In this article, we will learn and understand the complete process of the GST Input Tax Credit (ITC) reversal if in case the clients and the concerned parties miss the payments for more than 180 days or so. The post will take the sections and other major amendments in the provisions of the sub-sections. There is a complete table explaining the proviso and other changes explained apart with major effects on the applicability:

Fill Form for GST Compliance Software

Latest Update

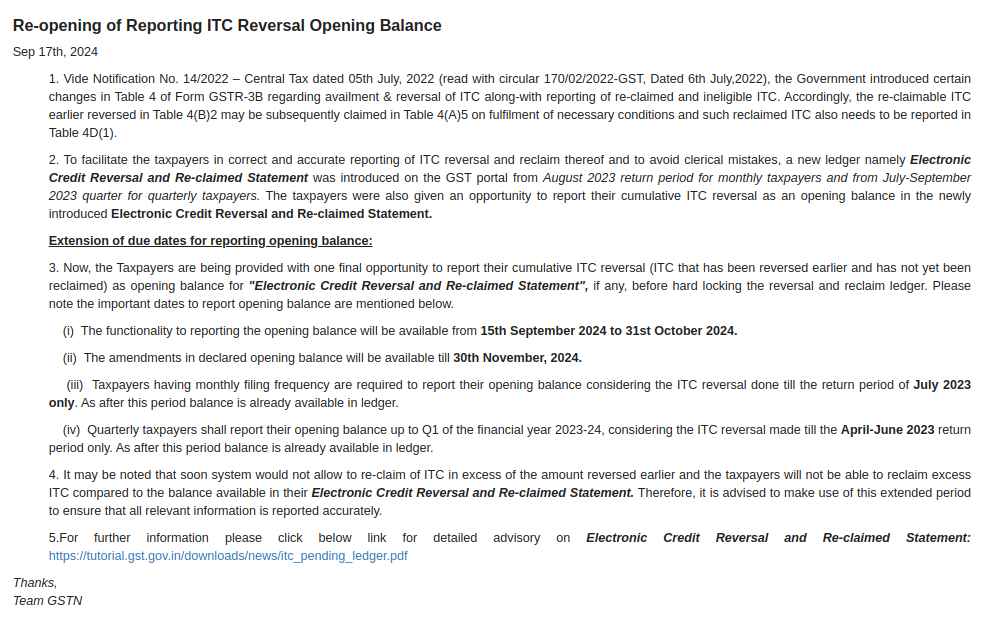

- GSTN department has issued a new advisory to extend the due date for re-opening claims for ITC reversal. View more Read PDF

- The Kerala GST official department has published guidance for SOP scanning ineligible IGST input tax credit reversals made by taxpayers on their GSTR 3B return form. Read more

GST ITC Reversal as Per Rule 37

After the start of GST, the businesses would have been facing issues following the provisions asking for the GST input tax credit (ITC) reversal including interest on the failure to file the taxes including the tax amount to the vendor in 180 days from the date of the issuing of the invoice. The major burden is from the compliance and the way where the related provision would have been worded directing to various irregularities.

Currently, the provisions mentioned in ITC reversal Rule 37 (concerned with the way to influence the reversal and re-availment) shall be substantially revised and have been carried into effect from the date 01.10.2022. The same article is concerned with analyzing the provided provisions and the problems related to them.

Legal Provisions Under Section 16(2) of GST ITC

Sec. 16(2) of the CGST Act, 2017 initiates with the non-obstante clause overriding anything held in the said Sec. 16 which furnishes that no enrolled individual shall be qualified to any ITC unless the prescribed conditions are defined. The specified conditions are concerned with the possession of valid documents filing the information of the mentioned documents via vendor the actual receipt of the goods or services or both, the tax payment to the government, and return filing under GST. The 2nd and the 3rd proviso to the articulated Sec. 16(2) additionally furnish as under:

“Provided further that where a recipient fails to pay to the supplier of goods or services or both, other than the supplies on which tax is payable on a reverse charge basis, the amount towards the value of supply along with tax payable thereon within a period of one hundred and eighty days from the date of issue of invoice by the supplier, an amount equal to the input tax credit availed by the recipient shall be added to his output tax liability, along with interest thereon, in such manner as may be prescribed:

Provided also that the recipient shall be entitled to avail of the credit of input tax on payment made by him of the amount towards the value of supply of goods or services or both along with tax payable thereon.”

GST Input Tax Credit Time Limit

The mentioned second proviso, hence asked to furnish that the amount identical to the ITC claimed via the recipient would get added to his output tax liability including the interest on it in this way as might be specified in which the provided recipient is not able to pay to the supplier i.e the amount for the supply value including the tax applicable on it in the duration of 180 days from the issuance date of the invoice.

The third proviso furnished that the recipient will get qualified to claim the credit ( which gets summed to the output tax of the second proviso) on the incurred payment that he has performed of the amount for the supply value including the tax subjected to get paid on it.

GST ITC Rule 37 Under CGST Act 2017

5. Rule 37 of the CGST Rules, 2017 comprises the process to prove the mentioned provisions. Effected from the date 01.10.2022 vide Notification No. 19/2022-Central Tax on 28.09.2022 the stated Rule 37 has been revised. Below mentioned is the comparison table which described the revisions effectively.

| Sub-rule | Old Till 30th September 2022 | New Amendment from 1st October 2022 |

|---|---|---|

| 1. | An enrolled individual who claimed the ITC on any inward supply of goods or services or both, though unable to pay the supplier, after that these supply including the tax liability to get paid on it in the mentioned duration in the second proviso to sub-section (2) of section 16, will file the information of these supply, the amount unpaid align with the ITC claimed of the proportionate to the amount not filed to the supplier in FORM GSTR-2 for the month just after the 180-day period from the date of the issuance of the invoice: Given that the supply value incurred with no acknowledgement cited in Schedule I of the said Act shall be treated to have been paid for the second proviso to sub-section (2) of section 16: Provided that the supply on any amount summed as per the provisions of clause (b) of sub-section (2) of section 15 would be treated to be paid for the proviso to sub-section (2) of section 16. | An enrolled individual who claimed for ITC on any inwards supply of goods or services or both excluding the supplies on which the tax would subject to be paid on the reverse charge basis, though unable to pay to the supplier after which, the amount for the supply value including the tax subjected to be paid on it in the mentioned time in the second proviso to sub-section(2) of section 16, will pay the amount identical to the claimed ITC for the same supply including the interest subjected to be paid on it under section 50 and filing return in FORM GSTR-3B for the tax duration following the duration of 180 days from the issuance date: Provided that the supply value incurred with no acknowledgement cited in Schedule I of the said Act shall be treated to have been paid for the second proviso to sub-section (2) of section 16: Furnished that the supply on any amount summed as per the provisions of clause (b) of sub-section (2) of section 15 would be treated to be paid for the proviso to sub-section (2) of section 16. |

| 2. | The ITC amount referred to in sub-rule (1) would sum to the output tax liability of the enrolled person for the month where information has been provided. | The registered individual afterwards performed the payment of the amount for the value of such supply including the tax subjected to be paid on it to the supplier after that, he is qualified to again claim the ITC directed in sub-rule (1) |

| 3. | An enrolled individual is obligated to pay interest at the rate specified under sub-section (1) of section 50 for the duration initiating from the credit claim date on these supplies till the date when the amount summed to the output tax liability, as noted in sub-rule (2), is paid. | Omitted |

| 4. | The mentioned time limit in sub-section (4) of section 16, not applies to a claim for re-availing of any credit, as per the provisions of the Act or the provisions of this Chapter, which already being reversed in the former times. | No revision |

Explaining the problems that come in the context of the mentioned provisions-

Applicability of the Proviso(s) to GST Section 16(2)

A proviso would direct an exception to the main provision. Therefore the same would be unavoidable that the major provision should get concerned with the subject matter i.e worked with the proviso. 16(2) comprises various conditions which would be needed to meet for the enrolled individual to be a qualified ITC. There are no conditions given that the enrolled individual should pay the supplier in the 180 days duration. Therefore the questioned proviso(s) occur is incompatible with the scheme of Sec. 16(2). Hence the validity of the same proviso(s) is needed to be tested.

An individual is indeed required to acknowledge if the validity of the related proviso(s) could be sustained by recognizing the same as an independent provision and not as a proviso to any major provision. It is an obligation for a person to comply with section 16(2) which is concerned with the conditions relevant to the credit entitlement and not for the reversal of the credit after entitlement. Thus when the appropriate proviso(s) would be acknowledged to be independent even if the identical occurs to be incongruent within section 16(2) itself and hence on the same basis the validity would be needed to get tested.

One might acknowledge for the related provision(s) would remain applicable if the same would be stated that the tax (towards which the credit would get claimed) has actually been furnished to the government via a vendor. The same would be due to the purpose of the actual payment condition u/s 16(2)(c) permits the credit exclusively when the government obtains the amount. Thus when the specified purpose would get satisfied, then is there any chance of an issue for refusing the credit on the failure of the enrolled person for paying the vendor within a 180-day duration? In the same situation, the purpose of still refusing the credit does not have any reason. Hence on the above foundation, the validity should get tested.

Investigating the enrolled person is the purpose of the related proviso(s) to forward the payment of tax by not suffering from any load as per cash flows. But the purpose would get defeated via the fact that the related proviso(s) would furnish the time of 180 days to attain the investigation particular. Thus on the same basis, the purpose to refuse the credit laid on the 180 days of the test resembles to be arbitrary. Hence on the same basis, there is a need to test the validity.

Taxpayer Fails to Pay Within 180 Days

The related proviso(s) would be applied for the failure of the enrolled individual to pay the vendor within 180 days duration from the invoice date. Failure does not being described in the act. The normal meaning of the mentioned term failure resembles neglect of the anticipated or needed action. Therefore it should be an expected action for the recipient and supplier to remit dues within the 180-day duration after that it could be asked to call the anger of the subject proviso(s).

The specified issue is assisted by the ostensible purpose behind the conceptualization of the subject proviso(s). The articulated purpose mentioned above would be to facilitate the vendor’s agreement to allow the recipient to remit the dues post 180 days duration the same could be stated in the absence of any grudge of the vendor, could there be a grudge to ask for the credit reversal in these situations? The mentioned propositions would be applicable to the context of retention payments, and others.

Validity Revised Under GST Rule 37(2)

The proviso(s) furnished that on the pay failure within 180 days, the identical amount to the ITC would get summed to the output tax liability including the interest on it, in the same way as specified. Therefore the law empowers the executive to conceptualize the rule in the mentioned way where the amount in question would sum to the output tax liability including the interest on it.

Thus the law does not empower the Executive to conceptualize the Rule overruling the factor which deals with the addition of the amount as ‘output tax liability. Rule 37(1) as changed read with the modified form GSTR 3B along with Circular No.170/02/2022-GST dt. 06.07.2022 shows that the credit in question is needed to be reversed from the available credit in the related tax period. Therefore the ITC revised rule 37(1) resembles to be in conflict with the proviso(s) since the same does not mention the addition of the amount as the output tax liability however it furnishes for the reversal of the amount via available credit.

GST Rule 37 Validity Before 1st October 2022

Rule 37(1) r/w 37(2) as in existence before 1.10.2022 allotted to file the information of the failure in furnishing the payment within 180 days in GSTR 2 and the specified amount was to be sum to the output tax liability in the mentioned duration.

Therefore the mentioned rule on the side furnished for the addition of the amount of the output tax liability however the same was to be performed merely post the assessee filed the information in GSTR 2. It comes into force from 1.10.2022 that the amount in question is needed to get reversed in GSTR 3B under the revised rule 37.

Filing the GSTR 2 would be abandoned. It needs to recognize if the need to sum the amount to the output tax liability before 1.10.2022 could affect in absence of any process to file the information via GSTR 2. The stated rule 37 validity before 1.10.2022 would be questioned again provided the recent revision which is prospective in nature.

Partial GST Payment within 180 Days

Rule 37(1) as in existence before the date 01.10.2022 specified that only the amount proportionate to the invoice value which does not pay after 180 days period is needed to be summed. The revised Rule 37(1) clearly misses the word ‘proportionate’. Despite the subject proviso(s) u/s 16(2) omits the word ‘proportionate’. Thus the same could mean, the whole credit needed to be reversed even when a proportionate amount is not paid at the finish of 180 days. Thus a credit is obligated to be reversed.

Interest Liability Under GST Rules 50 & 37

Rule 37 as in existence before the date 01.10.2022 given that the interest on the amount that would be summed to the output tax liability will be revealed u/s 50(1) of the CGST Act, 2017 for the duration starting from the date of credit claim till the date, the amount summed to the output tax liability. The ITC revised rule 37 came into force on the date 1.10.2022 misses the whole reference to Sec. 50(1) furnishes that the interest payable u/s 50 files the return in form GSTR-3B. Since the discussion was performed, the revised rule 37 furnishes for the reversal of the credit rather than the addition of the amount to the output tax liability.

Thus interest u/s 50(1) (applies in the concern of a failure to file the tax) couldn’t be applicable which comes into force 01.10.2022. If the interest could be levied u/s 50(3)? Now Sec. 50(3) will be subjected to which the ITC has claimed bogusly and is being used. The credit entitlement during the receipt of the inward supplies (even when there would be a next failure to file in 180 days) does not get disputed.

The same would be done when the next failure occurs and the need for reversal comes. Therefore the same could argue that the provided case would not be where the assessee has claimed bogusly and used the credit. Moreover the revised rule 37 unlike the before version unable to furnish the duration for which the interest is needed to get computed. Thus the revised Rule 37 asking to levy the interest u/s 50 seems not to be consistent with the main provisions.

A person should acknowledge that under Sec. 50(3) r/w Rule 88B the interest will not be levied when the related amount of the credit has been claimed though it does not be used during the reversal.

Reversal Duration

The revised Rule 37 furnishes, the assessee is obligated to pay the amount during filing the return in Form GSTR-3B for the tax duration following the duration of 180 days from the issuance invoice date. Thus when the duration of 180 days shall get lapsed (in Oct 2022), the needed amount to get paid via filing the information in GSTR 3B of September 2022 (the tax duration just following). Does this render, the assessee would be burdened with the other interest for the duration of one month more? The same might be acknowledged that the assessee in freedom to undertake the reversal prior to the occurrence failure date. Therefore to that stretch, the interest must not be levied.

Closure

The mentioned investigation shows, there are various issues upheld in effectuating the provisions needing the credit reversal failure to incur the payment under 180 days. It would be effective if the mentioned above issues shall get resolved in the forthcoming time.

{kind=link}

Sir- if the unpaid ITC is not utilised since other paid itc and rcm were available adequately to discharge output tax in each month –whether reversal of itc for unpaid amount beyond 180 days will it attract interest on unutilised itc or will it not attract interest since itc was not utilised sir ?