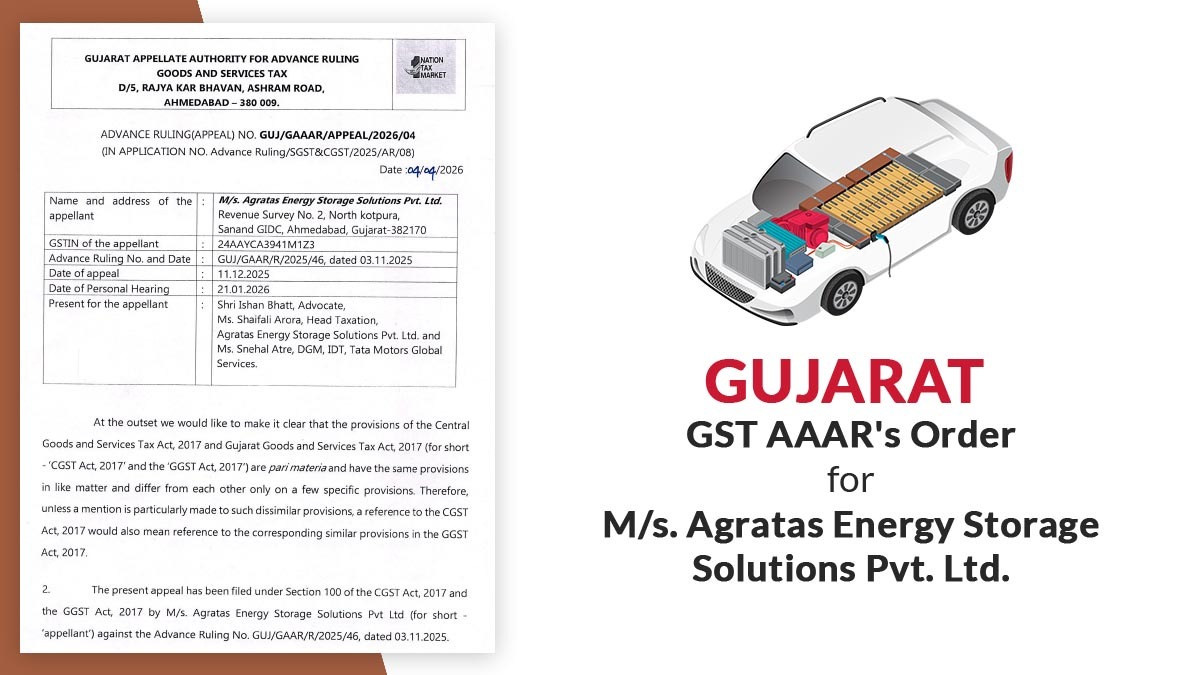

The Gujarat Appellate Authority for Advance Ruling (GAAAR), in a ruling, has dismissed an appeal, reaffirming that Input Tax Credit (ITC) on Goods and Services Tax(GST) paid for annual lease rentals of industrial land allotted by the Government of Gujarat is not considerable u/s 17(5)(d) of the Central Goods and Services Tax Act, 2017.

The applicant, Agratas Energy Storage Solutions Pvt. Ltd had entered into a 50‑year lease agreement with the state government for nearly 321 acres of land. As per the agreement, Agratas was required to pay annual lease rent at 6% of the market value, with a 10% escalation every 5 years.

Agratas approached the Gujarat Authority for Advance Ruling (GAAR), asking for clarification on whether ITC could be claimed on GST paid under the RCM for lease rentals both before and after construction of its factory, and for vacant or green‑belt portions of the land.

The GAAR, in its order dated 03 November 2025, held that ITC was blocked u/s 17(5)(d), which restricts credit on goods or services utilised for the construction of immovable property. The authority said that the objective of the leased land was industrial construction and therefore fell within the restriction.

The applicant was not satisfied with that and submitted the appeal u/s 100 of the CGST Act, claiming that the lease was not “for construction” and is for industrial usage and that the term must be interpreted narrowly, which includes only materials directly used in construction, not land‑related services.

The company put reliance on Supreme Court precedents, including CCE v. TELCO (2003), and stated that refusing GST ITC on annual lease payments while exempting upfront premiums under Notification No. 12/2017‑CT (Rate) established an unfair difference.

The Appellate Authority, after hearing the case, including Arti Kanwar (SGST) and Sunil Kumar Mall (CGST), upheld the findings of GAAR. It mentioned that both upfront premiums and annual lease rentals have a different nature, the former being a capital payment, the latter a revenue expense, and that the legislature deliberately chose to exempt only upfront premiums.

The bench said that the land was leased for the construction of a factory, which makes the GST paid on these lease rentals ineligible for ITC.

Also Read: How GST Software Handles Input Tax Credit (ITC) Tracking

The authority rejected the claim that ITC must be permitted for vacant or green‑belt areas, arguing that such portions form part of the industrial project. Hence, it is included under the same restriction.

Subsequently, the appeal was dismissed.

| Case Title | M/s. Agratas Energy Storage Solutions Pvt. Ltd. |

| Case No | GUJ/GAAAR/APPEAL/2026/04 |

| GSTIN | 24AAYCA3941M1Z3 |

| Present for the Appellant | Shri Ishan Bhatt, Ms Shaifali Arora, Ms Snehal Atre |

| Gujarat AAAR | Read Order |