The Criterion for filing the MSME I form (MCA) by those specified companies whose outstanding payment to MSME suppliers exceeds 45 days is discussed below:

- Order Named: Specified Companies (Detailed information regarding payment to micro and small enterprise suppliers) Order, 2019

- Date of Notification: In context to the Order dated January 22, 2019, issued under Section 405 of the Companies Act, 2013

- Effective Date: From the Date of Publication in the Official Gazette

Latest Update

- Notification F. No. 16/8/2018/E-P&G/Policy serves as a reminder to submit the half-yearly return for payments exceeding 45 days. Read the Notification

File MSME Form 1 Via Gen ROC Software, Get Demo!

- MSME Form 1

- MSME Form 1 Due Date Half Yearly Return

- Important Definitions

- Micro & Small Enterprise Category

- Late Filing Penalty MSME Form 1

- Procedure for Filing MSME Form 1

- Steps to File MCA MSME Form 1

- FAQs Related to MSME Form 1

What is MSME Form 1 (MCA)?

The MSME I Form is to provide information on a half-yearly basis in the context of the outstanding payments to Micro or Small Enterprises for a period exceeding 45 days with the Registrar of Companies (ROC).

Major changes have been made by the Ministry of Corporate Affairs in the context of protecting the interests of a small group of companies or businesses. He laid emphasis on following compliance by all Specified Companies Whether Public or Private Company, Micro or Small.

Recommended: Due Dates of Filing ROC Annual Return by Companies

A half-yearly return is required to be submitted to the Ministry of Corporate Affairs on a mandatory basis, by all those companies who receive the supply of goods or services from Micro or small enterprises and the payment done to these micro and small enterprises’ suppliers exceeds forty-five days from the date of acceptance (or deemed acceptance) of the relevant good or services.

The following points should be stated in it:

- the amount of payment due and

- the reasons for the delay

Following the provision of section 405 of the Companies Act, 2013, (18 of 2013) the Central Government made it necessary for all the “Specified Companies” to furnish the above-notified information about the payment to micro and small enterprise suppliers.

MSME Form 1 Due Date Half-Yearly Return

In cases where payments are due to MSME more than 45 days after acceptance of services or goods, companies must submit a half-yearly return form. The government has announced the MSME Form 1 due date for the financial year 2025-26 on the official MCA website. Companies are required to file this form twice a year: once for April to September, and once for October to March.

| Period of Return | Filing Period | Due Date | Purpose |

|---|---|---|---|

| 1st half-year | April 2026 to September 2026 | 31st October, 2026 | For all eligible companies |

| 2nd half-year | October 2025 to March 2026 | 30th April, 2026 | Outstanding payments to Micro or Small Enterprises |

Important Definitions:

Specified Companies: As per the provisions of section 9 of the MSME Development Act, 2006, Specified companies are those companies that receive the supply of goods or services from MSMEs, and the payment against these supplies to the suppliers of these MSMEs exceeds 45 days from the date of acceptance (deemed acceptance) of the goods or services

Micro and Small Enterprise: The Micro and Small Enterprise mentioned above means any class or classes of enterprises (including proprietorship, Hindu undivided family, partnership firm, company, undertaking, an association of persons or cooperative society), in which conditions applied as per below:

Pre & Post 01-04-2025

| Category | Investment (₹ Crore) | Turnover (₹ Crore) | ||

|---|---|---|---|---|

| Old | New | Old | New | |

| Micro | 1 Crore | 2.5 Crore | 5 Crore | 10 Crore |

| Small | 10 Crore | 25 Crore | 50 Crore | 100 Crore |

| Medium | 50 Crore | 125 Crore | 250 Crore | 500 Crore |

Note: The Criteria specified above are specified based on the Micro, Small and Medium Enterprises Development Act, 2006.

The MSME Act of 2006 defines Micro Small and Medium Enterprises.

Read Also: All About of MCA E-Form INC-22A with Step-by-Step Filing Process

MSME Act, 2006, MSME Broadly Classified Into 2 Categories

1) In the First category come those Enterprises which are engaged in the manufacturing and production of goods for any industry.

- Manufacturing Enterprises – As per the first schedule to the Industries (Development and Regulation) Act, 1951, Manufacturing enterprises defined in terms of investment in Plant & Machinery, are those enterprises that are engaged in the manufacture or production of goods for any specific industry

2) In the second category come those enterprises that are engaged in providing or rendering services

- Service Enterprises – Defined in terms of investment in equipment, service enterprises are those enterprises that are engaged in providing or rendering services

Under the MSMED Act 2006, the Micro Small & Medium Enterprises (MSMEs) in India are categorised and defined based on capital investment in plant and machinery, but excluding the investments made in land and buildings.

Micro & Small Enterprise Category

In the Micro and Small Enterprise category, there are entities that include Proprietorship, Hindu Undivided Family, Partnership Firm, Company, Undertaking, an Association of Persons, or Co-Operative Society.

Applicability on Companies:

As per a notification issued by the MCA, it has been mandated to file disclosures through Form MSME I for every type of Company – Public or Private Company, Micro or Small Companies. If a company is required to submit this half-yearly report, it must meet the following two conditions:

- The company is classified as a “Specified Company,” meaning it can be either a public or private company

- The company has outstanding payments due to Micro or Small enterprises for more than 45 days from the date of acceptance or deemed acceptance of goods or services

We have outlined simple guidelines for when payments should be made:

- If there is a written agreement, payment should be made within 45 days

- If there is no written agreement, payment should be made within 15 days

Late Filing Penalty for MSME Form 1

Section 405(4), which covers penalties for non-furnishing, incomplete, or incorrect information, prescribes a fine of up to ₹25,000 (minimum), plus ₹1,000 per day, subject to a maximum of ₹3 lakh, by the company & every officer of the company who is in default. Therefore, directors must file MSME Form 1.

Procedure for Filing MSME Form 1 (MCA)

The companies should file the MSME Form I detailing all the outstanding/ dues against the Micro or small enterprises suppliers that exist on the date of notification of the related order within 30 days from the date of deployment of E-form MSME-1 on the MCA Portal.

“Form MSME I (half-yearly return) has to be filed within 30 days from the end of each half-year in respect of outstanding payments to Micro or Small Enterprise, i.e. 30th April 2026 (for October 2025 to March 2026), 31st October 2025 (April 2026 to September 2026)”

- All the Companies falling under the above-mentioned category would be required to file MSME Form I as a half-yearly return by October 31st, for the period from April to September and later by April 30th for the period from October to March and must furnish the following details in it:

1) the amount of payment due and

2) reasons for the delay

- Thus Concludingly, each Specified Company, public or private, that obtains goods and services from the small and micro-enterprises and whose payment is due with such micro and small enterprise suppliers for 45 days from the date of acceptance, shall be required to file the MSME Form as a half-yearly return every year.

Read Also: Free Download ROC Return Filing Software for Companies

Step-by-Step Procedure to File MCA MSME Form 1

Below are the details of the form:

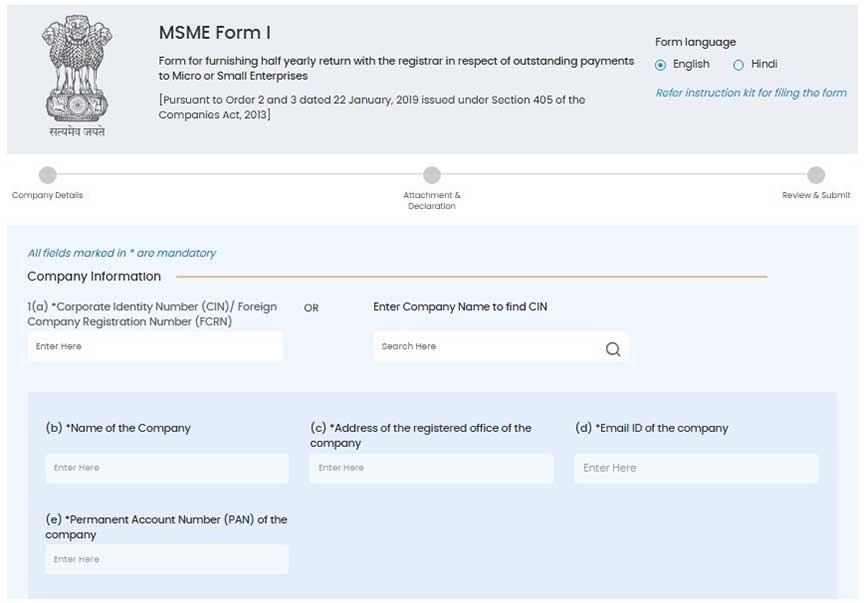

Step 1: Enter the company details such as the corporate identity number, Foreign Company Registration Number (FCRN), and other details such as the name pf the company, address will be auto populated.

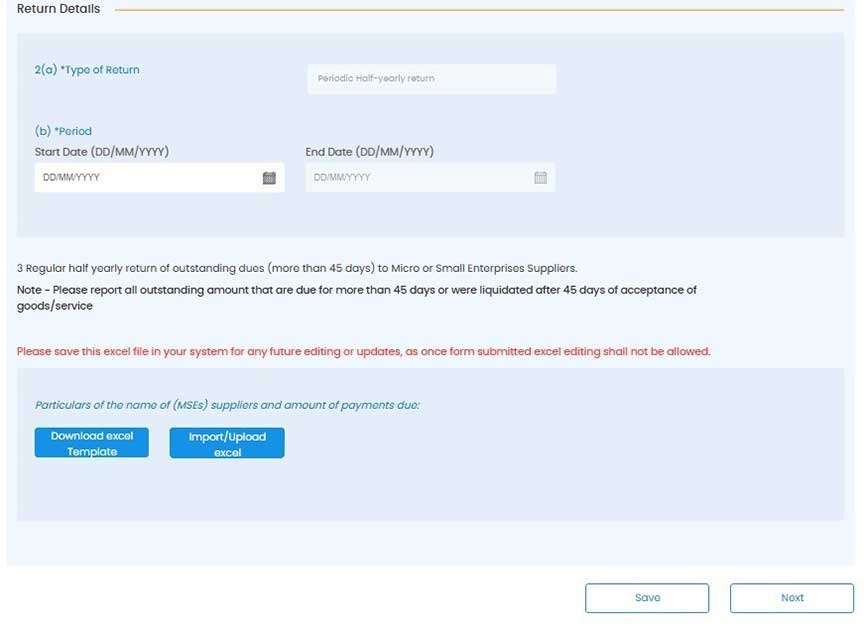

Step 2: Provide the period for which the return is to be filed & after that, download the Excel template & fill in all details, including the names of (MSEs) suppliers and the amount of payments due, save the form and click on the next button.

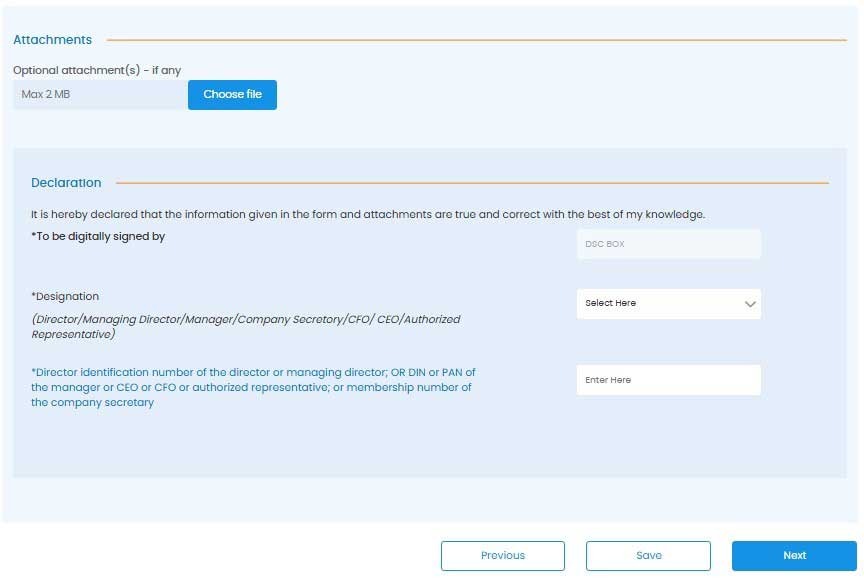

Step 3: Attach the optional document if required. Make a declaration by the company director, affix the digital signature, save the form, and the final step is to submit it.

Who should not file the form? (Exemption to this rule)

- This Rule applies not to all the Companies but only to those Specified Companies whose payment to MSME suppliers exceeds 45 days from the date of acceptance or deemed acceptance of the goods or services as per the provisions under section 9 of the MSME Development Act, 2006.

- If the payment against the supplier exceeds 45 days, the supplier/Creditors give a declaration that they do not fall under the category of Micro or small Enterprises.

Some FAQs Related to MSME Form 1:

Q.1 – Why was the MSME-1 Form introduced by the MCA?

MSME-1 Form has been introduced for companies, who received supplies of goods or services from micro and small enterprises and whose payments for such supplies are outstanding for more than 45 days by the MCA.

Form MSME 1 introduction by MCA will help specified companies submit a half-yearly return to the MCA disclosing details like the amount of payment due, the reasons for the delay, etc.

Q.2 – Who are Micro, Small & Medium Enterprises?

| Category | Investment (₹ Crore) | Turnover (₹ Crore) | ||

|---|---|---|---|---|

| Old | New | Old | New | |

| Micro | 1 Crore | 2.5 Crore | 5 Crore | 10 Crore |

| Small | 10 Crore | 25 Crore | 50 Crore | 100 Crore |

| Medium | 50 Crore | 125 Crore | 250 Crore | 500 Crore |

Q.3 – What details need to be furnished by companies in Form MSME-1?

Companies must furnish the following details to their concerning ROC via Form MSME-1:

- The amount of payment due

- The reasons for the delay

- Supplier Name

- PAN of supplier

- Whether the amount is paid within 45 days, paid after 45 days, outstanding for 45 days or less or outstanding for more than 45 days.

Q.4 – What do you mean by a Specified Company under MSME Form-1?

A specified Company under MSME Form-1 refers to a Public or Private company that:

- Receives goods/services from Micro or Small Enterprises (MSME)

- The payment for such services is still outstanding from the company side for more than 45 days

Q.5 – What are the steps to file the initial return, i.e., MSME Form I by specified company?

- In the first step, the specified company must rectify its suppliers whose payments are due for more than 45 days as on 22nd January 2019

- Now, the company must obtain a Micro or Small Enterprises Registration Certificate from the same suppliers rectified in step 1

- Finally, the company must settle all dues pending for more than 45 days with suppliers registered under MSME Act 2016 in order to avoid filing MSME Form I

Q.6 – What is the initial return date of Form MSME-1?

Based on the MCA general circular dated 21.02.2019, the initial return filing of MSME Form 1 must be done within 30 days, starting from the date of said e-form deployment on the MCA 21 portal.

Q.7 – What is the due date of regular half-yearly return of MSME Form I:

List of documents needed adjacent to form MGT 7:

MSME Form I is filed on a half-yearly basis, the due date for which is given below:

| Time Period | Half-year return date of MSME Form I |

|---|---|

| October to March | 30th April |

| April to September | 31st October |

Q.8 – What is the Penalty Fees against the non-filing of Form MSME-1?

| Entities | Penalty Fees |

|---|---|

| For Specified Companies | INR 25000 |

| Defaulting Officer (related to company) | A penalty of INR 25000 to INR 3 lakh |

Any attachment is required in MSME Form

No specified document is compulsorily required, attachment option is optional.

The article is good and informative except nothing was mentioned regarding government fee to filing this MSME Form 1. Could you please provide the Govt. fee/charge to filing MSME Form1.

Neither fee or late fee prescribed for filing of MSME-1 by MCA Department. But the provision of Section 405 of Companies Act 2013 shall be applicable on failure to file MSME-1: –

Fine: On Company: Up to INR 25,000.

On officer who is in default: (1) Fine: Between rupees 25000 to 300000, OR (2) Imprisonment up to 6 Months OR, (3) Both

If the supplier is registered under MSME but he traded the goods by procuring form market and payment is done after 45 days. Will, it required to report in Return? Please reply.

Dear Madam,

if a company fails to file the return on the due date. what will be the late fee or penalties imposed by MCA or MSME authorities?

Under Companies Act 2013

Non-compliance will attract the following Punishment and Penalty under Section 405(4) of the Companies Act:

Fine: On Company: Up to INR 25,000.

On officer who is in default: (1) Fine: Between rupees 25000 to 300000, OR (2) Imprisonment up to 6 Months OR, (3) Both

Penal Interest on Delayed Payment to MSME Enterprise

The penal interest chargeable for delayed payment to an MSME enterprise is three times of the bank rate notified by the Reserve Bank of India.

1. The invoice date is 01.04.18 invoice acceptance date is also 01.04.18 but we have paid the same on dt-30.06.18 which is after 45 days. Should we show the same in the initial and regular return?

2. can we rectify the MSME return & how?

Any payment to MSME registered suppliers outstanding on 22nd January 2019 need to be reported in MSME form. No provision for rectification provided.

I HAVE AROUND 350 CREDITORS,, OUT OF WHICH 160 CREDITORS ARE MORE THAN 45 DAYS OLD. BUT WE DO NOT HAVE ANY DETAILS REGARDING THEIR STATUS I.E WHETHER MSME REGISTERED OR NOT??

CAN WE ASSUME THAT ALL OF THEM ARE NOT MSME REGISTERED? WHAT SHOULD BE DONE?

If the suppliers of goods and services are MSME registered and to whom payment is delayed for more than 45 days on the notification date i.e. 22nd January 2019 than Form MSME – 1 is mandatory to file with a reason of delay.

Contact your creditors to know whether they are MSME registered or not.