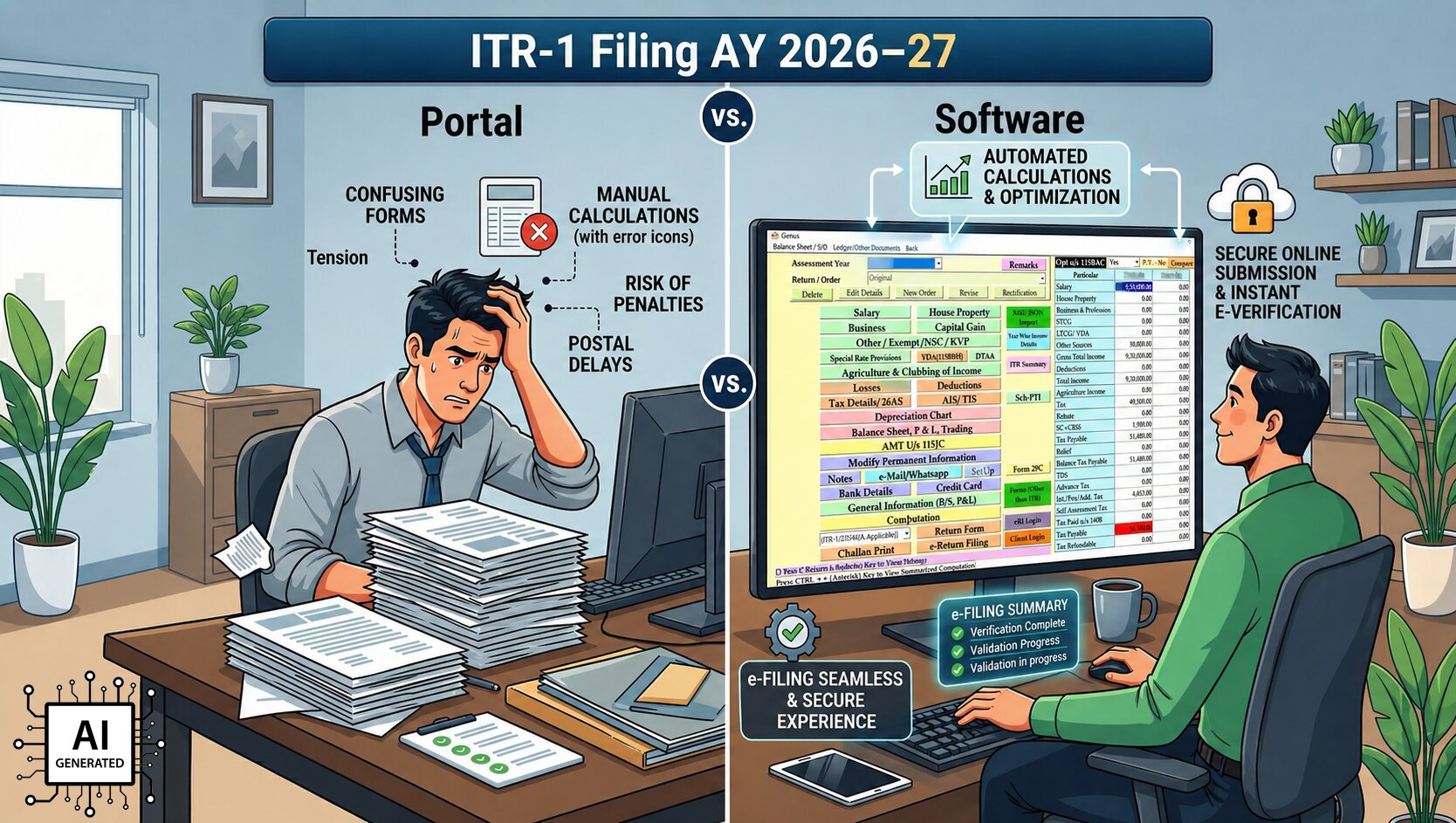

The ITR-1 (Sahaj) form for AY 2026-27 introduces several important updates to simplify return filing and expand eligibility. However, these changes also bring new reporting responsibilities for taxpayers.

Understanding how these updates work in portal-based filing versus software-based filing can help you choose the best approach and avoid errors.

Allow Two House Properties

Portal: For AY 2026-27, the ITR-1 form now allows reporting of up to two house properties instead of one. In portal filing, taxpayers must calculate income or loss separately for each property, including interest on housing loans and municipal taxes. They must also ensure that the total income remains within the ₹50 lakh limit to stay eligible for ITR-1. Any mistake in calculation may lead to incorrect tax liability or rejection.

Software: Professional software automatically handles multiple house property entries. It calculates income, applies deductions, and adjusts losses in accordance with tax rules. The system also checks eligibility limits in real time, ensuring the taxpayer continues to qualify for ITR-1 without manual verification.

Also Read: How ITR Software Eases HRA Calculation for Tax Year 2026-27

LTCG Up to INR 1.25 Lakh Allow Under Section 112A

Portal: Taxpayers can now report Long-Term Capital Gains (LTCG) of up to ₹1.25 lakh in ITR-1. However, portal filing requires careful entry of capital gains details and an understanding of applicable exemptions. Navigating new schedules and ensuring correct tax treatment can be complex, especially for first-time investors.

Software: The IT software simplifies capital gains reporting by auto-calculating LTCG based on imported data or user inputs. It also alerts users if gains exceed ₹1.25 lakh and suggests switching to ITR-2, preventing incorrect form selection and compliance issues.

Improve Validation and Compliance

Portal: With more validations introduced in the ITR utility and portal, taxpayers must carefully cross-check entries such as PAN, Aadhaar, bank details, and TDS information. Errors can lead to notices or a defective return status.

Software: The software performs real-time validation checks and cross-verifies data with Form 26AS, AIS, and TDS records. It minimises the chances of mismatches and ensures accurate filing.

Capital Gains Reporting

Portal: The revised format reduces some complexity but still requires taxpayers to understand the updated reporting structure. Portal users must ensure correct classification and avoid duplication or incorrect disclosures.

Software: It also incorporates updated formats and automatically maps entries to the correct fields. This reduces confusion and ensures compliance with the latest reporting structure without requiring deep technical knowledge.

New Data Fields (Secondary Address)

Portal: The updated ITR-1 includes new fields such as a secondary address and expanded personal information sections. While filing on the portal, taxpayers must carefully input all additional details, increasing the time required and the risk of missing mandatory fields.

Software: It automatically organises and validates personal data. It prompts users to fill in required fields and avoids incomplete submissions by flagging missing or inconsistent information.

Tax Regime Selection

Portal: Taxpayers can choose between the old and new tax regimes while filing. On the portal, they must compute tax liability under both regimes separately to determine the better option, which can be time-consuming and prone to errors.

Software: Tax software automatically compares tax liability under both regimes and suggests the most beneficial option. This ensures optimal tax savings without requiring manual calculations.

E-Filing Experience

Portal: Portal filing is suitable for very simple cases, but becomes increasingly complex as new changes are introduced. It requires tax knowledge, careful calculations, and multiple checks to avoid errors.

Software: It provides a guided, automated, and error-free experience. It adapts to new changes instantly and ensures compliance, making it ideal for both professionals and individuals with slightly complex income structures.

Conclusion: The changes in ITR-1 for AY 2026-27 make the form more inclusive but also slightly more complex in terms of reporting. The portal filing remains a free option but demands accuracy, time, and tax knowledge. The best income tax software offers automation, validation, and ease of use, significantly reducing errors.