The Central Board of Indirect Taxes and Customs (CBIC) had published the Quarterly Return Monthly Payment Scheme.

CBIC states that the enrolled individual to whom the return in form GSTR-3B is to be filed while providing the eligibility for QRMP, and those whose average turnover is Rs 5 cr in the previous fiscal year are entitled to QRMP policy.

From 1/1/2020 a new scheme will be applied. Moreover, in case the average turnover is more than Rs 5 cr while in any quarter in the present fiscal year then the enrolled person will not be liable for the policy from the next quarter.

Latest Update in QRMP Scheme

- “CBIC implemented new changes in GST QRMP Scheme for the taxpayers on the GSTN portal. The new changes include auto-population of form GSTR-3B, NIL filing of GSTR-1 via SMS, and related to the registration cancellation.” Read PDF

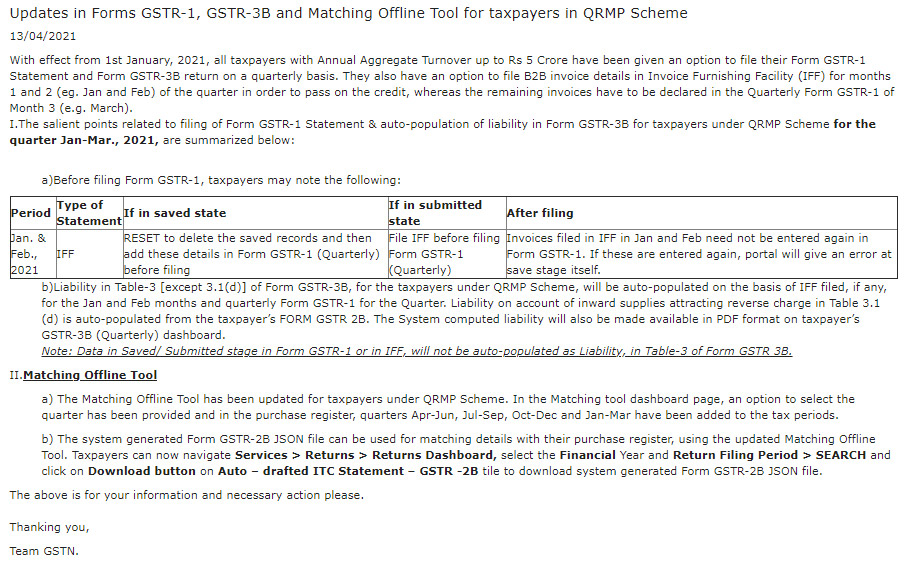

- CBIC has provided a new update related to GSTR-1, GSTR-3B and matching offline tool in the QRMP scheme. Read more

- CBIC released auto-generation in GSTR 2B and auto-population of ITC in GSTR 3B form for the QRPM taxpayers. Read more

- “Important FAQs and details of filing IFF and payment of tax (in Form GST PMT-06) under QRMP scheme.” Check PDF

- “Know details on how to file QRMP scheme https://bit.ly/3oZgBU1 and tax details in PMT 06 furnishing in IFF https://bit.ly/3aMU7Rg“

- “GSTN has started a new Invoice Furnishing Facility (IFF) under quarterly return filing & monthly payment scheme for taxpayers.” Read more

Who can Choose the QRMP Scheme?

Following enrolled individuals (hereinafter RP) could furnish quarterly returns and pay tax on a monthly basis w.e.f. 01.01.2021:

- An RP who is obligated to furnish form GSTR 3B with AATO of up to Rs 5 Cr before the fiscal year is eligible. If AATO exceeds Rs 5 Cr. throughout a quarter, RP will become unsuitable for the policy from the subsequent quarter.

- Any individual procuring the new enrollment or selecting the Composition Scheme can also choose for this Scheme.

- As per the GSTN, one can claim the scheme. Thus some GSTINs to the PAN can choose for the policy and other GSTINs can be out of the scheme.

Alteration on the GST Portal

For Jan. 2021 to March 2021 quarter, the RPs whose AATO for the FY 2019-20 is up to Rs 5 Cr. and has filed a return in form GSTR-3B for 30/10/2020 shall be relocated by default in the GST system as written below:

| Sl. No. | Class of RPs with AATO | Default Return Option |

|---|---|---|

| 1 | Up to Rs. 5 Cr., who have furnished Form GSTR-1 on a quarterly basis in current FY | Quarterly |

| 2 | Up to Rs. 5 Cr., who have furnished Form GSTR-1 on monthly basis in current FY | Monthly |

| 3 | More than Rs. 5 Cr. in preceding FY | Monthly |

When Would the Person Choose for the QRMP Scheme:

- For any quarter and in any year the Facility can be claimed.

- On practicing the option for QRMP scheme will carry till RP revises the option or his AATO will cross Rs 5 cr.

- RPs moved by default can wish to prevail out of the scheme by practicing their option from 5th, 2020 till 31st Jan. 2021.

The RPs choosing for the policy can claim the facility of invoice furnishing facility (IFF) such that the outgoing supplies to the enrolled person will be mentioned in their form GSTR 2A & 2B.

Due Date of Form/Challan PMT-06

The due date of GST Form/Challan PMT-06 under QRMP for tax deposit liability of the current month is 25th of Next month

Payment of Tax Beneath the QRMP Scheme:

- The RPs are payable the rest in each of the two months by 25th of next month in the quarter by choosing “Monthly payment for the true taxpayer” as a judgement to generate Challan.

- Post the adjustment of Input Tax Credit the Fixed Sum Method (pre-filled challan) or Self-Assessment Method (actual tax due) to pay for the monthly payment can be opted by RPs only for 2 months.

- If there are no tax liabilities then no deposit is needed for the particular month.

- To maintain the liability for the quarter for form GSTR-3B the tax deposited for 2 months can be utilized and not for any other purpose till the furnishing of return for the quarter.

A late fine shall be imposed if any delay in the return for an outgoing supply is furnished as per section 47 of the CGST act. Following that, a late fee will be applied for the delay in filing the quarterly returns and the information of outgoing supply. It is understood that there will be no late fine imposed on those who pay delayed tax in the 1st two months of the quarter.

{kind=link}

{kind=link}