It was carried by the Madhya Pradesh High Court (HC) that an order passed u/s 148A(d) of the Income Tax Act 1961 is not an appealable order hence the mere remedy with an aggrieved party is to invoke the writ jurisdiction of the HC.

The proceedings under section 148A are initiated when the income tax officers speculate that an assessee may have the concealed income via any assessment year.

The concern of section 148(1) (b) is towards the issue of the show cause to furnish a chance of hearing to the taxpayer. Sub-section (1)(d) provides the authority to the assessing officer to decide whether the reassessment notice u/s 148 must be provided to the taxpayer.

Therefore an order passed u/s 148(1)(d) is not a final judgment of income escapement.

A division bench of Justices Vivek Rusia and Binod Kumar Dwivedi in this scheme noted,

“Admittedly, the order passed under Section 148A(d) of the Income Tax Act is not an appealable order, therefore, except writ petition the petitioner has no other alternative efficacious remedy.”

The applicant was dissatisfied with the order passed against him under section 148A(d) and significant show-cause notice u/s 148.

According to the factual matrix of the matter, the applicant was served with a SCN u/s 148A(b) dated 24.03.2024. Before AO he appeared dated 31.03.2024 and asked for the adjournment to submit a detailed response.

The AO “wrongly observed” that the petitioner had submitted a response on 31.03.2024, HC observed.

The applicant submitted a response dated 05.04.2024 and on the same date, the competent authority passed the order u/s 148A(d) and re-assessment notice under Section 148.

Read Also: Provision for Re-assessment Under Section 147 of I-T Act

The court marked that the applicant was not furnished a chance of hearing to defend himself.

It stated “Once the statute provides an opportunity of hearing before initiation of proceedings under Section 148 of the Act, then effective opportunity of hearing should be provided to the assessee. It is not the case where the time to pass the final order was going to expire and the order was liable to be passed on 05.04.2024. As per Section 148A(b) of the Income Tax Act, a minimum of 7 days and a maximum of 30 days is liable to be given as an opportunity of hearing to the notice. In the present case, the impugned order has been passed before the expiry of 30 days from the date of issuance of show cause notice, therefore, the order is unsustainable in the eyes of the law,”

As per that the court remitted the case back to the AO to determine the Show Cause Notices (SCN) furnished u/s 148(b) afresh post providing a chance of hearing to the applicant.

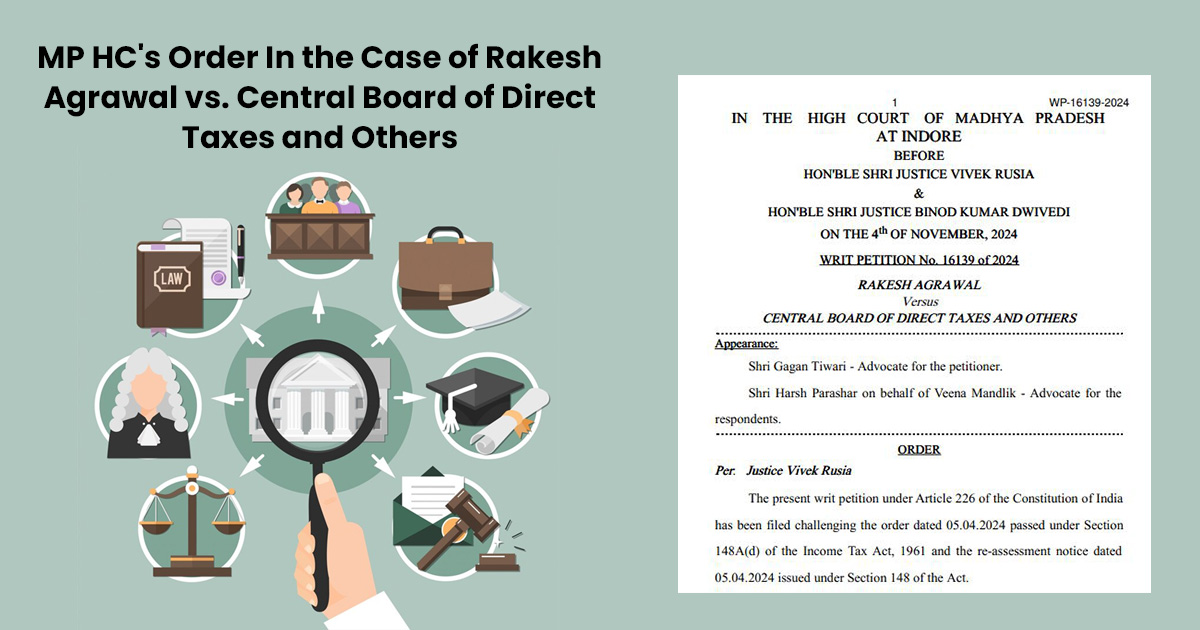

| Case Title | Rakesh Agrawal vs. Central Board of Direct Taxes and Others |

| Citation | Writ Petition No. 16139 of 2024 |

| Date | 04.11.2024 |

| For Petitioner | Shri Gagan Tiwari |

| For Respondents | Shri Harsh Parashar on behalf of Veena Mandlik |

| Madhya Pradesh High Court | Read Order |