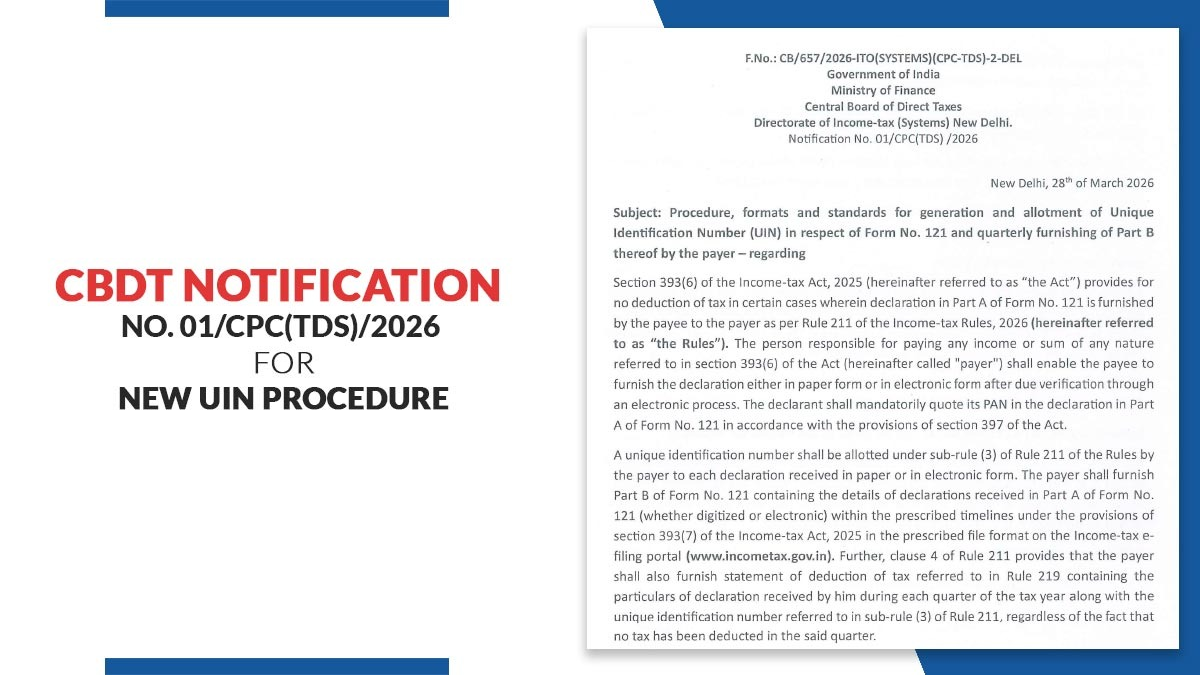

On March 28, 2026, the Central Board of Direct Taxes (CBDT) issued Notification No. 01/CPC(TDS)/2026. The notification specifies a detailed structure for the generation, allotment, and reporting of Unique Identification Numbers (UINs) for declarations made in Form No. 121 under the Income Tax Act, 2025.

W.e.f April 1, 2026, the new system shall come into force and shall apply to all the payers obligated for managing declarations where tax is not deducted u/s 393(6).

What is the Amendment?

Under the new norms, a payee files a declaration in Part A of Form 121 (for non-deduction of tax), the payer is now required to:

- Generate a Unique Identification Number (UIN) for each declaration

- Maintain proper records of such declarations

- Furnish Part B of Form 121 every quarter

The same is applicable irrespective of whether tax has actually been deducted or not.

Read Also:- CBDT Circular No. 02/2026: Extension of Due Date for Issuance of TDS Certificates for Q3 FY26

UIN Structure

The CBDT has specified a 26-character UIN format, which includes three components:

- Sequence Number (10 characters)

Starts with “D” followed by 9 digits

- Tax Year (6 digits)

Example: 202627 for FY 2026-27

3. TAN of the Payer (10 characters)

Example format:

0000000001202627MUMN12345A

Additionally:

- The sequence resets every financial year

- Applies separately for each TAN

All Declarations Covered: Digital and Paper

The notification confirms uniformity by including both:

- Electronic submissions and

- Paper-based declarations (which must be digitised by the payer)

Manually received declarations should be assigned a UIN and included in reporting.

Mandatory Quarterly Filing of Part B

Payers should submit Part B of Form 121 every quarter through the Income Tax e-filing portal, which comprises:

- Information on all declarations received

- Corresponding UINs

- Reporting even if no tax deduction occurred

The same forms a comprehensive audit trail for all non-TDS transactions.

Key Actions for Payers

The framework has been rolled out under:

- Section 393(6) & 393(7) of the Income Tax Act, 2025

- Rule 211 and Rule 332 of the Income Tax Rules, 2026

Such norms ensure that non-deduction claims are effectively tracked and validated.

Its significance

The decision is expected to-

- Improve Tax Authority Oversight

- Clarify Tax Deductions

- Prevent False Exemptions

- Enhance Data Tracking

For tax professionals and businesses, this marks a transformation toward more structured, data-driven TDS compliance.

Action Points for Payers

- Maintain Audit Records

- Automate UIN Generation

- Digitalize Declarations

- Coordinate Quarterly Compliance

- Verify Declarants’ PAN Details

Read CBDT Notification 01/CPC(TDS)/2026