What is the ITR 2 Form?

The ITR-2 is filed by individuals or HUFs not having income from profit or gains of business or profession and to whom ITR-1 is not applicable. It includes income from capital gains, foreign income, or any agricultural income of more than Rs 5,000.

- What is ITR 2 Form

- Eligibility File ITR 2 Online AY 2026-27

- File ITR 2 Via Gen IT Software

- ITR 2 Due Date for AY 2025-26

- Structure of ITR 2 Filing

- ITR 2 Form Filing Online and Offline Mode

Latest Update

- Now, taxpayers can download the Excel-based utility, JSON schema, and validation for ITR-2 AY 2026-27 from the official e-Filing portal. Download now

ITR 2 Filing Start Date for Taxpayers

The Income Tax Department has not yet started online filing for the ITR-2 form.

Eligible Taxpayers for Filing ITR 2 Online AY 2026-27

The taxpayers who are eligible for filing the ITR-2 form are the persons whose source of income is as mentioned below:

- A resident having any asset located outside India or a signing authority in any account.

- A non-resident or non-ordinary resident.

- Taxpayers who earn agricultural income above Rs. 5000/-.

- Income from winnings of a lottery, horse race, gambling, etc., under the head of other sources.

- Both short and long-term capital gains/losses from the sale of property/investments/securities. (if there is only long term capital gain exempt u/s 10(38) then ITR-1 can be filed)

The taxpayers who are not eligible to file the ITR-2 form are as follows:

- Taxpayers who earn from a business or profession

- Taxpayers who are eligible to file an Income Tax Return 1.

File ITR 2 Via Gen IT Software, Get Demo!

Due Date for Filing ITR 2 Online AY 2026-27

| Financial Year | Due Date |

|---|---|

| FY 2025-26 (AY 2026-27) | 31st July 2026 |

| FY 2024-25 (AY 2025-26) | |

| FY 2023-24 (AY 2024-25) | 31st July 2024 |

Every year, on or before 31st July, is termed as the last date for filing ITR 2.

Note: ITR-2 form corrigendum via Notification No. 58/2026. Read More

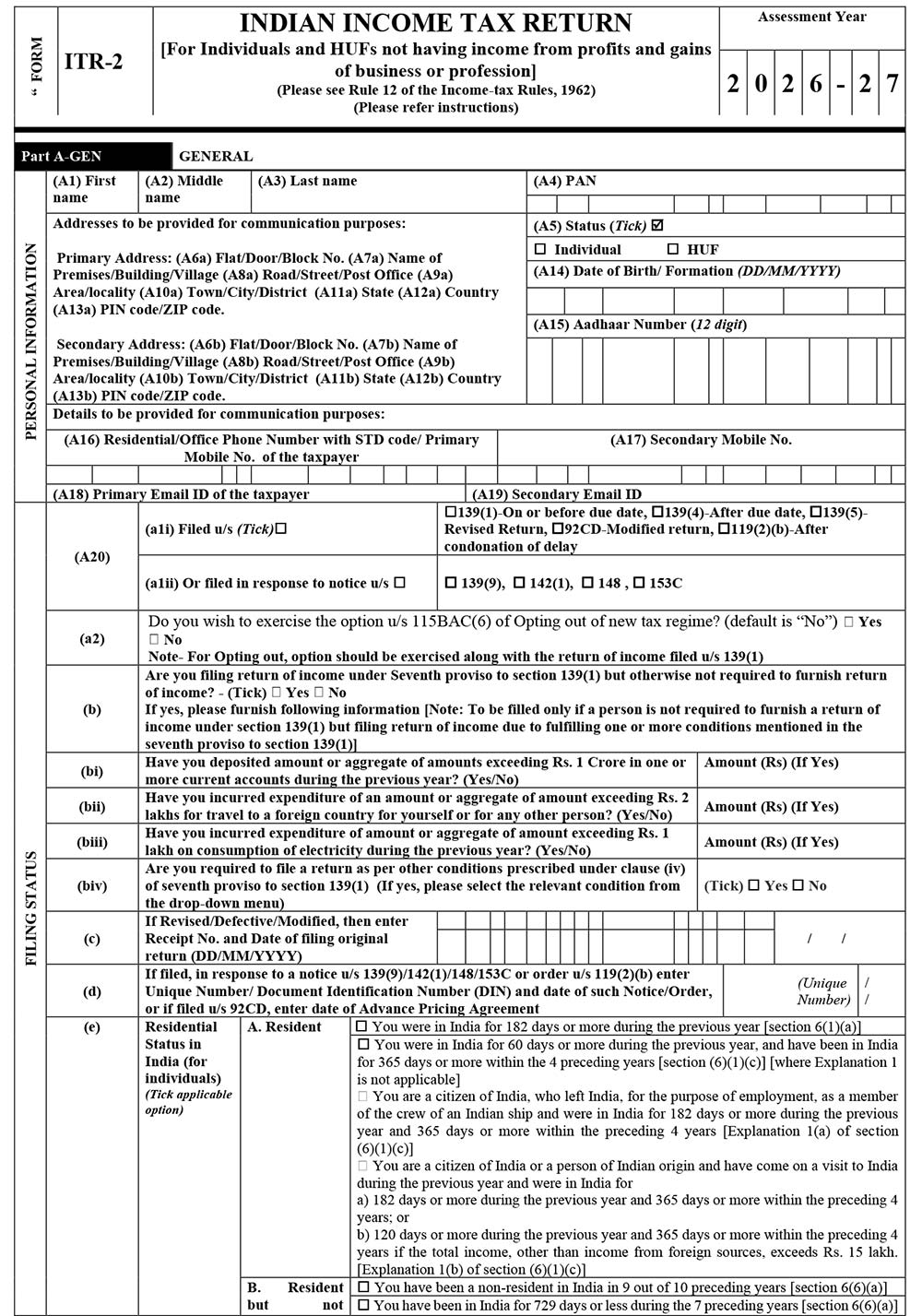

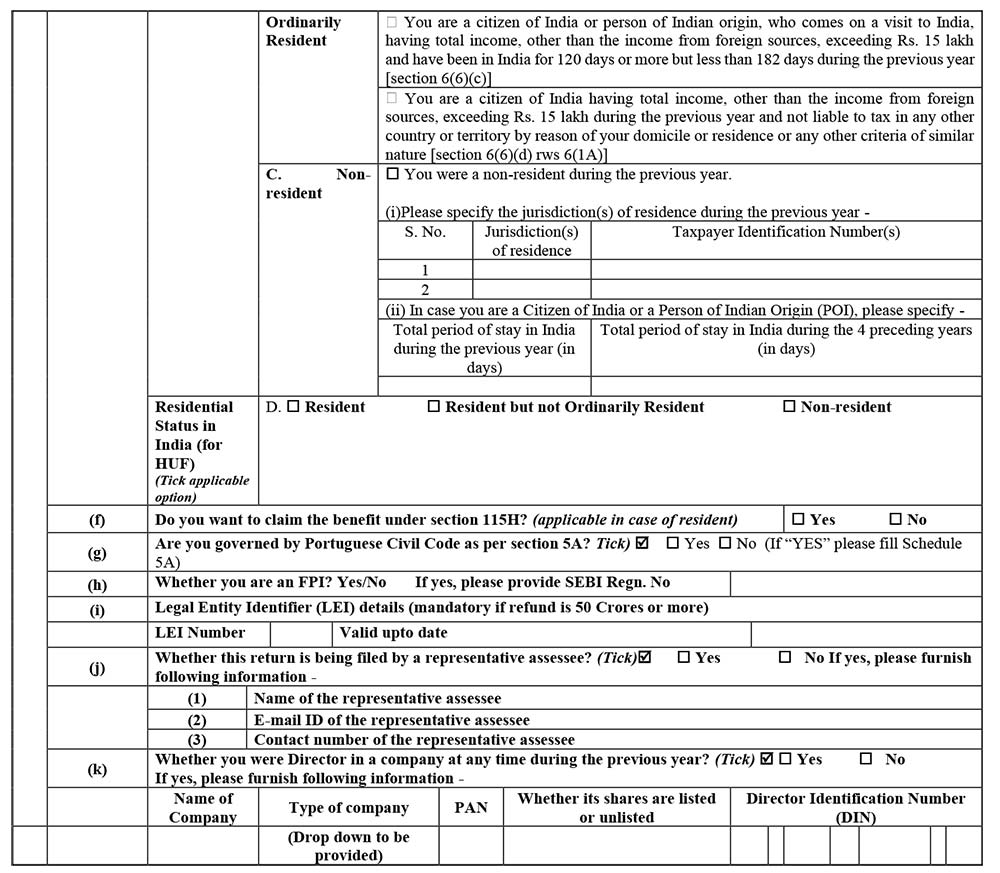

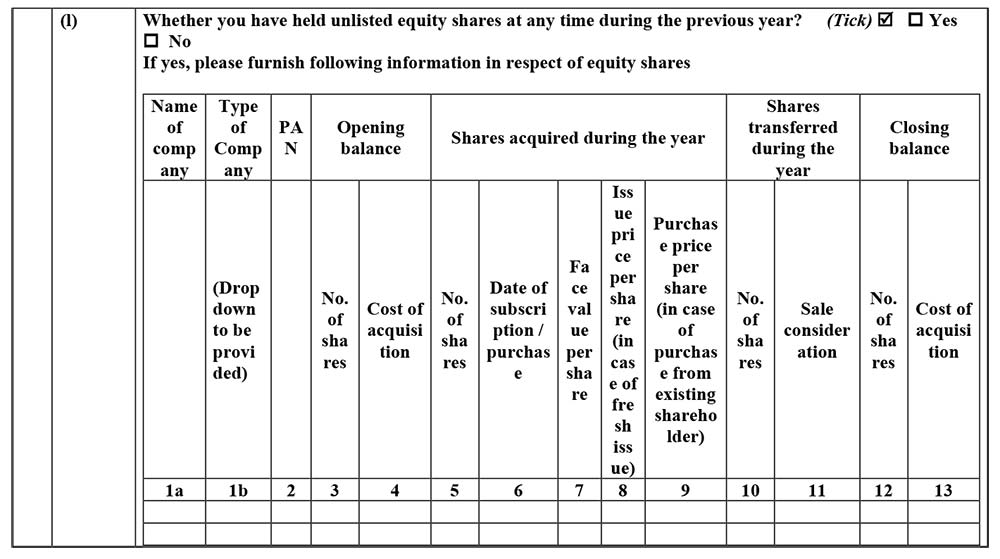

Structure of ITR 2 Filing for AY 2026-27 Online

Part A: General Information

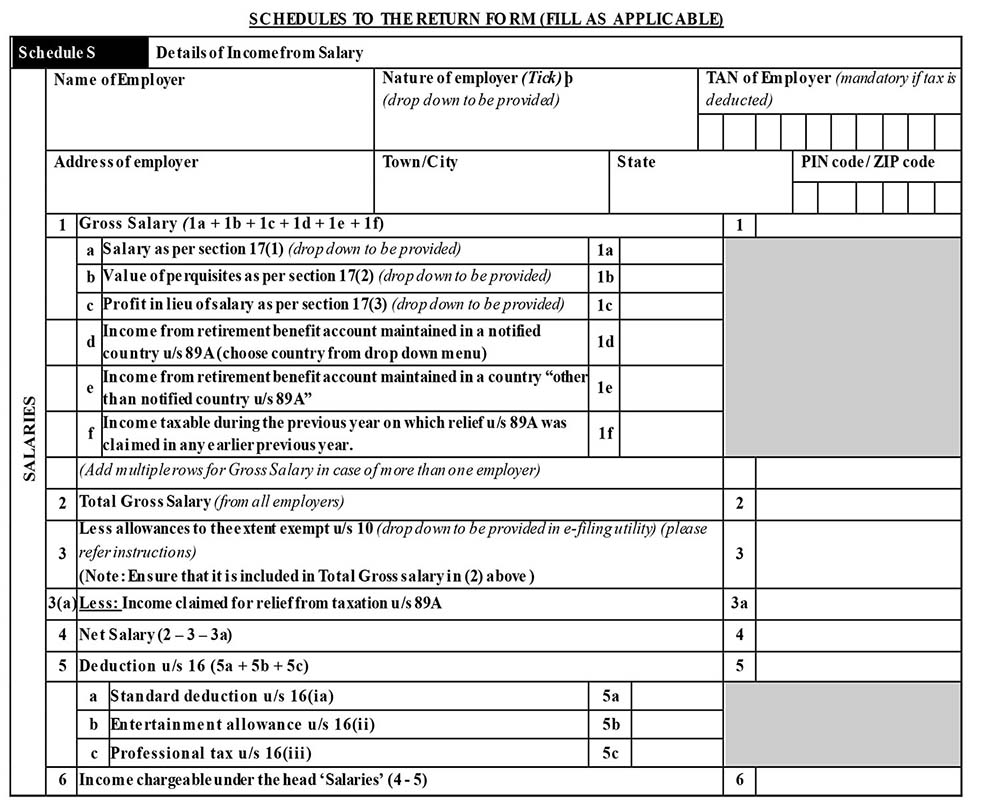

Schedule S: Details of Income from Salary

Schedule HP: Details of Income from House Property

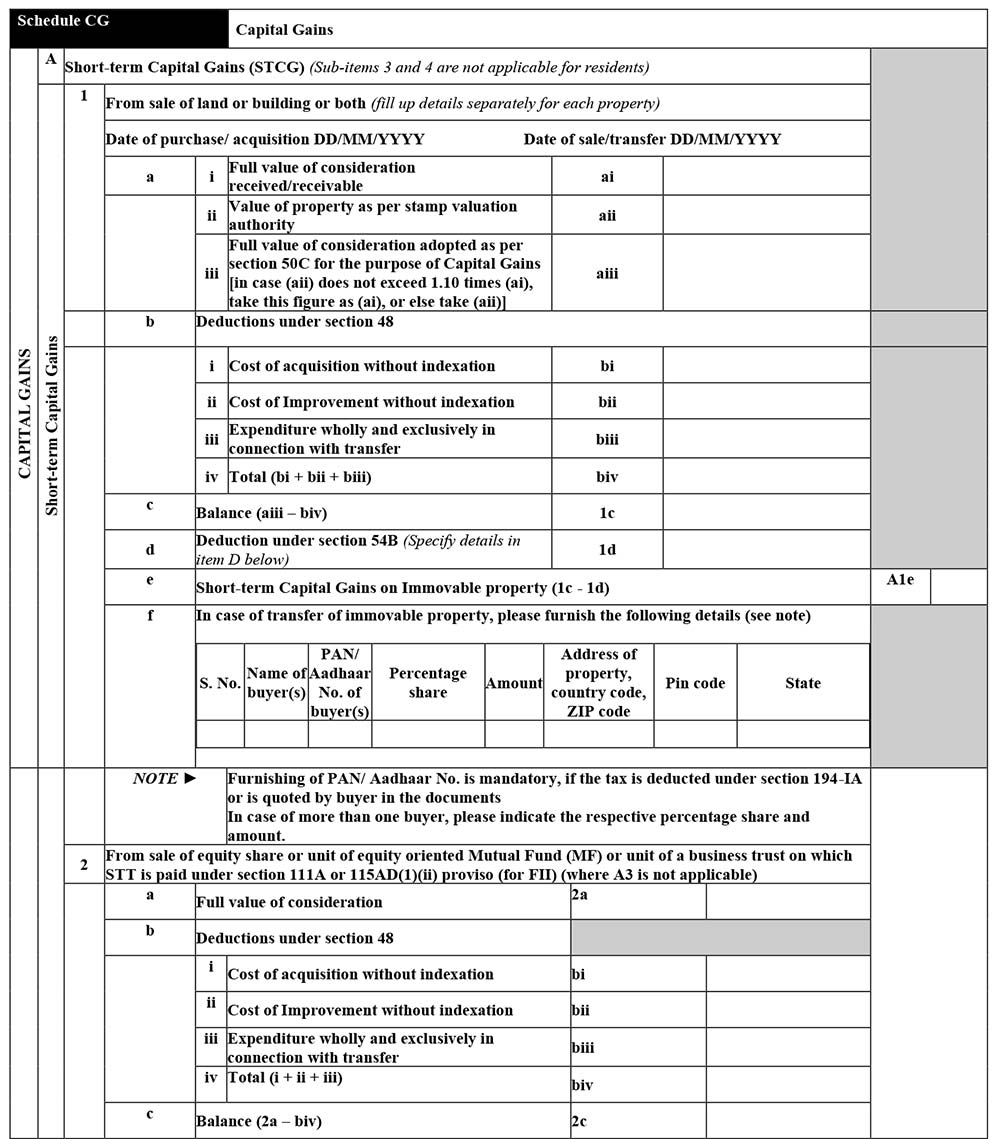

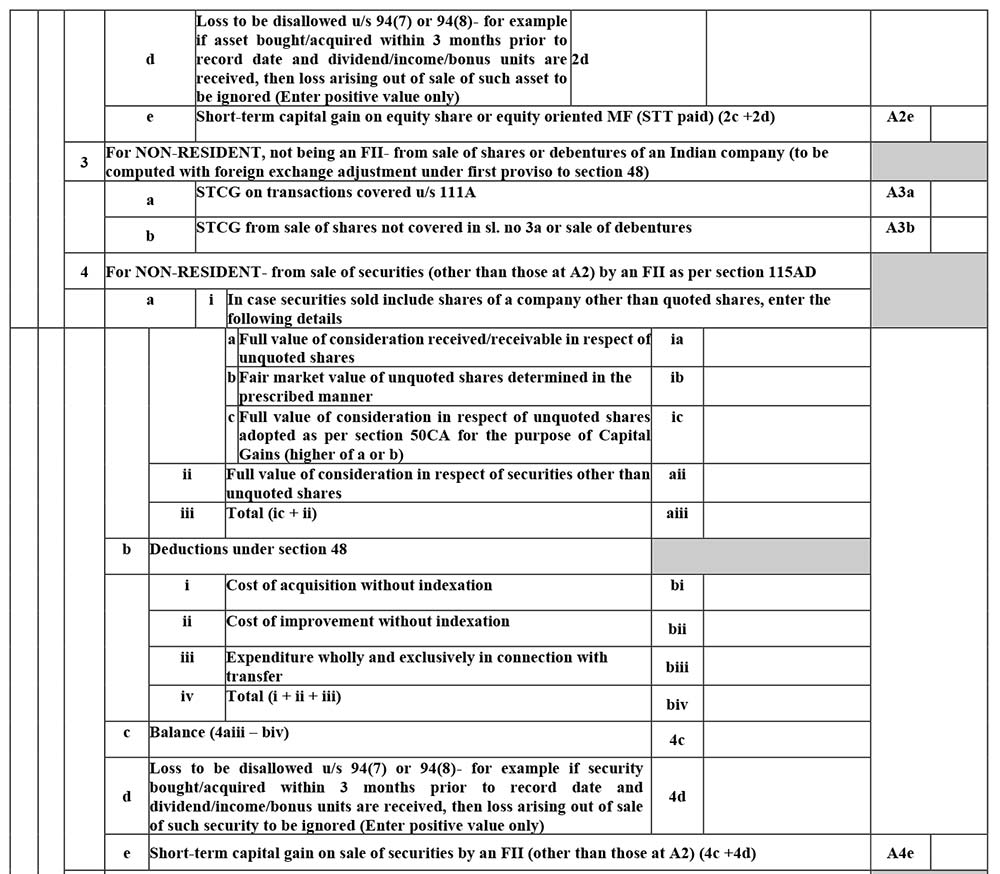

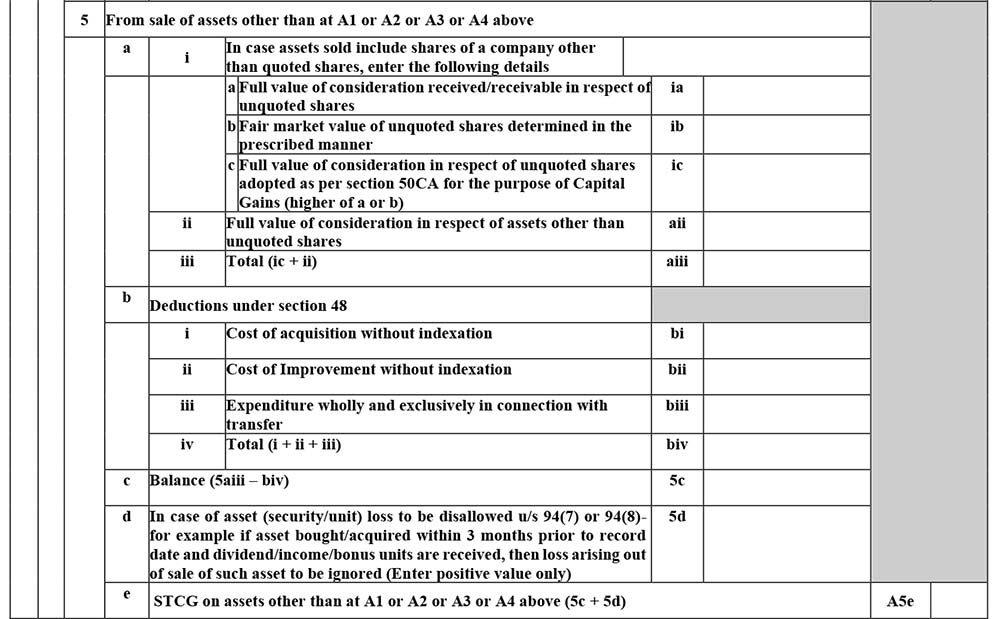

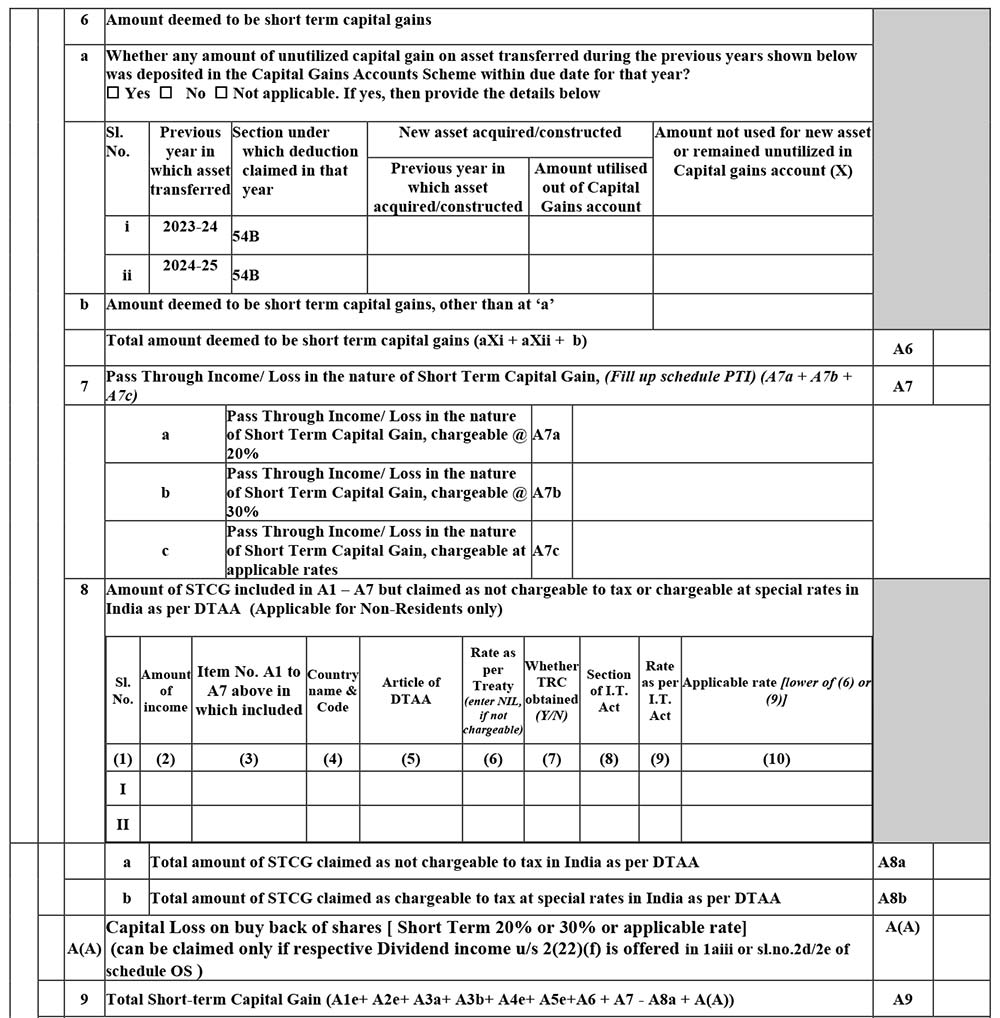

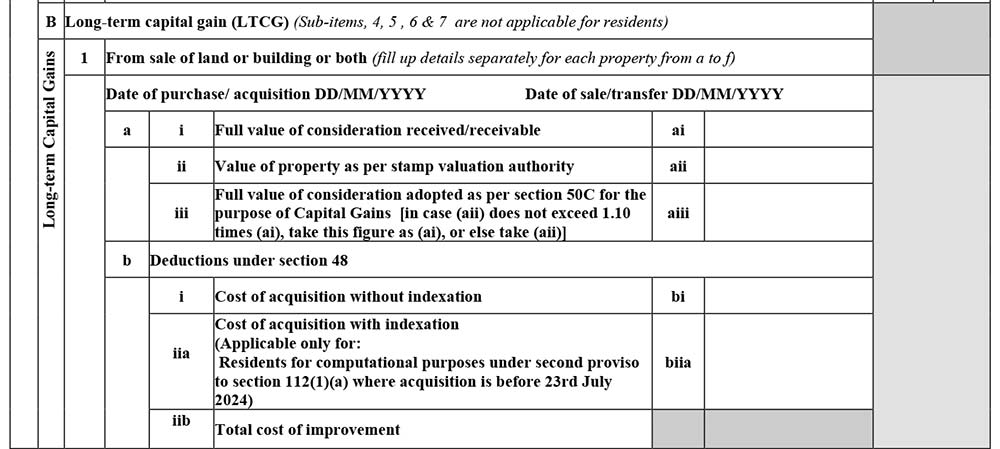

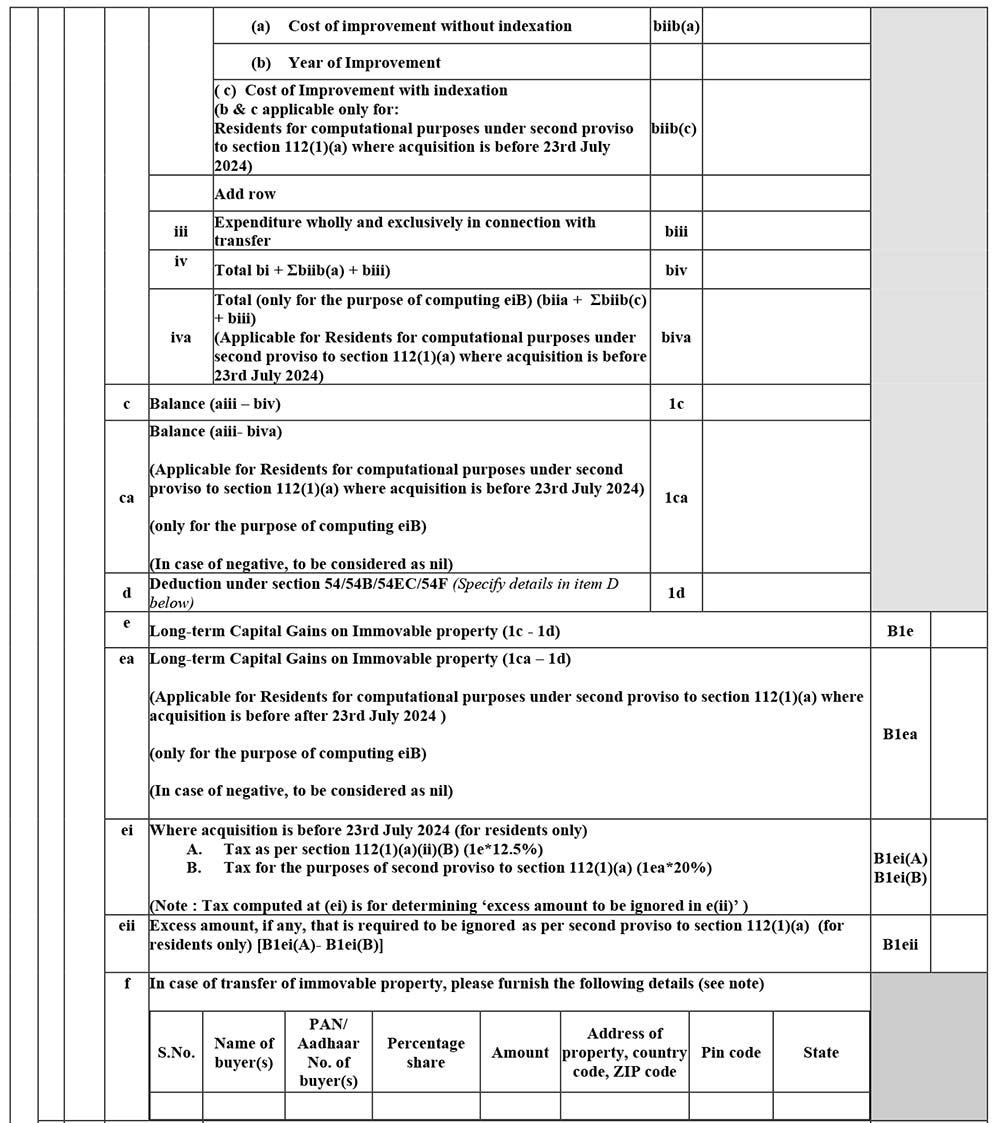

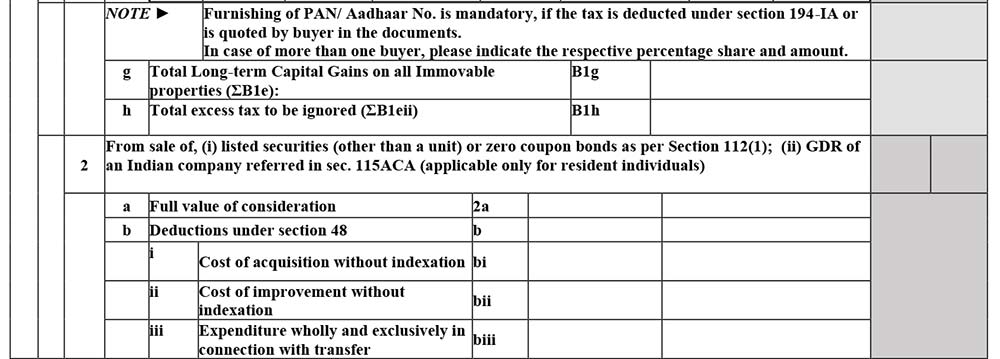

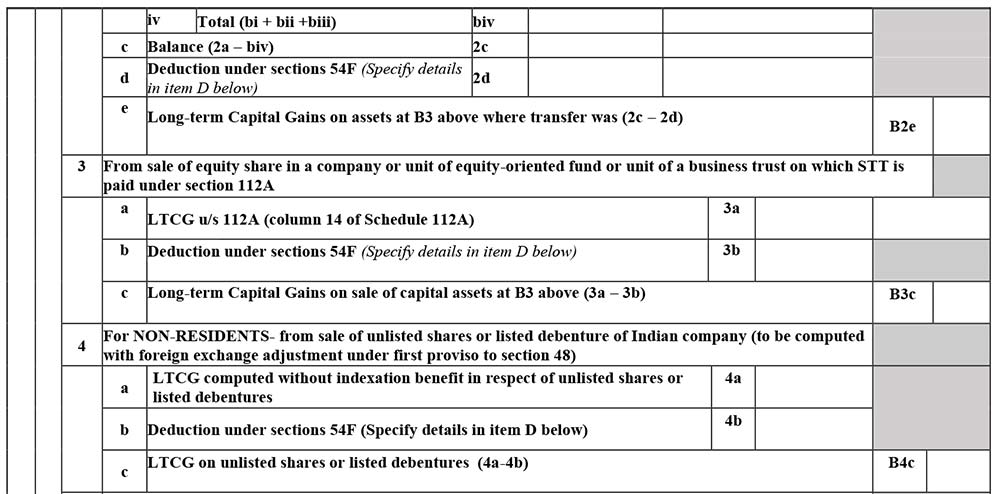

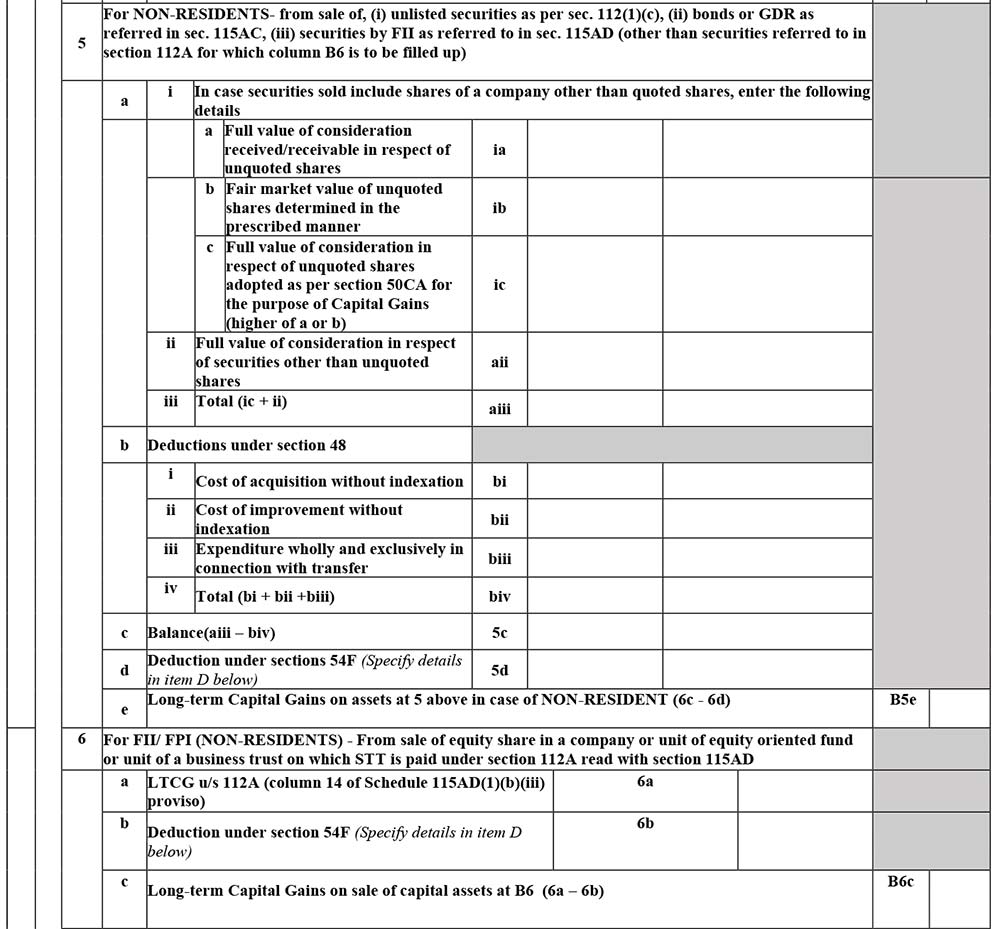

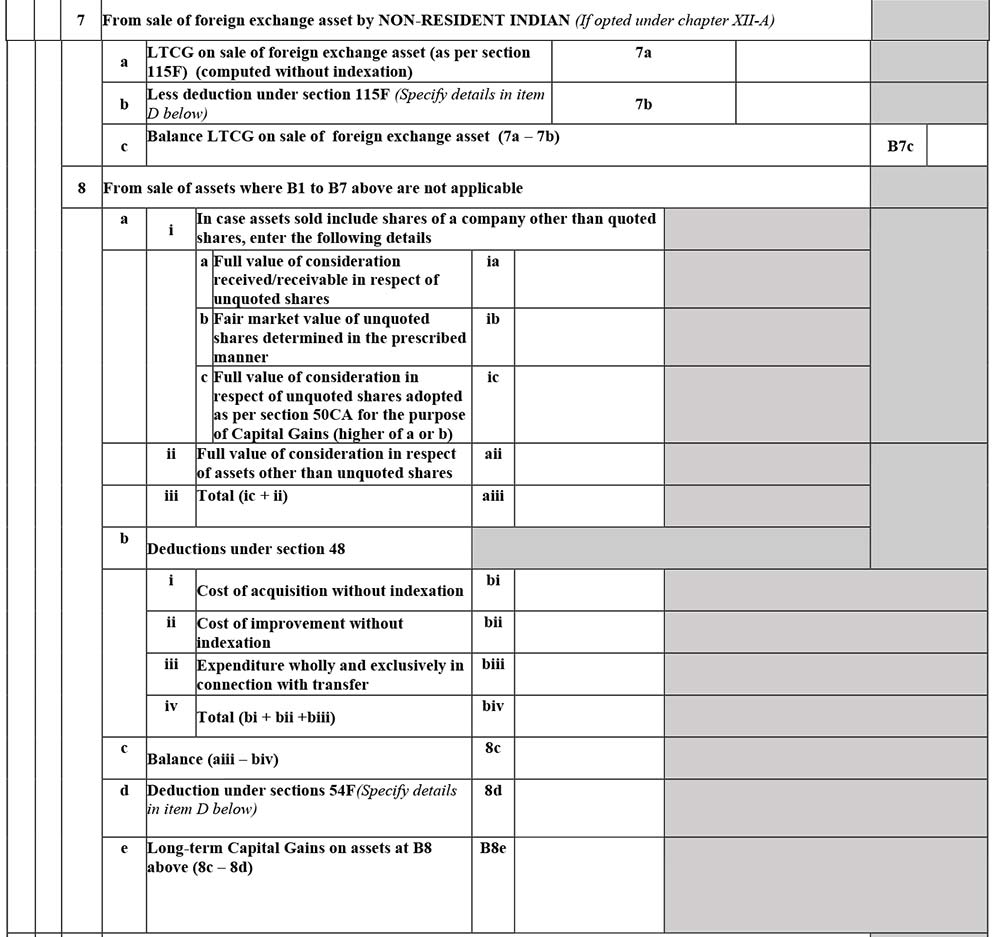

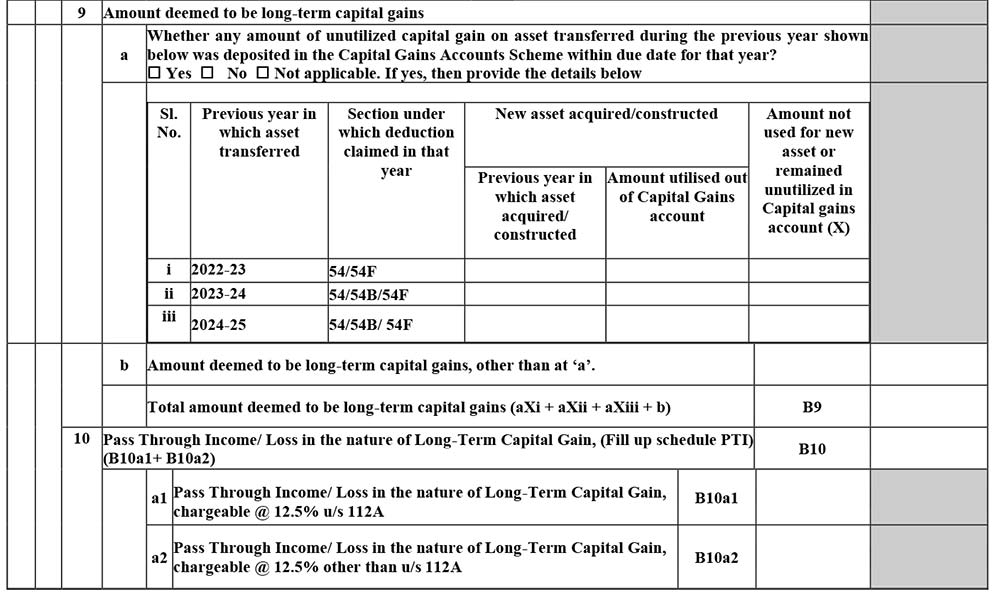

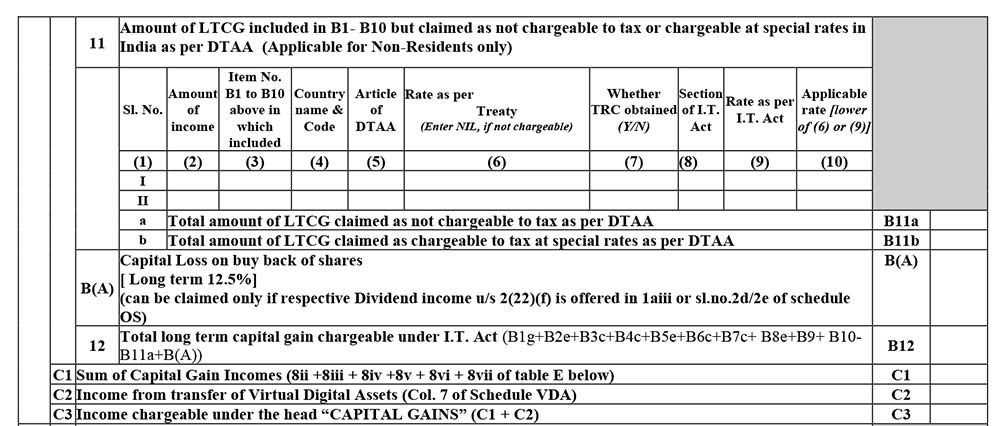

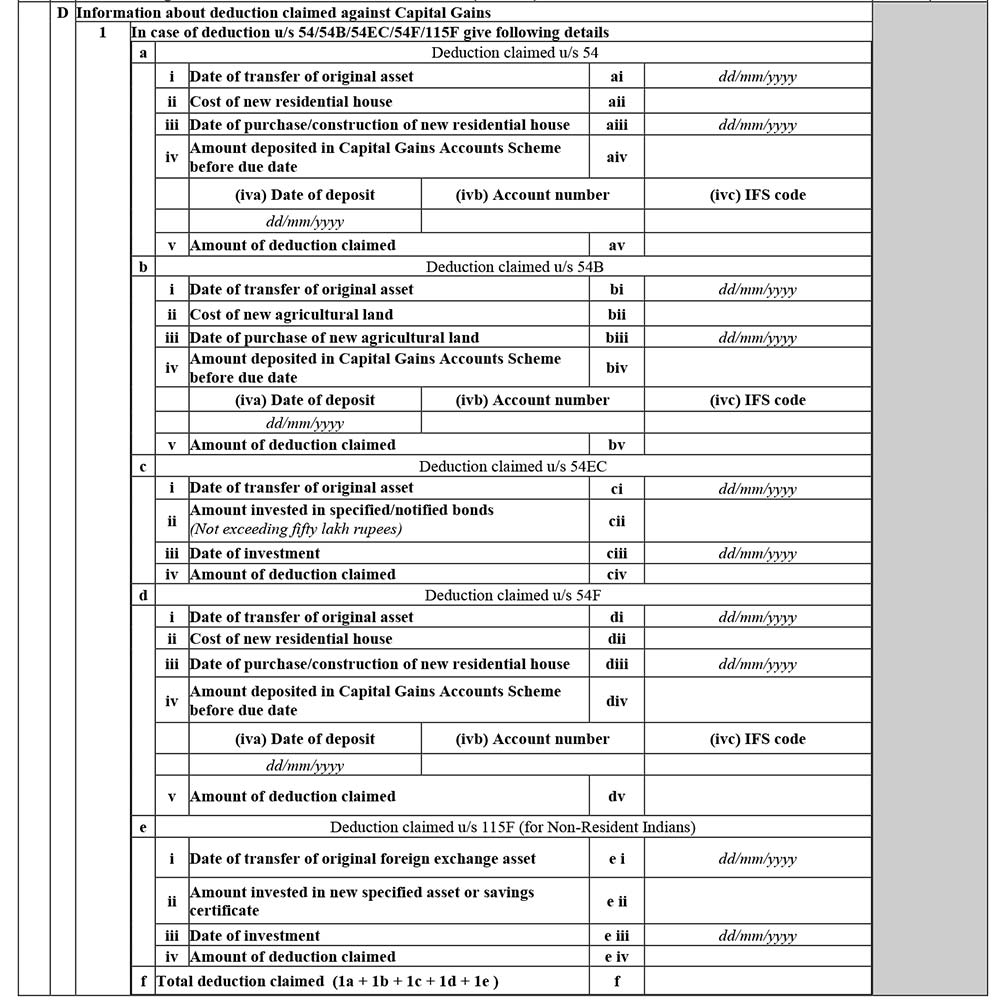

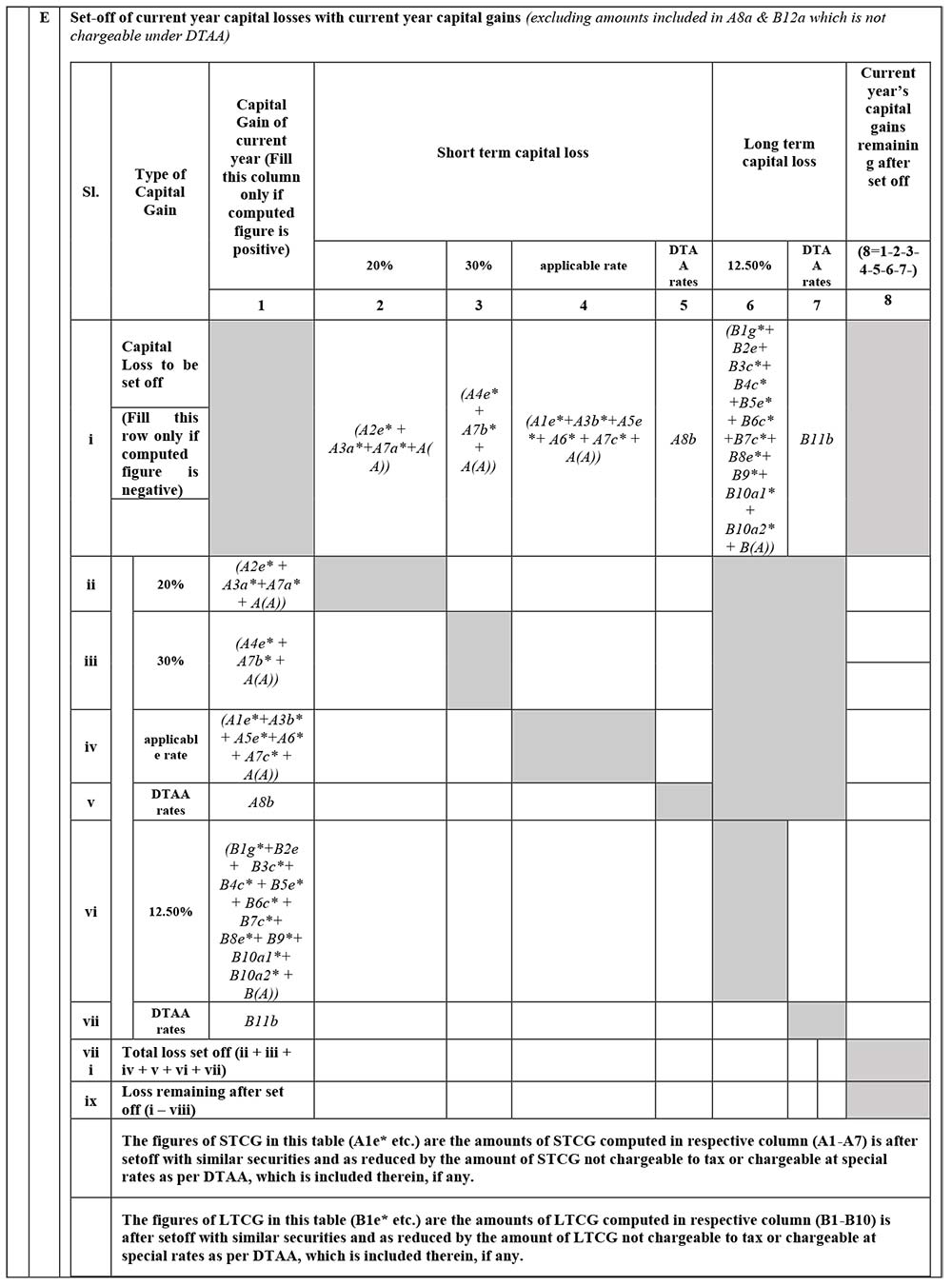

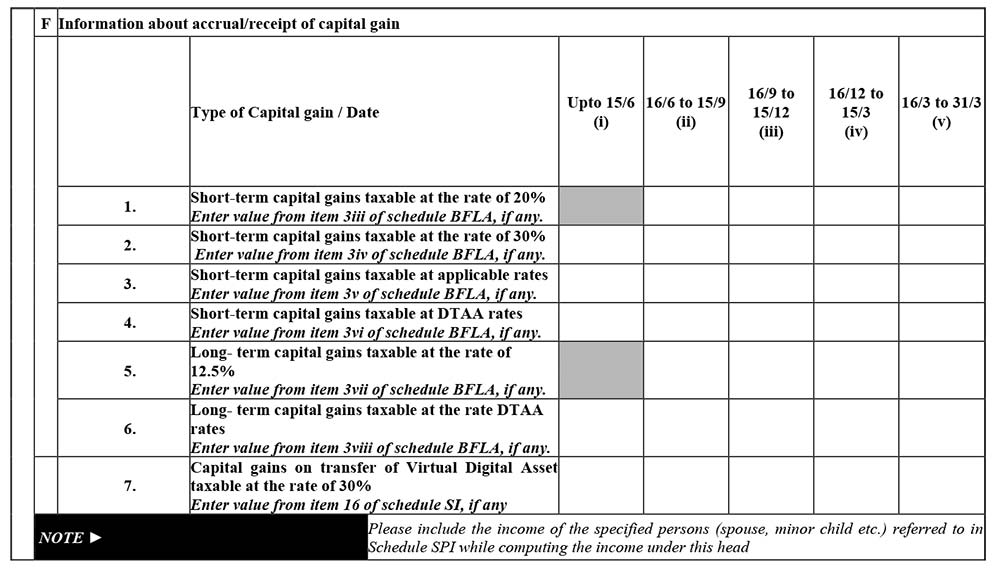

Schedule CG: Capital Gains

The information regarding Capital gains is enclosed with the following details of the taxpayer to furnish:

A. Short-term Capital Gains (STCG)

B. Long-term capital gain (LTCG)

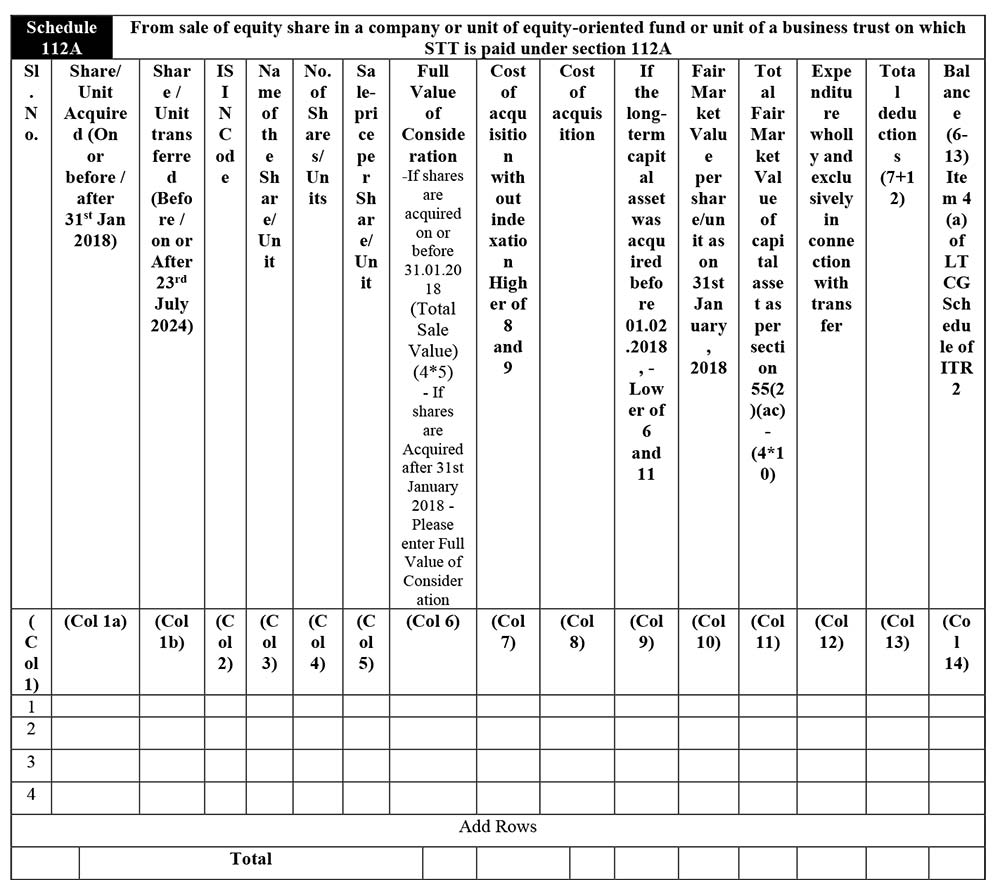

Schedule 112A:

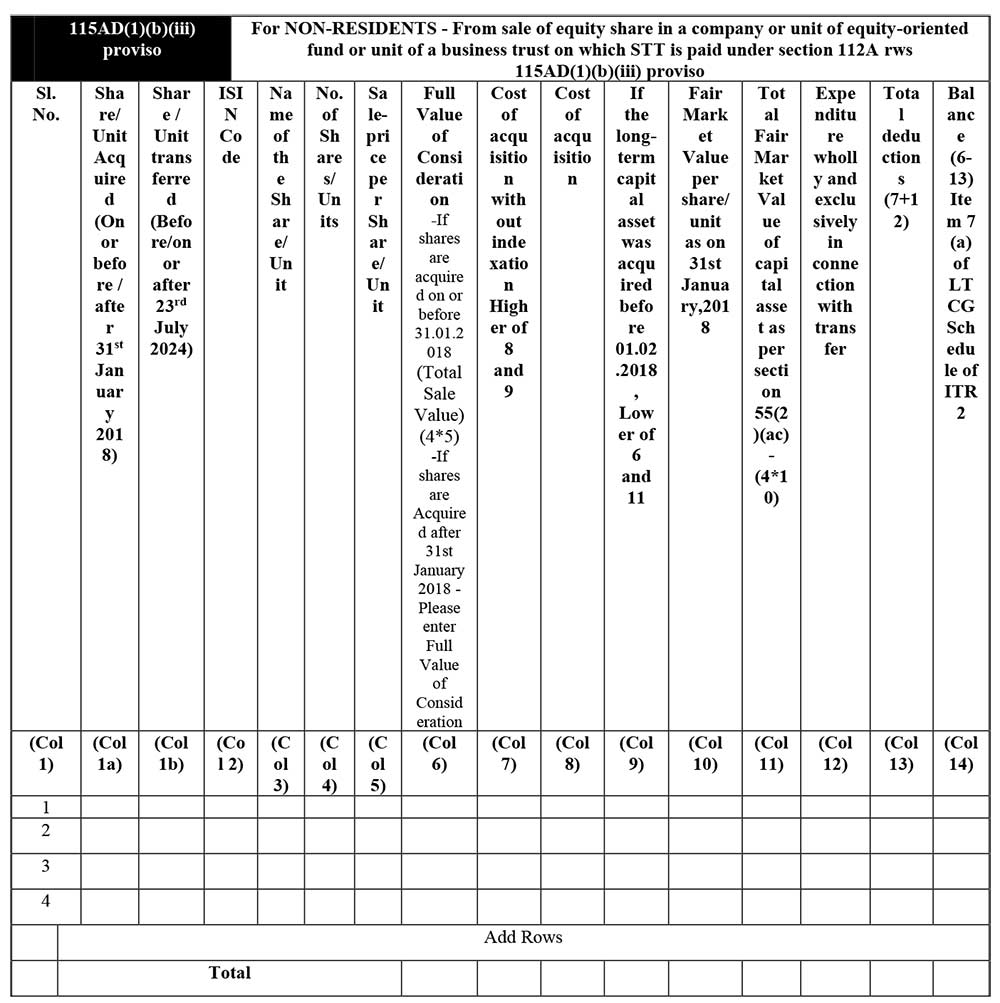

115AD(1)(b)(iii) proviso

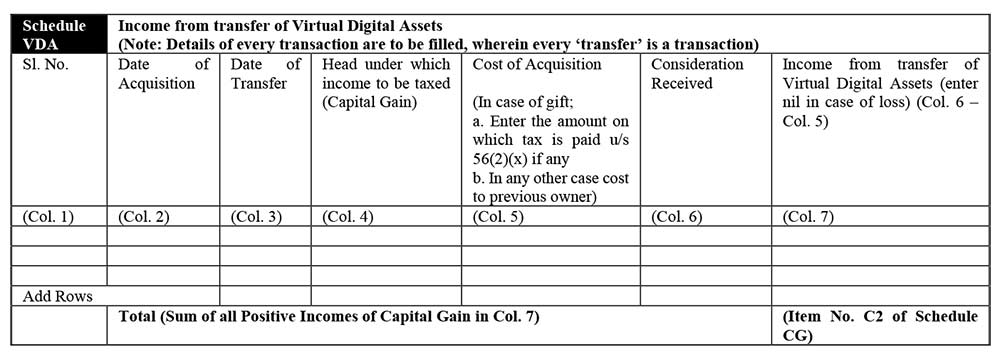

Schedule VDA

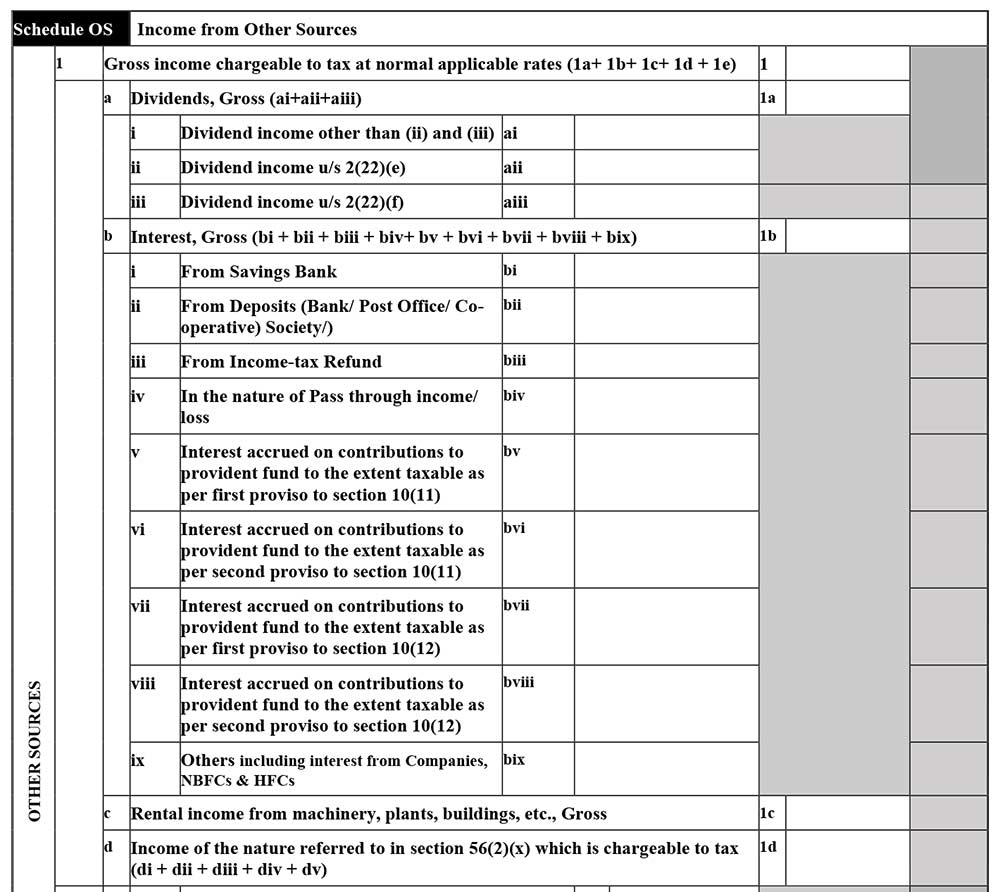

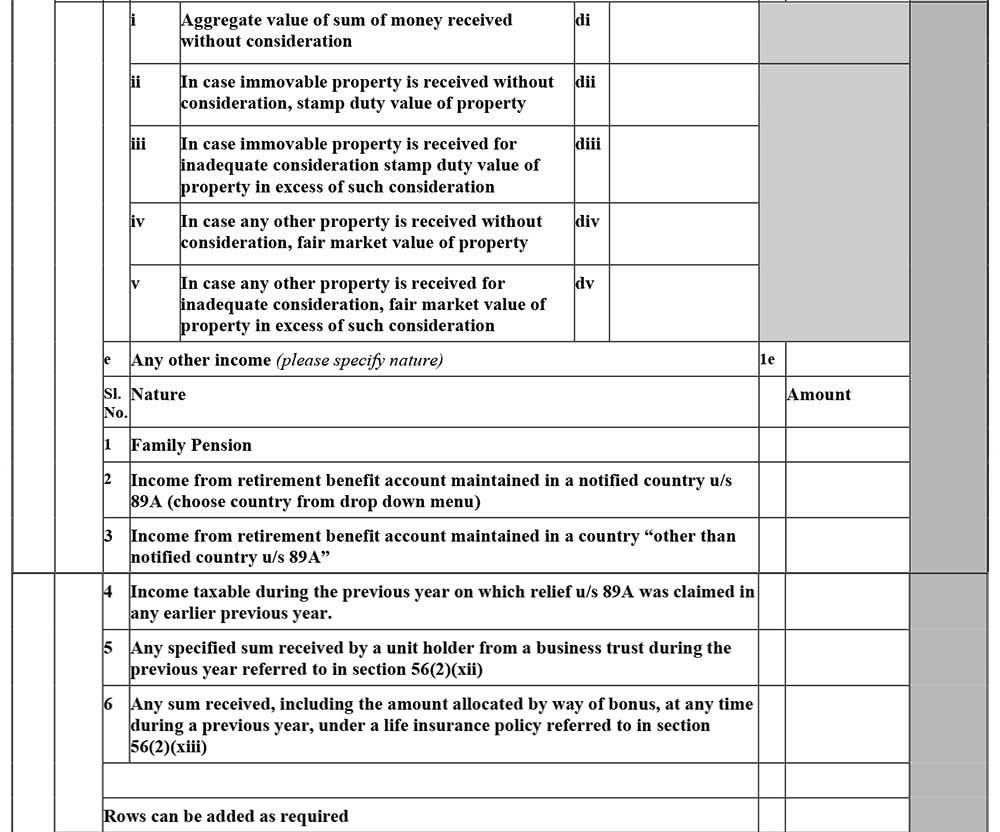

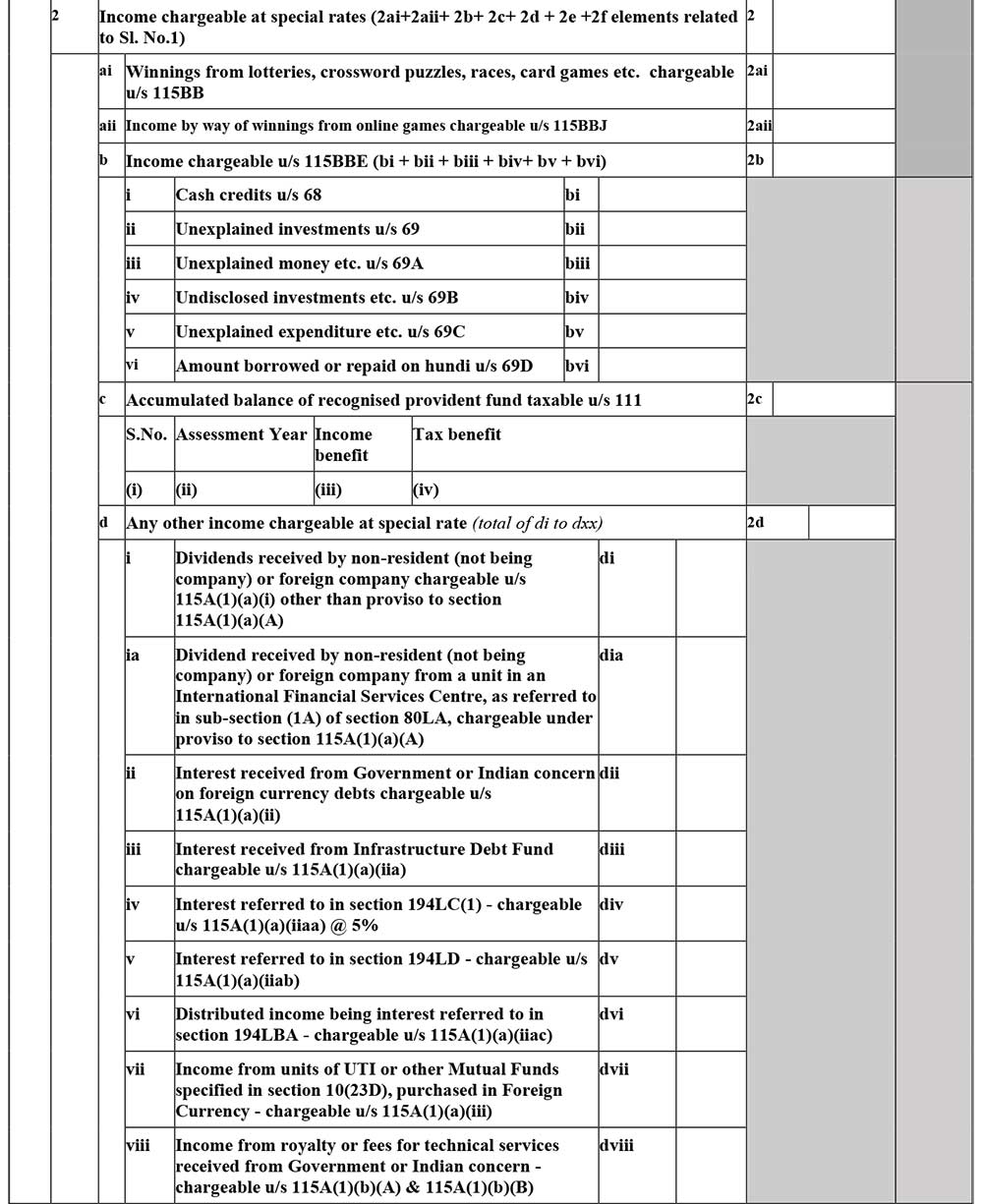

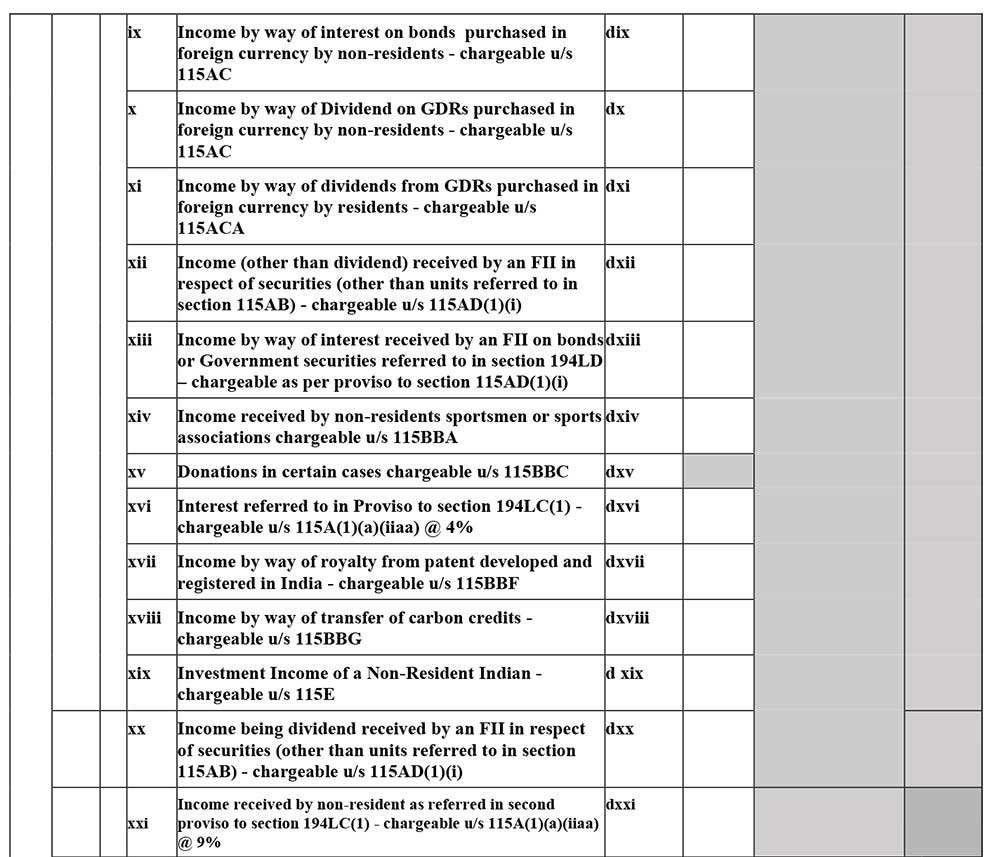

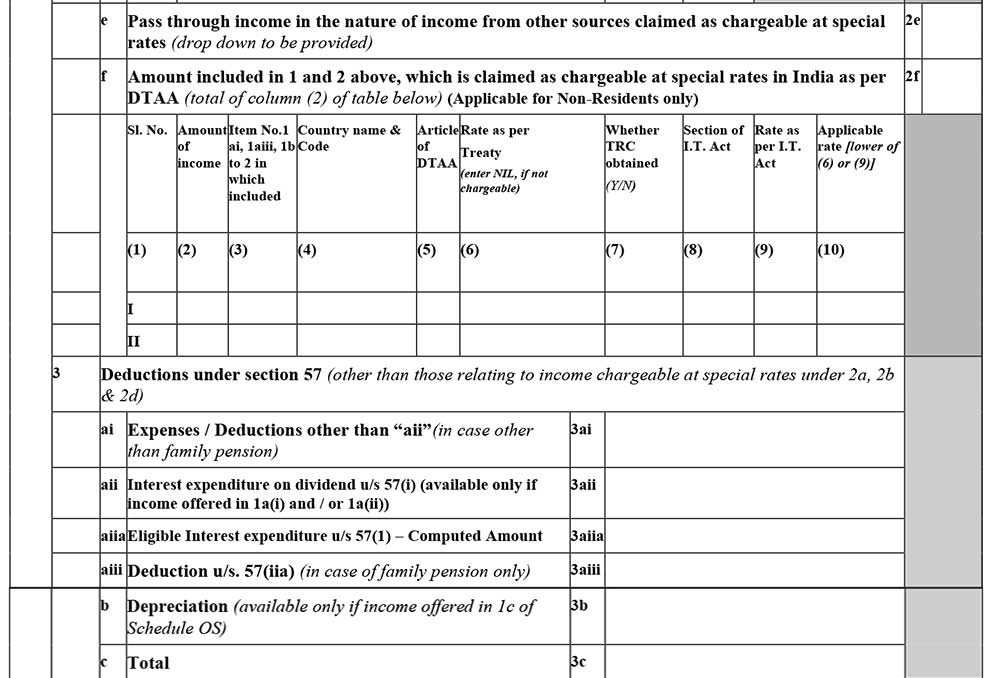

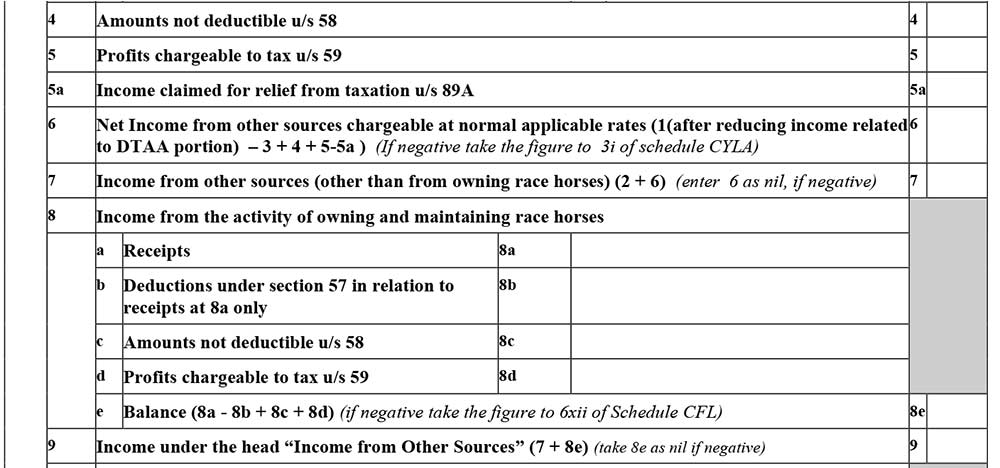

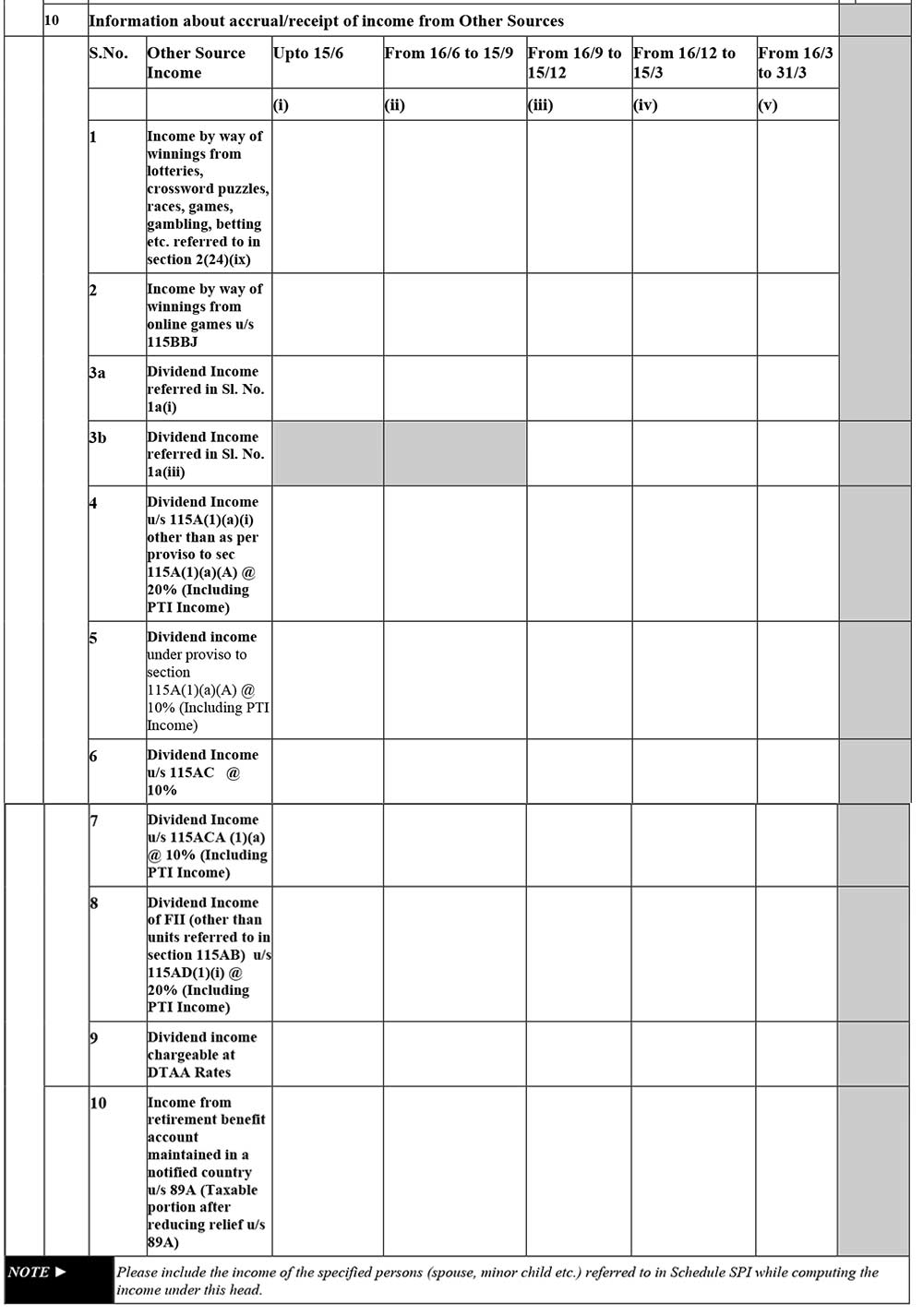

Schedule OS:

- Income from other sources: The information regarding income from other sources is enclosed.

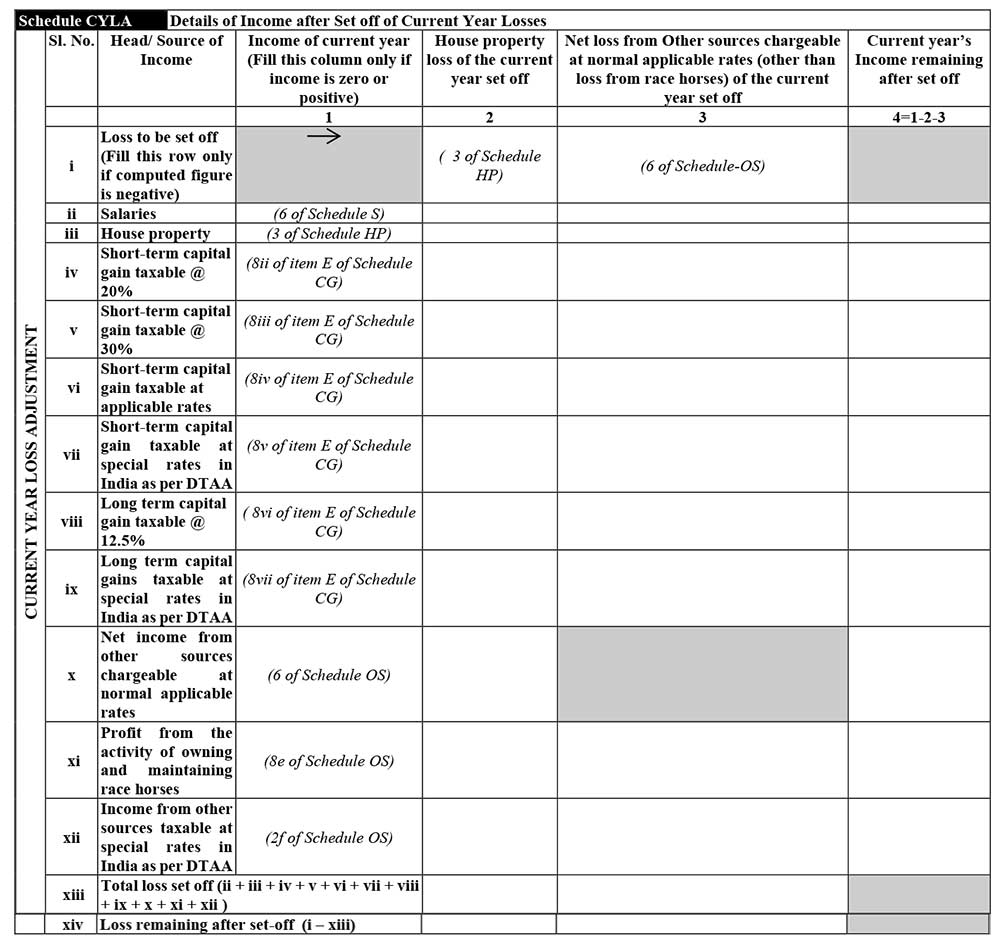

Schedule CYLA:

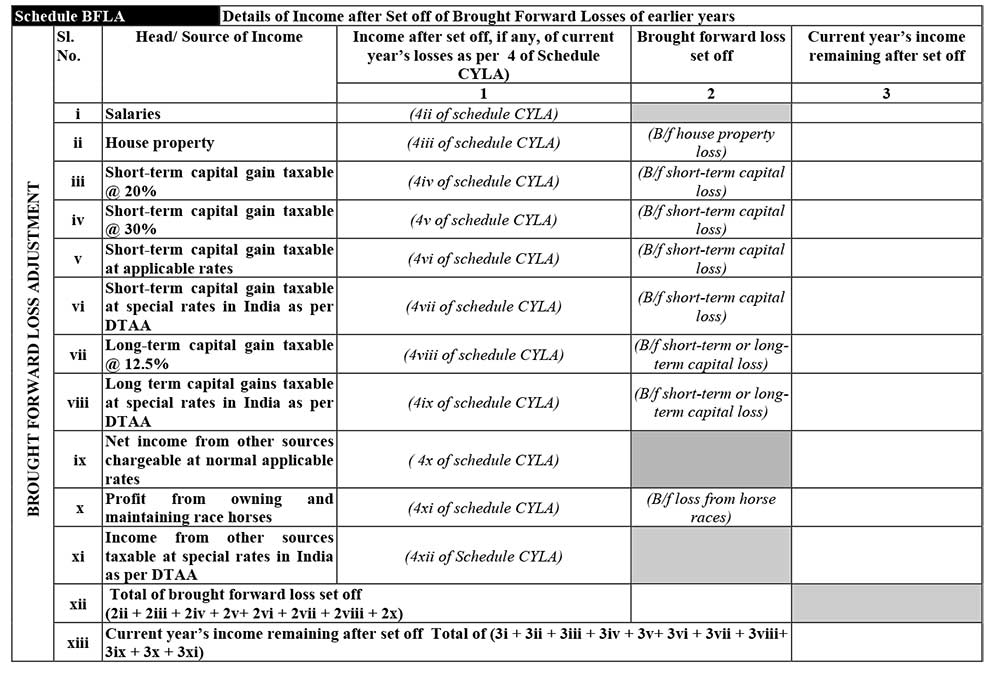

Schedule BFLA:

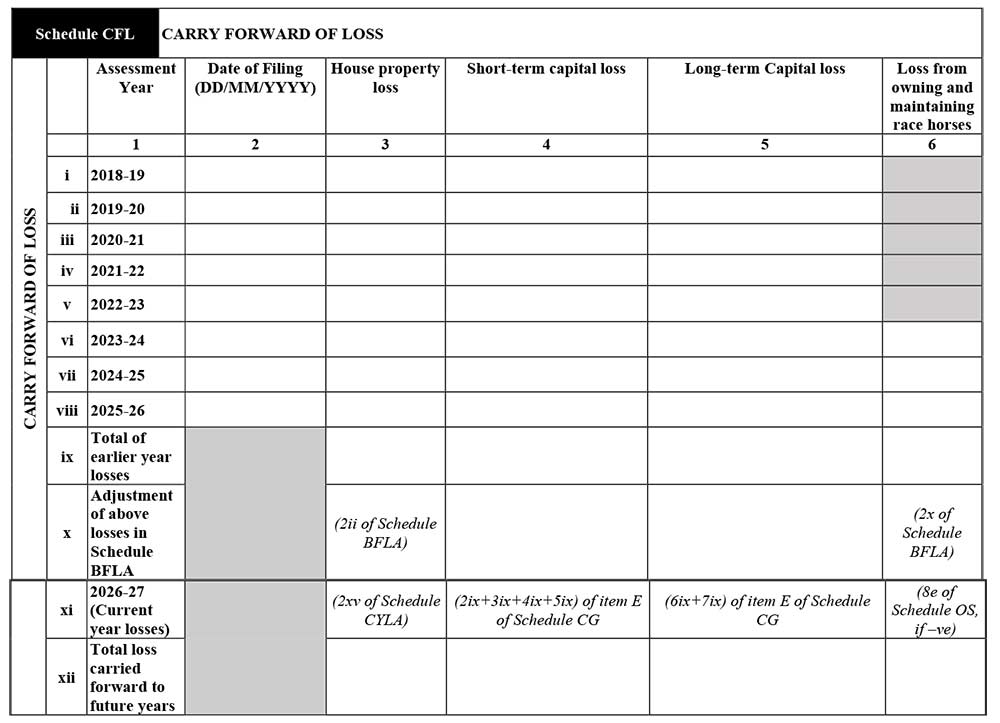

Schedule CFL: Carry Forward of Loss

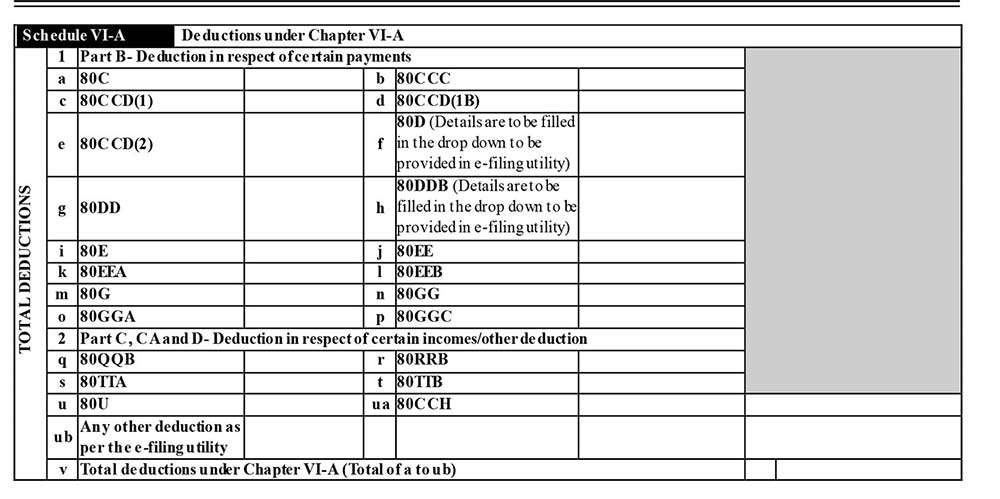

Schedule VI-A: Deductions under Chapter VI-A

Details under this title are enclosed with the following details of the taxpayer to furnish:

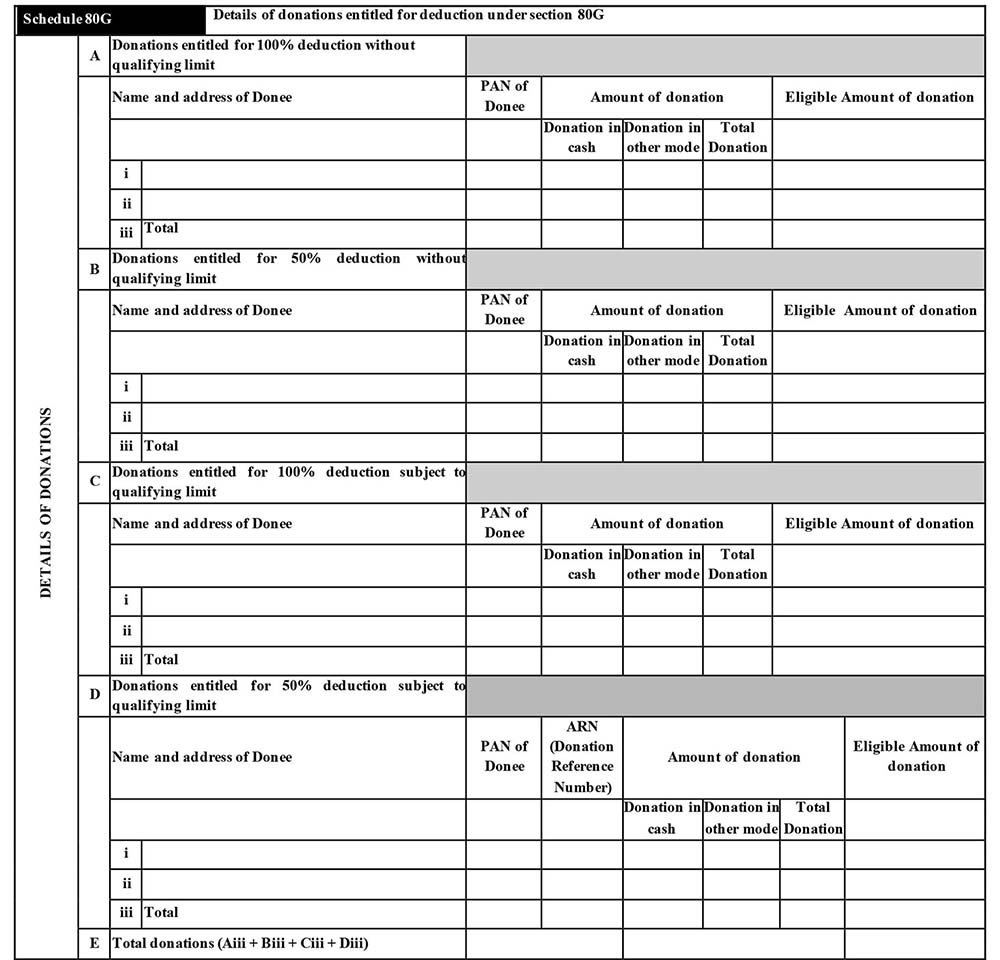

Schedule 80G: Details of donations entitled for deduction under section 80G

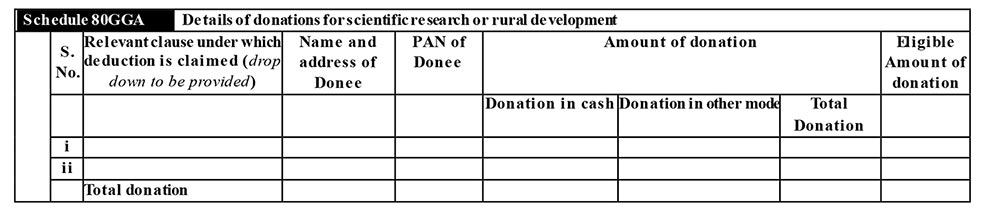

Schedule 80GGA: Details of donations for scientific research or rural development

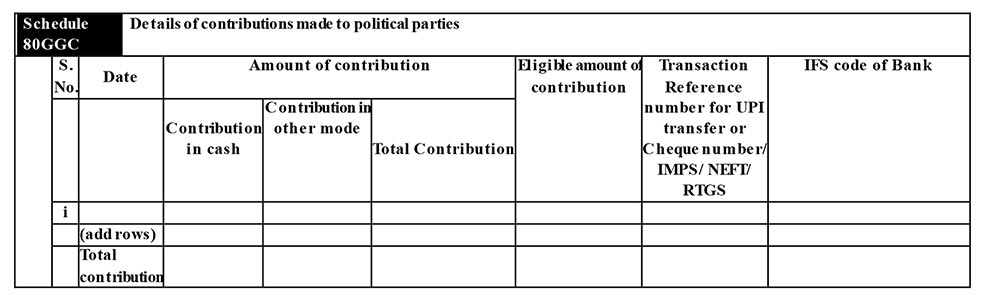

Schedule 80GGC: Details of contributions made to political parties.

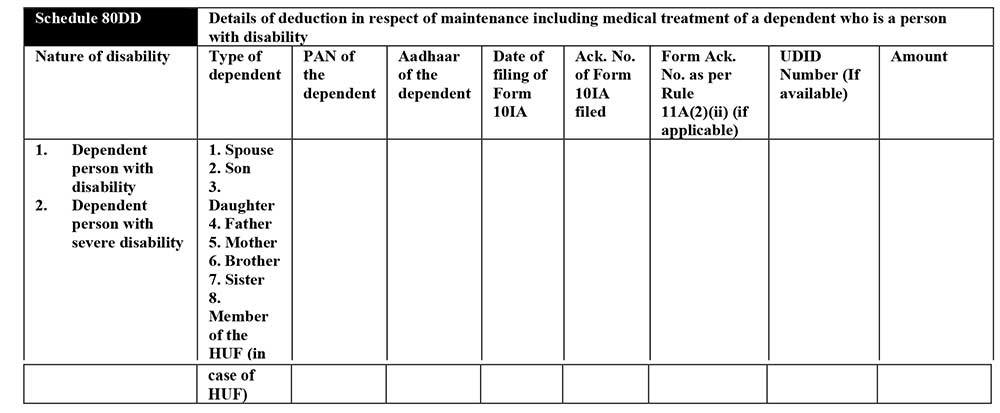

Schedule 80DD: Details of deduction in respect of maintenance including medical treatment of a dependent who is a person with disability.

Schedule 80U: Details of deduction in case of a person with disability

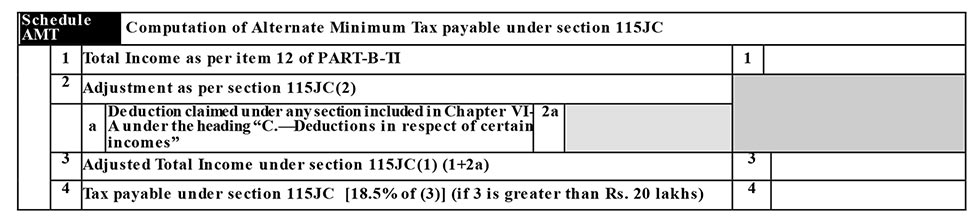

Schedule AMT: Computation of Alternate Minimum Tax payable under section 115JC

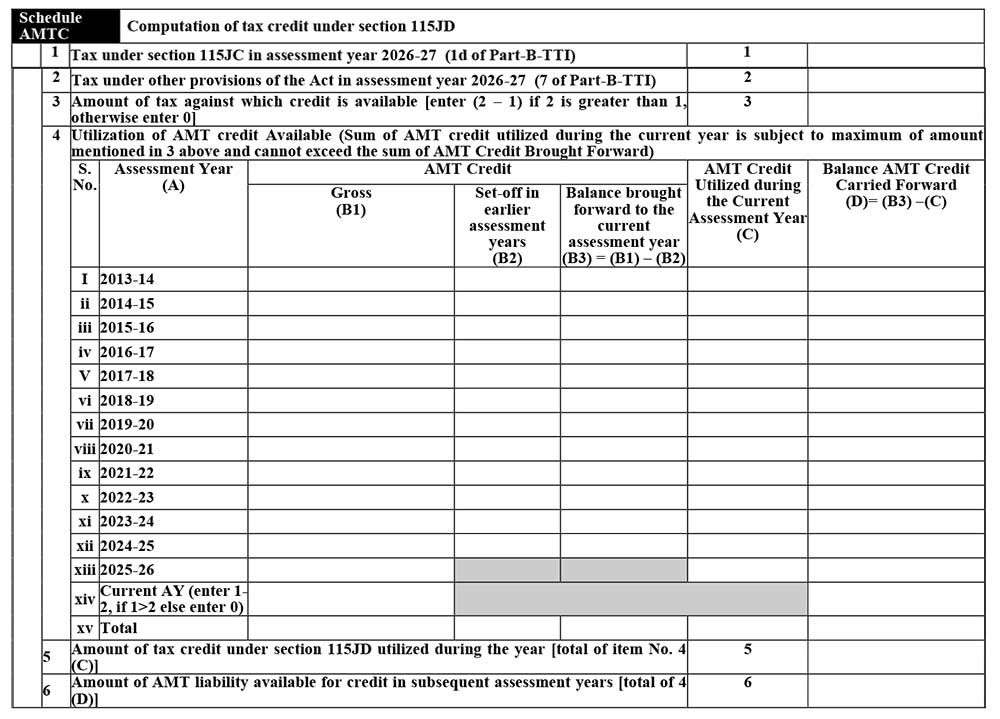

Schedule AMTC: Computation of tax credit under section 115JD

Schedule SPI: Income of specified persons (spouse, minor child etc.), includable in the income of the assessee as per section 64

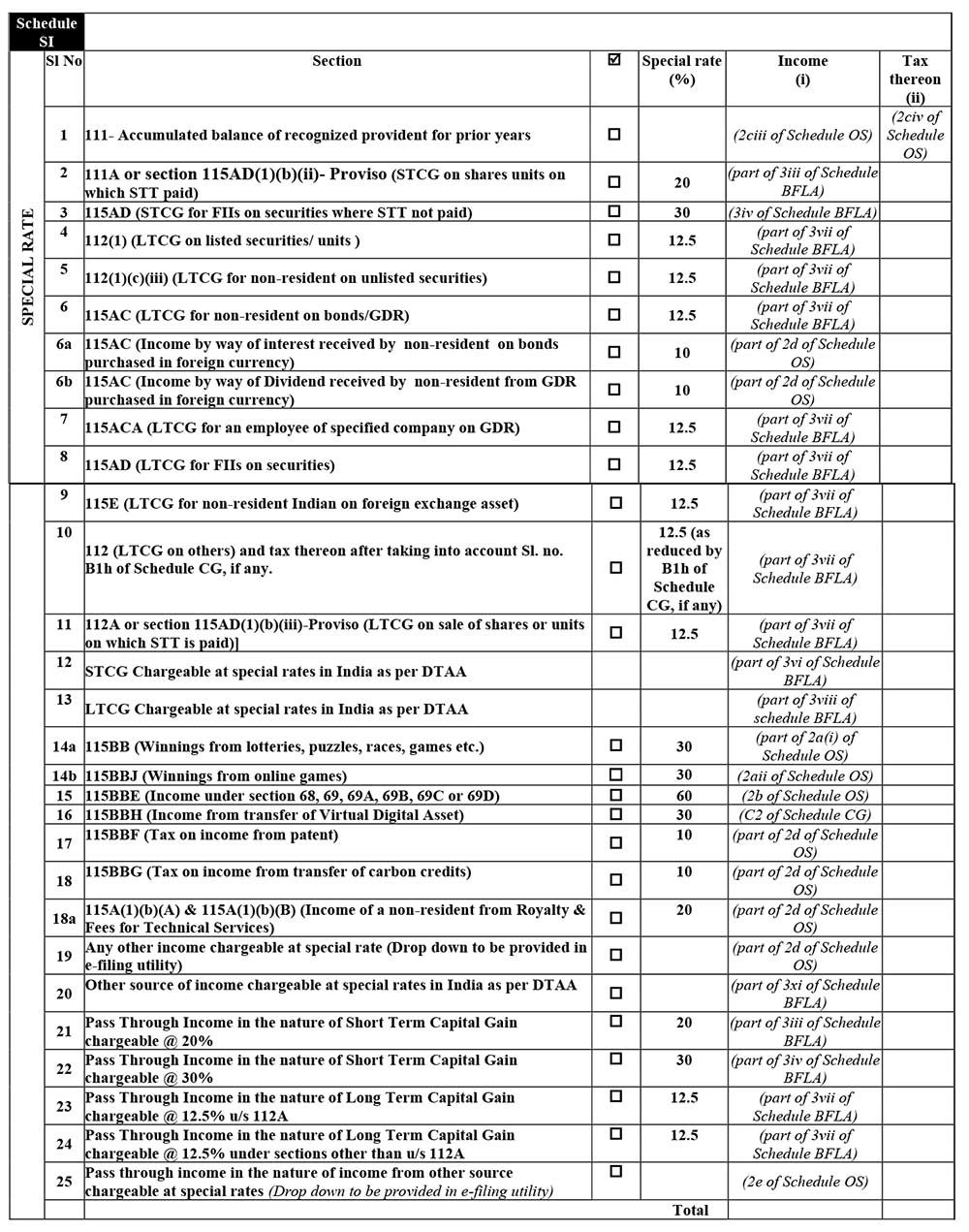

Schedule SI: Income chargeable to tax at special rates

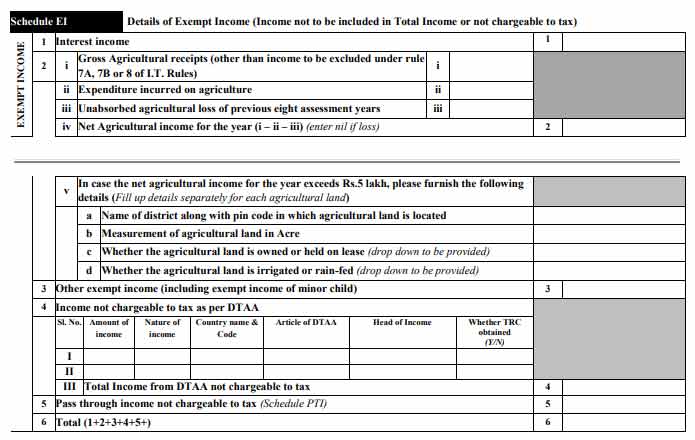

Schedule EI: Details of Exempt Income (Income not to be included in Total Income or not chargeable to tax)

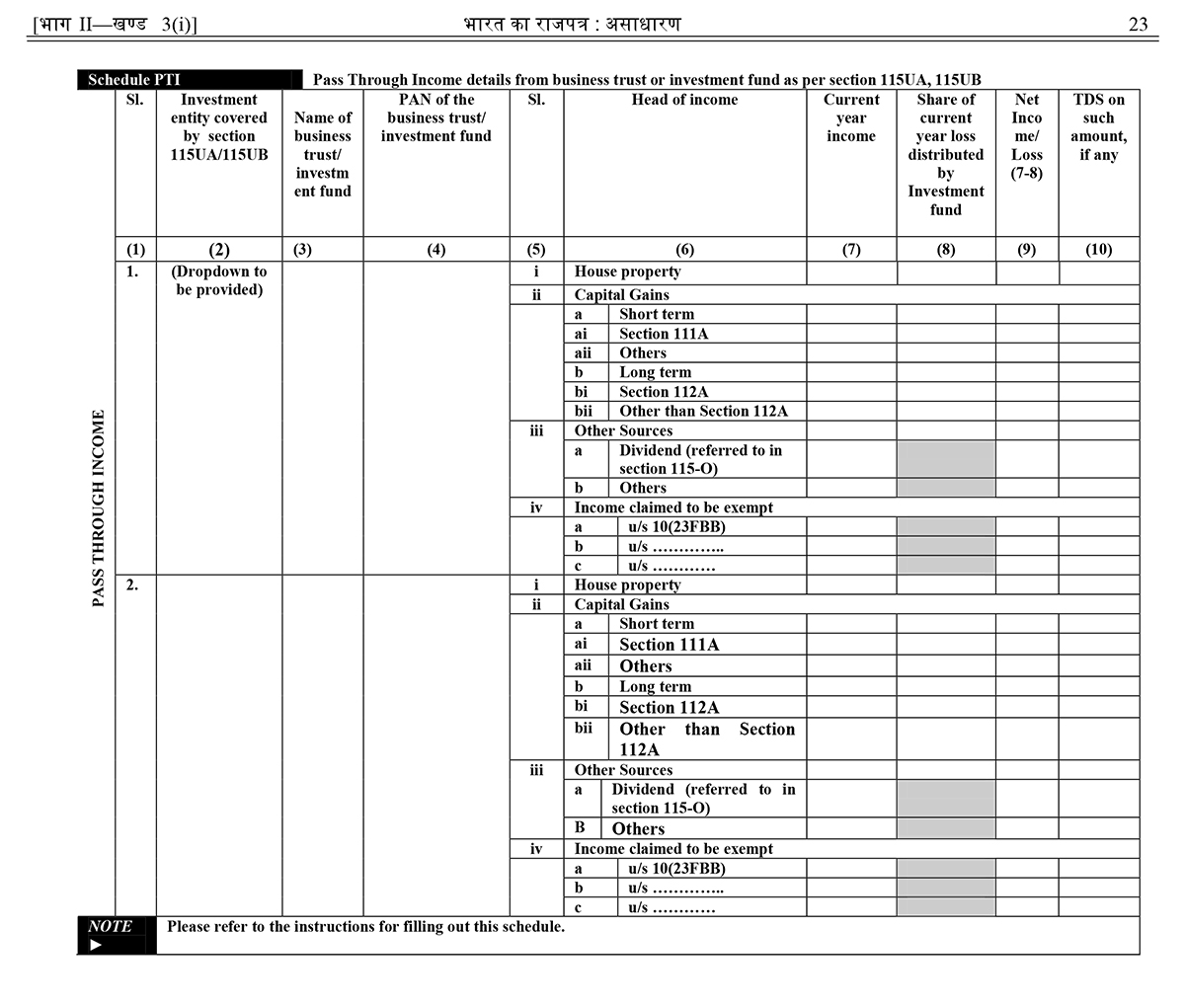

Schedule PTI: Pass Through Income details from business trust or investment fund as per section 115U, 115UA and 115UB

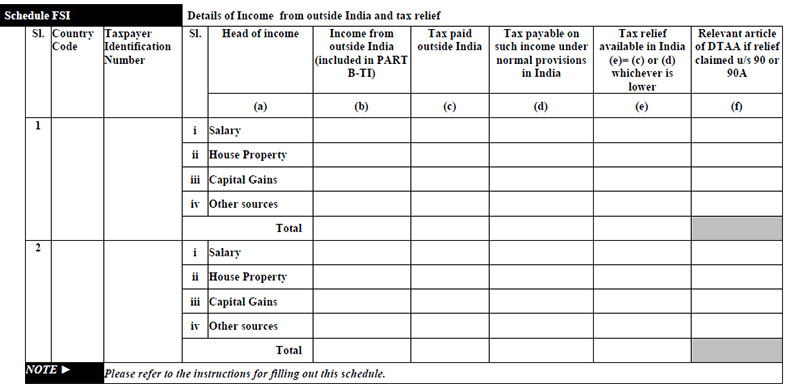

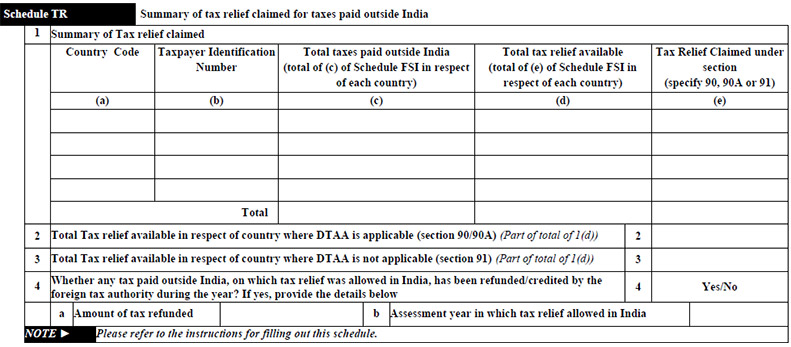

Schedule FSI: Details of Income from outside India and tax relief

Schedule TR: Summary of tax relief claimed for taxes paid outside India

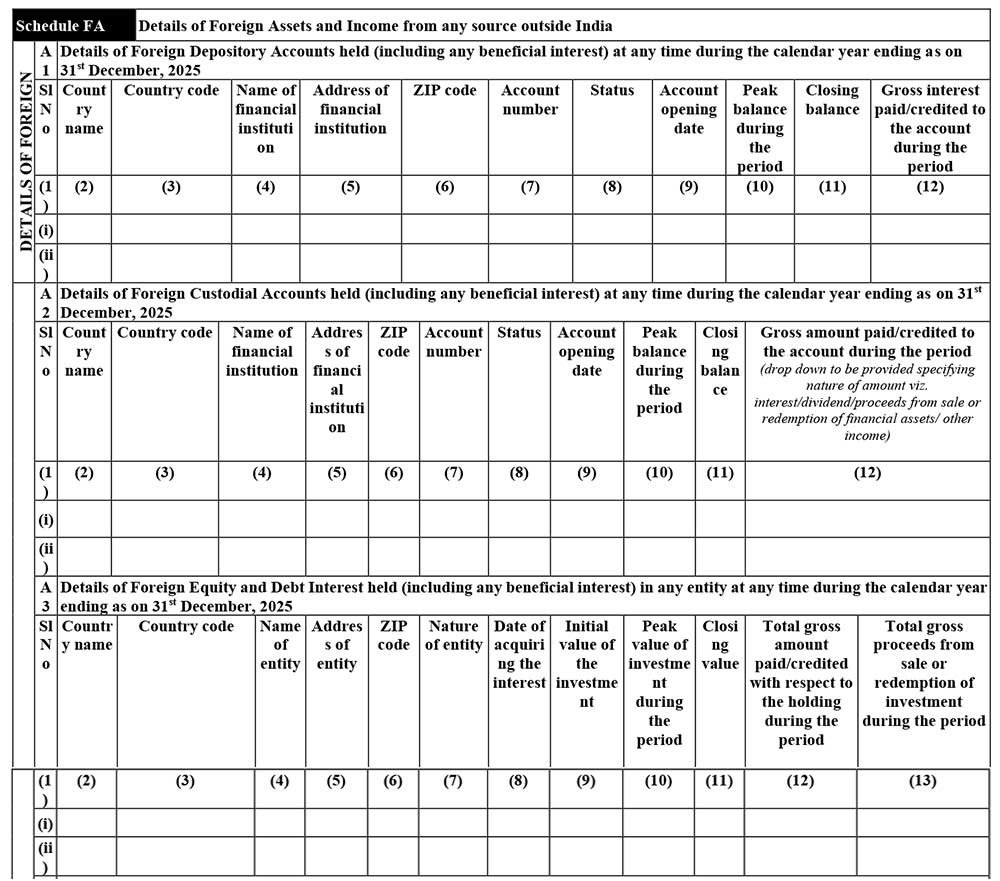

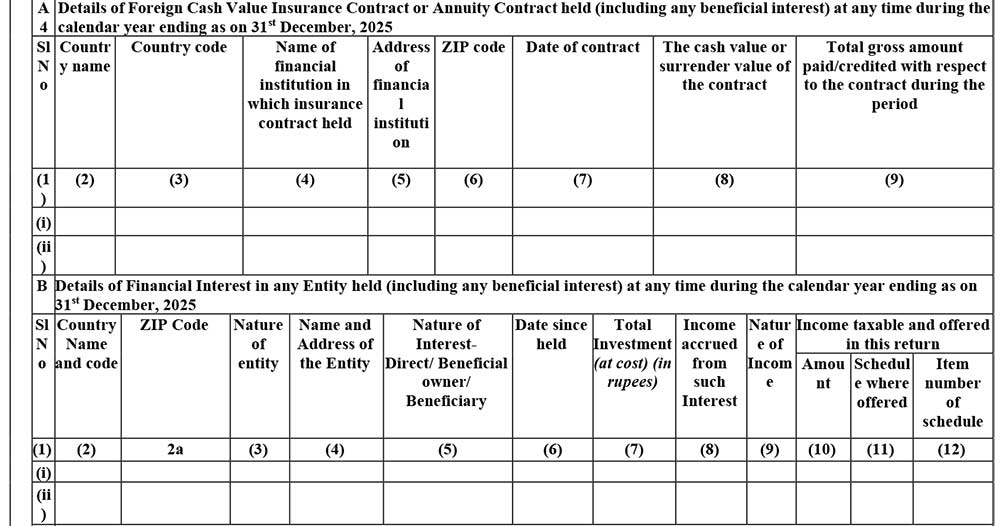

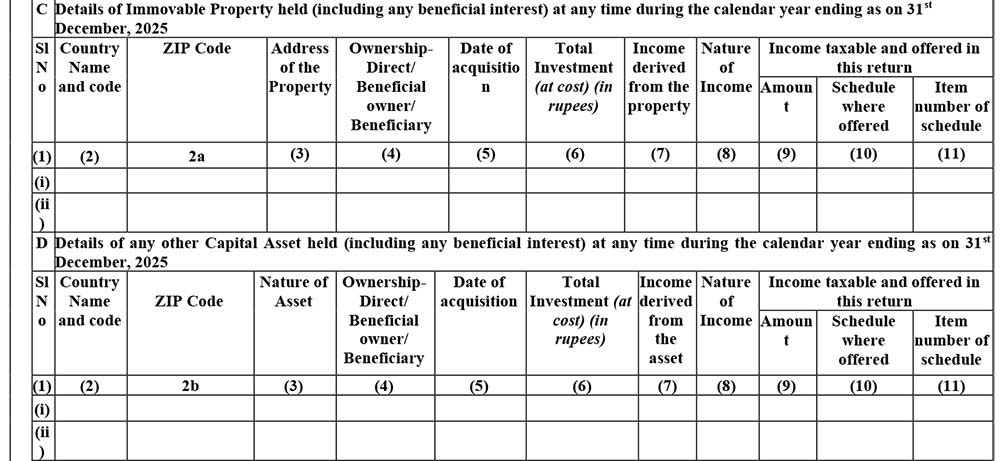

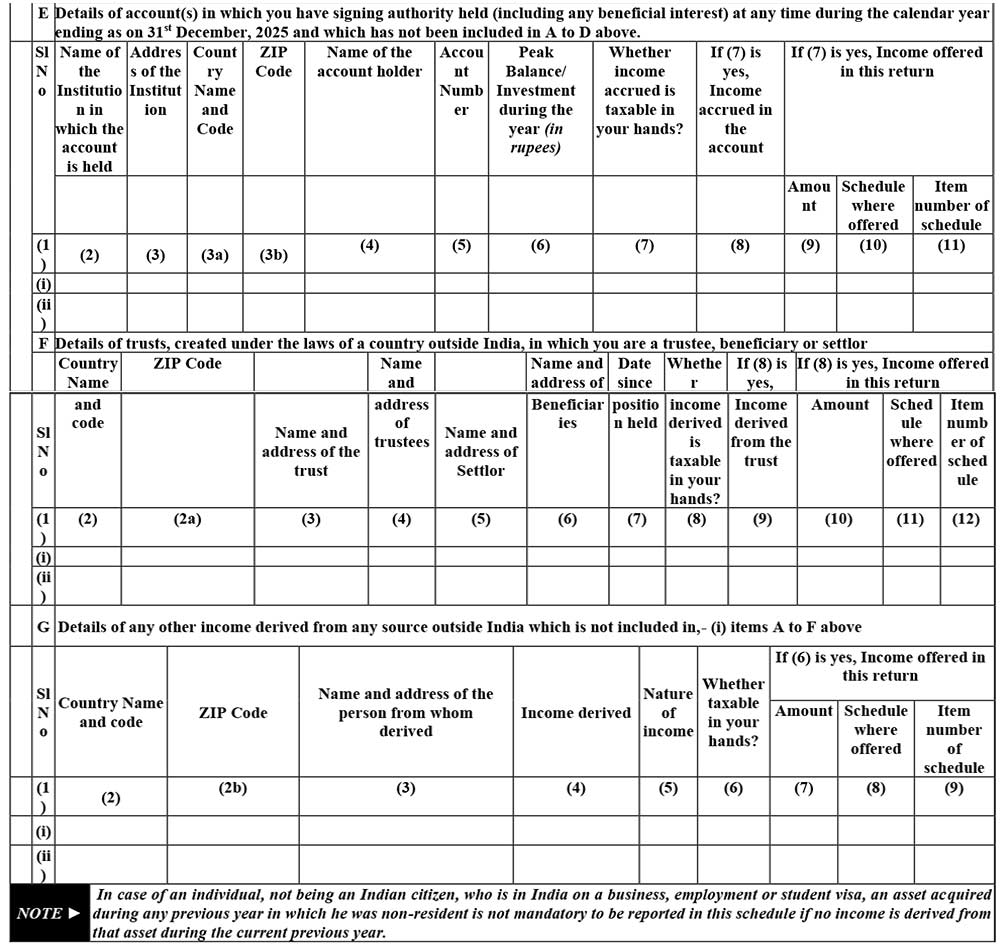

Schedule FA: Details of Foreign Assets and Income from any source outside India

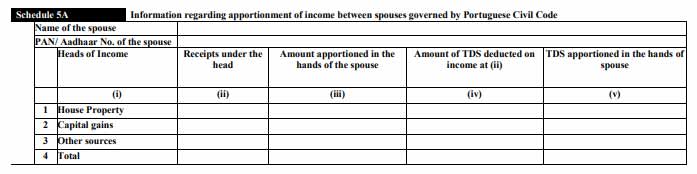

Schedule 5A: Information regarding apportionment of income between spouses governed by Portuguese Civil Code

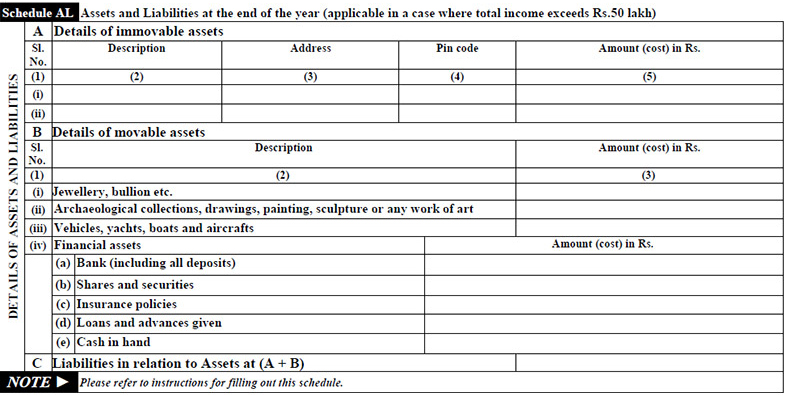

Schedule AL: Assets and Liabilities at the end of the year (applicable in a case where total income exceeds Rs. 1 Crore)

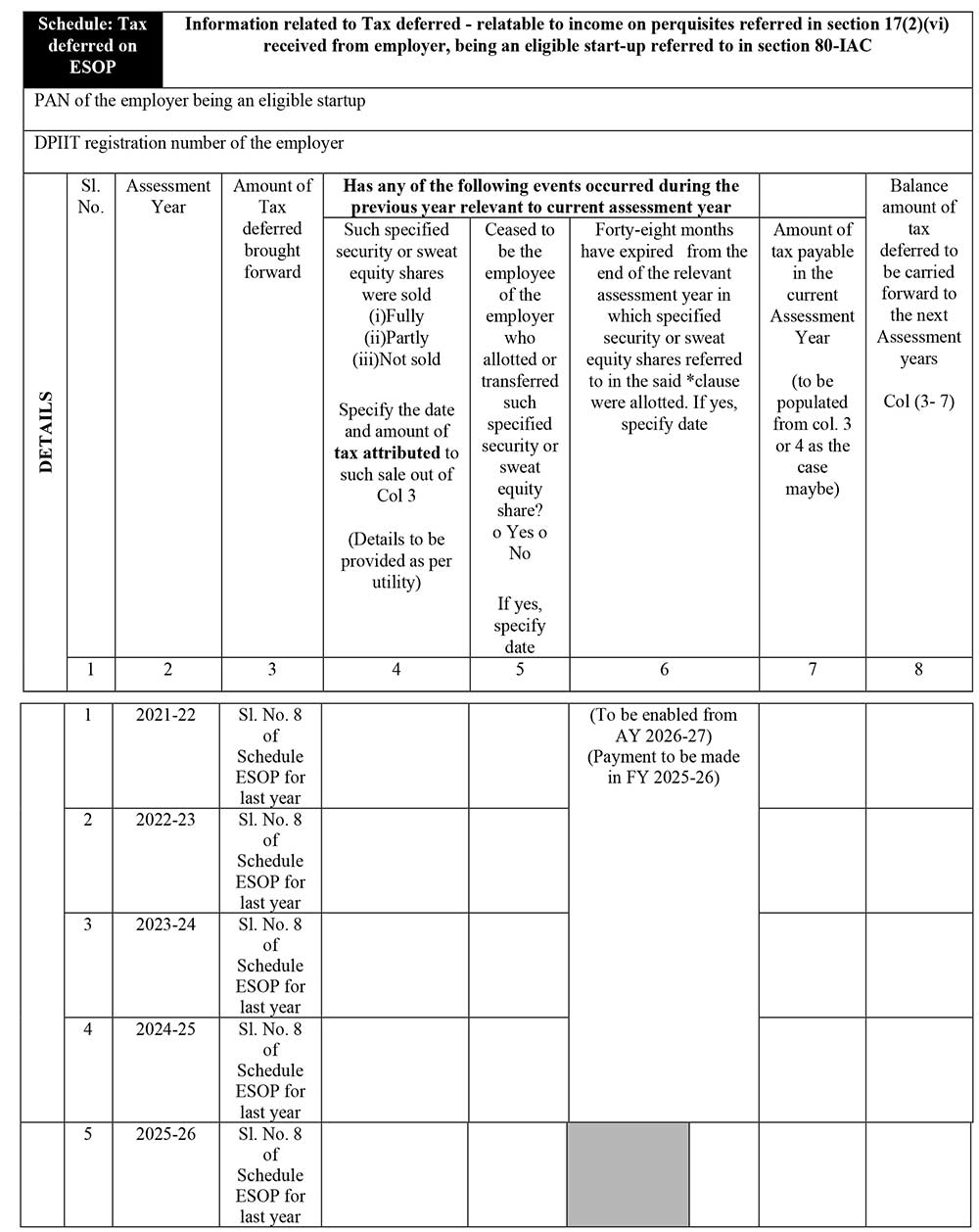

Schedule Tax-deferred on ESOP: Information related to Tax deferred – relatable to income on perquisites referred in section 17(2)(vi) received from employer, being an eligible start-up referred to in section 80-IAC

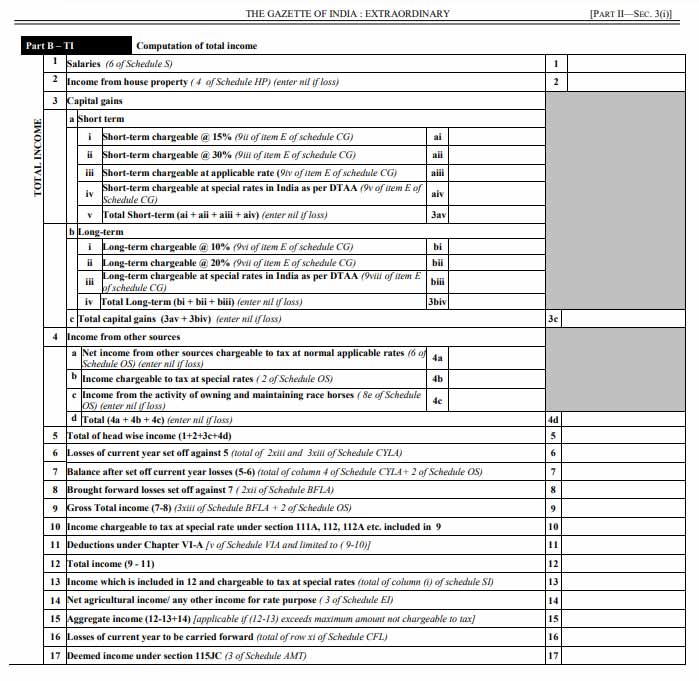

Part B-TI: Computation of Total Income

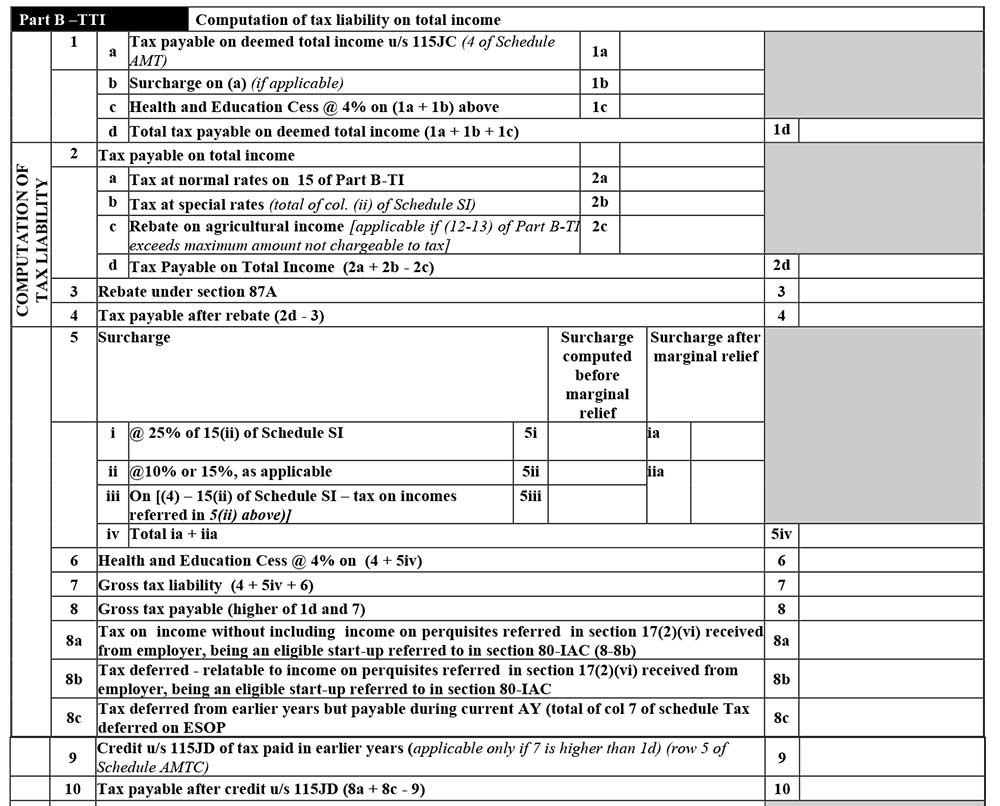

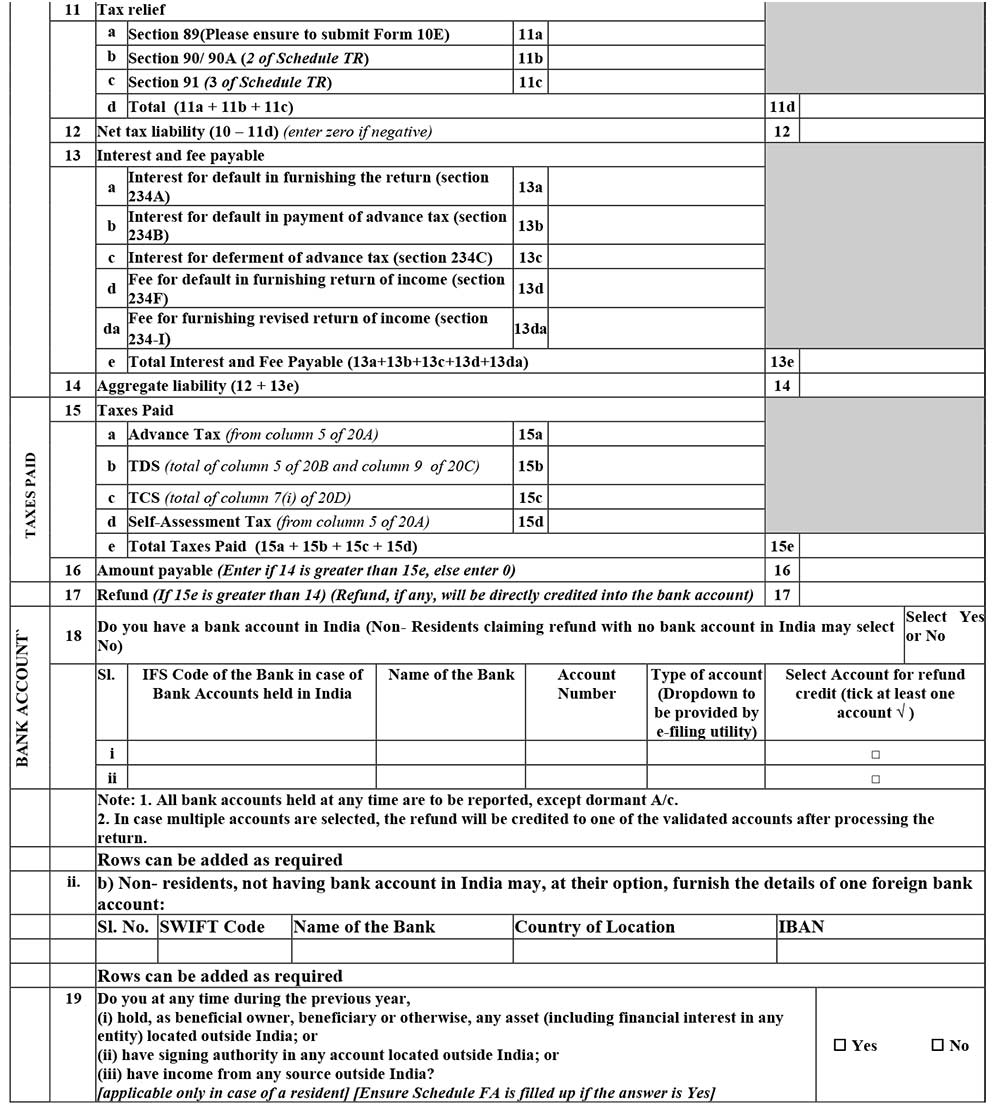

Part B-TTI: Computation of tax liability on total income

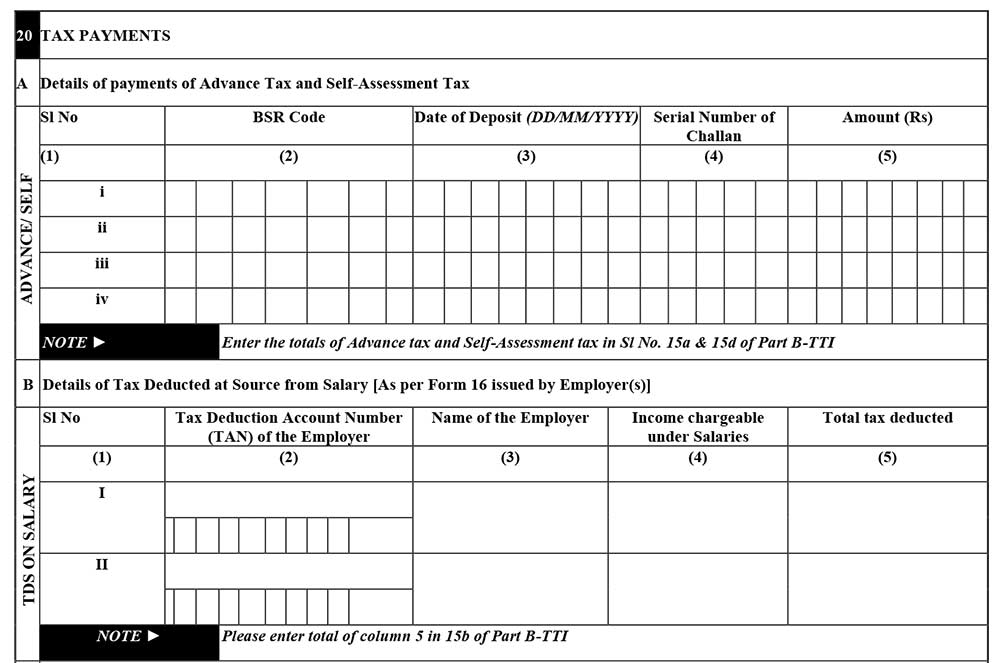

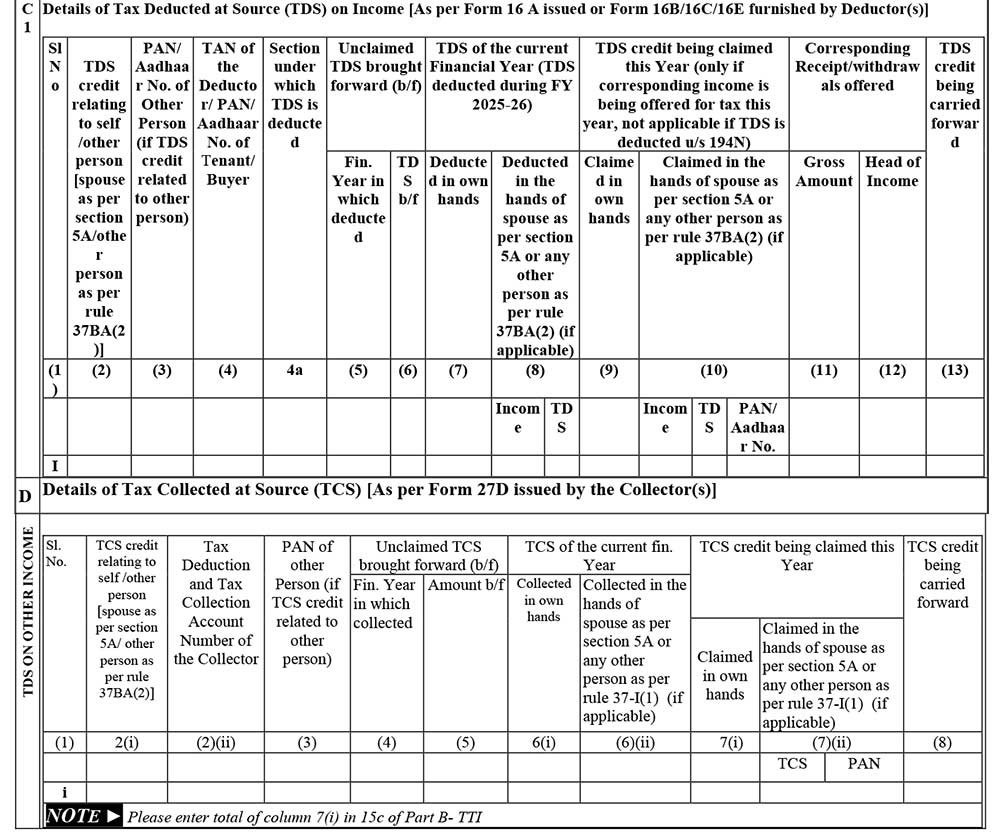

20 Tax Payments

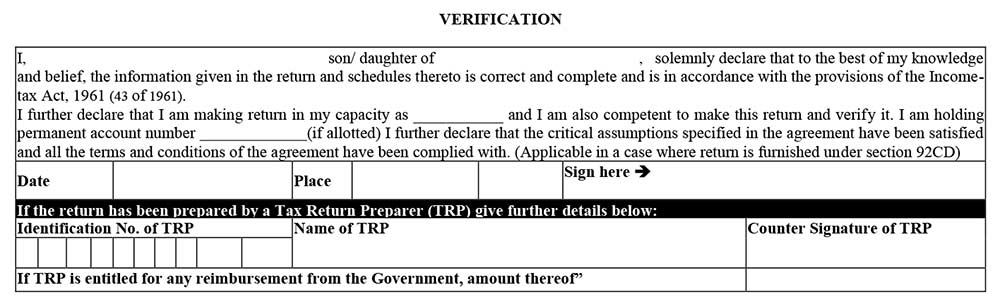

Verification: There will be verification at the end of all the General, Part B TI and Part B TTI, ensuring that the details given are factually correct and self-attested by the taxpayer.

If the return has been prepared by a Tax Return Preparer (TRP), give further details below:

- Identification No. of TRP

- Name of TRP

- Counter Signature of TRP

Income Tax Return 2 Form Filing Mode

An ITR-2 form can be furnished either online or offline. In offline mode, a JSON file (generated via a utility) needs to be uploaded. Alternatively, the user can log in to the portal and select ‘Prepare and submit online’. Data is pre-filled from the AIS, TIS, and Form 26AS. Super senior citizens (80+) may be eligible for paper filing under specific conditions.

Online:

- While furnishing ITR-2 online, feed the details and e-verify the return using EVC via Bank Account/Net Banking/Demat Account/Aadhar OTP or

- 2. Feed the details using an electronic medium and send a physical copy of ITR V to the Centralised Processing Centre (CPC), Bengaluru, through speed post or normal post. When you furnish the ITR-2 return form using an electronic medium, the receipt will be seen in the inbox of the registered email ID. It can also be downloaded from the official income tax website manually. After downloading the acknowledgement, you need to sign the form and then send it to the CPC office, Bangalore, before completing 30 days counting from the e-filing date. On the other hand, it is not required to send the ITR V to the CPC if the EVC/OTP option is used

Offline:

- If the age of the person is 80 or more years during the respective tax period or in the previous year, he/she can opt for offline return filing.

Hi, I am an NRI. I have to file ITR 2. My resident status is of Bahrain, where has Nil Income Tax. I have to provide salary earned in Bahrain under exempt income and foreign income. But as per my understanding, NRI will not cover under DTAA. Is it correct? Then where should we show a foreign salary in ITR 2

If any tax is paid in a foreign country, you will have to show the income in the relevant head along with Schedule FSI. Otherwise, show the income directly under the exempt income schedule.

I have exempt LTCG and taxable STCG. Is it compulsory to fill in the new Schedule 112A?

There is no concept of LTCG exempt from AY 2019-20. It is mandatory to fill details in Sch 112A if the conditions of this section are satisfied.

In my case, I have 25000 LTCG from shares. But up to 1 Lakh is not taxable. In that case, what should I do?

Could you kindly advise where should I fill the details of the Gratuity amount received? In the Exempt Income page on the excel utility file, I’m unable to find Sec 10(10) to fill the gratuity amount received.

Gratuity amount should be shown under Schedule Salary under column Salary as per section 17(1) and exempt amount to be shown under column ” less: Allowances exempt u/s 10″ in other section columns.

hi, I want to file ITR 2 for the first time. I want to know whether tax paid particulars are populated straightaway or I have to type those particulars. And how do I make any payment if there is a short, whether the window will automatically open? thanks

If the details of taxes paid are available in 26AS, then that will be auto-populated in prefilled generated XML and for the short tax payment, you need to enter the entry manually.

In the ITR-2 for excel utility under LTCG section 4a

i A. Cost of acquisition

i B. if the long term capital assets acquired before 01.02.2018 Lower of B1 & B2

Is it correct? Please clarify sir.

As per new changes in LTCG calculation, and insertion of new section 112A and grandfathering provision, details of FMV should need to be entered for arriving at cost of acquisition.

Hello Sir,

In ITR-2 of AY 2020-21 under Schedule 112A it makes “FMV as on 31/1/18” field mandatory & computes LTCG on assets bought after 1/2/18 based on this FMV.

How is FMV as on 31/1/18 relevant while computing LTCG for any asset bought post 1/2/18? Shouldn’t this FMV field be not-applicable in such a case? Isn’t this a bug? OR is there a different Schedule/section in ITR-2 to declare LTCG from assets bought after 1/2/2018?

Please clarify.

If assets purchased after 31st Jan 2018, FMV field be not-applicable