The ITR-6 Form for Income Tax Return filing with the IT department of India is meant for only those companies that are not claiming exemption u/s 11 (Income from property held for charitable or religious purposes).

Get a Demo of Gen IT Software for ITR 6 Form

Who Can File the ITR 6 Form?

ITR-6 can be used by companies that are not claiming exemption u/s 11 (Income from property held for charitable or religious purposes).

Who is Not Eligible to File the ITR 6 Form?

Taxpayers who are not liable to file for the ITR-6 Form are mentioned below.

- Individuals, Hindu Undivided Family (HUF), Firm, Association of Persons (AOP), Body of Individuals (BOI), Local Authority and Artificial Judiciary Person

- Companies that claim an exemption under section 11 (Income from property held for charitable or religious purposes)

What are the Eligibility Criteria for Filing ITR-6 Form?

The companies that are registered under the Indian Companies Act of 1956 or any other law are eligible to file the ITR-6 Form if they are not claiming exemption u/s 11 (Income from property held for charitable or religious purposes)

Read Also: Complete Guide to File ITR 4 Sugam Form Online

What is the Last Date for Filing ITR-6 Form FY 2026-27?

- AY 2026-27 – 31st October 2026

- AY 2025-26 –

31st October 202510th December 2025 | 30th November 2025 (This date is approaching for companies that do global commerce or individual domestic arrangements to propose a detailed report called Form 3CEB, which connects to how they price their trades between various organisations.) - AY 2024-25 – 31st October 2024 | 15th November 2024 (Revised)

- AY 2023-24 – 31st October 2023

Note: ITR-6 form corrigendum via Notification No. 61/2026. Read More

Let’s Go for Online ITR 6 Filing Guide

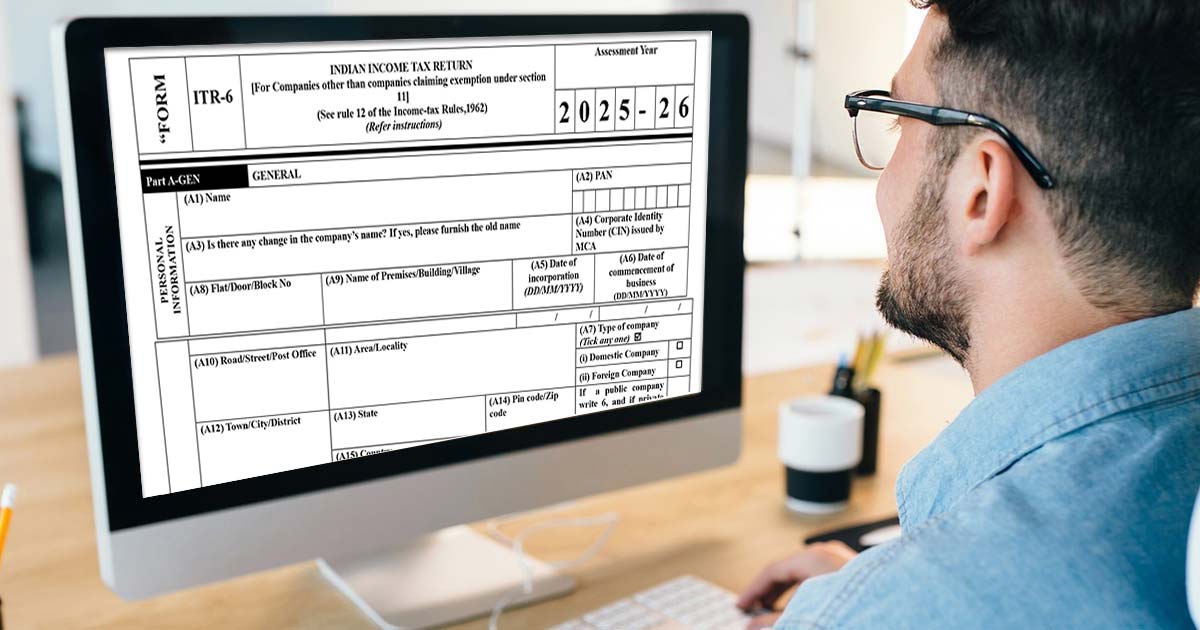

Part A-GEN General:PERSONAL INFORMATION

- (A1) Name

- (A2) PAN

- (A3) Is there any change in the company’s name? If yes, please furnish the old name

- (A4) Corporate Identity Number (CIN) issued by MCA

- (A5) Date of incorporation (DD/MM/YYYY)

- (A6) Date of commencement of business (DD/MM/YYYY)

- (A7) Type of company (Tick any one)

- (i) Domestic Company

- (ii) Foreign Company

- (A8) Flat/Door/Block No

- (A9) Name of Premises/Building/Village

- (A10) Road/Street/Post Office

- (A11) Area/Locality

- (A12) Town/City/District

- (A13) State

- (A14) Pin code/Zip code If a public company write 6, and if private company write 7 (as defined in section 3 of The Companies Act)

- (A15) Country

- (A16) Office Phone Number with STD code/ Mobile No. 1

- (A17) Mobile No. 2

- (A18) Email Address-1 Email Address-2

- (A19) (ai) Due date for filing return of income [Dropdown to be provided]:

- 31st October

- 30th November

FILING STATUS

- (A19)(aii)

- 1 Filed u/s (Tick)[Please see instruction ]

- 139(1)- On or Before due date

- 139(4)- After due date

- 139(5)- Revised Return

- 92CD-Modified return

- 119(2)(b)- After condonation of delay

- 170A- After order by the tribunal or court

- 2 Or filed in response to notice u/s

- 139(9)

- 142(1)

- 148

- 153C

- (b) If revised/ defective/Modified, then enter Receipt No and Date of filing original return (DD/MM/YYYY)

- (c) If filed, in response to notice u/s 139(9)/142(1)/148/153C or order u/s 119(2)(b) or order referred to in section 170A , enter Unique Number /Document Identification Number and date of such notice/order, or if filed u/s 92CD enter date of advance pricing agreement

- (d) Residential Status (Tick) Resident Non-Resident

- (e) Have you opted for taxation under section 115BA/115BAA/115BAB? (drop down to be provided in efiling utility) (applicable on Domestic Company).

- If yes, please furnish the AY in which said option is exercised for the first time along with date of filing of relevant form (10-IB/ 10-IC/ 10-ID) & acknowledgment number.

- If no, whether you are choosing to opt for taxation under section 115BA/115BAA/115BAB this year? (drop down to be provided in efiling utility)

- Please provide the date of filing of relevant form (10-IB/10-IC/10-ID) & acknowledgment number.

- (f) Whether total turnover/ gross receipts in the previous year 2022-2023 exceeds 400 crore rupees? (Yes/No) (applicable for Domestic Company)

- (g) Whether assessee is a resident of a country or specified territory with which India has an agreement referred to in sec 90

- (1) or Central Government has adopted any agreement under sec 90A(1)?

- (h) In the case of non-resident, is there a Permanent Establishment (PE) in India (Tick) Yes No

- (i) In the case of non-resident, is there a Significant Economic Presence (SEP) in India (Tick) Yes No please provide details of

- (a) aggregate of payments arising from the transaction or transactions during the previous year as referred in Explanation 2A(a) to Section 9 (1)(I)

- (b) number of users in India as referred in Explanation 2A(b) to Section 9(1)(i).

- (j) Whether assessee is required to seek registration under any law for the time being in force relating to companies? If yes, please provide details.

- Act under which registration required

- Date of Registration (DD/MM/YYYY) Registration Number

- (k) Whether the financial statements of the company are drawn up in compliance to the Indian Accounting Standards specified in Annexure to the companies (Indian Accounting Standards) Rules, 2015 (Tick) Yes No

- (l) Whether assessee has a unit located in an International Financial Services Centre and derives income solely in convertible foreign exchange? (Tick) Yes No

- (m) Whether the assessee company is under liquidation (Tick) Yes No

- (n) Whether you are an FII / FPI? Yes/No If yes, please provide SEBI Regn. No.

- (o) Whether the company is a producer company as defined in Sec.581A of Companies Act, 1956? Yes No

- (p) Whether this return is being filed by a representative assessee? (Tick) Yes No If yes, please furnish following information –

- (1) Name of the representative assessee

- (2) Capacity of the Representative (drop down to be provided)

- (3) Address of the representative assessee

- (4) Permanent Account Number (PAN)/Aadhaar No. of the representative assessee

- (q) Whether you are recognized as start up by DPIIT Yes No

- 1 If yes, please provide start up recognition number allotted by the DPIIT

- 2 Whether certificate from inter-ministerial board for certification is received? Yes No

- 3 If yes provide the certification number

- 4 Whether declaration in Form-2 in accordance with para 5 of DPIIT notification dated 19/02/2019 has been filed before filing of the return? Yes No

- 5 If yes, provide date of filing Form-2

- (r) Legal Entity Identifier (LEI) details (mandatory if refund is 50 Crores or more)

- LEI Number

- Valid upto date

- (s) Whether you are recognized as MSME? Yes No

- If yes, please provide registration number allotted as per MSMED Act, 2006

Audit Information

- (a1) Whether liable to maintain accounts as per section 44AA? (Tick) Yes No

- (a2) Whether assessee is declaring income only under section 44AE/ 44B/ 44BB/ 44BBA/ 44BBB/ 44BBC/ 44D? (Tick) Yes No

- (a2i) If No, Whether during the year total sales/turnover/gross receipts of business is more than 1 Crore Rupees but does not exceed 10 Crore Rupees? (Tick) Yes No, turnover does not exceed 1 crore No , turnover exceeds 10 crores

- (a2ii) If (a2i) is Yes, whether aggregate of all amounts received, including amount received for sales, turnover or gross receipts or on capital account such as capital contribution, loans etc. during the previous year, in cash & non-a/c payee cheque/DD, does not exceed five per cent of said amount? (a2ii) (Tick) Yes No

- (a2iii) If (a2i) is Yes, whether aggregate of all payments made including amount incurred for expenditure or on capital account such as asset acquisition, repayment of loan etc., in cash & non-a/c payeecheque/DD, during the previous year does not exceed five per cent of the said payment

- (b) Whether liable for audit under section 44AB? (Tick) Yes No (Note to Systems: For cases where

- a2i exceeds INR 10 crores, this should be an automatic Yes)

- If Yes is selected at (b), mention by virtue of which of the following conditions:

- (bi) Sales, turnover or gross receipts exceeds the limits specified under section 44AB (Tick)

- (bii) Assessee falling u/s 44BB but not offering income on presumptive basis (Tick)

- (biii) Assessee falling u/s 44BBB but not offering income on presumptive basis (Tick)

- (biv) Others (Tick)

- (c) If (b) is Yes, whether the accounts have been audited by an accountant? (Tick) Yes No (If Yes, furnish the following information below)

- (1) Mention the date of furnishing of audit report (DD/MM/YYYY)

- (2) Name of the auditor signing the tax audit report

- (3) Membership No. of the auditor

- (4) Name of the auditor (proprietorship/ firm)

- (5) Proprietorship/firm registration number

- (6) Permanent Account Number (PAN/Aadhaar No.) of the auditor (proprietorship/ firm)

- (7) Date of audit report

- (8) Acknowledgement Number of the Audit Report

- (9) UDIN

- (di) Are you liable for Audit u/s 92E? Yes No

- (dii) If (di) is Yes, whether the accounts have been audited u/s. 92E? Yes No

- Date of furnishing audit report? DD/MM/YYYY

- Acknowledgement Number

- (diii) If liable to furnish other audit report under the Income-tax Act, mention whether have you furnished such report. If yes, please provide the details as under: ) (Please see Instruction 5)

- Sl. No.

- Section Code

- Date (DD/MM/YYYY)

- Acknowledgement Number

- (e) Mention the Act, section and date of furnishing the audit report under any Act other than the Income-tax Act

HOLDING STATUS

- (a) Nature of company (select 1 if holding company, select 2 if a subsidiary company, select 3 if both, select 4 if any other)

- (b) If subsidiary company, mention the details of the Holding Company

- PAN Name of Holding Company

- Address of Holding Company

- Percentage of Shares held

- (c) If holding company, mention the details of the subsidiary companies

- PAN Name of Holding Company

- Address of Holding Company

- Percentage of Shares held

BUSINESS ORGANISATION

- (a) In case of amalgamating company, mention the details of amalgamated company

- PAN

- Name of Amalgamated Company

- Address of Amalgamated Company

- Date of Amalgamation

- (b) In case of amalgamated company, mention the details of amalgamating company

- PAN

- Name of Amalgamated Company

- Address of Amalgamated Company

- Date of Amalgamation

- (c) In case of demerged company, mention the details of resulting company

- PAN

- Name of Amalgamated Company

- Address of Amalgamated Company

- Date of Amalgamation

- (d) In case of resulting company, mention the details of demerged company

- PAN

- Name of Amalgamated Company

- Address of Amalgamated Company

- Date of Amalgamation

KEY PERSONS: Particulars of Managing Director, Directors, Secretary and Principal officer(s) who have held the office during the previous year and the details of eligible person who is verifying the return.

- S.No.

- Name

- Designation

- Residential Address

- PAN/Aadhaar No.

- Director Identification Number (DIN) issued by MCA, in case of Director

SHAREHOLDERS INFORMATION: Particulars of persons who were beneficial owners of shares holding not less than 10% of the voting power at any time of the previous year

- S.No.

- Name and Address

- Percentage of shares held

- PAN (if allotted)

OWNERSHIP INFORMATION: In case of unlisted company, particulars of natural persons who were the ultimate beneficial owners, directly or indirectly, of shares holding not less than 10% of the voting power at any time of the previous year

- S.No.

- Name

- Address

- Percentage of shares held

- PAN/Aadhaar No. (if allotted)

In case of Foreign company, please furnish the details of immediate parent company.

- S.No

- Name

- Address

- Country of residence

- PAN (if allotted)

- Taxpayer’s registration number or any unique identification number allotted in the country of residence

In case of foreign company, please furnish the details of ultimate parent company

- S.No

- Name

- Address

- Country of residence

- PAN (if allotted)

- Taxpayer’s registration number or any unique identification number allotted in the country of residence

NATURE OF COMPANY AND ITS BUSINESS

Nature of company

- 1 Whether a public sector company as defined in section 2(36A) of the Income-tax Act Yes No

- 2 Whether a company owned by the Reserve Bank of India Yes No

- 3 Whether a company in which not less than forty percent of the shares are held (whether singly or taken together) by the Government or the Reserve Bank of India or a corporation owned by that Bank Yes No

- 4 Whether a banking company as defined in clause (c) of section 5 of the Banking Regulation Act,1949 Yes No

- 5 Whether a scheduled Bank being a bank included in the Second Schedule to the Reserve Bank of India Act Yes No

- 6 Whether a company registered with Insurance Regulatory and Development Authority (established under sub-section (1) of section 3 of the Insurance Regulatory and Development Authority Act, 1999) Yes No

- 7 Whether a company being a non-banking Financial Institution Yes No

- 8 Whether the company is unlisted? (If yes, please ensure to fill up the Schedule SH-1 and Schedule AL-1 Yes No)

- Nature of business or profession, if more than one business or profession indicate the three main activities/ products (Other than those declaring income under section 44AE

Part A-BS: Balance sheet as on 31st day of March, 2025 or as on the date of amalgamation

- 1 Equity and Liabilities

- 1 Shareholder’s fund

- A Share capital

- i Authorised Ai

- ii Issued, Subscribed and fully Paid up Aii

- iii Subscribed but not fully paid Aiii

- iv Total (Aii + Aiii) Aiv

- B Reserves and Surplus

- i Capital Reserve Bi

- ii Capital Redemption Reserve Bii

- iii Securities Premium Reserve Biii

- iv Debenture Redemption Reserve Biv

- v Revaluation Reserve Bv

- vi Share options outstanding amount Bvi

- vii Other reserve (specify nature and amount) Bvii

- viii Surplus i.e. Balance in profit and loss account (Debit balance to be shown as –ve figure) Bviii

- ix Total (Bi + Bii + Biii + Biv + Bv + Bvi + Bvii + Bviii) (Debit balance to be shown as –ve figure) Bix

- C Money received against share warrants 1C

- D Total Shareholder’s fund (Aiv + Bix + 1C) 1D

- A Share capital

- 1 Shareholder’s fund

- 2 Share application money pending allotment

- i Pending for less than one year i

- ii Pending for more than one year ii

- iii Total (i + ii) 2

- 3 Non-current liabilities

- A Long-term borrowings

- i Bonds/ debentures

- a Foreign currency ia

- b Rupee ib

- c Total (ia + ib) ic

- ii Term loans

- a Foreign currency iia

- b Rupee loans

- 1 From Banks b1

- 2 From others b2

- 3 Total (b1 + b2) b3

- c Total Term loans (iia + b3) iic

- iii Deferred payment liabilities iii

- iv Deposits from related parties (see instructions) iv

- v Other deposits v

- vi Loans and advances from related parties (see instructions) vi

- vii Other loans and advances vii

- viii Long term maturities of finance lease obligations viii

- ix Total Long-term borrowings (ic + iic + iii + iv + v + vi + vii + viii) 3A

- i Bonds/ debentures

- A Long-term borrowings

- B Deferred tax liabilities (net) 3B

- C Other long-term liabilities

- i Trade payables i

- ii Others ii

- iii Total Other long-term liabilities (i + ii) 3C

- D Long-term provisions

- i Provision for employee benefits i

- ii Others ii

- iii Total (i + ii) 3D

- E Total Non-current liabilities (3A + 3B + 3C + 3D) 3E

- 4 Current liabilities

- A Short-term borrowings

- B Trade payables

- C Other current liabilities

- D Short-term provisions

- E Total Current liabilities (4A + 4B + 4C + 4D) 4E

- Total Equity and liabilities (1D + 2 + 3E + 4E) I

II ASSETS

- 1 Non-current assets

- 2 Current assets

- C Trade receivables

- D Cash and cash equivalents

- E Short-term loans and advances

- F Other current assets

- G Total Current assets (Aviii + Bviii + Ciii + Dv + Eiii + F) 2G

- Total Assets (1F + 2G) II

Part A-BS IND AS: Balance sheet as on the 31st day of March, 2025 or as on the date of business combination [applicable for a company whose financial statements are drawn up in compliance to the Indian Accounting Standards specified in Annexure to the companies (Indian Accounting Standards) Rules, 2015]

- I Equity and Liabilities

- II Assets SSETS

1 Foreign currency a1

2 Rupee a2

3 Total (1 + 2) a3

b Term loans

1 Foreign currency b1

2 Rupee loans

i From Banks i

ii From other parties ii

iii Total (i + ii) b2

3 Total Term loans (b1 + b2) b3

c Deferred payment liabilities c

d Deposits d

e Loans from related parties (see instructions) e

f Long term maturities of finance lease obligations f

g Liability component of compound financial instruments g

h Other loans h

i Total borrowings (a3 + b3 + c + d + e + f + g + h) i

j Trade Payables j

k Other financial liabilities (Other than those specified in II under provisions) k

II Provisions

a Provision for employee benefits a

b Others (specify nature) b

c Total Provisions IIc

III Deferred tax liabilities (net) III

IV Other non-current liabilities

a Advances a

b Others (specify nature) b

c Total Other non-current liabilities IVc

Total Non-Current Liabilities (Ii + Ij + Ik + IIc + III + IVc) 2A

B Current liabilities

I Financial Liabilities

i Borrowings

a Loans repayable on demand

1 From Banks 1

2 From Other parties 2

3 Total Loans repayable on demand (1 + 2) 3

b Loans from related parties b

c Deposits c

d Other loans (specify nature) d

Total Borrowings (a3 + b + c + d) Ii

ii Trade payables Iii

iii Other financial liabilities

a Current maturities of long-term debt a

b Current maturities of finance lease obligations b

c Interest accrued c

d Unpaid dividends d

e Application money received for allotment of securities to the extent refundable and interest accrued thereone

f Unpaid matured deposits and interest accrued thereon f

g Unpaid matured debentures and interest accrued thereon g

h Others (specify nature) h

i Total Other financial liabilities (a + b +c +d +e +f +g+ h) Iiii

iv Total Financial Liabilities (Ii + Iii + Iiii) Iiv

II Other Current liabilities

a Revenue received in advance a

b Other advances (specify nature) b

c Others (specify nature) c

d Total Other current liabilities (a + b+ c) IId

III Provisions

a Provision for employee benefits a

b Others (specify nature) b

c Total provisions (a + b) IIIc

IV Current Tax Liabilities (Net) IV

Total Current liabilities (Iiv + IId + IIIc+ IV) 2B

Total Equity and liabilities (1C + 2A +2B) I

II ASSETS

1 Non-current assets

A Property, Plant and Equipment

a Gross block a

b Depreciation b

c Impairment losses c

d Net block (a – b – c) Ad

B Capital work-in-progress B

C Investment Property

a Gross block a

b Depreciation b

c Impairment losses c

d Net block (a – b – c) Cd

D Goodwill

a Gross block a

b Impairment losses b

c Net block (a – b) Dc

E Other Intangible Assets

a Gross block a

b Amortisation b

c Impairment losses c

d Net block (a – b – c) Ed

F Intangible assets under development F

G Biological assets other than bearer plants

a Gross block a

b Impairment losses b

c Net block (a – b) Gc

H Financial Assets

I Investments

i Investments in Equity instruments

a Listed equities ia

b Unlisted equities ib

c Total (ia + ib) ic

ii Investments in Preference shares ii

iii Investments in Government or trust securities iii

iv Investments in Debenture or bonds iv

v Investments in Mutual funds v

vi Investments in Partnership firms vi

vii Others Investments (specify nature) vii

viii Total non-current investments (ic + ii + iii + iv + v + vi + vii) HI

II Trade Receivables

a Secured, considered good a

b Unsecured, considered good b

c Doubtful c

d Total Trade receivables HII

III Loans

i Security deposits i

ii Loans to related parties (see instructions) ii

iii Other loans (specify nature) iii

iv Total Loans (i + ii + iii) HIII

v Loans included in HIII above which is-

a for the purpose of business or profession va

b not for the purpose of business or profession vb

c given to shareholder, being the beneficial owner of share, or to any concern or on behalf/ benefit of such shareholder as per section 2(22)(e) of I.T. Act vc

IV Other Financial Assets

i Bank Deposits with more than 12 months maturity i

ii Others ii

iii Total of Other Financial Assets (i + ii) HIV

I Deferred Tax Assets (Net) I

J Other non-current Assets

i Capital Advances i

ii Advances other than capital advances ii

iii Others (specify nature) iii

iv Total non-current assets (i + ii + iii) J

v Non-current assets included in J above which is due from

shareholder, being the beneficial owner of share, or from

any concern or on behalf/ benefit of such shareholder as

per section 2(22)(e) of I.T. Act

v Total Non-current assets (Ad + B + Cd + Dc + Ed + F + Gc + HI + HII + HIII + HIV + I + J) 1

2 Current assets

A Inventories

i Raw materials i

ii Work-in-progress ii

iii Finished goods iii

iv Stock-in-trade (in respect of goods acquired for trading) iv

v Stores and spares v

vi Loose tools vi

vii Others vii

viii Total Inventories (i + ii + iii + iv + v + vi + vii) 2A

B Financial Assets

I Investments

i Investment in Equity instruments

a Listed equities ia

b Unlisted equities ib

c Total (ia + ib) ic

ii Investment in Preference shares ii

iii Investment in government or trust securities iii

iv Investment in debentures or bonds iv

v Investment in Mutual funds v

vi Investment in partnership firms vi

vii Other Investments vii

viii Total Current investments (ic + ii + iii + iv + v + vi + vii) I

II Trade receivables

i Secured, considered good i

ii Unsecured, considered good ii

iii Doubtful iii

iv Total Trade receivables (i + ii + iii) II

III Cash and cash equivalents

i Balances with Banks (of the nature of cash and cash equivalents) i

ii Cheques, drafts in hand ii

iii Cash on hand iii

iv Others (specify nature) iv

v Total Cash and cash equivalents (i + ii + iii + iv) III

IV Bank Balances other than III above IV

V Loans

i Security Deposits i

ii Loans to related parties (see instructions) ii

iii Others (specify nature) iii

iv Total loans (i + ii + iii) V

v Loans and advances included in V above which is-

a for the purpose of business or profession va

b not for the purpose of business or profession vb

c given to a shareholder, being the beneficial owne of share, or to any concern or on behalf/ benefit of such shareholder as per section 2(22)(e) of I.T. Act vc

VI Other Financial Assets VI

Total Financial Assets (I + II + III + IV + V + VI) 2B

C Current Tax Assets (Net) 2C

D Other current assets

i Advances other than capital advances i

ii Others (specify nature) ii

iii Total 2D

Total Current assets (2A + 2B + 2C + 2D) 2

Total Assets (1 + 2) II

Part A-

Manufacturing Account Manufacturing Account for the financial year 2024-25 (fill items 1 to 3 in a case where regular books of account are maintained, otherwise fill items 61 to 62 as applicable)

1 Debits to Manufacturing account

A Opening Inventory

i Opening stock of raw-material i

ii Opening stock of Work in progress ii

iii Total (i + ii) Aiii

B Purchases (net of refunds and duty or tax, if any) B

C Direct wages C

D Direct expenses (Di + Dii + Diii) D

i Carriage inward i

ii Power and fuel ii

iii Other direct expenses iii

E Factory Overheads

i Indirect wages i

ii Factory rent and rates ii

iii Factory Insurance iii

iv Factory fuel and power iv

v Factory general expenses v

vi Depreciation of factory machinery vi

vii Total (i+ii+iii+iv+v+vi) Evii

F Total of Debits to Manufacturing Account (Aiii+B+C+D+Evii) 1F

2 Closing Stock

i Raw material 2i

ii Work-in-progress 2ii

Total (2i +2ii) 2

3 Cost of Goods Produced – transferred to Trading Account (1F – 2) 3

Part A- Trading Account Trading Account for the financial year 2024-25 (fill items 4 to 12 in a case where regular books of account are maintained, otherwise fill items 61 to 62 as applicable)

C R 4 Revenue from operations

A Sales/ Gross receipts of business (net of returns and refunds and duty or tax, if any)

i Sale of goods i

ii Sale of services ii

iii Other operating revenues (specify nature and amount)

a iiia

b iiib

c Total (iiia + iiib) iiic

iv Total (i + ii + iiic) Aiv

B Gross receipts from Profession B

C Duties, taxes and cess received or receivable in respect of goods and services sold or supplied

i Union Excise duties i

ii Service tax ii

iii VAT/ Sales tax iii

iv Central Goods & Service Tax (CGST) iv

v State Goods & Services Tax (SGST) v

vi Integrated Goods & Services Tax (IGST) vi

vii Union Territory Goods & Services Tax (UTGST) vii

viii Any other duty, tax and cess viii

ix Total (i + ii + iii + iv +v+ vi+vii+viii) Cix

D Total Revenue from operations (Aiv + B +Cix) 4D

5 Closing Stock of Finished Goods 5

6 Total of credits to Trading Account (4D + 5) 6

DEBITS TO TRADING ACCOUNT 7 Opening Stock of Finished Goods 7

8 Purchases (net of refunds and duty or tax, if any) 8

9 Direct Expenses (9i + 9ii + 9iii) 9

i Carriage inward i

ii Power and fuel ii

iii Other direct expenses

Note: Row can be added as per the nature of Direct Expenses iii

10 Duties and taxes, paid or payable, in respect of goods and services purchased

i Custom duty 10i

ii Counter veiling duty 10ii

iii Special additional duty 10iii

iv Union excise duty 10iv

v Service tax 10v

vi VAT/ Sales tax 10vi

vii Central Goods & Service Tax (CGST) 10vii

viii State Goods & Services Tax (SGST) 10viii

ix Integrated Goods & Services Tax (IGST) 10ix

x Union Territory Goods & Services Tax (UTGST) 10x

xi Any other tax, paid or payable 10xi

xii Total (10i + 10ii + 10iii + 10iv + 10v + 10vi + 10vii + 10viii + 10ix + 10x + 10xi) 10xii

11 Cost of goods produced – Transferred from Manufacturing Account 11

12 Gross Profit from Business/Profession – transferred to Profit and Loss account (6-7- 8-9-10xii-11) 12

12a Turnover from Intraday Trading 12a

12b Income from Intraday Trading – transferred to Profit and Loss account 12b

Part A-P& L Profit and Loss Account for the financial year 2024-25 (fill items 13 to 60 in a case where regular books of account are maintained, otherwise fill items 61 to 62 as applicable)

CREDITS TO PROFIT AND LOSS ACCOUNT 13 Gross profit transferred from Trading Account (12+12b) 13

14 Other income

i Rent i

ii Commission ii

iii Dividend income iii

iv Interest income iv

v Profit on sale of fixed assets v

vi Profit on sale of investment being securities chargeable to Securities Transaction Tax (STT) vi

vii Profit on sale of other investment vii

viii Gain (loss) on account of foreign exchange fluctuation u/s 43AA viii

ix Profit on conversion of inventory into capital asset u/s 28(via) (Fair Market Value of inventory as on the date of conversion) ix

x Agricultural income x

xi Any other income (specify nature and amount)

A xia

B xib

C Total (xia + xib) xic

xii Total of other income (i + ii + iii + iv + v + vi + vii + viii + ix + x + xic) 14xii

15 Total of credits to profit and loss account (13+14xii) 15

DEBITS TO PROFIT AND LOSS ACCOUNT 16 Freight outward 16

17 Consumption of stores and spare parts 17

18 Power and fuel 18

19 Rents 19

20 Repairs to building 20

21 Repairs to machinery 21

22 Compensation to employees

i Salaries and wages 22i

ii Bonus 22ii

iii Reimbursement of medical expenses 22iii

iv Leave encashment 22iv

v Leave travel benefits 22v

vi Contribution to approved superannuation fund 22vi

vii Contribution to recognised provident fund 22vii

viii Contribution to recognised gratuity fund 22viii

ix Contribution to any other fund 22ix

x Any other benefit to employees in respect of which an expenditure has been incurred 22x

xi Total compensation to employees (total of 22i to 22x) 22xi

xiia Whether any compensation, included in 22xi, paid to non- residents xiia Yes / No

xiib If Yes, amount paid to non-residents xiib

23 Insurance

i Medical Insurance 23i

ii Life Insurance 23ii

iii Keyman’s Insurance 23iii

iv Other Insurance including factory, office, car, goods, etc. 23iv

v Total expenditure on insurance (23i + 23ii + 23iii + 23iv) 23v

24 Workmen and staff welfare expenses 24

25 Entertainment 25

26 Hospitality 26

27 Conference 27

28 Sales promotion including publicity (other than advertisement) 28

29 Advertisement 29

30 Commission

i Paid outside India, or paid in India to a non-resident other than a company or a foreign company i

ii To others ii

iii Total (i + ii) 30iii

31 Royalty

i Paid outside India, or paid in India to a non-resident other than a company or a foreign company i

ii To others ii

iii Total (i + ii) 31iii

32 Professional / Consultancy fees / Fee for technical services

i Paid outside India, or paid in India to a non-resident other than a company or a foreign company i

ii To others ii

iii Total (i + ii) 32iii

33 Hotel, boarding and Lodging 33

34 Traveling expenses other than on foreign traveling 34

35 Foreign travelling expenses 35

36 Conveyance expenses 36

37 Telephone expenses 37

38 Guest House expenses 38

39 Club expenses 39

40 Festival celebration expenses 40

41 Scholarship 41

42 Gift 42

43 Donation 43

44 Rates and taxes, paid or payable to Government or any local body (excluding taxes on income)

i Union excise duty 44i

ii Service tax 44ii

iii VAT/ Sales tax 44iii

iv Cess 44iv

v Central Goods & Service Tax (CGST) 44v

vi State Goods & Services Tax (SGST) 44vi

vii Integrated Goods & Services Tax (IGST) 44vii

viii Union Territory Goods & Services Tax (UTGST) 44viii

ix Any other rate, tax, duty or cess incl STT and CTT 44ix

x Total rates and taxes paid or payable (44i + 44ii +44iii +44iv + 44v + 44vi + 44vii + 44viii+44ix) 44x

45 Audit fee 45

46 Other expenses (specify nature and amount)

i i

ii ii

iii Total (i + ii) 46iii

47 Bad debts (specify PAN/Aadhaar No. of the person, if available, for whom Bad Debt for amount of Rs. 1 lakh or more is claimed and amount)

48 Provision for bad and doubtful debts 48

49 Other provisions 49

50 Profit before interest, depreciation and taxes [15 – (16 to 21 + 22xi + 23v + 24 to 29 + 30iii + 31iii + 32iii + 33 to 43 + 44x + 45 + 46iii + 47iv + 48 + 49)] 50

51 Interest

i Paid outside India, or paid in India to a non-resident other than a company or a foreign company i

ii To others ii

iii Total (i + ii) 51iii

52 Depreciation and amortization 52

53 Net profit before taxes (50 – 51iii – 52) 53

PROVISIONS PROVISION FOR TAX AND APPROPRIATIONS 54 Provision for current tax 54

55 Provision for Deferred Tax 55

56 Profit after tax (53 – 54 – 55) 56

57 Balance brought forward from previous year 57

58 Amount available for appropriation (56 + 57) 58

59 Appropriations

i Transfer to reserves and surplus 59i

ii Proposed dividend/ Interim dividend 59ii

iii Tax on dividend/ Tax on dividend for earlier years 59iii

iv Appropriation towards Corporate Social Responsibility (CSR) activities

(in case of companies covered under section 135 of Companies Act, 2013) 59iv

v Any other appropriation 59v

vi Total (59i + 59ii + 59iii + 59iv+59v) 59vi

60 Balance carried to balance sheet (58 – 59vi) 60

61 COMPUTATION OF PRESUMPTIVE INCOME FROM GOODS CARRIAGES UNDER SECTION 44AE

(Please Note : At any time during the year the number of vehicles should not exceed 10 vehicles)

NOTE— If the profits are lower than prescribed under S.44AE or the number of goods carriage owned / leased / hired at any time during the year exceeds 10, then, it is mandatory to maintain books of account and have a tax audit under section 44AB

NO ACCOUNT

62 In case of Foreign Company whose total income comprises of profits and gains from business referred to in sections 44B, 44BB, 44BBA, 44BBB, 44BBC, 44D or having eligible business of selling raw diamond (refer rule 10TIA) furnish the following information

a Gross receipts / Turnover 62a

b Net profit 62b

Part A- Manufacturing

Account Ind- AS

Manufacturing Account for the financial year 2024-25 [applicable for a company whose financial statements are drawn up in compliance to the Indian Accounting Standards specified in Annexure to the companies (Indian Accounting Standards) Rules, 2015)]

1 Debits to Manufacturing account

A Opening Inventory

i Opening stock of raw-material i

ii Opening stock of Work in progress ii

iii Total (i + ii) Aiii

B Purchases (net of refunds and duty or tax, if any) B

C Direct wages C

D Direct expenses D

i Carriage inward i

ii Power and fuel ii

iii Other direct expenses iii

E Factory Overheads

i Indirect wages

ii Factory rent and rates

iii Factory Insurance

iv Factory fuel and power

v Factory general expenses

vi Depreciation of factory machinery

vii Total (i+ii+iii+iv+v+vi) Evii

F Total of Debits to Manufacturing Account (Aiii+B+C+D+Evii) 1F

2 Closing Stock

i Raw material 2i

ii Work-in-progress 2ii

Total (2i +2ii) 2

3 Cost of Goods Produced – transferred to Trading Account (1F – 2) 3

Part A- Trading

Account Ind- AS

Trading Account for the financial year 2024-25 [applicable for a company whose financial statements are drawn up in compliance to the Indian Accounting Standards specified in Annexure to the companies (Indian Accounting Standards) Rules, 2015]

C R

4 Revenue from operations

A Sales/ Gross receipts of business (net of returns and refunds and duty or tax, if any)

i Sale of goods i

ii Sale of services ii

iii Other operating revenues (specify nature and amount)

a iiia

b iiib

c Total (iiia + iiib) iiic

iv Total (i + ii + iiic) Aiv

B Gross receipts from Profession B

C Duties, taxes and cess received or receivable in respect of goods and services sold or supplied

i Union Excise duties i

ii Service tax ii

iii VAT/ Sales tax iii

iv Central Goods & Service Tax (CGST) iv

v State Goods & Services Tax (SGST) v

vi Integrated Goods & Services Tax (IGST) vi

vii Union Territory Goods & Services Tax (UTGST) vii

viii Any other duty, tax and cess viii

ix Total (i + ii + iii + iv +v+ vi+vii+viii) Cix

D Total Revenue from operations (Aiv + B +Cix) 4D

5 Closing Stock of Finished Goods 5

6 Total of credits to Trading Account (4D + 5) 6

DEBITS TO TRADING ACCOUNT

7 Opening Stock of Finished Goods 7

8 Purchases (net of refunds and duty or tax, if any) 8

9 Direct Expenses (9i + 9ii + 9iii) 9

i Carriage inward i

ii Power and fuel ii

iii Other direct expenses

10 Duties and taxes, paid or payable, in respect of goods and services purchased

i Custom duty 10i

ii Counter veiling duty 10ii

iii Special additional duty 10iii

iv Union excise duty 10iv

v Service tax 10v

vi VAT/ Sales tax 10vi

vii Central Goods & Service Tax (CGST) 10vii

viii State Goods & Services Tax (SGST) 10viii

ix Integrated Goods & Services Tax (IGST) 10ix

x Union Territory Goods & Services Tax (UTGST) 10x

xi Any other tax, paid or payable 10xi

xii Total (10i + 10ii + 10iii + 10iv + 10v + 10vi + 10vii + 10viii + 10ix + 10x + 10xi) 10xii

11 Cost of goods produced – Transferred from Manufacturing Account 11

12 Gross Profit from Business/Profession – transferred to Profit and Loss account (6-7- 8-9-10xii-11) 12

12a Turnover from Intraday Trading 12a

12b Income from Intraday Trading – transferred to Profit and Loss account 12b

Part A-P& L Ind-AS Profit and Loss Account for the financial year 2024-25 [applicable for a company whose financial

statements are drawn up in compliance to the Indian Accounting Standards specified in Annexure to the companies (Indian Accounting Standards) Rules, 2015]

CREDITS TO PROFIT AND LOSS ACCOUNT

13 Gross profit transferred from Trading Account (12+12b)

14 Other income

i Rent i

ii Commission ii

iii Dividend income iii

iv Interest income iv

v Profit on sale of fixed assets v

vi Profit on sale of investment being securities chargeable to Securities Transaction Tax (STT) vi

vii Profit on sale of other investment vii

viii Gain (loss) on account of foreign exchange fluctuation u/s 43AA viii

ix Profit on conversion of inventory into capital asset u/s 28(via)

(Fair Market Value of inventory as on the date of conversion) ix

x Agricultural income x

xi Any other income (specify nature and amount)

a xia

b xib

c Total (xia + xib) xic

xii Total of other income (i + ii + iii + iv + v + vi + vii + viii + ix + x + xic) 14xii

15 Total of credits to profit and loss account (13+14xii) 15

16 Freight outward 16

17 Consumption of stores and spare parts 17

18 Power and fuel 18

19 Rents 19

20 Repairs to building 20

21 Repairs to machinery 21

22 Compensation to employees

i Salaries and wages 22i

ii Bonus 22ii

iii Reimbursement of medical expenses 22iii

iv Leave encashment 22iv

v Leave travel benefits 22v

vi Contribution to approved superannuation fund 22vi

vii Contribution to recognised provident fund 22vii

viii Contribution to recognised gratuity fund 22viii

ix Contribution to any other fund 22ix

x Any other benefit to employees in respect of which an expenditure has been incurred 22x

xi Total compensation to employees (total of 22i to 22x) 22xi

xii Whether any compensation, included in 22xi, paid to non-residents xiia Yes / No

If Yes, amount paid to non-residents xiib

23 Insurance

i Medical Insurance 23i

ii Life Insurance 23ii

iii Keyman’s Insurance 23iii

iv Other Insurance including factory, office, car, goods, etc. 23iv

v Total expenditure on insurance (23i + 23ii + 23iii + 23iv) 23v

24 Workmen and staff welfare expenses 24

25 Entertainment 25

26 Hospitality 26

27 Conference 27

28 Sales promotion including publicity (other than advertisement) 28

29 Advertisement 29

30 Commission

i Paid outside India, or paid in India to a non-resident other than a company or a foreign company i

ii To others ii

iii Total (i + ii) 30iii

31 Royalty

i Paid outside India, or paid in India to a non-resident other than a company or a foreign company i

ii To others ii

iii Total (i + ii) 31iii

32 Professional / Consultancy fees / Fee for technical services

i Paid outside India, or paid in India to a non-resident other than a company or a foreign company i

ii To others ii

iii Total (i + ii) 32iii

33 Hotel, boarding and Lodging 33

34 Traveling expenses other than on foreign traveling 34

35 Foreign travelling expenses 35

36 Conveyance expenses 36

37 Telephone expenses 37

38 Guest House expenses 38

39 Club expenses 39

40 Festival celebration expenses 40

41 Scholarship 41

42 Gift 42

43 Donation 43

44 Rates and taxes, paid or payable to Government or any local body (excluding taxes on income)

i Union excise duty 44i

ii Service tax 44ii

iii VAT/ Sales tax 44iii

iv Cess 44iv

v Central Goods & Service Tax (CGST) 44v

vi State Goods & Services Tax (SGST) 44vi

vii Integrated Goods & Services Tax (IGST) 44vii

viii Union Territory Goods & Services Tax (UTGST) 44viii

ix Any other rate, tax, duty or cess incl STT and CTT 44ix

x Total rates and taxes paid or payable (44i + 44ii +44iii +44iv + 44v + 44vi + 44vii + 44viii +44ix) 44x

45 Audit fee 45

46 Other expenses (specify nature and amount)

47 Bad debts (specify PAN/Aadhaar No. of the person, if available, for whom Bad Debt for amount of Rs. 1 lakh or more is claimed and amount)

48 Provision for bad and doubtful debts 48

49 Other provisions 49

50 Profit before interest, depreciation and taxes [15 – (16 to 21 + 22xi + 23v + 24 to 29 + 30iii + 31iii + 32iii + 33 to 43 + 44x + 45 + 46iii + 47iv + 48 + 49)] 50

51 Interest

i Paid outside India, or paid in India to a non-resident other than a company or a foreign company i

ii To others ii

iii Total (i + ii) 51iii

52 Depreciation and amortisation 52

53 Net profit before taxes (50 – 51iii – 52) 53

PROVISIONS PROVISION FOR TAX AND APPROPRIATIONS

54 Provision for current tax 54

55 Provision for Deferred Tax 55

56 Profit after tax (53 – 54 – 55) 56

57 Balance brought forward from previous year 57

58 Amount available for appropriation (56 + 57) 58

59 Appropriations

i Transfer to reserves and surplus 59i

ii Proposed dividend/ Interim dividend 59ii

iii Tax on dividend/ Tax on dividend for earlier years 59iii

iv Appropriation towards Corporate Social Responsibility (CSR) activities (in case of companies covered under

section 135 of Companies Act, 2013) 59iv

v Any other appropriation 59v

vi Total (59i + 59ii + 59iii + 59iv+59v) 59vi

60 Balance carried to balance sheet (58 – 59vi) 60

61 A Items that will not be reclassified to P&L

i Changes in revaluation surplus i

ii Re-measurements of the defined benefit plans ii

iii Equity instruments through OCI iii

iv Fair value Changes relating to own credit risk of financial liabilities designated at FVTPL iv

v Share of Other comprehensive income in associates and joint ventures, to the extent not to be classified to P&L v vi Others (Specify nature) vi

vii Income tax relating to items that will not be reclassified to P&L vii

viii Total 61A

B Items that will be reclassified to P&L

i Exchange differences in translating the financial statements of a foreign operation i

ii Debt instruments through OCI ii

iii The effective portion of gains and loss on hedging instruments in a cash flow hedge iii

iv Share of OCI in associates and joint ventures to the extent to be classified into P&L iv

v Others (Specify nature) v

vi Income tax relating to items that will be reclassified to P&L vi

vii Total 61B

62 Total Comprehensive Income (56 + 61A + 61B) 62

Part A- OI Other Information (mandatory, if liable for audit under section 44AB, for other fill, if applicable)

OTHER INFORMATION

1 Method of accounting employed in the previous year (Tick) mercantile cash

2 Is there any change in method of accounting (Tick) Yes No

3a Increase in the profit or decrease in loss because of deviation, if any, as per Income Computation 3a

Disclosure Standards notified under section 145(2) [column XI(3) of Schedule ICDS]

3b Decrease in the profit or increase in loss because of deviation, if any, as per Income Computation 3b

Disclosure Standards notified under section 145(2) [column XI(4) of Schedule ICDS]

4 Method of valuation of closing stock employed in the previous year (optional in case of professionals)

a Raw Material (if at cost or market rates whichever is less write 1, if at cost write 2, if at market rate write 3) •

b Finished goods (if at cost or market rates whichever is less write 1, if at cost write 2, if at market rate write 3) •

c Is there any change in stock valuation method (Tick) Yes No

d Increase in the profit or decrease in loss because of deviation, if any, from the method of 4d

valuation specified under section 145A

e Decrease in the profit or increase in loss because of deviation, if any, from the method of 4e

valuation specified under section 145A

5 Amounts not credited to the profit and loss account, being –

a the items falling within the scope of section 28 5a

b the proforma credits, drawbacks, refund of duty of

customs or excise or service tax, or refund of sales tax or

value added tax, or refund of GST, where such credits, 5b

drawbacks or refunds are admitted as due by the

authorities concerned

c escalation claims accepted during the previous year 5c

d any other item of income 5d

e capital receipt, if any 5e

f Total of amounts not credited to profit and loss account (5a+5b+5c+5d+5e) 5f

6 Amounts debited to the profit and loss account, to the extent disallowable under section 36

due to non-fulfilment of condition specified in relevant clauses-

a Premium paid for insurance against risk of damage or 6a

destruction of stocks or store [36(1)(i)]

b Premium paid for insurance on the health of employees 6b

[36(1)(ib)]

Any sum paid to an employee as bonus or commission

c for services rendered, where such sum was otherwise 6c

payable to him as profits or dividend [36(1)(ii)]

d Any amount of interest paid in respect of borrowed 6d

capital [36(1)(iii)]

e Amount of discount on a zero-coupon bond [36(1)(iiia)] 6e

f Amount of contributions to a recognised provident fund 6f

[36(1)(iv)]

g Amount of contributions to an approved superannuation fund [36(1)(iv)] 6g

h Amount of contribution to a pension scheme referred to in section 80CCD [36(1)(iva)] 6h

i Amount of contributions to an approved gratuity fund [36(1)(v)] 6i

j Amount of contributions to any other fund 6j

k Any sum received from employees as contribution to any provident fund or superannuation fund or any fund set up under ESI Act or any other fund for the welfare of employees to the extent not credited to the employees account on or before the due date [36(1)(va)] 6k

l Amount of bad and doubtful debts [36(1)(vii)] 6l

m Provision for bad and doubtful debts [36(1)(viia)] 6m

n Amount transferred to any special reserve [36(1)(viii)] 6n

o Expenditure for the purposes of promoting family planning amongst employees [36(1)(ix)] 6o

p Amount of securities transaction paid in respect of transaction in securities if such income is not included in business income [36(1)(xv)] 6p

q Marked to market loss or other expected loss as computed in accordance with the ICDS notified u/s 145(2) [36(1)(xviii)] 6q

r Any other disallowance 6r

s Total amount disallowable under section 36 (total of 6a to 6r) 6s

t Total number of employees employed by the company (mandatory in case company has recognized Provident Fund)

i deployed in India i

ii deployed outside India ii

iii Total iii

7 Amounts debited to the profit and loss account, to the extent disallowable under section 37

a Expenditure of capital nature [37(1)] 7a

b Expenditure of personal nature [37(1)] 7b

c Expenditure laid out or expended wholly and exclusively NOT for the purpose of business or profession [37(1)] 7c

d Expenditure on advertisement in any souvenir, brochure, tract, pamphlet or the like, published by a political party [37(2B)] 7d

e Expenditure by way of penalty or fine for violation of any law for the time being in force 7e

f Any other penalty or fine 7f

g Expenditure incurred for any purpose which is an offence or which is prohibited by law 7g

h Expenditure incurred on corporate social responsibility (CSR) 7h

i Amount of any liability of a contingent nature 7i

j Any other amount not allowable under section 37 7j

k Total amount disallowable under section 37 (total of 7a to 7j) 7k

8 A. Amounts debited to the profit and loss account, to the extent disallowable under section 40

a Amount disallowable under section 40 (a)(i), on account of non-compliance with the provisions of Chapter XVII-B Aa b Amount disallowable under section 40(a)(ia) on account of non-compliance with the provisions of Chapter XVII-B Ab c Amount disallowable under section 40(a)(ib) on account of non-compliance with the provisions of Chapter VIII of the

Finance Act, 2016 Ac

d Amount disallowable under section 40(a)(iii) on account of non-compliance with the provisions of Chapter XVII-B Ad e Amount of tax or rate levied or assessed on the basis of profits [40(a)(ii)] Ae

f Amount paid as wealth tax [40(a)(iia)] Af

g Amount paid by way of royalty, license fee, service fee etc. as per section 40(a)(iib) Ag

h Amount of interest, salary, bonus, commission or remuneration paid to any partner or member inadmissible under section [40 (b)/ 40(ba)] Ah

i Any other disallowance Ai

j Total amount disallowable under section 40(total of Aa to Ai ) Aj

B. Any amount disallowed under section 40 in any preceding previous year but allowable during the previous year 8B

9 Amounts debited to the profit and loss account, to the extent disallowable under section 40A

a Amounts paid to persons specified in section 40A(2)(b) 9a

b Amount paid otherwise than by account payee cheque or account payee bank draft or use of electronic clearing system through a bank account or through such electronic mode as may be prescribed, disallowable under section 40A(3) 9b

c Provision for payment of gratuity [40A(7)] 9c

d any sum paid by the assessee as an employer for setting up or as contribution to any fund, trust, company, AOP, or BOI or society or any other institution [40A(9)] 9d

e Any other disallowance 9e

f Total amount disallowable under section 40A (Total of 9a to 9e) 9f

10 Any amount disallowed under section 43B in any preceding previous year but allowable during the previous year

a Any sum in the nature of tax, duty, cess or fee under any law 10a

b Any sum payable by way of contribution to any provident fund or superannuation fund or gratuity fund or any other fund for the welfare of employees 10b

c Any sum payable to an employee as bonus or commission for services rendered 10c

d Any sum payable as interest on any loan or borrowing from any public financial institution or a State financial corporation or a State Industrial investment corporation 10d

da Any sum payable as interest on any loan or borrowing from such class of non-banking financial companies as may be notified by the Central Government , in accordance with the terms and conditions of the agreement governing such loan or borrowing 10da

e Any sum payable as interest on any loan or borrowing from any scheduled bank or a co-operative bank other than a primary agricultural credit society or a primary co-operative agricultural and rural development bank 10e

f Any sum payable towards leave encashment 10f

g Any sum payable to the Indian Railways for the use of railway assets 10g

h Any sum payable to a micro or small enterprise beyond the time limit specified in section 15 of the Micro, Small and Medium Enterprises Development Act, 2006 10h

i Total amount allowable under section 43B (total of 10a to 10h ) 10i

11 Any amount debited to profit and loss account of the previous year but disallowable under section 43B

a Any sum in the nature of tax, duty, cess or fee under any law 11a

b Any sum payable by way of contribution to any provident fund or superannuation fund or gratuity fund or any other fund for the welfare of employees 11b

c Any sum payable to an employee as bonus or commission for services rendered 11c

d Any sum payable as interest on any loan or borrowing from any public financial institution or a State financial corporation or a State Industrial investment corporation 11d

da any sum payable as interest on any loan or borrowing from such class of non-banking financial companies as may be notified by the Central Government, in accordance with the terms and conditions of the agreement governing such loan or borrowing

11da

e Any sum payable as interest on any loan or borrowing from any scheduled bank or a co-operative bank other than a primary agricultural credit society or a primary co-operative agricultural and rural development bank 11e

f Any sum payable towards leave encashment 11f

g Any sum payable to the Indian Railways for the use of railway assets 11g

h Any sum payable to a micro or small enterprise beyond the time limit specified in section 15 of the Micro, Small and Medium Enterprises Development Act, 2006 11h

i Total amount disallowable under Section 43B (total of 11a to 11h) 11i

12 Amount of credit outstanding in the accounts in respect of

a Union Excise Duty 12a

b Service tax 12b

c VAT/sales tax 12c

d Central Goods & Service Tax (CGST) 12d

e State Goods & Services Tax (SGST) 12e

f Integrated Goods & Services Tax (IGST) 12f

g Union Territory Goods & Services Tax (UTGST) 12g

h Any other tax 12h

i Total amount outstanding (total of 12a to 12h) 12i

13 Amounts deemed to be profits and gains under section 33AB or 33ABA or 33AC 13

14 Any amount of profit chargeable to tax under section 41 14

15 Amount of income or expenditure of prior period credited or debited to the profit and loss account (net) 15

16 Amount of expenditure disallowed u/s 14A 16

17 Whether assessee is exercising option under subsection 2A of section 92CE (Tick) Yes No

[If yes , please fill schedule TPSA] 17

Part A – QD Quantitative details (mandatory, if liable for audit under section 44AB)

QUANTITATIVE DETAILS

(a) In the case of a trading concern

1 Opening stock 1

2 Purchase during the previous year 2

3 Sales during the previous year 3

4 Closing stock 4

5 Shortage/ excess, if any 5

(b) In the case of a manufacturing concern

6 Raw materials

a Opening stock 6a

b Purchases during the previous year 6b

c Consumption during the previous year 6c

d Sales during the previous year 6d

e Closing stock 6e

f Yield finished products 6f

g Percentage of yield 6g

h Shortage/ excess, if any 6h

7 Finished products/ By-products

a opening stock 7a

b purchase during the previous year 7b

c quantity manufactured during the previous year 7c

d sales during the previous year 7d

e closing stock 7e

f shortage/ excess, if any 7f

RECEIPT AND PAYMENT ACCOUNT OF COMPANY UNDER LIQUIDATION

1 Opening balance

i Cash in hand 1i

ii Bank 1ii

iii Total opening balance 1iii

2 Receipts

i Interest 2i

ii Dividend 2ii

iii Sale of assets (pls. specify nature and amount)

a 2iiia

b 2iiib

c 2iiic

d Total (iiia + iiib + iiic) 2iiid

iv Realisation of dues/debtors 2iv

v Others (pls. specify whether revenue/capital, nature and amount)

a 2va

b 2vb

c Total of other receipts (va + vb) 2vc

vi Total receipts (2i + 2ii + 2iiid+ 2iv + 2vc) 2vi

3 Total of opening balance and receipts 3

4 Payments

i Repayment of secured loan 4i

ii Repayment of unsecured loan 4ii

iii Repayment to creditors 4iii

iv Commission 4iv

v Others (pls. specify)

a 4va

b 4vb

c Total of other payments (4va + 4vb) 4vc

vi Total payments (4i + 4ii + 4iii + 4iv + 4vc) 4vi

5 Closing balance

i Cash in hand 5i

ii Bank 5ii

iii Total of closing balance (5i + 5ii) 5iii

6 Total of closing balance and payments (4vi + 5iii) 6

SCHEDULES TO THE RETURN FORM (FILL AS APPLICABLE)

Schedule HP Details of Income from House Property (Please refer instructions) (Drop down to be provided indicating ownership of property)

HOUSE PROPERTY

1 Address of property 1 Town/ City State Country PIN Code / Zip Code

Is the property co-owned? Yes No (if “YES” please enter following details)

Assessee’s percentage of share in the property %

Name of Co-owner(s) PAN/Aadhaar No. of Co-owner (s) Percentage Share in Property

I

II

[Tick the applicable option]

Let out

Deemed let out Name(s) of

Tenant(s) (if let out) PAN/Aadhaar No. of Tenant(s) (Please see Note ) PAN/TAN/Aadhaar No. of Tenant(s) (if TDS credit is claimed)

I

II

a Gross rent received or receivable or lettable value 1a

b The amount of rent which cannot be realized 1b

c Tax paid to local authorities 1c

d Total (1b + 1c) 1d

e Annual value (1a – 1d) 1e

f Annual value of the property owned (own percentage share x 1e) 1f

g 30% of 1f 1g

h Interest payable on borrowed capital (Details are to be filled in the drop down to be provided in e-filing 1h

i Total (1g + 1h) 1i

j Arrears/Unrealised rent received during the year less 30% 1j

k Income from house property 1 (1f – 1i+1j) 1k

(fill up details separately for each property

2 Pass through income/loss if any * 2

3 Income under the head “Income from house property” (Ʃ 1k + 2)

(if negative take the figure to 2i of schedule CYLA) 3

NOTE► Furnishing of PAN/Aadhaar No. of tenant is mandatory, if tax is deducted under section 194-IB.

Schedule BP Computation of income from business or profession

INCOME FROM BUSINESS OR PROFESSION

A From business or profession other than speculative business and specified business

1 Profit before tax as per profit and loss account (item 53, 61(ii) and 62(b) of Part A-P&L) / (item 53 of Part A-P&L – Ind AS) (as applicable) 1

2a Net profit or loss from speculative business included in 1 (enter –ve sign in case of loss) (Sl. No. 12b of Schedule Trading Account or Trading-Ind As account) (as applicable) 2a

2b Net profit or Loss from Specified Business u/s 35AD included in 1 (enter –ve sign in case of loss) 2b

3 Income/ receipts credited to profit and loss account considered under other heads of income or chargeable u/s 115BBF or chargeable u/s 115BBG or chargeable u/s 115BBH a House property 3a

b Capital gains 3b

c Other sources 3c

ci Dividend 3ci

cii other than Dividend 3cii

d u/s 115BBF 3d

e u/s 115BBG 3e

f u/s 115BBH (net of Cost of Acquisition, if any) 3f

(Item No. A of Schedule VDA)

4a Profit or loss included in 1, which is referred to in section 44B/44BB/44BBA/44BBB/44BBC/44AE/44D/44DA/Chapter-XII-G/

First Schedule of Income-tax Act (other than 115B) (Dropdown to be 4a

4b Profit and gains from life insurance business referred to in section 4b

4c Profit from activities covered under rule 7, 7A, 7B(1), 7B(1A) and 8 (Dropdown to be provided) 4c

4d Profit from eligible business of selling raw diamonds (refer rule 10TIA) 4d

5 Income credited to Profit and Loss account (included in 1) which is exempt

a Share of income from firm(s) 5a

b Share of income from AOP/ BOI 5b

c Any other exempt income (specify nature and amount)

i ci

ii cii

iii Total (ci + cii) 5ciii

d Total exempt income (5a + 5b + 5ciii) 5d

6 Balance (1– 2a – 2b – 3a – 3b – 3c – 3d – 3e – 3f-4– 5d) 6

7 Expenses debited to profit and loss account considered under other heads of income/related to income chargeable u/s 115BBF or u/s 115BBG or u/s 115BBH A House property 7a

B Capital gains 7b

C Other sources 7c

D u/s 115BBF 7d

E u/s 115BBG 7e

F u/s 115BBH (other than Cost of 7f

8a Expenses debited to profit and loss account which relate to exempt 8a

8b Expenses debited to profit and loss account which relate to exempt income and disallowed u/s 14A (16 of Part A-OI) 8b

9 Total (7a + 7b + 7c + 7d + 7e + 7f+ 8a+8b) 9

10 Adjusted profit or loss (6+9) 10

11 Depreciation and amortization debited to profit and loss account 11

12 Depreciation allowable under Income-tax Act

i Depreciation allowable under section 32(1)(ii) and 32(1)(iia) (item 6 of Schedule-DEP) 12i

ii Depreciation allowable under section 32(1)(i)

(Make your own computation refer Appendix-IA of IT Rules) 12ii

iii Total (12i + 12ii) 12iii

13 Profit or loss after adjustment for depreciation (10 +11 – 12iii) 13

14 Amounts debited to the profit and loss account, to the extent disallowable under section 36 (6s of Part A-OI) 14

15 Amounts debited to the profit and loss account, to the extent disallowable under section 37 (7k of Part A-OI) 15

16 Amounts debited to the profit and loss account, to the extent disallowable under section 40 (8Aj of Part A-OI) 16

17 Amounts debited to the profit and loss account, to the extent disallowable under section 40A (9f of Part A-OI) 17

18 Any amount debited to profit and loss account of the previous year but disallowable under section 43B (11i of Part A-OI) 18

19 Interest disallowable under section 23 of the Micro, Small and Medium Enterprises Development Act, 2006 19

20 Deemed income under section 41 20

21 Deemed income under section 32AC/ 32AD/ 33AB/ 33ABA/35ABA/ 35ABB/ 35AC/ 40A(3A)/ 33AC/ 72A/ 80HHD/ 80-IA 21

22 Deemed income under section 43CA 22

23 Any other item of addition under section 28 to 44DB 23

24 Any other income not included in profit and loss account/any other expense not allowable (including income from salary, commission, bonus and interest from firms in which company is a partner) 24

25 Increase in profit or decrease in loss on account of ICDS adjustments and deviation in method of valuation of stock (Column 3a + 4d of PartA- OI) 25

26 Total (14 + 15 + 16 + 17 + 18 + 19 + 20 + 21+22 +23+24+25) 26

27 Deduction allowable under section 32(1)(iii) 27

28 Amount allowable as deduction under section 32AC 28

29 Amount of deduction under section 35 or 35CCC or 35CCD in excess of the amount debited to profit and loss account (item x(4) of Schedule ESR) (if amount deductible under section 35 or 35CCC or 35CCD is lower than amount debited to P&L account, it will go to item 24) 29

30 Any amount disallowed under section 40 in any preceding previous year but allowable during the previous year(8B of Part A- OI) 30

31 Any amount disallowed under section 43B in any preceding previous year but allowable during the previous year (10i of Part A-OI) 31

32 Any other amount allowable as deduction 32

33 Decrease in profit or increase in loss on account of ICDS adjustments and deviation in method of valuation of stock (Column 3b + 4e of Part 33

34 Total (27+28+29+30+31+32+33) 34

35 Income (13+26-34) 35

36 Profits and gains of business or profession deemed to be under –

i Section 44AE (61(ii) of schedule P&L ) 36i

ii Section 44B 36ii

iii Section 44BB 36iii

iv Section 44BBA 36iv

va Section 44BBB 36va

vb Section 44BBC 36vb

vi Section 44D 36vi

vii Section 44DA 36vii (item 4 of Form 3CE)

viii Chapter-XII-G (tonnage) 36viii (total of col. 7 of item 10 of

ix First Schedule of Income-tax Act (other than 115B) 36ix

x Total (36i to 36ix) 36x

37 Net profit or loss from business or profession other than speculative and specified business (36+36x) 37

38 Net Profit or loss from business or profession other than speculative business and specified business after applying rule 7A, 7B or 8, if applicable (If rule 7A, 7B or 8 is not applicable, enter same figure as in 37) (If loss take the figure to 2i of item F) (38a+ 38b + 38c + 38d + 38e + 38f) A38

a Income chargeable under Rule 7 38a

b Deemed income chargeable under Rule 7A 38b

c Deemed income chargeable under Rule 7B(1) 38c

d Deemed income chargeable under Rule 7B(1A) 38d

e Deemed income chargeable under Rule 8 38e

f Income other than Rule 7A, 7B & 8 (Item No. 37) 38f

39 Balance of income deemed to be from agriculture, after applying Rule 7, 7A, 7B(1), 7B(1A) andRule 8 for the purpose of aggregation of income as per Finance Act [4c- (38a+38b+38c+38d+38e)] 39

B Computation of income from speculative business

40 Net profit or loss from speculative business as per profit or loss account 40

41 Additions in accor7dance with section 28 to 44DB 41

42 Deductions in accordance with section 28 to 44DB 42

43 Income from speculative business (40+41-42) (if loss, take the figure to 6xvii of schedule CFL) B43

C Computation of income from specified business under section 35AD

44 Net profit or loss from specified business as per profit or loss account 44

45 Additions in accordance with section 28 to 44DB 45

46 Deductions in accordance with section 28 to 44DB (other than deduction under section,- (i) 35AD, (ii) 32 or 35 on which deduction u/s 35AD is claimed) 46

47 Profit or loss from specified business (44+45-46) 47

48 Deductions in accordance with section 35AD(1) 48

49 Income from Specified Business) (47-48 )(if loss, take the figure to 7xvii of schedule CFL) C49

50 Relevant clause of sub-section (5) of section 35AD which covers the specified business (to be selected from drop down menu) C50

D Income chargeable under the head ‘Profits and gains from business or profession’ (A38+B43+C49)

E Intra head set off of business loss of current year

iva Income of Foreign Company from eligible business of selling raw

Schedule DPM Depreciation on Plant and Machinery (Other than assets on which full capital expenditure is allowable as deduction under any other section)

DEPRECIATION ON PLANT AND MACHINERY

1 Block of assets Plant and machinery

2 Rate (%) 15 30 40 45

(i) (ii) (iii) (iv)

3 Written down value on the first day of previous year

4 Additions for a period of 180 days or more in the previous year

5 Consideration or other realization during the previous year out of 3 or 4

6 Amount on which depreciation at full rate to be allowed (3 + 4 -5) (enter 0, if result is negative)

7 Additions for a period of less than 180 days in the previous year

8 Consideration or other realizations during the year out of 7

9 Amount on which depreciation at half rate to be allowed (7 – 8) (enter 0, if result is negative)

10 Depreciation on 6 at full rate

11 Depreciation on 9 at half rate

12 Additional depreciation, if any, on 4

13 Additional depreciation, if any, on 7

14 Additional depreciation relating to immediately preceding year on asset put to use for less than 180 days

15 Total depreciation (10+11+12+13+14)

16 Depreciation disallowed under section 38(2) of the I.T. Act (out of column 15)

17 Net aggregate depreciation (15-16)

18 Proportionate aggregate depreciation allowable in the event of succession, amalgamation, demerger etc. (out of column 17)

19 Expenditure incurred in connection with transfer of asset/ assets

20 Capital gains/ loss under section 50 (5 + 8 -3 – 4 -7 -19) (enter negative only, if block ceases to exist)

21 Written down value on the last day of previous year* (6+ 9 -15) (enter 0, if result is negative)

Schedule DOA Depreciation on other assets (Other than assets on which full capital expenditure is allowable as deduction)

DEPRECIATION ON OTHER ASSETS

1 Block of assets Land Building (not including land) Furniture and fittings Intangible assets Ships

2 Rate (%) Nil 5 10 40 10 25 20

(i) (ii) (iii) (iv) (v) (vi) (vii)

3 Written down value on the first day of previous year

4 Additions for a period of 180 days or more in the previous year

5 Consideration or other realization during the previous year out of 3 or 4

6 Amount on which depreciation at full rate to be allowed (3 + 4 -5) (enter 0, if result is negative) 7 Additions for a period of less than 180 days in the previous year

8 Consideration or other realizations during the year out of 7

9 Amount on which depreciation at half rate to be allowed (7-8) (enter 0, if result is negative)

10 Depreciation on 6 at full rate

11 Depreciation on 9 at half rate

12 Total depreciation (10+11)

13 Depreciation disallowed under section 38(2) of the I.T. Act (out of column 12)

14 Net aggregate depreciation (12-13)

15 Proportionate aggregate depreciation allowable in the event of succession, amalgamation, demerger etc. (out of column 14)

16 Expenditure incurred in connection with transfer of asset/ assets

17 Capital gains/ loss under section 50* (5 + 8 -3-4 -7 -16) (enter negative only if block ceases to exist) 18 Written down value on the last day of previous year* (6+ 9 -12) (enter 0 if result is negative)

Schedule DEP Summary of depreciation on assets (Other than on assets on which full capital expenditure is allowable as deduction under any other section)

SUMMARY OF DEPRECIATION ON ASSETS

1 Plant and machinery

a Block entitled for depreciation @ 15 per cent( Schedule DPM – 17i or 18i as applicable) 1a

b Block entitled for depreciation @ 30 per cent( Schedule DPM – 17ii or 18ii as applicable) 1b

c Block entitled for depreciation @ 40 per cent( Schedule DPM – 17iii or 18iii as applicable) 1c

d Block entitled for depreciation @ 45 per cent( Schedule DPM – 17iv or 18iv as applicable) 1d

e Total depreciation on plant and machinery ( 1a + 1b + 1c+1d) 1e

2 Building (not including land)

a Block entitled for depreciation @ 5 per cent(Schedule DOA- 14ii or 15ii as applicable) 2a

b Block entitled for depreciation @ 10 per cent(Schedule DOA- 14iii or 15iii as applicable) 2b

c Block entitled for depreciation @ 40 per cent(Schedule DOA- 14iv or 15iv as applicable) 2c

d Total depreciation on building (2a+2b+2c) 2d

3 Furniture and fittings(Schedule DOA- 14v or 15v as applicable) 3

4 Intangible assets (Schedule DOA- 14vi or 15vi as applicable) 4

5 Ships (Schedule DOA- 14vii or 15vii as applicable) 5

6 Total depreciation ( 1e+2d+3+4+5) 6

Schedule DCG Deemed Capital Gains on sale of depreciable assets

1 Plant and machinery

a Block entitled for depreciation @ 15 per cent(Schedule DPM – 20i) 1a

b Block entitled for depreciation @ 30 per cent(Schedule DPM – 20ii) 1b

c Block entitled for depreciation @ 40 per cent(Schedule DPM – 20iii) 1c

d Block entitled for depreciation @ 45 per cent(Schedule DPM – 20iii) 1d

e Total ( 1a +1b + 1c+1e) 1e

2 Building (not including land)

a Block entitled for depreciation @ 5 per cent(Schedule DOA- 17ii) 2a

b Block entitled for depreciation @ 10 per cent(Schedule DOA- 17iii) 2b

c Block entitled for depreciation @ 40 per cent(Schedule DOA- 17iv) 2c

d Total ( 2a + 2b + 2c) 2d

3 Furniture and fittings ( Schedule DOA- 17v) 3

4 Intangible assets (Schedule DOA- 17vi) 4

5 Ships (Schedule DOA- 17vii) 5

6 Total ( 1e+2d+3+4+5) 6

Schedule ESR Expenditure on scientific Research etc. (Deduction under section 35 or 35CCC or 35CCD)

Sl No Expenditure of the nature referred to in section

(1) Amount, if any, debited to profit and loss account

(2) Amount of deduction allowable

(3) Amount of deduction in excess of the amount debited to profit and loss account (4) = (3) – (2)

i 35(1)(i)

ii 35(1)(ii)

iii 35(1)(iia)

iv 35(1)(iii)

v 35(1)(iv)

vi 35(2AA)

vii 35(2AB)

viii 35CCC

ix 35CCD

x Total

NOTE In case any deduction is claimed under sections 35(1)(ii) or 35(1)(iia) or 35(1)(iii) or 35(2AA), please provide the details as per Schedule RA.

Schedule CG Capital Gains

CAPITAL GAINS

A Short-term Capital Gains (STCG) (Sub-items 4 & 5 are not applicable for residents)

Short-term Capital Gains

1 From sale of land or building or both (fill up details separately for each property)(in case of co- ownership, enter your share of capital gain)

Date of purchase/ acquisition DD/MM/YYYY Date of sale/transfer DD/MM/YYYY

a i Full value of consideration received/receivable ai

ii Value of property as per stamp valuation authority aii

iii Full value of consideration adopted as per section 50C for the

purpose of Capital Gains [in case (aii) does not exceed 1.10 times (ai), take this figure as (ai), or else take (aii)] aiii

b Deductions under section 48

i Cost of acquisition without indexation bi

ii Cost of Improvement without indexation bii

iii Expenditure wholly and exclusively in connection with transfer biii

iv Total (bi + bii + biii) biv

c Balance (aiii – biv) 1c

d Deduction under section/ 54G/54GA (Specify details in item D below) 1d

e Short-term Capital Gains on Immovable property (1c – 1d) A1e

F In case of transfer of immovable property, please furnish the following details (see note)

S.No. Name of buyer(s) PAN/Aadhaar No. of buyer(s) Percentage share Amount Address

NOTE

► Furnishing of PAN/Aadhaar No. is mandatory, if the tax is deduced under section 194-IA or is quoted by buyer in the documents.

In case of more than one buyer, please indicate the respective percentage share and amount.

2 From slump sale

A i Fair market value as per Rule 11UAE(2) 2ai

ii Fair market value as per Rule 11UAE(3) 2aii

iii Full value of consideration (higher of ai or aii) 2aiii

B Net worth of the under taking or division 2b

C Short term capital gains from slump sale (2aiii-2b) A2c

3 From sale of equity share or unit of equity oriented Mutual Fund (MF) or unit of a business trust on which STT is paid under section 111A or 115AD(1)(b)(ii) proviso (for FII) (where A4 is not applicable)

Where transfer before 23rd July 2024 Where transfer on or after 23rd July 2024

a Full value of consideration 3a

b Deductions under section 48

i Cost of acquisition without indexation bi

ii Cost of Improvement without indexation bii

iii Expenditure wholly and exclusively in connection with transfer biii

iv Total (i + ii + iii) biv

c Balance (3a – biv) 3c

d Loss to be disallowed u/s 94(7) or 94(8)- for example if asset bought/acquired within 3 months prior to record date and dividend/income/bonus units are received, then loss arising out of sale of such asset to be ignored (Enter positive value only) 3d

e Short-term capital gain on equity share or equity oriented MF (STT paid) (3c+3d) 3ei 3eii A3e

4 For NON-RESIDENT, not being an FII- from sale of shares or debentures of an Indian company (to be computed with foreign exchange adjustment under first proviso to section 48)

a STCG on transactions covered u/s 111A (A4ai + A4aii) A4a

i Where the transfer was before 23rd July 2024 A4ai

ii Where the transfer was on or after 23rd July 2024 A4aii

b STCG from sale of shares not covered in sl.no. 4a or sale of debentures A4b

5 For NON-RESIDENTS- from sale of securities (other than those at A3 above) by an FII as per section 115AD

a i In case securities sold include shares of a company other than quoted shares, enter the following details

a Full value of consideration received/receivable in respect of unquoted shares ia

b Fair market value of unquoted shares determined in the prescribed manner ib c Full value of consideration in respect of unquoted shares adopted as per section 50CA for the purpose of Capital Gains (higher of a ic

ii Full value of consideration in respect of securities other than unquoted shares aii

iii Total (ic + ii) aiii

b Deductions under section 48

i Cost of acquisition without indexation bi

ii Cost of improvement without indexation bii

iii Expenditure wholly and exclusively in connection with transfer biii

iv Total (i + ii + iii) biv

c Balance (5aiii – biv) 5c