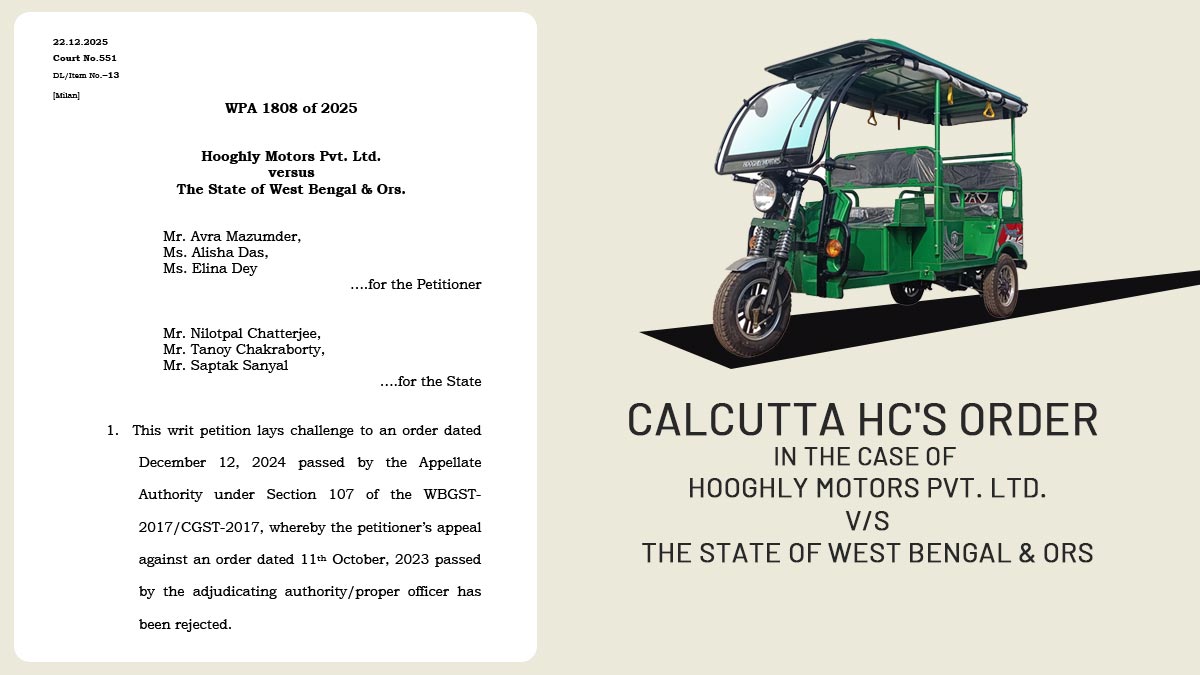

In a recent decision, the Calcutta High Court held that stereo systems used in the manufacturing of e-rickshaws qualify as ‘inputs’ under the GST framework and are eligible for a refund of unutilised Input Tax Credit (ITC) under Section 54(3)(ii) of the GST Act, 2017.

The applicant, Hooghly Motors Pvt. Ltd., had asked for a refund of Rs 8.94 lakh input tax credit (ITC) collected as per the inverted duty structure. In October 2023, the adjudicating authority rejected the claim, stating that stereo systems were not inputs in the manufacturing process.

In December 2024, the same decision was kept by the adjudicating authority. The company, dissatisfied with this, submitted a writ petition before the High Court.

The applicant’s counsel claimed that in May 2024, another appellate authority had permitted a refund in the same case, recognising stereo systems as inputs used in the course of business. The crux of the dispute has emerged from the inconsistency between the two appellate orders.

The counsel of the State in the hearing has given guidelines from the Additional Commissioner of Commercial Taxes (Law), dated July 1, 2025. The departmental clarification mentioned that, “ITC involved in the purchase of ‘stereo system’ to be used in e‑rickshaw would be eligible for refund vide clause (ii) of the first proviso to sub‑section (3) of Section 54 of the GST Act, 2017.”

The note emphasised that inputs should be understood from a business view, rather than being limited to raw materials used in the manufacturing process. The Court examined Section 2(59) of the GST Act, which describes “input” as any goods, excluding capital goods, that are used or intended to be used in the course of, or furtherance of, business.

It also referenced Section 2(17), which defines “business” broadly to include activities that are incidental or ancillary to primary functions. Based on these provisions, the Court concluded that stereo systems installed in e-rickshaws qualify as inputs.

Read Also: Sikkim HC Allows INR 4.37 Crore Tax Refund on Unutilized GST ITC After Business Closure

Justice Om Narayan Rai stated that the rejection of the refund by the adjudicating and appellate authorities was not sustainable under the regulatory norms and departmental clarifications. He said that once the revenue itself had considered the eligibility of the stereo systems as inputs, noting further remained to be adjudicated.

Subsequently, on December 12, 2024, the court set aside the appellate order and asked the respondents to validate records and GST refund the eligible amount to the applicant within 6 weeks.

| Case Title | Hooghly Motors Pvt. Ltd. vs. The State of West Bengal & Ors |

| Case No. | WPA 1808 of 2025 |

| For the Petitioner | Mr Avra Mazumder, Ms Alisha Das, and Ms Elina Dey |

| For the Respondent | Mr Nilotpal Chatterjee, Mr Tanoy Chakraborty, and Mr Saptak Sanyal |

| Calcutta High Court | Read Order |