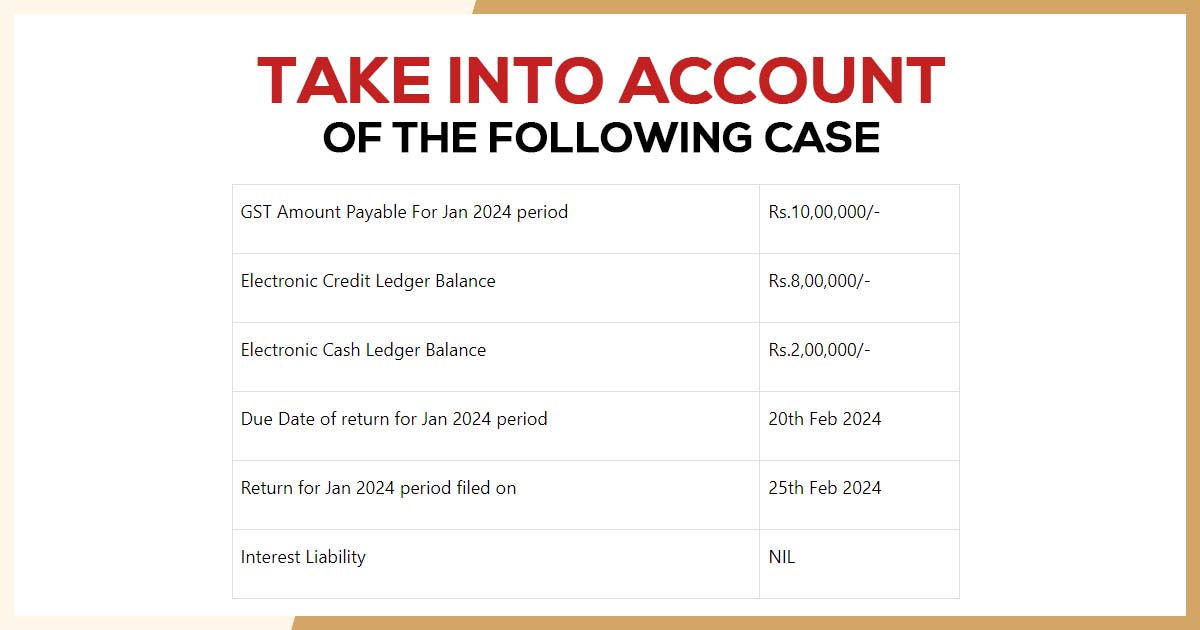

Section 50 of The CGST Act was revised to furnish that there would be no interest obligation on late filing of GSTR-3B to the extent of the balance in The Electronic Credit Ledger, the Courts in the following and other cases ruled that interest was subjected to be paid even after there was balance in the Electronic Cash Ledger.

Different Cases of High Courts

- Orissa Stvedores Ltd vs. Union of India reported in MANU/OR/1116/2022;

- RSB Transmission (India) Ltd. vs. Union of India reported in MANU/JH/1260 – 2022-VIL-745-JHR; Read Order

- Srinivasa Stampings vs. SPT of GST & CE in W.P.No.7129 of 2021 – 2022-VIL-285-MAD Read Order

- P.K. Ores P Ltd vs Commissioner of State Tax reported in MANU/OR/236/2022 – 2022-VIL-365-ORI; Read Order

- Haji Lal Mohd Biri Works vs. State of Uttar Pradesh reported in (1974) 3 SCC 137 – 1973-VIL-22-SC;

- Prahlad Rai vs. Sales Tax Officer reported in (1991) Supp (2) SCC 612 – 1990-VIL-20-SC;

- Commissioner of Sales Tax vs. Qureshi Crucible reported in (1993) Supp (3) SCC 495 – 1993-VIL-10-SC;

- Refex Industries vs. Assistant Commissioner of CGST reported in 2020 SCC Online Mad 587 – 2020-VIL-71-MAD; Read Order

- Manasarover Motors P Ltd vs Assistant Commissioner reported in 2020 SCC Online Mad 28155 – 2020-VIL-524-MAD;

- The Sales Tax Officer vs. Dwarika Prasad Sheo Karan Dass reported in (1977) 1 SCC 22 – 1976-VIL-43-SC;

- Khazan Chand vs. State of Jammu and Kashmir reported in (1984) 2 SCC 456 – 1984-VIL-12-SC;

The Madras High Court in the matter of M/s EICHER MOTORS LIMITED [2024-VIL-72-MAD] has carried otherwise. The foundation on which this judgment was delivered is as follows-

1. Section 39(1) and 39(7) of CGST Act (Act) mandate that assessees who are directed to provide GSTR-3B return under Section 39(1), will “pay” to the Government the tax due “before” providing the GSTR-3B return and disclose “tax paid” in the GSTR-3B return.

Section 39(1) and 39(7) states as below:

“39. 6[(1) Every enrolled individual excluding an input service distributor or a non-resident taxable individual or a person who files the tax under the provision of section 10 or section 51 or section 52 will to every calendar month or part thereof, provide, a return, electronically, of inward and outward supplies of goods or services or both, input tax credit availed, tax payable, tax filed and these additional particulars, in these form and manner, and the similar period, as may be specified:

Given that the Government might on the council’s suggestion show a specific class of enrolled individual who provides the return for every quarter on the part thereof, as per these conditions and limitations as might be stated in it.

7[(7) Every registered individual who is needed to provide a return under sub-section (1), excluding the person referred to in the proviso thereto, or sub-section (3) or sub-section (5), shall pay to the Government the tax due according to such return not later, the due date on which he is needed to provide such return:

9 [Given that every registered person providing the return under the proviso to sub-section (1) will pay to the Government, in such manner, and within such time, as may be prescribed,

(a) an amount equivalent to the tax due carrying into account inward and outward supplies of goods or services or both, ITC claimed, tax payable, and such other particulars during a month; or

(b) in place of the amount referred to in clause (a), an amount determined in a way and as per these conditions and restrictions as may be prescribed.]”

Given that each enrolled individual providing a return under sub-section (2) will pay before the Government the tax due taking into account turnover in the State or Union territory, inward supplies of goods or services or both, tax payable, and other particulars in a quarter, in such form and manner, and within such time, as may be prescribed.]

2. Section 49(1) mandates that amounts deposited via assessees will be credited to the electronic cash ledger (ECL) of the taxpayer. Rule 87(6) & 87(7) of The CGST Rules (Rules) also specifies that a CIN would only be generated after the Government’s accounts are credited.

Section 49(1) and Rule 87(6) & 87(7) specified as-

“Section 49(1) Every deposit created for tax, interest, penalty, fee, or any additional amount via a person through internet banking or by using credit or debit cards or National Electronic Fund Transfer or Real Time Gross Settlement or through this other mode and subject to these conditions and restrictions as may be specified, shall be credited to the electronic cash ledger of these individuals to be carried in a way as may be stipulated.”

“Rule 87 (6) On successful credit of the amount to the related government account kept in the authorized bank, a Challan Identification Number will be generated through the collecting bank and that will be demonstrated in the challan.

87(7) On the receipt of the Challan Identification Number from the collecting bank, the defined amount will be credited to the electronic cash ledger of the person on whose behalf the deposit has been made and the common portal make available a receipt to this impact.”

3. The RBI has made the amounts of so deposited before the accounts of the Government as clarified through the RBI in FAQ 8 on 14th April 2020. The Explanation (a) to Section 49 read with Section 49(11) specifies that the date when amounts are deposited is the date when the Government’s accounts are credited.

The pertinent extracts of provisions are as under –

“FAQ 8. What is the role of RBI in the Goods and Service Tax regime?

For accounting of all GST collections in the respective government accounts the Reserve Bank of India is the aggregator. Agency banks collect the GST for challans generated via taxpayers online on the report of the GST portal the collections for settlement to government accounts to RBI. RBI has eased the GST payment via taxpayers directly into government accounts at RBI by using NEFT / RTGS payment options provided in the GST portal.”

“Section 49 (11) Where any amount has been transferred before the electronic cash ledger under this Act, it will be considered to be deposited in the said ledger as furnished in sub-section (1).]”

Explanation- For this section-

“(a) the credit date to the account of the Government in the authorized bank will considered to be the date of deposit in the electronic cash ledger;”

4. GST collection numbers arrived at through the Government are made on the grounds of the amount deposited in the electronic cash ledger and not the amount set off at the time of filing the GSTR-3B returns.

5. The Government uses the money of the ECL. There is no financial loss for the Government. if the money in the Electronic Cash Ledger (ECL) is not set off by GSTR-3B. It shall be ruinous for the exchequer if the amounts are not authorized to be used.

6. Under Section 54(12) in case there is a delay from the Government side. in refunding the amount in the ECL availed via taxpayer beyond a time, it needs to pay interest. If the amounts in ECL were not used by the Government, in what way shall it pay interest on a delayed refund?

“Section 54 (12) in which a refund is kept under sub-section (11), the taxable individual will, notwithstanding anything included in section 56, be authorized to interest at the same rate not surpassing 6% as notified on the department’s recommendations, if as a result of the plea or additional proceedings, he becomes skilled for refund.”

The debate might not end as going forward the government might examine the particular that-

- Section 49(3) mandates that the amount available in ECL is used for tax payment etc. Section 39 demands that the GSTR-3B must be filed after ‘payment’ of taxes via using the amounts available in ECL and Electronic Credit Ledger. The final payment is incurred post-filing GSTR-3B and Interest is for tax paid after the due date.

Read Also: Recent High Court Ruling on GST Return Mismatch Cases

Section 49 (3) expresses that the amount available in the electronic cash ledger might be utilized to make any payment for the tax, interest, penalty, fees, or any other amount liable to get paid under the provisions of this Act or the rules made thereunder in a way and subject to these conditions and in a time as may be specified.

- Rule 61(1) of CGST Rules furnishes that every individual should file his GSTR-3B return within the 20th of the month as mandated under Section 39 of the CGST Act. Rule 61(2) demands that at the time of filing the GSTR-3B, the tax will only be released.

Rule 61(1) and 61(2) state as under

Rule 61 (1) Every registered individual will provide the return in FORM GSTR-3B, electronically via the common portal directly or via the Facilitation Centre notified through the Commissioner, as defined under

(2) Every person enrolled needed to provide the return, under sub-rule (1) will, subject to the provisions of section 49, release his obligation for tax, interest, penalty, fees or any other amount liable to be paid under the Act or the provisions of this Chapter through debiting the electronic cash ledger or electronic credit ledger and possess the information in the return in FORM GSTR-3B.