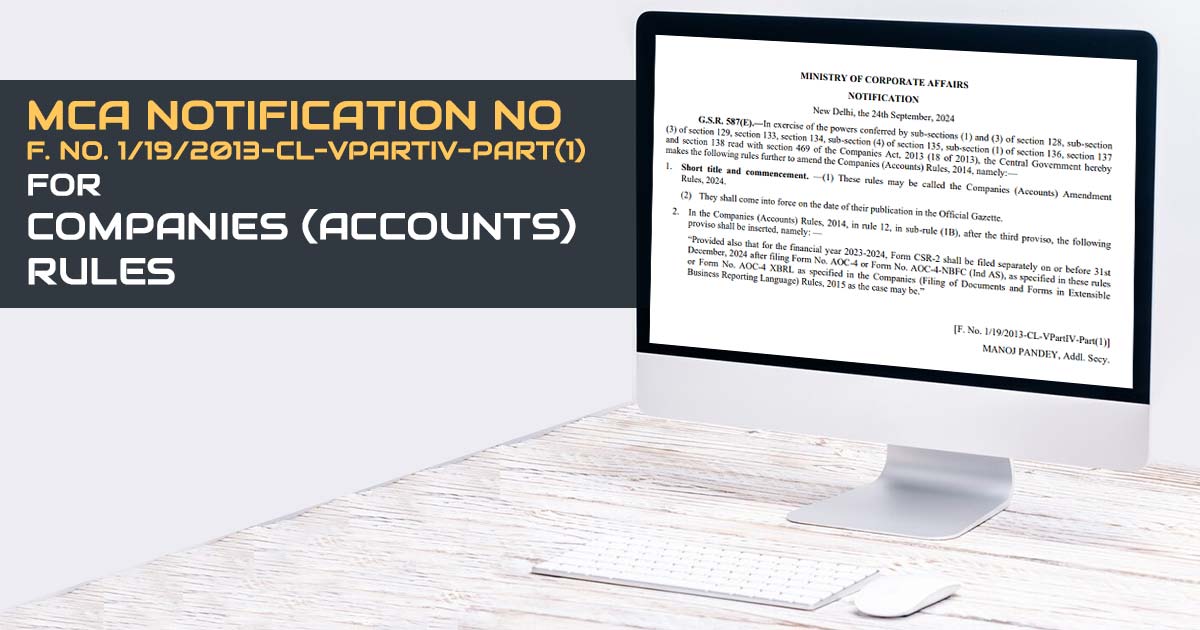

The Companies (Accounts) Rules, 2014 has been revised by the Ministry of Corporate Affairs (MCA) via the Companies (Accounts) Amendment Rules, 2024. Such revisions obligate that for the FY 2023-2024, Form CSR-2 is to be filed separately by companies on or before December 31, 2024.

The filing of Form CSR-2 is to pursue the submission of either Form AOC-4 or AOC-4-NBFC (Ind AS), as applicable under the respective rules, or Form AOC-4 XBRL following the Companies (Filing of Documents and Forms in Extensible Business Reporting Language) Rules, 2015.

Under diverse sections of the Companies Act, 2013, including sections 128, 129, 133, 134, 135, 136, 137, and 138, the reported revision assists the filing procedure for CSR reporting for the companies.

It mandates the companies to finish their financial statement submissions via the AOC-4 Form or its variants before moving to a separate filing of Form CSR-2, which consolidates Corporate Social Responsibility (CSR) data.

As per the notification, the CSR-2 would get filed separately post-filing of AOC-4 or AOC-4-NBFC (Ind AS) by a due date of December 31, 2024. Section 135 of the Companies Act, 2013 obligates specific companies to contribute to the public.

Companies that attain particular financial limits need to form a CSR committee and be involved in CSR activities. The criteria for enforcing CSR compliance include businesses with a net worth exceeding ₹500 crore, an annual turnover surpassing ₹1,000 crore, or a net profit greater than ₹5 crore.

Read Also: Annual Form AOC-4 Filing Via Gen Complaw with XBRL Software

These companies should provide a part of their profits for the CSR initiatives that contribute to social, economic, and environmental development. The CSR committee formation assures an effective oversight and execution of such activities.