The Delhi High Court has ordered the tax department to promptly release a refund related to the GST Input Tax Credit (ITC), along with interest. The court decided that the refund should not be delayed because there was no ongoing appeal or hold on the last decision made by the Appellate Authority, which authorised the refund to be processed.

JVG Technology Private Limited, the business of the applicant, is in exporting mobile phones and is registered under Goods and Services Tax with registration no. 07AAFCJ6874R1ZL. For domestic sales, it purchased input services and paid GST of 18%. Usually applicant had an unutilized GST ITC.

For September 2022, a Rs. 2.03 crore refund claim has been submitted by the applicant, and for October 2022, a Rs. 2.98 crore. On 29th May 2023, two SCNs were issued, and an online response was furnished by the applicant. Even after this, on 26th June 2023, the refund claims were rejected by the assistant commissioner.

On the appeal of the applicant, AO permitted the refund dated 11th December 2023, while setting aside the previous rejection orders. The applicant, after the order made various requests for the refund, but it was not released. Therefore, the applicant furnished the existing petition.

Read Also: GST Refund Claim Cannot Be Denied Based on Retrospective Application of Rule 90(3) Proviso

Through invoking Section 54(11) of the CGST Act, 2017, the department has withheld the refund, citing that the refund cannot be processed till the appeal against the order of the AA on 11th December 2023 is determined or the appeal proceedings are concluded. The revenue shall be harmed from granting the refund due to the alleged fraud, the department cited.

In Shalender Kumar v. Commissioner CGST, the Court referred to its earlier decision where it said that a refund can merely be withheld u/s 54(11) if two norms were fulfilled- (i) an appeal or proceedings was due against the order of refund, and (ii) the commissioner assumed that releasing the refund shall impact the revenue.

Read Also: How to File GST Refund Claims Manually?

Refund can not be stopped alone with the opinion of the department, the court said. As no appeal has been furnished against the order of AA, and there was no stay, the department cannot statutorily withhold the refund.

In the case of GS Industries, the court relied where it was ruled that only planning to furnish a plea cannot explain the late refund, particularly when the refund was permitted on appeal earlier.

As per the court asked the department was asked to release the refund with interest u/s 56 of the CGST Act within two months. If the department thereafter succeeds in any statutory challenge, then it can recover the refunded amount under the law. The applicant was allowed to apply if the refund was not credited by 10th July 2025.

If the department submits a plea contesting the order of AA, then the GST refund processing shall be within the consequences of the appeal, Justice Prathiba M.Singh and Justice Rajneesh Kumar Gupta ruled.

As per that, the petition was disposed of.

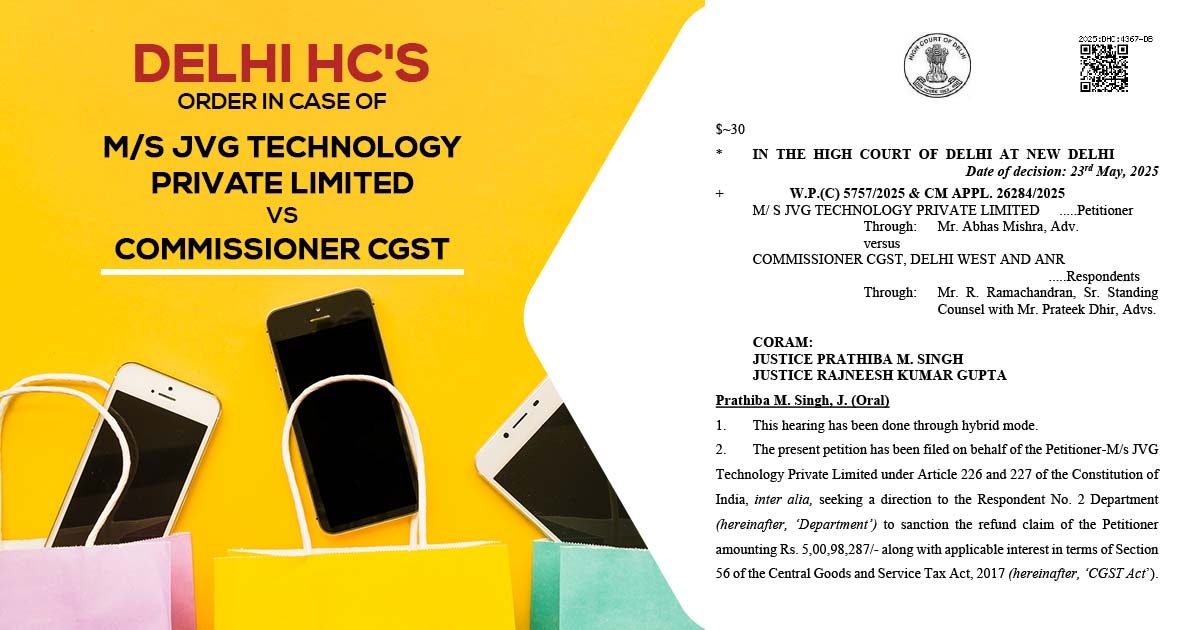

| Case Title | M/S JVG Technology Private Limited vs Commissioner CGST |

| Case No. | W.P.(C) 5757/2025 & CM APPL. 26284/2025 |

| For Petitioner | Mr. Abhas Mishra |

| For Respondent | Mr R. Ramachandran, Mr Prateek Dhir |

| Delhi High Court | Read Order |