E-commerce or electronic commerce (an online shopping hub) manages the buying and selling of products and services exclusively through electronic channels. The global e-commerce share of total retail sales is much lower. In 2024-2025, it is projected to be around 20% to 21% globally. According to the GST council 21st meeting, the registration for all the taxpayers registered under TCS can start their registration from 18th September 2017.

The relevant definitions and provisions are now contained in the Central Goods and Services Tax Act, 2017 (CGST Act), primarily Section 52 (for TCS) and Section 2(45) (for ECO definition). Also, a person providing any information or any other services incidental to or in connection with such supply of goods and services through an electronic platform would be considered as an Operator. A person supplying goods/services on his own account, however, would not be considered an Operator.

Latest Update in E-commerce Operators

- 53rd GST Council Meeting Update: GST Council has recommended halving the TCS rate for Electronic Commerce Operators (ECOs), from 1% (0.5% CGST + 0.5% SGST/UTGST or 1% IGST) to 0.5% (0.25% CGST + 0.25% SGST/UTGST or 0.5% IGST). View More

- GST Council had approved in principle the intra-state supply of goods through E-Commerce Operators (ECOs) by unregistered suppliers and composition taxpayers at its 47th meeting. read more

- The Authority for Advance Ruling (AAR) of Karnataka has ruled that an 18 per cent GST rate on the sale of internet advertising space on e-commerce portals. read order

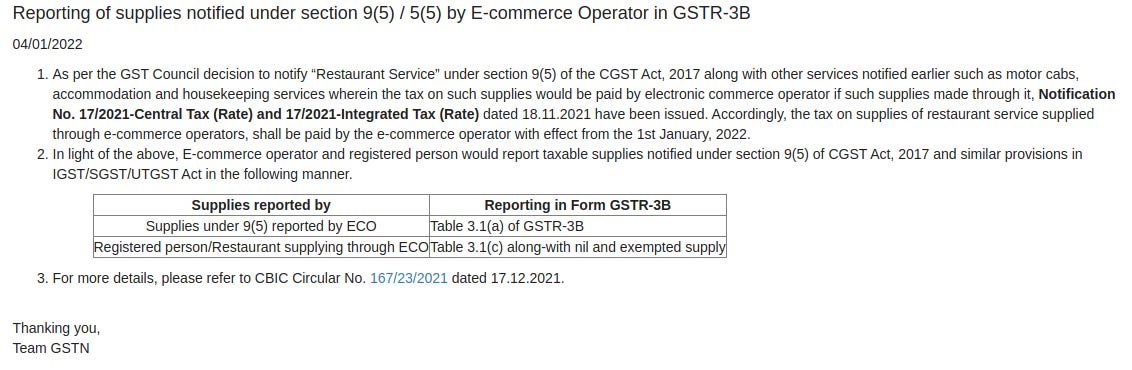

- “The GSTN has released the advisory related to reporting taxable supplies of restaurant services and other services by e-commerce operators in Table 3.1(a) and Table 3.1(c) of GSTR 3B.” Read More

For instance, Amazon and Flipkart are e-commerce Operators because they are facilitating actual suppliers to supply goods through their platform (popularly called the Marketplace model or Fulfilment Model). However, Titan supplying watches and jewels through its own website would not be considered as an e-commerce operator for the purposes of this provision. Similarly, Amazon and Flipkart will not be treated as e-commerce operators in relation to those supplies which they make on their own account (popularly called the inventory Model).

The MGL provides that every operator has to register at the GST portal, irrespective of the threshold limit specified for registration for GST. This is the biggest disadvantage for small retailers, as they work on fixed working capital and will have to pay taxes and apply for a refund later, which is a cumbersome process.

A centralised system for registration under service tax is available, but under the GST regime, the centralised registration may not be available as the place of supply will decide the scope of registration, in which state the registration will take place. The place of supply in case of B2C transactions would be the location of the service provider, and in the case of B2B transactions, it would be the location of the service recipient. Hence, obtaining registration in every state where there is a place of business will result in increased compliance.

The TCS provision in the final CGST Act, 2017, is Section 52. Section 43B of the Income Tax Act relates to the disallowance of expenses, and there are different sections under Chapter IX of the CGST Act. Such an amount of TCS is to be deposited by the E-commerce operator into the GST account by the 10th day of the next month. As per the MGL, both the supplier and the operator have to upload their respective entries and have to match. It is very important to reconcile the data entries otherwise, it will be unfair for the respective party. The TCS can play a major disadvantage in case of cash-on-delivery products being rejected at a later stage. The cash flow cycle of the operator may have an adverse effect on its operations. If we talk about the discounts offered by these operators, which are the most popular techniques to attract customers, it will give a major throwback as the e-commerce firms will have to pay tax on the price it has paid for goods, thereafter bearing the additional tax burden.

Read Also: GST Impact on Indian Telecom Industry

If we see the price impact of the product or service, it will be higher compared to the current service tax rate, but the higher credit will reduce the prices of the services or product.

With all the new regulations, it seems that the model GST law including the TCS (tax collection at source) clause can prove harmful for the companies as the clause demands the tax remitted should be deposited to the government on the behalf of sellers which is considered a very tedious task by the e-commerce companies. The parliament holds the decision to speculate on this issue and mold the clause.

The GST council, in the direction of giving some liberation to the e-commerce sector taken the step to cap the rate of highly controversial TCS in the clause of managing the e-commerce industry, which requires the companies to deduct a percentage of total sales before handing over the amount to the sellers. While the statutory cap is 2% (1% CGST + 1% SGST), the notified rate was 1% in total (0.5% CGST + 0.5% SGST/UTGST or 1% IGST) until the recent 53rd Council decision. The new effective rate is 0.5% in total.

As the TCS (Tax collected at source) clause it growing bigger within the e-commerce sector, its worries are making a panic too. The e-commerce industry has claimed that government has mistakenly considered the e-commerce sector as ‘shops’ which is meant to say a direct retailing point but the sector clarifies that they are a platform for the sellers and buyers to engage and make the transaction happen.

Various industry experts are commenting in support of the sector while also mentioning the government aspect of making no stone unturned in the case of tax evasion. There will be an approximately 400 crores of capital which might get stuck within the parameters of GST and may cause harm to the industry furthermore. Also, there are issues of compliance as the e-commerce sector will have to implement a lot of compliance which will also increase the cost of operation.

Amarjeet Singh, Partner, Tax, KPMG in India, “What the industry is saying is that they are not shops but platforms. TCS would increase a lot of compliance, a lot more disclosures would have to be made and costs would be high as the volume of data would increase. The intention of the government is right and one percent TCS is fine. Having said that, it would mean an increase in compliance for the sector.”

If we analyze, on the whole, we can conclude that e-commerce companies will be liable to comply with all the obligations cast on normal suppliers under MGL / IGST Act like obtaining registration, payment of GST, the filing of periodical returns, etc. With the arrival of GST, there will be more complexities, but it is expected that the government will provide some incentives/exemptions to overcome the same.

Update on E-commerce sector after Festive Season

Numerous e-commerce companies like Amazon, Flipkart, Snapdeal have gone through a great festive season in 2017 as input tax credit benefits of GST was given to the consumers this time which in return made bumper sales. According to the All India Online Vendors Association, this festive season proved beneficial for the vendors as earlier the e-commerce companies used to deduct commission from the sellers on every purchase, on which there was service tax applicable and there was no credit available on it.

But this time, under the GST regime there is only one tax applicable and on which the input tax credit is available. This availability of credit makes the sellers increase their approach in the sales and further discounting products.

KPMG tax partner also stated that earlier before GST, the companies and the vendors didn’t get input tax credit but after the implementation of GST, it has been getting ITC on taxes. This return credit is being offered to the customers in the name of discounts.

FAQs on E-commerce Sector Under GST

Q.1 – Would ECOs need to obtain TCS in complaints with section 52 of the CGST Act, 2017?

As the restaurant services would be reported under section 9(5) of the CGST Act, 2017, ECO will be responsible to furnish the GST on the furnished restaurant services, wef 1st Jan 2022, via ECO. As per that ECOs would no more need to collect TCS and furnish GSTR 8 on restaurant services upon which the same furnish tax in terms of section 9(5). Upon additional goods or services supplied via ECO, that would not be reported u/s 9(5), ECOs shall continue to file TCS as per section 52 of CGST Act, 2017 in an exact way.

Q.2 – Would ECOs need to avail a separate registration wrt the supply of restaurant services reported under 9(5) by them despite they are enrolled to file GST on the services on their own account?

As ECOs would be enrolled as per rule 8(in Form GST-REG 01) of the CGST Rules, 2017 (as a supplier of their own goods or services) then there will be no need of taking the separate registration through ECOs towards the tax payment on the restaurant services under section 9(5) of the CGST Act, 2017.

Q.3 – Would ECOs be responsible for filing the tax on the supply of restaurant services incurred through the unregistered business entities?

Yes. on any restaurant services supplied by them along with the unregistered individual an ECO would be obligated to file the GST.

Q.4 – What shall be the aggregate turnover of the individual who supplies the restaurant services via ECOs?

The same would be said that the aggregate turnover of the individual who used to supply the restaurant service via ECOs will be calculated as described in section 2(6) of the CGST Act, 2017 and thus consist of the aggregate value of the supplies incurred by the restaurant via ECOs. As per that, the consideration limit or any additional objective in the act, the individual furnishes the restaurant services via ECO will account for these services in his aggregate turnover.

Q.5 – Could the supplies of the restaurant services incurred via ECOs be recorded as the inward supply of ECOs (obligated to reverse charge) in GSTR 3B?

No. ECOs would not be the recipient of the restaurant services furnished by them. As these are not the input services to the ECO, the same would not be notified as the inward supply (responsible for the reverse charge).

Q.6 – Can ECOs be obligated to reverse proportional ITC on their input goods and services for the reason that the ITC would not admissible on the restaurant services?

ECOs furnish their own services as an electronic platform and an intermediary towards which the same shall take the inputs services where ECOs take the ITC. The ECO imposes the commission or fee towards the services which it furnishes. The ITC would be used through the ECOs regarding the GST payment on services furnished by ECO on its own account (a restaurant). The condition for that case will not be changed even after ECO would be obligated to file the tax on the restaurant service. ECO shall be qualified to ITC as before. As per that, the same would be specified that ECO will not need to reverse ITC on the basis of the restaurant services where the same furnishes the GST towards section 9(5) of the Act. the same would indeed be reported that on the services of the restaurant, ECO will file the whole GST liability in cash (no ITC can be used for the GST paid on the restaurant services supplied by ECO).

Q.7 – Could ECO use its ITC to file the tax with respect to the restaurant service supplied via ECO?

No. as mentioned above, the liability of the tax payment by ECO according to section 9(5) will be released in cash.

Q.8 – Can the supply of goods or services excluding the restaurant services via ECOs be taxed at a 5% rate without ITC?

ECO would be needed to file the GST on the services reported under section 9(5), apart from that the services or other supplies incurred on his own account. On any supply which would not be reported under section 9(5), which is supplied via individual via ECO, the obligation to file GST will be resumed subsequently on these suppliers and ECO will carry on to pay the TCS on these supplies. Hence, at the current time, the utility continues for ECO, on the supplies excluding the restaurant services. On these types of supplies (additional to restaurant services incurred via ECO) GST would continue to be billed, obtained, and deposited in a similar way as it is being executed at the current time. ECO shall deposit TCS on these supplies.

Q.9 – Could the service of the restaurant and goods or services excluding the restaurant services sold through the restaurant towards the customer, identical order be billed varies? Who is obligated to raise the invoices in these cases?

Acknowledge the liability to file the GST on the supplies excluding the restaurant services via ECO and the additional compliance beneath the act as well as the invoice issuance towards the customer lies towards the respective suppliers (and ECOs being responsible to collect tax at source (TCS) on these supplies), recommended that ECO asks for the separate bill on the restaurant service in these cases where ECO used to furnish additional supplies to the customer beneath the identical order.

Q.10 – Who shall furnish the invoice for the restaurant service furnished via ECO whether through the restaurant or through ECO?

ECO will issue the invoice for restaurant service supplied via ECO under section 9(5).

{kind=link}

{kind=link}

WOODEN HANDICRAFTS GST RATE LIST

Sir,

My friend is a service provider and has a turnover of about 3 lacks from his office plus below 1 lack from his own website and over all his total turnover is about 4 lacks.. Please inform me whether he requires to register in GST because he has online presence through his own website. he maintains himself his own website.

For Online Database and Information. Registration is compulsory. No limit of 20 lacs.

Due date is 31st July for Return filling. But you can file it before 31st march with interest.

In the Revised Model GST law,the definition of E-Commerce operator has been changed.

i.e Earlier it was defined in the main provision it self but now it is included in the definition part which reads as under

“MEANS any PERSON who owns,operates or manages digital or electronic facility or platform for ELECTRONIC COMMERCE”

and

E-COMMERCE “means supply of goods and/or services including digital products OVER digital or electronic network”. What is the exact meaning of E-Commerce ? Why they used the preposition OVER ? how goods can be supplied over digital network ?

and

While going through the revenue sources of FLIP-KART i found that it will charge commission on supplies-effected through it apart from the listing fee and advertising charges. So,can we consider FLIP-KART as an AGENT.If so,FLIP-KART is not required to collect TCS as per section 56 of the Revised Model GST law.

E-Commerce means if any person or agency sells his goods or services via internet or any electronic mode and receive payment for this cover under E-Commerce. Now as you say an agency has change its fees as commission in that situation too as a company is selling its goods through online so it is covered under e-commerce and that’s why the liability to collect TCS as per section 56 is required by the agency.

Can u please go through the question once again.Please refer the definition of E-Commerce under revised Model GST law.