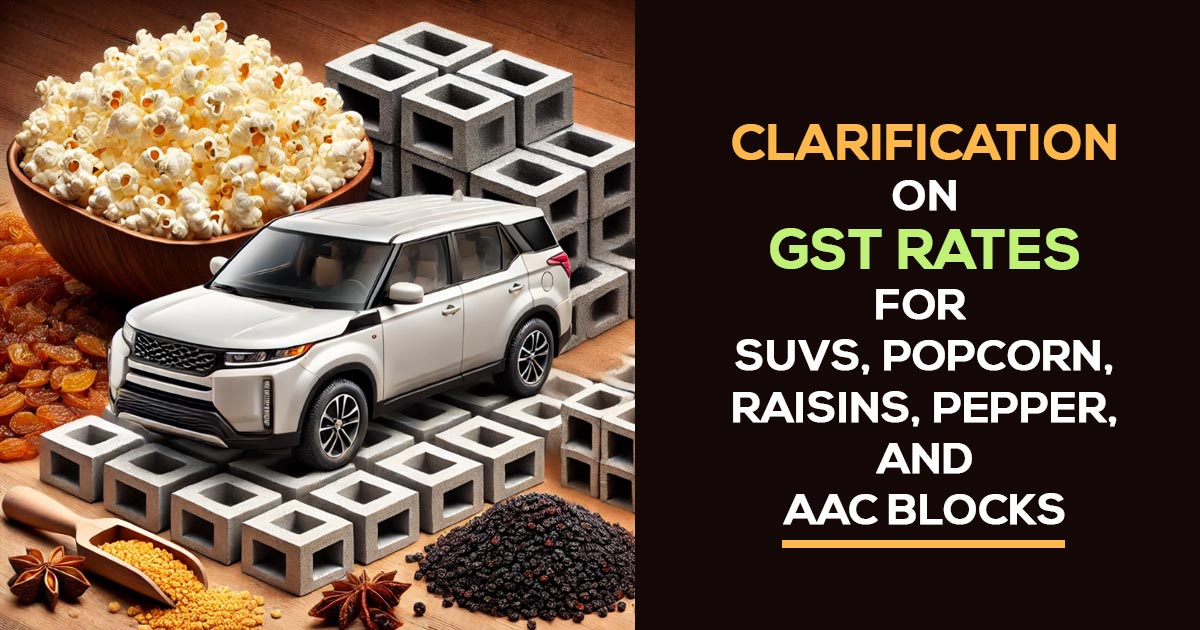

An important clarification has been issued by the Central Board of Indirect Taxes and Customs (CBIC) on the Goods and Services Tax (GST) rates and classification for several products, including pepper, raisins, ready-to-eat popcorn, autoclaved aerated concrete (AAC) blocks, and amendments associated to vehicle ground clearance.

Based on the 55th meeting of the GST Council carried out on December 21, 2024, these clarifications are grounded.

GST Rate on Pepper (Genus Piper)

Queries have been received before the board for the correct categorization and tax rate for pepper, including concerns about whether dried pepper supplied by agriculturists is within GST.

Following the recommendations of the GST Council, it has been decided that all forms of pepper, including green (fresh), white, and black, fall under HS Code 0904 and are levied to a 5% GST rate. This tax rate is established in S. No. 38 of Schedule I of Notification No. 1/2017-Central Tax (Rate) on June 28, 2017.

For agriculturists growing and selling dried pepper directly from their plantations, Section 23(1)(b) of the CGST Act states that individuals involved in farming activities do not require GST registration to sell produce grown on their land. Hence, farmers’ supplies of dried pepper are waived from GST.

Understanding How Raisins from Farmers Are Taxed

The board sought to specify the GST implications for the raisins sold via the agriculturists. As per the suggestions of the GST council, the supply of raisins by a farmer does not attract GST, and the farmer does not need to register under Section 23(1) of the CGST Act.

Taxes on Eat Popcorn

Representatives from various industries asked for guidance on the classification and the applicable GST rate for ready-to-eat popcorn.

The GST council analyzing the case mentioned that salted and spiced popcorn is covered by HS code 2106 90 99.

Unpackaged or non-labelled popcorn is imposed with tax at 5% GST (as per S. No. 101A of Schedule I of Notification No. 1/2017-Central Tax (Rate)).

Pre-packaged and labelled popcorn is taxed at 12% GST (as per S. No. 46 of Schedule II of the same notification).

Popcorn having sugar (e.g., caramel popcorn) is considered a sugar confectionery item under HS Code 1704 90 90 and draws 18% GST (as per S. No. 12 of Schedule III).

Read Also: GST Rates on All Types of Popcorn: FM Sitharaman Explains

The GST council has regularized all past transactions up to February 14, 2025, on an “as is where is” basis for solving the confusion of the past tax treatments of salted and spiced popcorn.

GST Rate on Fly Ash-Based AAC Blocks

For the precise classification, the questions were raised and the tax rate for the autoclaved aerated concrete (AAC) blocks made with at least 50% fly ash.

Fly ash-based bricks, aggregates, and blocks are classified under HS Code 6815 and draw 12% GST (as per S. No. 176B of Schedule II of Notification No. 1/2017-Central Tax (Rate)).

Other cement, concrete, or artificial stone articles (whether reinforced or not) fall under HS Code 6810 and are levied 18% GST (S. No. 181 of Schedule III of the same notification).

It was carried out by the GST council that AAC blocks that have more than 50% fly ash must be categorized under HS code 6815 which makes them qualified for the 12% GST rule.

For Amended Tax on Vehicles Based on Ground Clearance Concerns, the effective date was raised about differences in interpretation for the effective date of amended entry 52B in Notification No. 1/2017-Compensation Cess (Rate), which controls compensation cess on motor vehicles.

Vehicles with an engine capacity over 1500cc, commonly known as SUVs and utility vehicles, were charged with a 22% compensation cess, before the 50th GST Council Meeting.

Following the 50th GST Council Meeting, Notification No. 03/2023-Compensation Cess (Rate) dated July 26, 2023, modified entry 52B. It now stipulates that all utility vehicles, regardless of their name, will draw the 22% compensation cess if they fulfil the following requirements:

- Engine capacity exceeds 1500cc

- Length is greater than 4000mm

- Ground clearance (unladen) is at least 170mm

The GST Council established that this amendment came into force on July 26, 2023.