The Calcutta High Court ruled that tax officers do not have the power under the Goods and Services Tax (GST) Act to seal or take away cash. As a result, the court ordered that Rs. 24 lakhs should be released immediately.

Tax authorities are granted authority under Section 67 of the Central Goods and Services Tax (CGST) Act, 2017, to inspect, search, and seize for preventing tax evasion and ensuring compliance. Justice Om Narayan Rai analysed whether the GST authorities have the authority to seize cash u/s 67(2) of the CGST Act.

The search proceedings for the case were performed at the office and residential premises of the applicant u/s 67 of the CGST Act.

In the investigation, the cash of Rs 24 lacs was sealed by the GST authorities, thereby depriving the taxpayer of his right to use it.

The taxpayer’s counsel said that the whole proceedings have been performed de hors the provisions of law. The department that issued INS-01 does not reveal any cause to assume which could form the grounds of the investigation proceedings.

Read Also: Delhi HC: “Cash” is Not Considered a Type of “Goods”, Can’t Be Seized Under GST

The department claimed that the GST authorities can seize the cash, and in any case, the cash is still in the custody of the taxpayer.

Also, the department stated that as retention of cash to the tune of Rs 24 lacs was discovered by the GST authorities to be doubtful, the GST authorities had told the income tax authority about the same, and therefore, the action in sealing the cash of the taxpayer could not be criticised.

The bench referenced Section 67(2) of the CGST Act, noting that GST authorities have the power to seize goods, documents, books, or other items if they have reasonable grounds to believe that these items may be useful or relevant to any proceedings under this Act and are hidden in any location.

Additionally, the bench highlighted Section 2(52) of the CGST Act, which clearly states that money is excluded from the definition of goods.

Recommended: Kerala HC: GST Dept Cannot Illegally Seize and Transfer Cash to IT Dept U/S 132A

The bench discovered that the action of the GST authorities in seizing cash and sealing the same in the custody of the taxpayer is beyond the administration domain of the GST authorities.

The bench asked the GST authorities to de-seal the cited amount of Rs 24 lacs. The same order shall not be considered as a passport by the applicant to bypass any measure that could be chosen against the applicant if retention or possession of the said cash by the applicant is otherwise found to be illegal, the bench added.

The bench regarding the concern of the validity of the search and seizure proceeding asked the GST authorities to submit an affidavit within 4 weeks. The bench in the aforesaid view has asked the GST authorities to continue the investigation and pass a final order; however, they will not communicate or upload the same on the GST portal without any permission from the court.

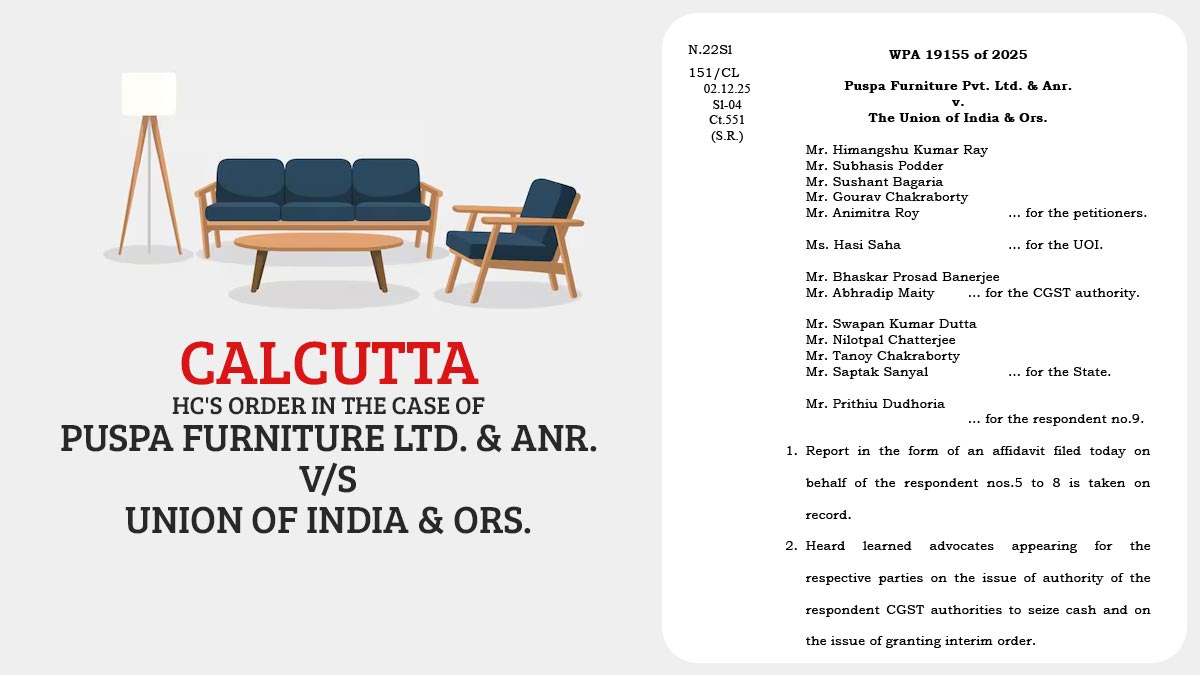

| Case Title | Puspa Furniture Pvt. Ltd. & Anr. vs The Union of India & Ors. |

| Case No. | W.P.(C) 5757/2025 & CM APPL. 26284/2025 |

| For Petitioner | Mr. Himangshu Kumar Ray Mr. Subhasis Podder Mr. Sushant Bagaria Mr. Gourav Chakraborty Mr. Animitra Roy |

| For Respondent | Mr. Prithiu Dudhoria |

| Calcutta High Court | Read Order |