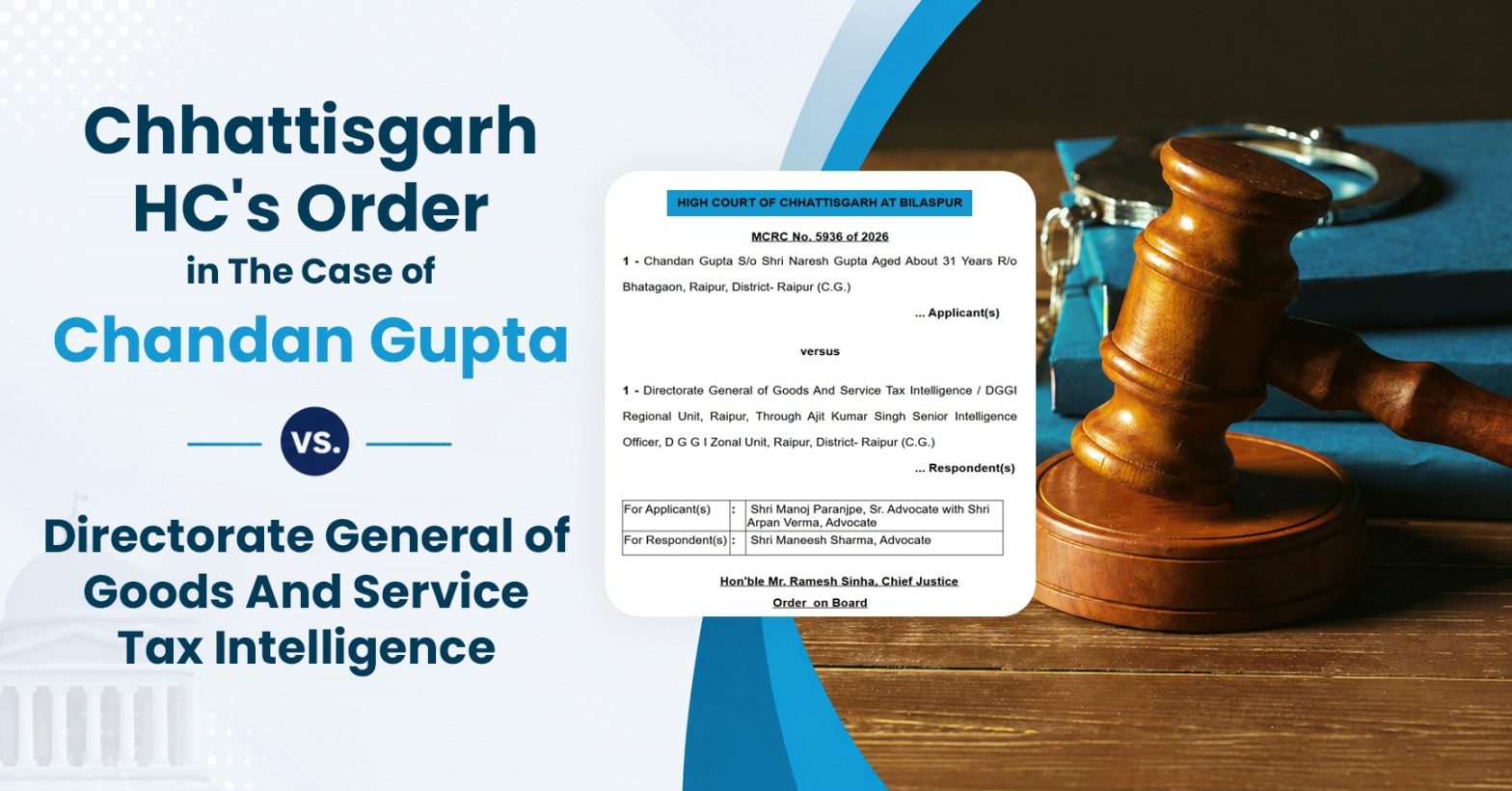

Just recently, the Uttarakhand High Court gave an important ruling where they decided that a petitioner should definitely get relief regarding the cancellation of their Goods and Services Tax (GST) registration.

This happens especially when the whole dispute is already covered by a past precedent that was set earlier by a Division Bench of this very same Court.

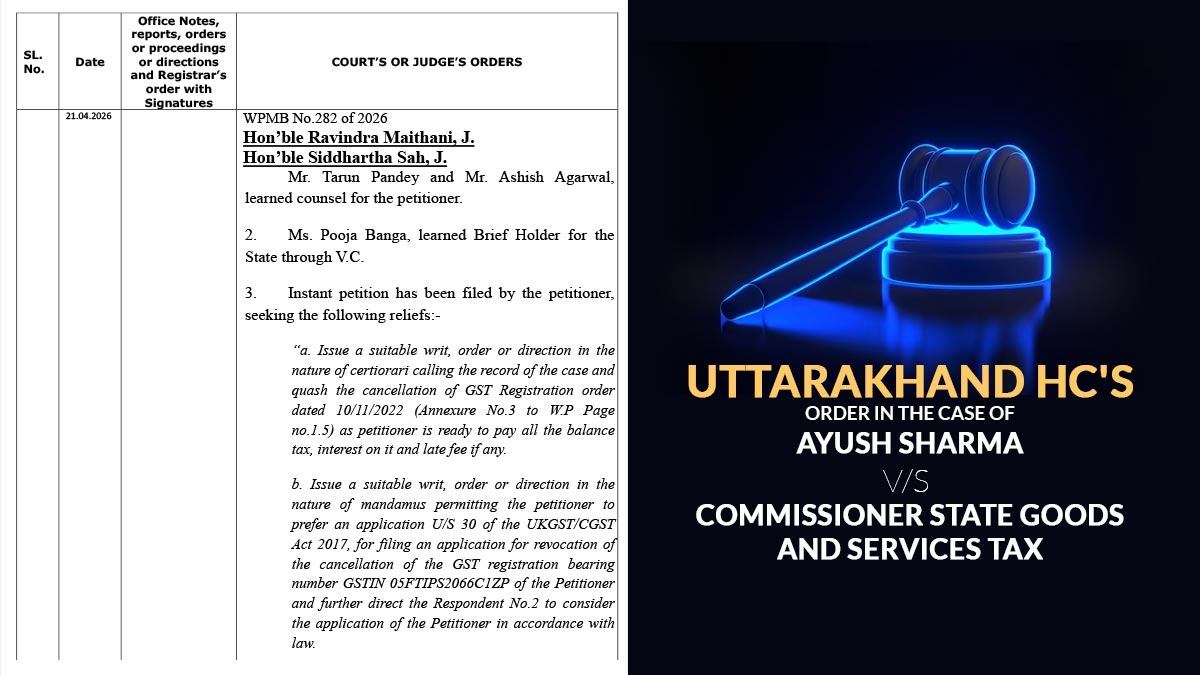

Going into the details, this specific case started with a writ petition that was filed by the petitioner, Ayush Sharma. He was basically challenging an older order from back on 10/11/2022 that had unfairly cancelled his GST registration.

To fight this, he asked the court for a writ of certiorari so that the cancellation order could be completely quashed. Along with that, he also requested a writ of mandamus to allow him to officially file an application for revocation under Section 30 of the Uttarakhand Goods and Services Tax (UKGST/CGST) Act, 2017.

To show his good faith, the petitioner also clearly mentioned that he is ready to clear and pay any pending balance tax, interest, and late fee charges that might be due.

While the hearing was taking place, the lawyer representing the petitioner pointed out something crucial. They made the argument that this whole matter is actually directly covered by an older judgment passed on 24.02.2025 by the Division Bench in the case of WPMB No.39 of 2025, which was titled M/s Anshul Enterprises through its proprietor Vs. State Tax Officer.

Important: Delhi HC Orders Cancellation of GST Registration Must Be Mentioned in the SCN

Interestingly enough, the lawyers for the opposing side (the respondents) agreed and admitted to this fact. In that older case, the Court had allowed the Petitioner to go ahead and file an application for the revocation of their GST registration cancellation order.

Now, it’s important to note that this kind of relief came with a specific condition. The petitioner had to deposit all the unpaid taxes, along with any interest and penalties, within a strict and specified timeframe.

Once that was done, the competent authority in charge was given clear directions to make a decision on the revocation application within exactly four weeks of it being filed. This was to make sure that the proper assessment of the revocation request was handled strictly in accordance with the law.

Looking at all these facts, the Division Bench consisting of Justice Ravindra Maithani and Justice Siddhartha Sah made a very clear observation.

Read Also: Uttarakhand HC: Filing NIL GST Returns Is Not a Valid Ground for Cancellation of Registration

They noted that since the factual background and the legal issues in this current dispute were totally identical to the previously decided matter, this instant petition simply had to be adjudicated by following the same exact logic of that earlier judgment.

Because of this solid reasoning, the High Court officially decided to resolve the petition based on the terms set out in the judgment dated 24.02.2025 (passed in M/s Anshul Enterprises through its proprietor Vs. State Tax Officer).

Must Read: How GST Software Helps Protect Your Business from Cancellation

In the end, they granted the exact relief that the petitioner was asking for.

| Case Title | Ayush Sharma vs. Commissioner State Goods and Services Tax |

| Citation | WPMB/282/2026 |

| For the Petitioner | Mr. Tarun Pandey and Mr. Ashish Agarwal |

| Uttarakhand High Court | Read Order |