 2 years.

While permitting the writ petition (W.P.(C) 10940/2023), the Delhi High Court bench comprising Justice Yashwant Varma and Justice Ravinder Dudeja ruled that the stay order is impacted by legal infirmities.

ECL ≠ ITC: The notion has been rejected by the court that the applicable limitations to the Electronic Credit Ledger (ECL) must be extended automatically to the Electronic Cash Ledger. The kept amounts in ECL are the funds of the taxpayer, other than ITC, and till a quantified demand comes into play, the refund cannot be arbitrarily withheld.

Absence of Adequate Reasoning in Revisional Order: The court discovered that the revisional authority is unable to record any conclusion that specifies the order of refund was incorrect or prejudicial. “Intelligence inputs” specified the order for ITC peculiarities that are not concerned with the cash refund claim.

Section 108 Misuse: The revisional authority has undertaken beyond the extent of Section 108, which requires a finding that the original order was “illegal, improper, or prejudicial to revenue.” Under challenge, the refund order dealt with amounts legitimately standing in the Electronic Cash Ledger, not ITC claims under scrutiny.

Therefore, the stay order has been quashed by the High Court on July 5, 2023, permitting the refund to proceed while allowing the liberty to the GST department to start fresh proceedings as per the law if required.

Supreme Court Dismisses SLP

The Union of India’s Special Leave Petition has been heard by the Apex Court, contesting the Delhi High Court’s ruling.

The Supreme Court does not interfere with the High Court’s decision, remarking, “We see absolutely no reason to interfere with the order of the High Court, in exercise of our jurisdiction under Article 136 of the Constitution of India. However, the question of law, if any, is kept open.”

Read Also: Madras HC: No Interest on GST Due if Paid to Cash Ledger, Even with Late GSTR-3B

The late filing of the SLP has been condoned by the court, though it dismissed the same, bringing closure to the refund-related proceedings in favour of the HCC-VCCL Joint Venture.

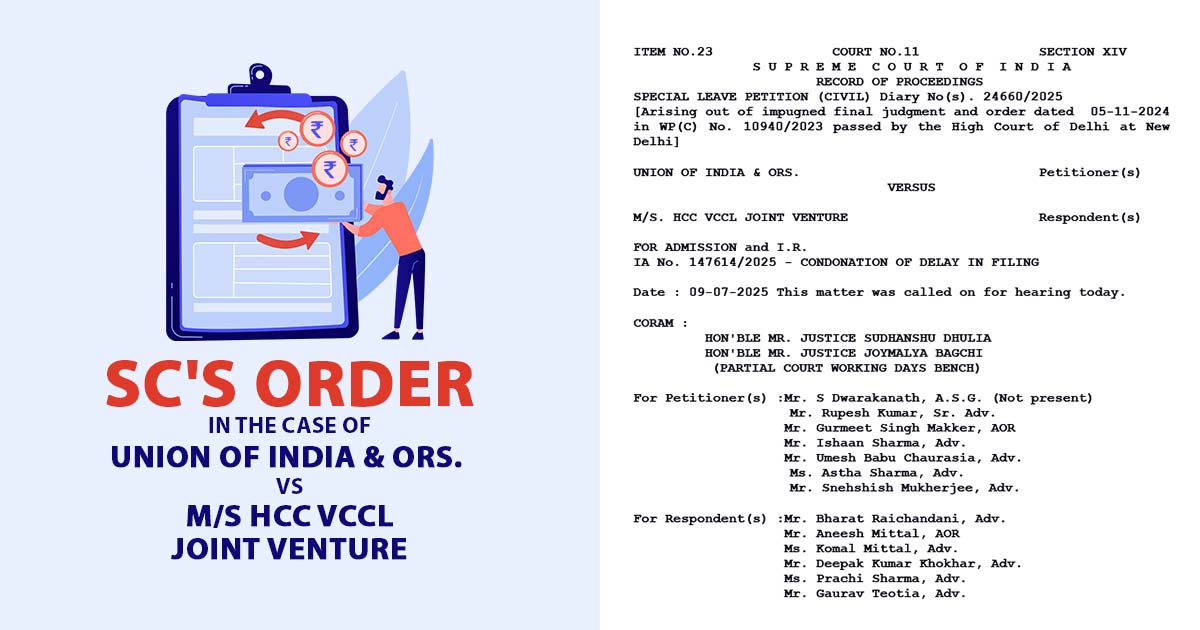

| Case Title | India & Ors. vs. M/s HCC VCCL Joint Venture |

| Case No. | SPECIAL LEAVE PETITION (CIVIL) Diary No(s). 24660/2025 |

| For Petitioner | Mr. S Dwarakanath, Mr. Rupesh Kumar, Mr. Gurmeet Singh Makker, Mr. Ishaan Sharma, Mr. Umesh Babu Chaurasia, Ms. Astha Sharma |

| For Respondent | Mr. Bharat Raichandani, Mr. Aneesh Mittal, Ms. Komal Mittal, Mr. Deepak Kumar Khokhar, Ms. Prachi Sharma, Mr. Gaurav Teotia |

| Supreme Court | Read Order |