The approach behind the Employee Provident Fund (EPF) scheme is to provide significant benefit to the employees at the time of their retirement. The scheme specifies that a nominal amount is deducted from the salary of an employee as a contribution towards the fund. According to the latest circular, which has got affected from June 1, 2015, changes have been made regarding the Income-tax rules on the EPF withdrawal by one of the biggest retirement funding associations worldwide, Employee Provident Fund Organization (EPFO).

(Update: Budget-2016)

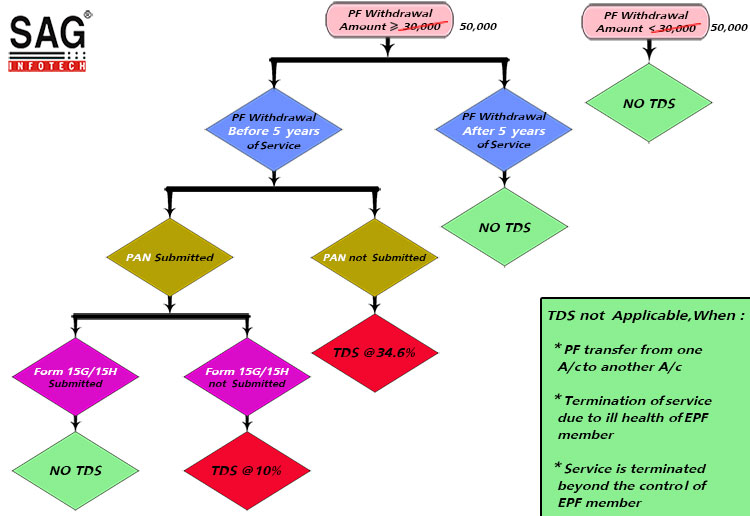

Payment of an accumulated balance to pay an employee from PF, the threshold limit increased from Rs. 30,000 to limit Rs. 50,000. So, TDS is not applicable if PF withdrawal amount is less than Rs 50,000.

PF Withdrawal Rules associated with TDS

Cases where TDS is not applicable

- If the amount, which is to be withdrawn as PF is less than

Rs. 30000Rs. 50,000. - No tax on pf Withdrawal after 5 years or more of continuous service.

- If an employee withdraws an amount of more than or equal to

Rs. 30000Rs. 50,000 before 5 years but submits Form 15G /15H along with his / her PAN. - When a transfer of PF is from one A/c to another A/c.

- Being an EPF member, if the service has been terminated due to ill-health and he withdraws his accumulation (balance).

- If the employer discontinues the business or any cause beyond the control of EPF Scheme’s member (Employee).

Cases where TDS is applicable

When accumulation is more than Rs. 30000 Rs. 50,000 and the employee i.e. the EPF member has worked less than 5 years, then two cases are there:

- Deduction of TDS will be at 10% if PAN is submitted, but 15G/15H Forms are not.

- Deduction of TDS will be at maximum marginal rate i.e., 34.608% if PAN is not submitted.

Flowchart: TDS on EPF Withdrawal

Some other important key points:

- If the subscriber has submitted all the required forms, then he/she will get an exemption from TDS with no taxable income.

- TDS will be deducted under Section 192A of Income Tax Act, 1961 and it is deductible at the time of payment.

- Form 15G and 15H are self-declarations and may be accepted in duplicate.

- If the amount of withdrawal is beyond 2,50,000 or 3,00,000 respectively, then Forms 15G and 15H cannot be accepted.

Hi,

I have left an organisation after 6 years and joined another organisation, but due to some situation I have left the same after 5 month, but I have transferred my pf amount old organisation to new organisation, currently, I am not working, can TDS applicable when I withdraw my pf amount please suggest.

No TDS will be deducted if the PF amount is withdrawn after a continuous service of 5 years.

Hi,

I applied for pf advance under form 31, they approved Rs. 7500 and received that amount. Now I am terminated and unemployed and applied pf amount only under form 19 for total amount Rs .47000, my UAN not attached with PAN due to an error in my father name. I have 2 years of experience.

For this transaction tax would be applicable?

Please advice.

If the amount has been withdrawn before completion of 5 years underemployment and reasons other than termination by reason of the employee’s ill-health, or by the contraction or discontinuance of the employer’s business or other cause beyond the control of the employee, the withdrawn amount will be taxable.

I have served in my previous organization for less than 5 years from May 2010 to April 2015. And I have withdrawn PF after 7 years in Nov 2017. My question is whether this PF amount is taxable?

It will be taxable since word “continuous employment for 5 years” have been specified to be eligible for exemption.

I have served in my previous organization for less than 5 years from May 2010 to April 2015. And I have withdrawn PF after 7 years in Nov 2017. My question is whether this PF amount is taxable?

Thanks,

I was asked to resign after serving for 4.5 years i.e June 2016. After 5 months of unemployment in November, I applied for PF transfer in UAN no. Being Pvt PF Trust they denied and asked me to file for the refund along with Form 15-G/15-H and assured it will not be taxable. Due to the difference of name in Bank A/C and PF, a/C refund was not made in FY 2016-17. subsequent to corrections and resubmit of documents refund was made in October 2017. They deducted TDS on the EPF Refund. In Dec 2016 I got employed and got the refund of 100 % tax deducted for being low in income. Whereas with this additional income of EPF taxable income falls in 30 % slab. This way there is double penalization. Please clarify a. is the EPF withdrawal is taxable since refund has been made after 5 years through years of service is < 5 years. (b) If it is taxable why not this income be considered in the FY 2016-17 in place of 2017-18.

Your suggestion is important and where and how the case be presented in the taxation department.

Thanks and regards,