Form ITR-B for FY 2025-26 (AY 2026-27) has been reported by the Ministry of Finance via a gazetted CBDT notification 30/2025 dated April 7, 2025.

What is the New ITR-B Form?

The new ITR-B form is used to disclose previously undisclosed income identified by the Income Tax Department during a search, investigation, or requisition operation conducted on or after 1st September 2024.

New Form ITR-B Filing

If you are required to submit ITR-B, then remember that, unlike other ITR forms like ITR-1, 2, 3, etc, ITR-B is submitted for block assessment years. It is similar to that once an investigation or requisition operation has been performed, then you shall be mandated to furnish the ITR for the income which has not been revealed for a particular number of assessment years in bulk, preceding the assessment year pertinent to the earlier year where the investigation was performed u/s 132 or any requisition was made u/s 132A. For instance, we file the ITR-1 Form for 1 financial year, but we can file the ITR-B for 6 years collectively.

Four essential notes have also been released by the ministry for this ITR-B form, which is beneficial in these cases.

ITR-B Form Requirement and Deadline

Under the gazetted notification, the ITR-B is required to be filed u/s 158BC.

The notification cites “Return of income under section 158BC.– (1) The return of income required to be furnished by any person under clause (a) of sub-section (1) of section 158BC, relating to any search initiated under section 132 or requisition made under section 132A on or after the 1st day of September, 2024 shall be in the Form ITR-B and be verified in the manner indicated therein.”

The ITR filing deadline is typically 60 days from the date of the tax notice provided after a search or requisition operation.

CBDT introduced the ITR-B Form dated April 7, 2025, through notification no 30/2025, thereby allowing the searched taxpayers to completely reveal the undisclosed income.

The same comprises classifying it under distinct heads of income, assessment year-wise within the restricted period, and item-wise assets, like as money bullion, jewellery, and virtual digital assets.

The same detailed classification was asked to rectify the transparency, ensuring a thorough assessment of undisclosed income.

Another new form feature is the provision permitting the taxpayers to claim the TDS and TCS credits against an undisclosed income. These claims stayed within the verification and the satisfaction of the tax officer, who might face challenges with the procedure.

Mixed reactions can be drawn by the introduction of ITR-B. It seems to be a positive development focused on transparency and the digitalization of income reporting following search operations.

Significant Notes for Filing ITR-B Form

As per the notification, below is the information-

Note 1: AY Y6 to Y1

6 assessment years preceding the assessment year pertinent to the earlier year in which the search was begun u/s 132 or any requisition was incurred u/s 132A.

AY Y0

Where search/requisition is concluded in the same year in which it was begun: Y0 is the period in the assessment year pertinent to the previous year, which will be from the 1st April of the year in which search/requisition begins up to the date of execution of the last of the authorisations for search or requisition.

Where the date of execution of the last of the authorisations for search or requisition comes in an earlier year next to the year in which the search or requisition was started, Y0 is the complete assessment year pertinent to the earlier year commencing from the 1st April of the year in which the search/requisition is started and up to 31st March of that year.

AY Y+1

(To be filled in case the date of execution of the last of the authorisations for search or requisition comes in a previous year after the year in which the search or requisition was initiated) Y+1 is the period in the assessment year pertinent to the aforementioned year, which will be from the 1st April of the year in which the last authorisations of search/requisition were performed and ending with the date of the last authorisation of search/requisition.

Note 2

Section 158BB(1A)(c)(i)- Towards the objective to file the details of the assessment year Year 1, where the pertinent last year has ended, and the deadline for providing the return under section 139(1) for there year does not expire, where the accounts are not audited (if they are needed to be audited), provisional numbers are mandated to be provided established on the books of account kept in the normal course.

It would not be regarded as a return u/s 139(1) for the pertinent assessment year. Also, the same income is mandated to be included in the income return provided u/s 139 for the pertinent assessment year.

Note 3

Section 158BB(1A)(c)(i): For the objective to file the information of the assessment year Y0 (where Y0 is a complete year), where the pertinent earlier year has ended and the deadline to file the return u/s 139(1) for the year does not lapse, provisional numbers are mandated to be provided established on the books of account kept in the normal course.

It will not be regarded as a return u/s 139(1) for the pertinent assessment year. Also, the same income needs to be comprised in the income return provided u/s 139 for the pertinent assessment year.

Note 4

Section 158BB(3): As per the provisions of the same section, any undisclosed income concerning any international transaction or particular domestic transaction related to the part earlier year, including in the block period, is mandated to be computed under provisions apart from the applicable provisions for block assessment.

As per that, any undisclosed income based on this does not need to be submitted as part of the block return.

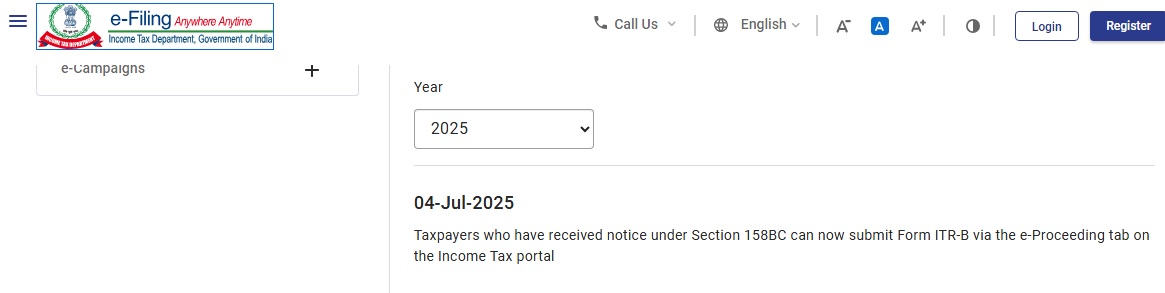

Note: The ITR-B form is now available on the e-filing portal for taxpayers who have received a notice under Section 158BC. View More

Online Process to File ITR-B Form

- Open the Income Tax e-Filing Portal

- After opening the portal, log in using your PAN-based credentials

- From the dashboard, hover over the relevant menu and click on e-Proceedings

- Select the applicable case under Section 158BC

- Finally, upload Form ITR-B and attach any supporting documents as needed

{kind=link}