The Delhi High Court has ruled that Section 260A of the Income Tax Act, 1961, which relates to appeals to High Courts, does not envisage the filing of cross-objections by the opposite party, unlike Order XLI Rule 22 CPC.

A division bench of Justices Yashwant Varma and Harish Vaidyanathan Shankar stated that “The Legislature appears to have consciously desisted from adopting principles akin to Order XLI Rule 22 of the Code or specifically introducing provisions enabling the respondent in an appeal under Section 260A to prefer cross-objections.”

The Court determined this “conscious silence” regarding the right to prefer cross-objections with Section 253 (Appeals to the Appellate Tribunal), which allows both the Revenue and the assessee to file cross-objections.

Read Also:- Major 9 Provisions of Income Tax Act: All You Need To Know

“Section 260A refrains from incorporating a specific provision permitting the filing of a cross-objection. This is in stark contrast to what is provisioned for at the second appeal stage before the Tribunal. Thus, while at the stage of an appeal reaching the board of the Tribunal, both the Revenue as well as the assessee are statutorily enabled to prefer a cross-objection on receipt of notice of an appeal, the Legislature has not made any corresponding or parallel provision in Section 260A.”

Court emphasized that while cross-objection u/s 253 could be concerning “any part of such order” which forms the subject matter of the appeal filed before the Tribunal, the right of the respondents in an appeal u/s 260A stands confined to urging that the appeal does not deliver rise to any “substantial question of law”.

The department has preferred a plea against the Income Tax Appellate Tribunal disallowing the specific additions incurred via the assessing officer. The department raised a preliminary objection directing to this ruling since the respondent-assessee desired to file cross-objections.

It was claimed by the department that the cross-objections shall not be kept under section 260A of the Act, neither envisaging nor making such a remedy. It was claimed that section 260A is a remedy of redressal before the HC concerning an order passed via the Tribunal furnished an influential question of law emerges.

The department furnished that the CPC itself does not acknowledge the cross-objection as an avenue to be pursued in a plea from an appellate decree. Therefore, it was claimed that it would be wrong completely to blame the principles underlying Order XLI Rule 22 CPC as applying to an appeal u/s 260A.

It was claimed by the respondent-taxpayer that the right to choose cross-objections must be read into the provisions of Section 260A of the Act, and the provision must not be granted as an interpretation that denies the taxpayer such a right.

Recommended: Bookkeeping is Required To Invoke Section 69A Of Income Tax Act: Delhi High Court

It outlines stress on the language in Section 260A(4) that the provisions of CPC, as far as may be applicable, would rule. The court denied the proposition citing that the language in which sub-section (4) stands cast mentions that the plea shall be heard merely on the question so made, and the right of the respondent during the hearing is validated to argue that the case does not comprise such a question.

The Court considered whether Section 260(6) would allow the filing of cross-objections. The provision authorizes the High Court, while considering an appeal, to rule on any issue which may have been in its view, incorrectly decided or not determined by the Tribunal.

According to the Court’s Ruling in the Negative,

“The incorrect determination of an issue by the Tribunal is tied to the decision rendered by the Tribunal on the question of law on which the appeal may be liable to be entertained and admitted. The wrongful determination of an issue is thus indelibly connected to that part of the order of the Tribunal and which is referred to in Section 260A(1). Sub-section (6), therefore, could at best be construed as being preferable to the substantial question and a finding of the Tribunal in connection therewith. Thus this too cannot be possibly construed as the embodiment of a right sought to be conferred upon a respondent to raise an issue which is neither connected nor concerned to the question of law on which the appeal comes to be admitted.”

The court turned to section 260A(7), which provides that the provisions of CPC pertinent to the pleas to the HC will, as far as may be applicable, also control the pleas created under the cited provision.

Though, it ruled that this provision too, does not grant a right to the respondent to file cross-objections. It ruled, “Each statute may create an independent right of appeal and regulate the exercise of such a right subjecting it to such conditions and stipulations as may be considered appropriate. It is for this reason that Section 260A(7) desists from fully or completely adopting the provisions comprised in the Code. The Legislature has thus clearly been circumspect when stipulating that the provisions of the Code would apply only to the extent that Section 260A of the Act may envisage or sanction.”

Influential to mark that the Karnataka High Court in Smt. Jyoti Kumari v. Asst. CIT (2010) held that a cross-objection shall not be maintainable in an appeal u/s 260A.

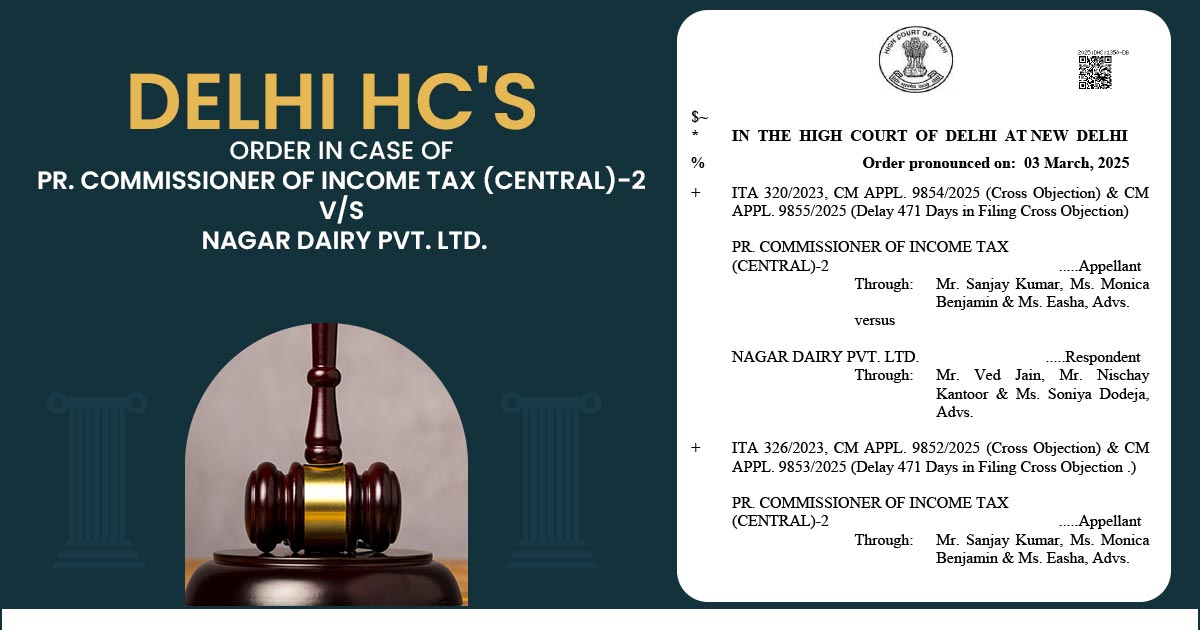

Appearance: Mr. Sanjay Kumar, Ms. Monica Benjamin & Ms. Easha, Advs. for Appellant; Mr. Ved Jain, Mr. Nischay Kantoor & Ms. Soniya Dodeja, Advs for Respondent.

| Case Title | Pr. Commissioner Of Income Tax (Central)-2 V/S Nagar Dairy Pvt. Ltd. |

| Citation | Case no.: ITA 320/2023 and batch |

| Date | 03.03.2025 |

| Counsel For Appellant | Mr. Sanjay Kumar, Ms. Monica Benjamin & Ms. Easha, Advs. |

| Counsel For Respondent | Mr. Ved Jain, Mr. Nischay Kantoor & Ms. Soniya Dodeja, Advs. |

| Delhi High Court | Read Order |