GSTR 9, based on Table 8A, is a significant section for taxpayers, as it has auto-populated features and eligible ITC details for the complete financial year, derived from the relevant GSTR 2A/2B return. Also, note that the left-out section’s columns and fields in Table 8 are to be filled up with the complete analyses of the taxpayer. One must keep track of multiple things to make a note of GSTR 9 Table 8A.

It includes the details of inward supplies, and means of Inward supplies can be attached to the purchases made with the services received from SEZs, but excludes imports and inward supplies liable to reverse charge.

Latest Update

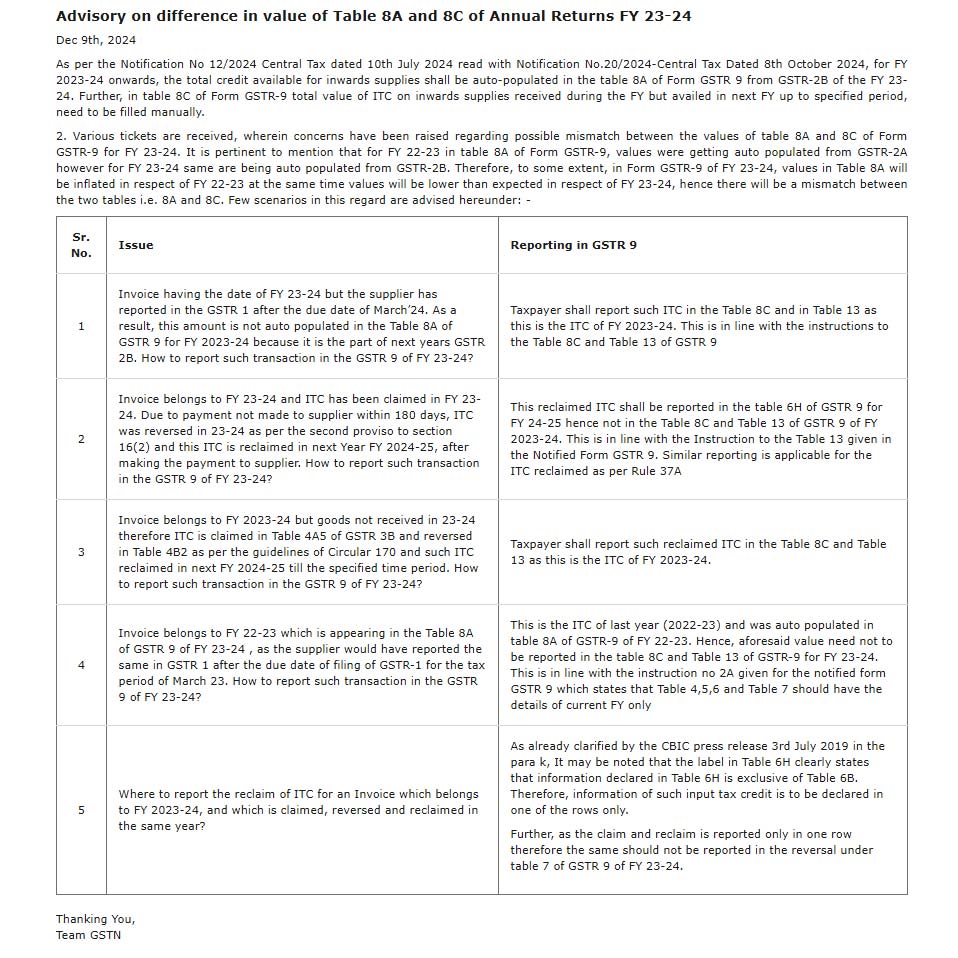

- The new GSTR-9 advisory is for reporting mismatches between Table 8A and 8C values. View more

Download GSTR 9 Filing Software

Know About Table 8A in GSTR-9

Table 8A is the yearly Form GSTR-9 return, which presents the information on the total input tax credit (ITC) available in the fiscal year from the inward supplies. The inward supplies consist of all purchases made along with the services obtained through SEZs; however, they do not include imports, and inward supplies are subject to reverse charge.

Table 8A Data Population in GSTR-9

Upon the grounds of Tables 3 and 5 of Form GSTR-2A/2B from FY 2024-25, data will be auto-populated from GSTR-2A/2B. The ITC data shall be auto-populated in this table. This is auto-populated from the return furnished every month through the business entity’s suppliers in their Form GSTR-1. It indeed consists of the tax credits circulated through the non-resident suppliers in Form GSTR-5.

The GST portal provides the choice to download the break-up of Table 8A data in an Excel file to the assessee. As soon as the assessee logs in to his account, he is required to coordinate with Form GSTR-9 (Prepare Online), and then tap on the button titled ‘Download Table 8A Document Details’. A downloaded folder is a zipped one. Unzip the folder to extract the file. Towards the case in which there is much more information, then distinct hyperlinks shall be furnished next to the button.

The assessee shall be enabled to see the invoice-wise information and reconcile that through their enrolled purchases. The document-wise information shall show all the documents like B2B, B2BA, CDNR, and CDNRA written in the Excel file of Table 8A, which shall indeed show the mentioned information:

- The time when the document is reported in Form GSTR-2A/2B.

- The filing information where the invoice was uploaded in the supplier’s GSTR-1 return.

- The reason shall not be acknowledged if the invoice does not consider Table 8A data.

- When the buying is executed via an e-commerce operator, then the GSTIN of the e-commerce operator shall be prompted.

- The invoice type is indeed written like ‘R’ for regular supplies, ‘SEZWP’ for SEZ supplies with payment of tax, ‘SEZWOP’ for SEZ supplies excluding the payment of tax, and others.

Table 8A Reconciling of Data While Filing GSTR-9 Form

Table 8A inside the GSTR-9 shows all the ITC data towards the specific fiscal year. The correct reporting of the ITC information in Table 8A assists the assessee in availing the ITC towards the same fiscal year. The same table can not be edited, that pointed towards the fact that, even if the ITC amounts mentioned are not correct, the assessee is not able to edit it to insert the accurate amounts.

GSTR-9, when furnished, could not be amended. ITC settlement is an important factor for the assessee to lessen their tax liability at the effective level. The assessee can settle ITC on an invoice-wise level through the information in Table 8A and the document-wise breakup. It indeed assists the business entities’ auditor in reporting the mismatches in ITC, besides making the yearly settlement in Form GSTR-9C.

Towards claiming the ITC, Table 8A is crucial. If the amount of ITC revealed in Table 8A is lower with respect to the ITC reported in Form GSTR-2A/2B or the books of accounts, then the assessee shall urge to finish filing the tax liability because of no mistake from his side.

Reasons for Data Mismatch Between Table 8A and GSTR-2A

Various causes revealed why the data reported in Table 8A of the GSTR-9 is not similar to the information reported in Form GSTR-2A/2B. There are the points mentioned below:

- Invoices get saved or furnished in the supplier’s Form GSTR-1, however, they are not furnished yet. The GSTR-2A/2B shall be shown in the status “Not yet filed” for these invoices. Such a difference is not visible between GSTR 2A/2B & Table 8A.

- After the cut-off date, GSTR-1 is furnished by the supplier. The cut-off date is said to be the date after which no information shall be acknowledged towards the Table 8A computation.

- If the supplier has furnished the invoice in his GSTR-1, however, he is at fault that the supply is for the reverse charge, then this shall not get recognised in table 8A of the recipient.

- When the GSTIN of the recipient get faulty changed, then the ITC shall be available toward the changed GSTIN.

- ITC does not get included in Table 8A if the place of supply (POS) comes under the identical state of the supplier and not the recipient. However, the same information shall be shown in GSTR-2A/2B.

- If the date of the document is under the period when the assessee was under the composition scheme, then the ITC concerning the mentioned purchases shall not be acknowledged in Table 8A.

Apart from the above, the ITC might not get matched between the ITC reported every month in GSTR-2A/2B and the original ITC recorded in the assessee’s books of accounts. The cause for that can be:

- Instability in the invoice number convention within the original invoices and the data reported in the GSTR-2A/2B.

- Mismatches in the invoice date format.

- Mismatches in the return duration because of the invoice furnished in a specific month and reported or furnished in a distinct month.

- Invoices were issued to an incorrect GSTIN for the same vendor.

Difference Between GSTR-3B Vs GSTR-1

The GSTR-3B Vs. GSTR-1 Comparison Report provides the assessee with information on the differences between the GSTR-3B and GSTR-1 returns furnished concerning the outward tax, outward taxable value, supplies under the Reverse Charge Mechanism in both returns and others. The assessee could opt for the action on the grounds of a monthly, quarterly, or annual basis by distinguishing the information at the GSTIN level or cumulatively on the PAN level.

Difference Between GSTR-3B Vs GSTR-2A/2B

GSTR-3B Vs. GSTR-2A/2B undergoes an important practice that a business should hold on to so that it does not forget to claim the ITC. It not only assists in claiming the correct ITC for trades but also in reversing any excess ITC availed. It shall assist in preventing the demand notices sent from the tax council. SAG Infotech helps in the simpler settlement of the information between Table 8A of the GSTR-9 and the purchase records. Through the assistance of our Advanced Reconciliation Tool, one cannot forget to avail the ITC on any invoice. Just secure time and taxes, and make sure that there is 100% precision during the furnishing of GSTR-9.

Steps to Provide GSTR 9 Table 8A Under GSTR-2A/2B

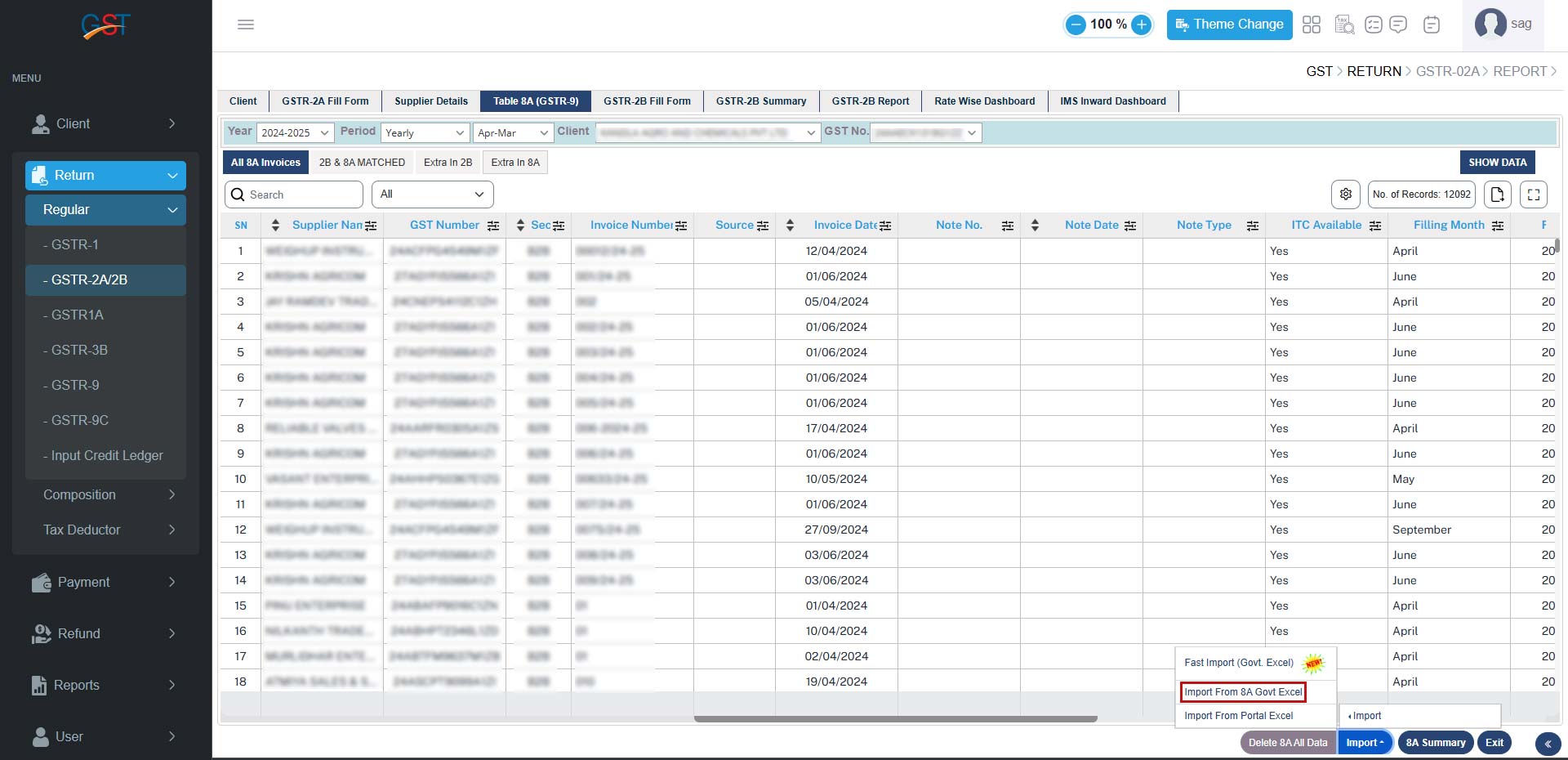

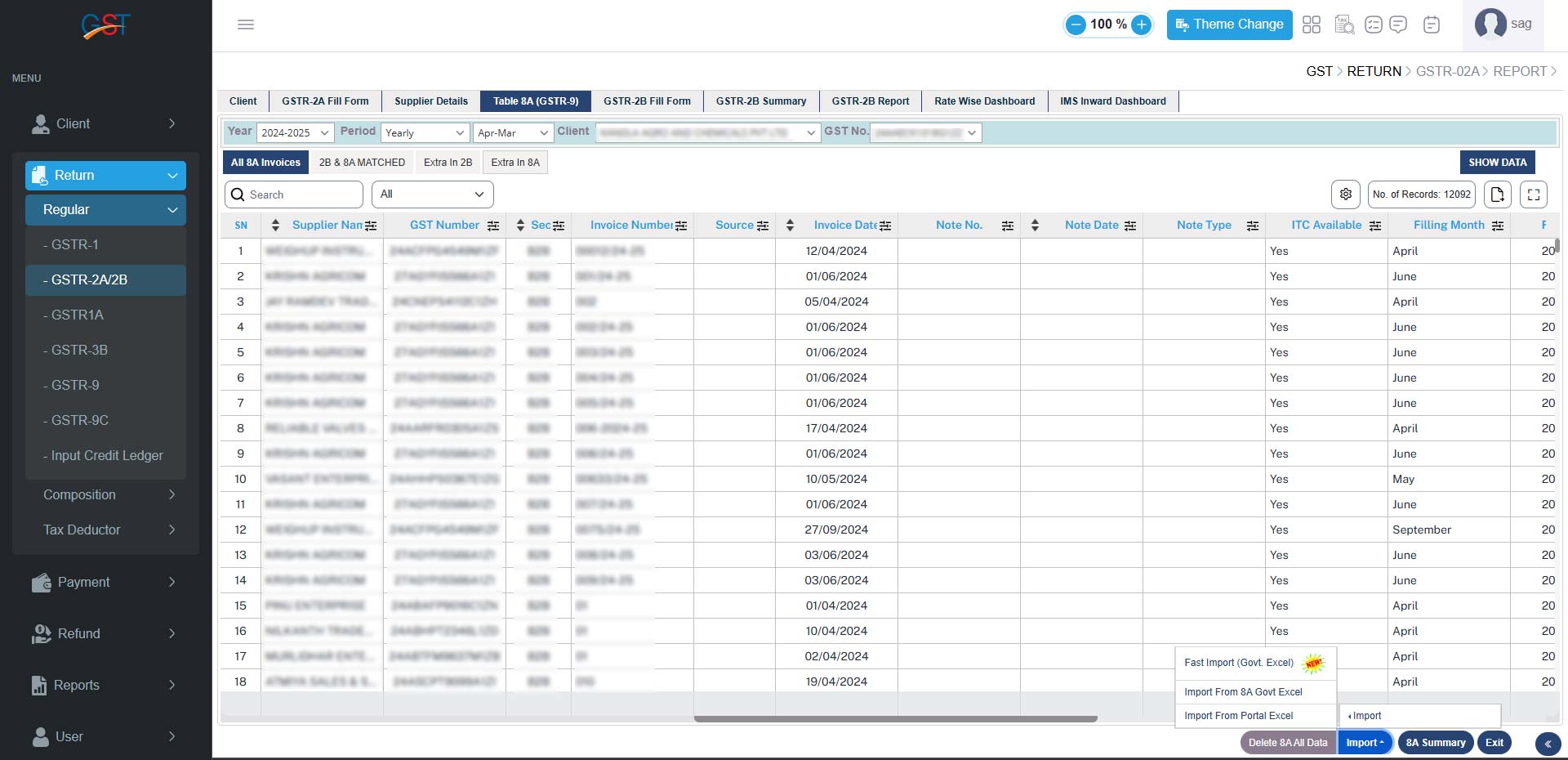

Step 1: Path to goto GSTR-2A/2B is Return==> Regular==>GSTR-2A/2B==>Table 8A (GSTR-9).

Step 2: The first step is to import Table 8A data into the software, which you have already downloaded from the GST portal.

- Alternatively, you can now directly download GSTR 9 Table 8A data from the portal into the software. To do this, simply click on the ‘Import’ button, then select ‘Import from Portal Excel’ and ‘Fast Import (Govt Excel)’.

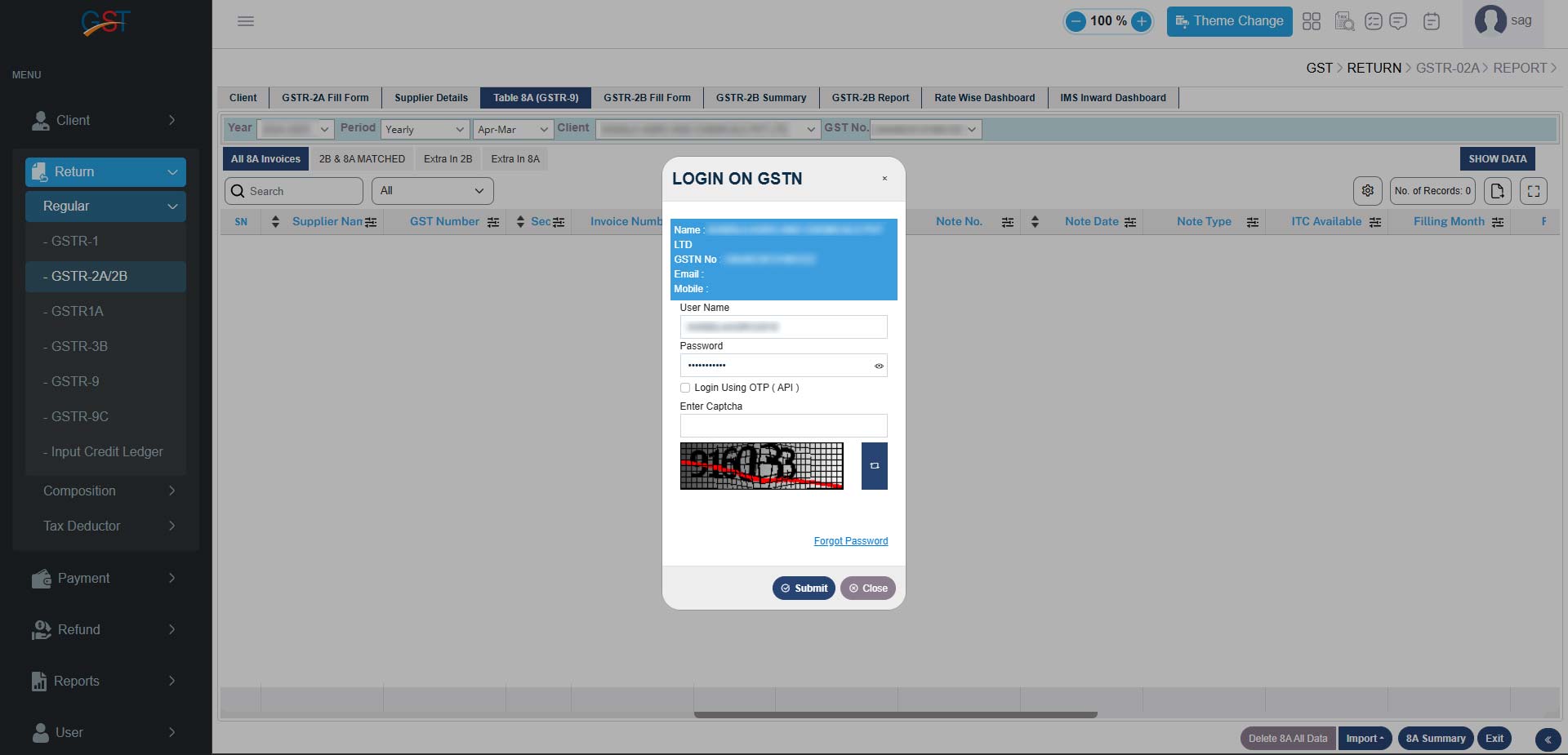

- After that, enter your Login details, & Then the captcha

- After that, the data automatically comes into the software from the GST portal

- After that, click on ‘Import data’ to save the data into the software

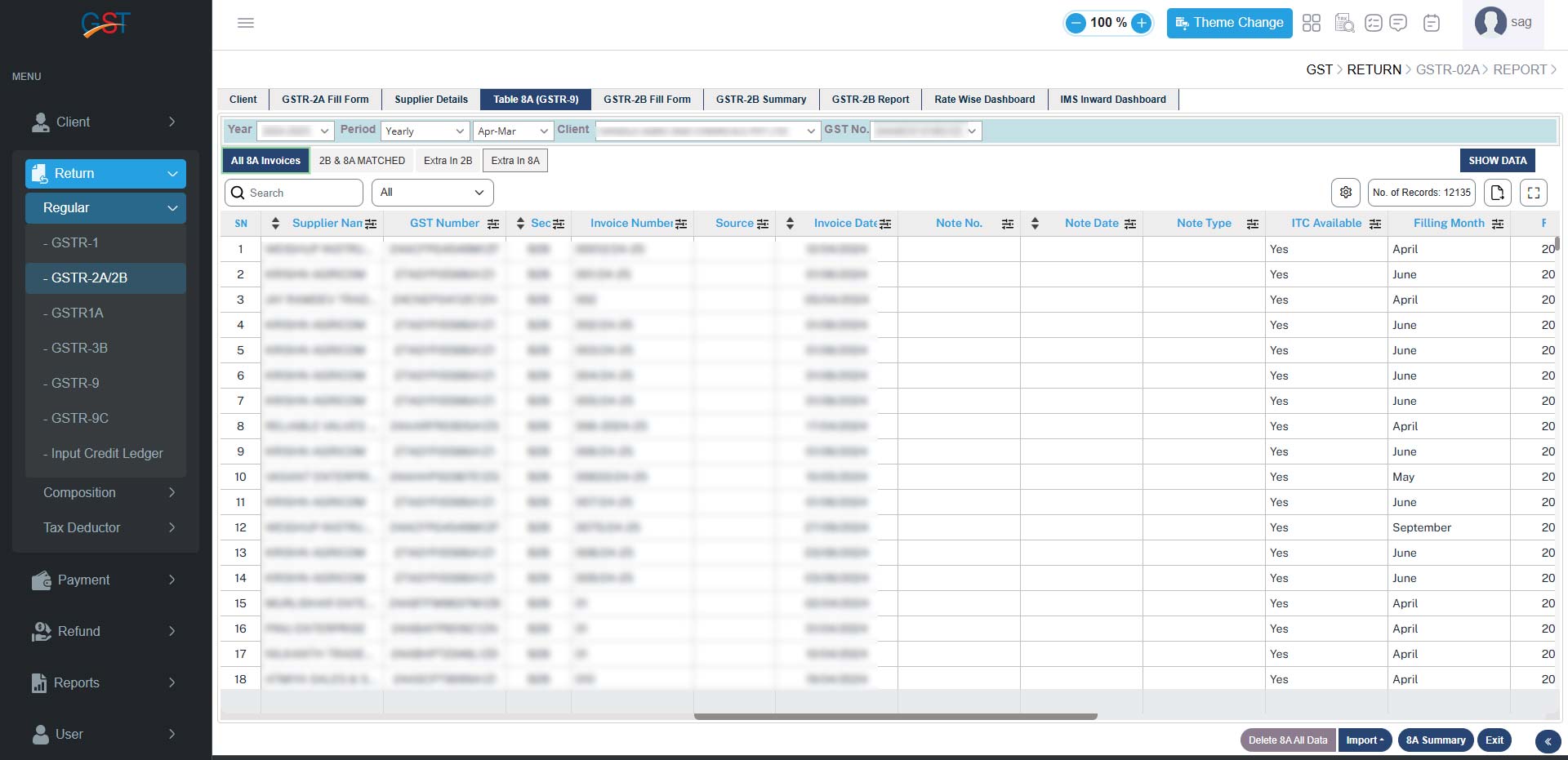

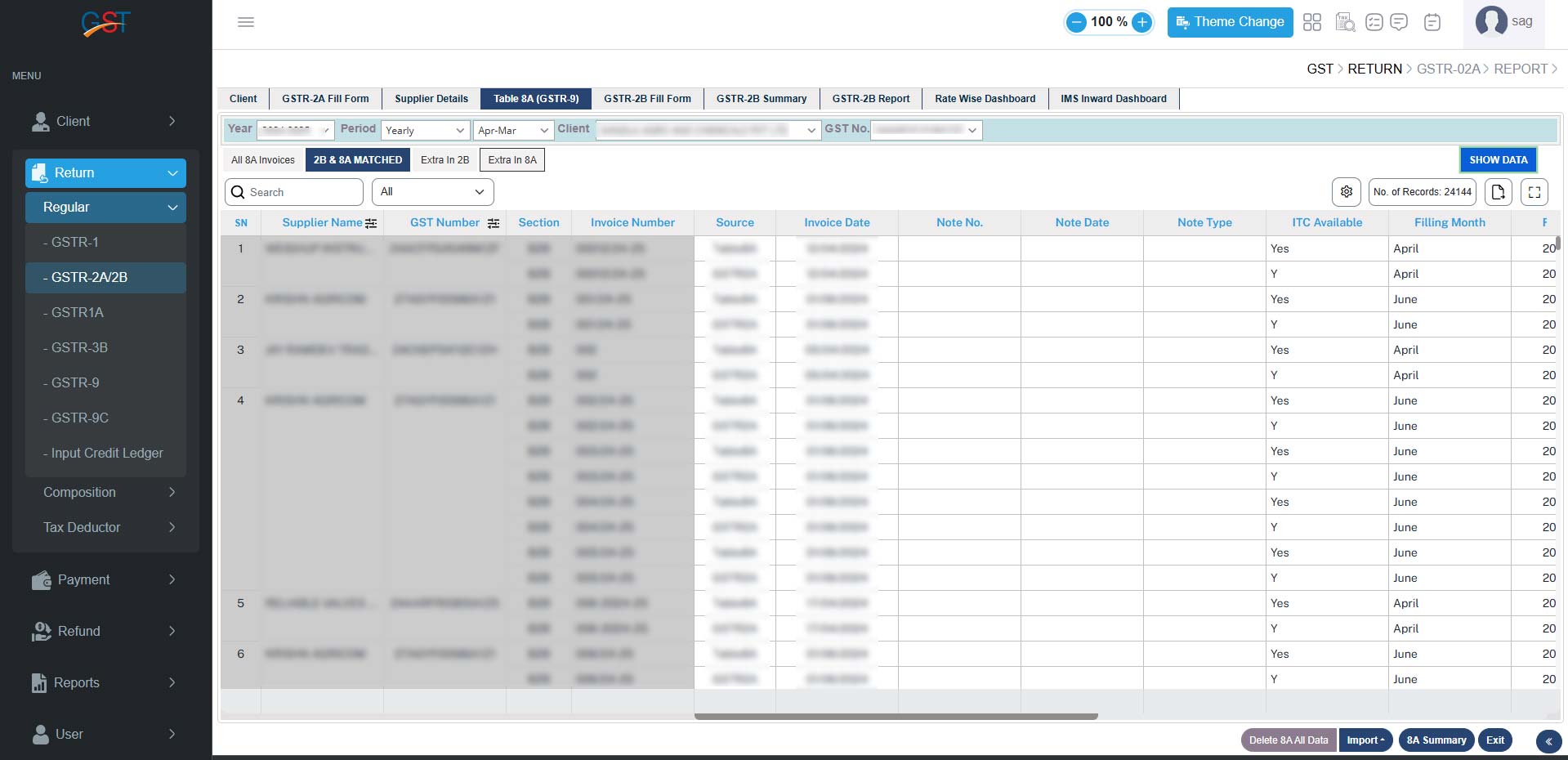

Step 3: After importing all Table 8A data, come under ALL 8A Invoices like this.

Step 4: The second tab is the GSTR-2A return & Table 8A matched

Step 5: In this table, common data coming from GSTR-2A & Table 8A will be displayed

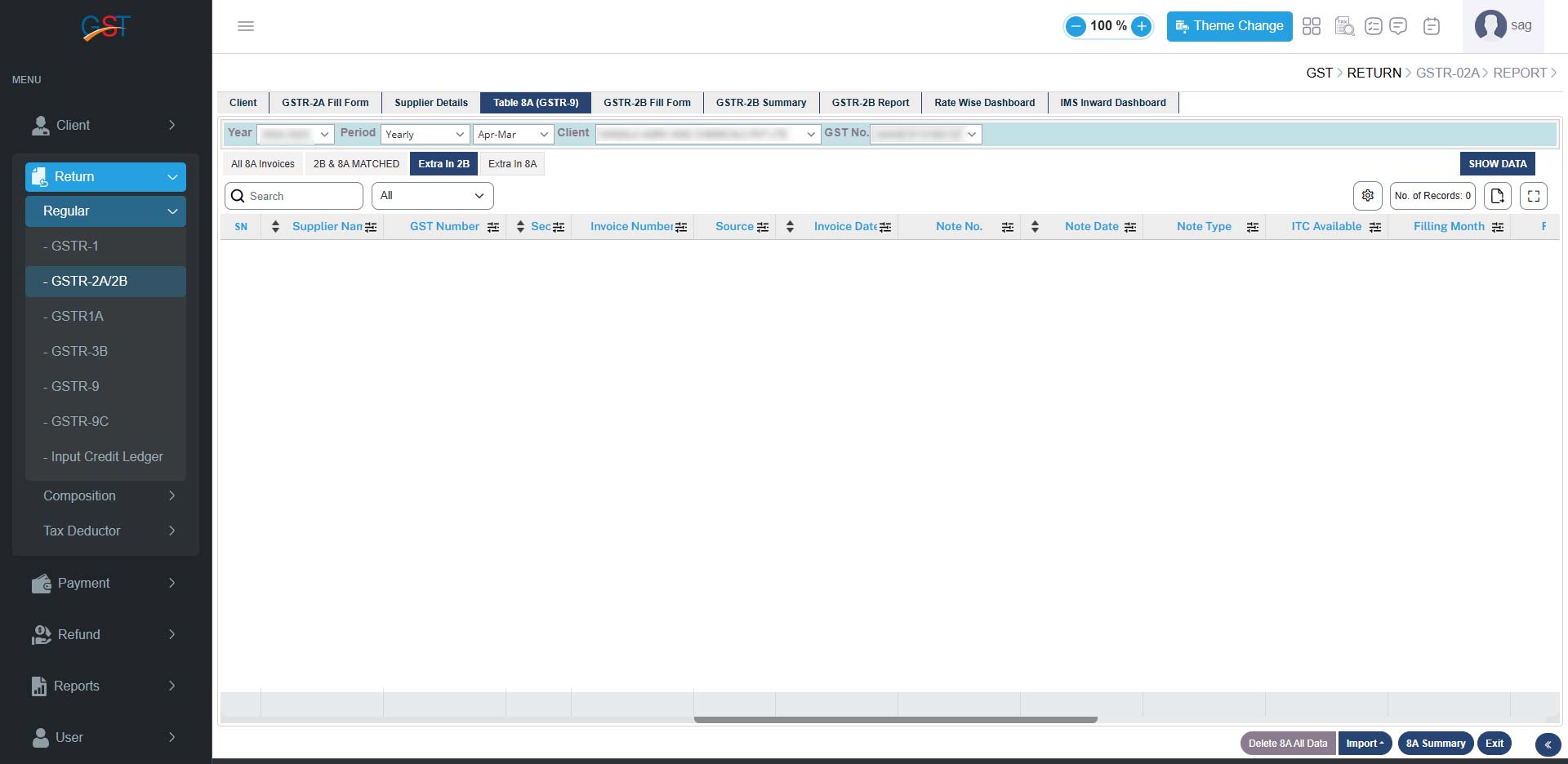

Step 6: After that, the extra in the GSTR-2A data table comes.

Step 7: It contains the Previous year data/ Current Year data with CFS-NO/ Current Year data after the cut-off date.

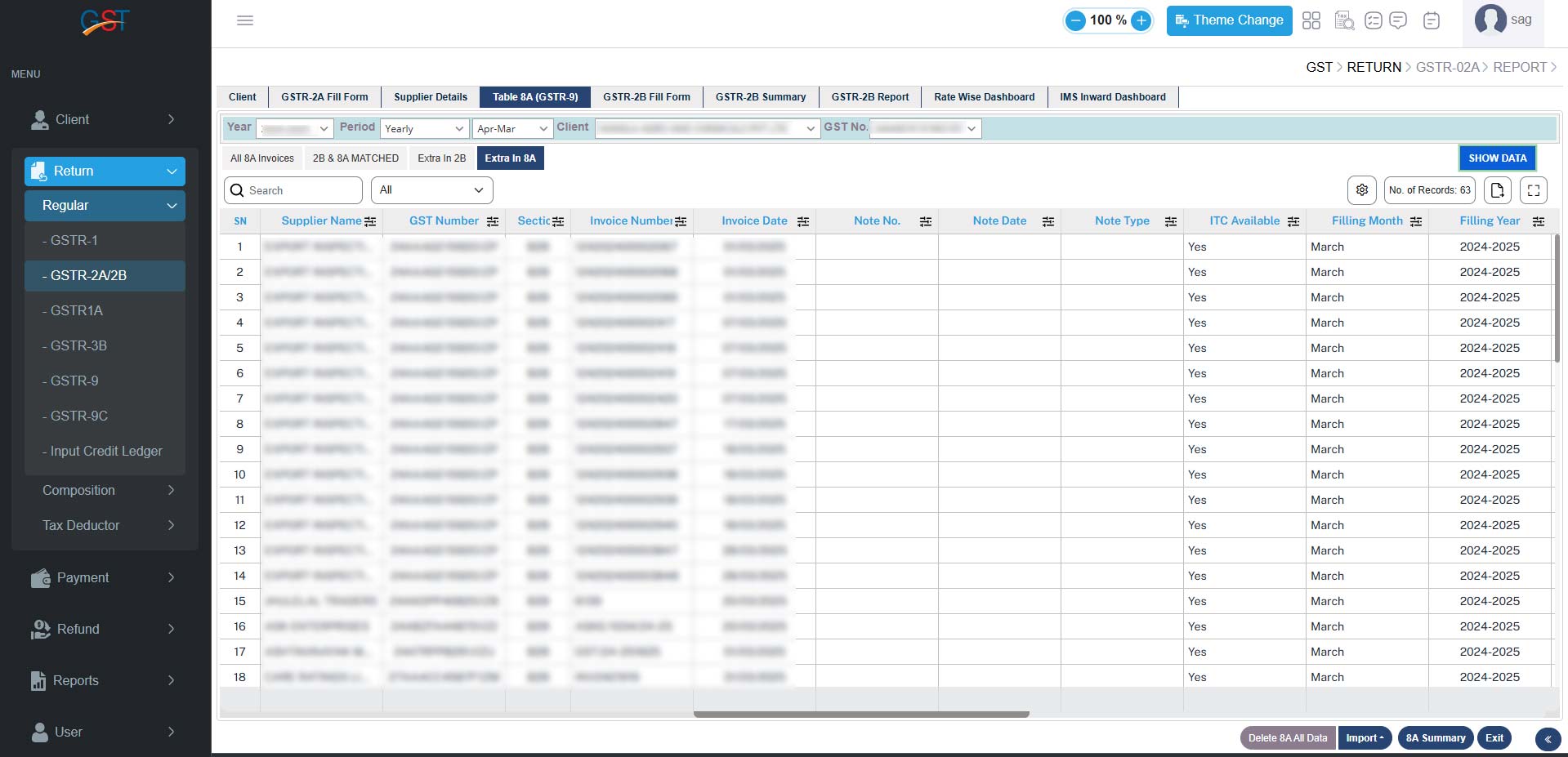

Step 8: And the last one is Extra in Table 8A

Step 9: It contains the Current Year data/ Current Year data in the next year, i.e. from 1-Apr 2025 to the cut-off date.

Step 10: And at the bottom, you will find Table 8A summary. Here, you get Section-wise ITC according to Eligibility. And that’s all about Table 8A of GSTR-9

{kind=link}