The Income Tax Appellate Tribunal has deleted a transfer pricing adjustment of ₹2.84 crore arising from transactions between the assessee and its wholly owned US LLC.

The Tribunal observed that the profits earned by the US LLC had already been included in the assessee’s taxable income and subjected to tax in India. Accordingly, it held that making a separate transfer pricing adjustment would result in double taxation of the same income.

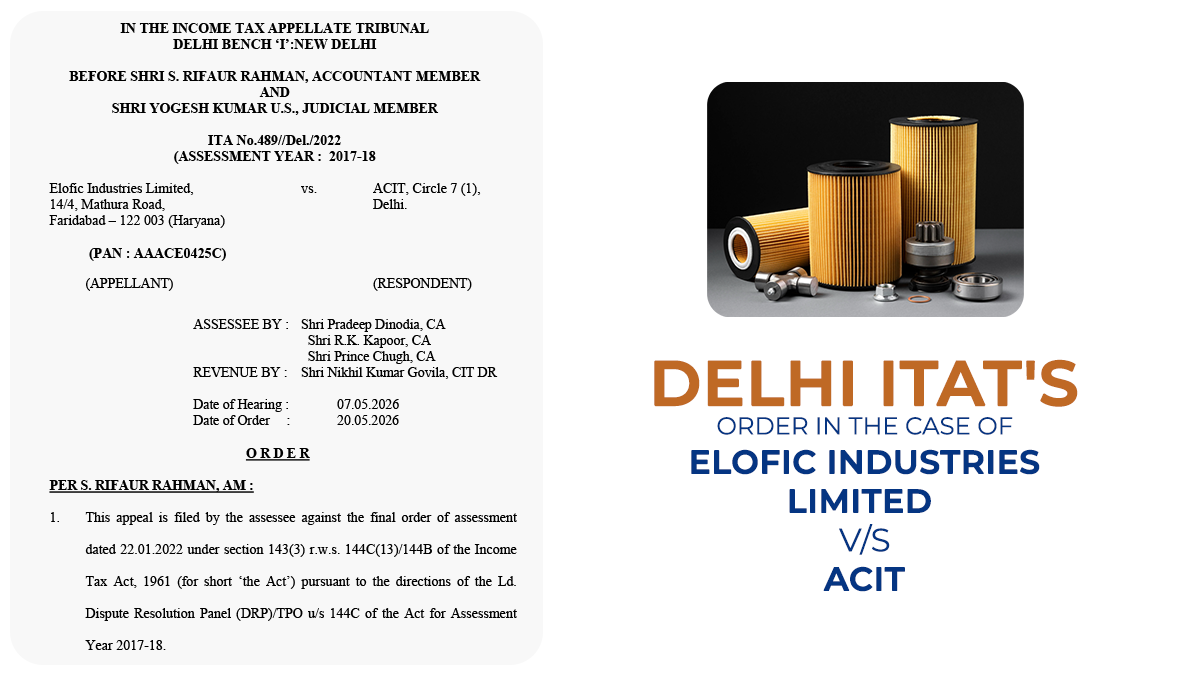

The taxpayer, Elofic Industries Limited, is in the business of manufacturing automotive filters and lubricants and had entered into international transactions with Elofic USA LLC. The LLC was considered an associated enterprise, and the profits earned by it formed part of the taxpayer’s taxable income in India.

The TPO made a transfer-pricing adjustment of Rs 2.84 crore regarding the transactions performed with the US LLC, which was kept by the DRP.

The dissatisfied taxpayer filed a plea before the Tribunal.

Before the Tribunal, the taxpayer argued that Elofic USA LLC was simply a pass-through entity under US law, meaning that all profits earned by it were accurately recorded and reported for taxation in India.

The assessee further stated that there was no diversion of profits outside India and that any adjustments in transfer pricing would not impact the taxable profits of the assessee.

Read Also: ITAT Delhi Removes Tax Penalty Levied U/S 271(1)(c) Over Unspecified Reasons

The orders of TPO and DRP are upheld by the Revenue.

The Tribunal, including S. Rifaur Rahman (Accountant Member) and Yogesh Kumar U.S. (Judicial Member), noted the undisputed fact that the assessee was the sole owner of the LLC and that all income earned via the LLC had been offered for taxation in India.

The Tribunal noted that, according to established legal principles, one cannot trade with oneself or earn profits from oneself. Citing the cases of CIT v. Hind Construction Ltd. (1972) and Aithent Technologies Pvt. Ltd. v. DCIT (2016), the Tribunal held that the lower authorities had failed to recognise that the profits of the foreign entity had already been included in the assessee’s taxable income in India.

Therefore, the Tribunal affirmed that the Assessing Officer (AO) and TPO were not justified in making the transfer pricing adjustment and asked for the removal of the addition of Rs 2.84 crore.

The appeal of the taxpayer was partly permitted.

| Case Title | Elofic Industries Limited vs. ACIT |

| Case No. | ITA No.489//Del./2022 |

| Assessee by | Shri Pradeep Dinodia, Shri R.K. Kapoor, and Shri Prince Chugh |

| Revenue by | Shri Nikhil Kumar Govila |

| Delhi ITAT | Read Order |