The Himachal Pradesh High Court said that the State and Central Governments have expanded the identical powers under the CGST and SGST Act and if any officer has begun proceedings then it cannot be transferred to another and he would be needed to issue process under the Act and ended logically.

The Bench of Justice Tarlok Singh Chauhan noted that “….where a proper officer under the CGST Act had initiated proceedings on a subject matter, no proceedings would be initiated by a proper officer authorized under the SGST Act or UGST Act on the same subject matter.”

It has been furnished under section 6(1) of the CGST Act, 2017 that State and Union Territory tax officers can act as proper officers under the same act, following the specifications mentioned under the Government based on Council recommendations.

Additionally, Section 6(2)(a) of the CGST Act, 2017 furnishes that when the proper officer furnishes an order under the act then he would indeed furnish an order under the SGST or the UGST Act, and notify the pertinent State or Union Territory tax officer.

Furthermore, Section 6(2)(b) of the CGST Act, 2017 furnishes that a proper officer under the SGST Act and UGST Act begin the proceedings on a subject matter, under the act the proper officer should not start proceedings, on the identical subject matter.

The statute has been laid down by section 70 of the CGST ACT 2017 for the power of the officer to summon any individual before them to furnish proof in the form of documents for any particular manner.

Case Facts

Summons Section 70 of the HP-GST/CGST Act, 2017 was been issued to the assessee/petitioner by the Department of State Taxes & Excise (Respondent No. 1) to provide documents to show the genuineness of the transactions with the suppliers. The taxpayer furnishes all the documents sought under the Department of State Taxes & Excise.

However, the Director General of GST Intelligence, Rohtak (Respondent No. 2) issued another summons for the same suppliers. The taxpayer notified DGGI, Rohtak that the proceedings for those suppliers were in progress with the Department of State Taxes & Excise and that documents had been furnished accordingly. Despite this, DGGI, Rohtak blocked the Input Tax Credit of the taxpayer. Rohtak the assessee aggrieved by the action of DGGI, has filed a writ petition to the Himachal Pradesh High Court.

High Court Observations

It was mentioned by the bench that a proper officer under the CGST Act had started the proceedings on the subject matter, proper officer who was authorized under the SGST Act or UGST Act did not commence the proceedings on the same subject matter.

The bench after directing to the Circular issued via the Ministry of Finance/ Department of Revenue on 05.10.2018, mentioned that the central government has regarded that after the action of an officer of the State authority, the proper officer shall need to conduct further proceedings under the Act.

Read Also: Govt of HP Divides Excise and GST Wings to Improve Efficiency in Departments

“The State and Central Governments have been extended the same powers under the CGST and SGST Act and if one of the officers has already initiated proceedings, the same cannot be transferred to another and he alone is to issue process under the Act and take it to its logical end”, bench mentioned.

It was concluded by the bench that the term ‘subject matter’ used in Section 6(2)(b) of the CGST Act refers to ‘the nature of proceedings.’ Thus, it signifies that if proceedings have been initiated before by respondent No. 1 (Department of State Taxes & Excise), respondent No. 2 (DGGI, Rohtak) cannot initiate proceedings for the same subject matter. Permitting such action would be disobedient to the provisions of Section 6(2)(b) of the CGST Act.

The bench in the above-said matter permitted the appeal.

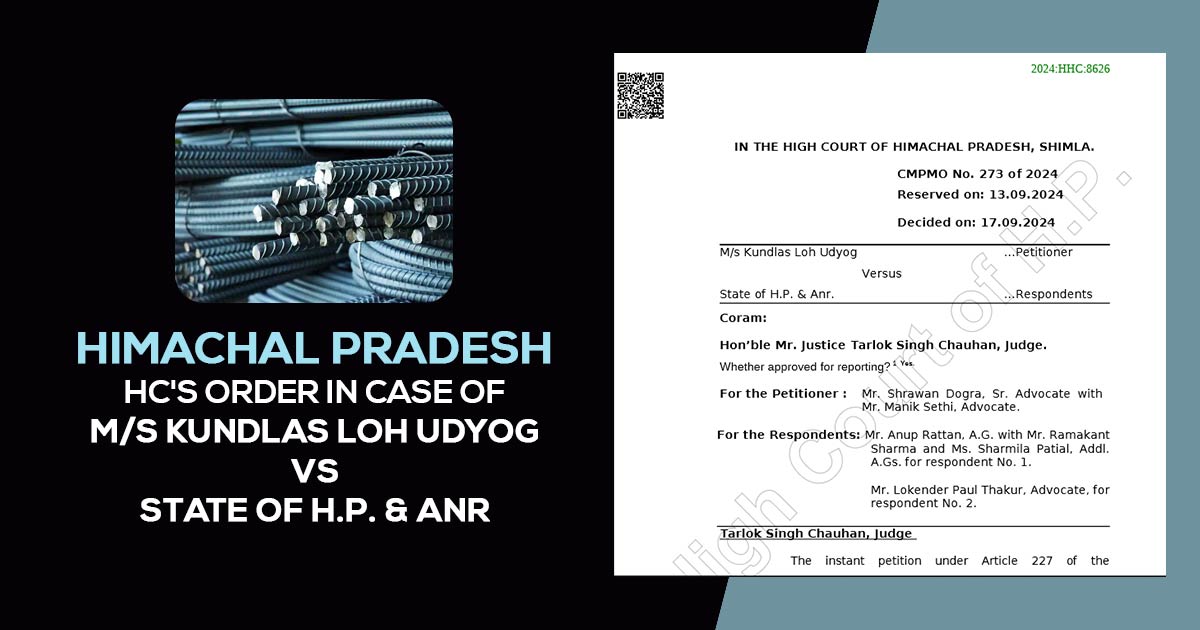

| Case Title | M/s Kundlas Loh Udyog Versus State of H.P. & Anr. |

| Citation | CMPMO No. 273 of 2024 |

| Date | 17.09.2024 |

| For Petitioner | Mr Shrawan Dogra, Mr Manik Sethi |

| For Respondents | Mr Anup Rattan, Mr Ramakant Sharma, Ms Sharmila Patial, Mr Lokender Paul Thakur |

| Himachal Pradesh High Court | Read Order |