A Delhi Court convicted and sentenced a woman to 6 months in jail for not filing a return on income of Rs 2 crores.

This case is related to the complaint filed via the Income Tax Office (ITO) alleging that TDS (tax deducted at source) amounting to Rs. 2 lakh was deducted against the receipt of Rs. two crores made to the charged in FY 2013-14, yet, no income return for the AY 2014-15 was filed via the taxpayer/accused.

After hearing submissions and regarding the facts and events of the case Additional Chief Metropolitan Magistrate (ACMM) Mayank Mittal convicted Savitri.

ACMM Mittal said in the order passed dated March 4, “The convict is awarded a sentence of simple imprisonment for six months with a fine of Rs 5,000 and in default to undergo simple imprisonment for one month,”

To contest the order after regarding her application the court granted her 30 days’ bail.

Special public prosecutor (SPP) Arpit Batra furnished that what is material for charging a sentence on a convict is not the tax amount evaded, but the intention of the provision.

It was furnished that the provision objective is deterrence among the individuals obligated to file the tax to furnish their income tax return in time and to file the tax as per that.

He provides that a maximum amount of imprisonment must be awarded to the convict and a substantial amount of fine must be levied.

The counsel for the convict furnished that the sentence granted to the convict must be concerned with the social cases of the convict and the condition of the convict during the commission of a crime and the levying of the sentence.

Read Also: Legal Provisions for Tax Evaders and ITR Non-filers Under I-T Act

It was provided that the convict is a widow lady and is not educated. No one is there in the family of the convicts to take care of the family excluding the convict.

According to the Prosecution, a letter dated September 11, 2017, was issued via the ITO to the convict for verification of data on whether the income tax return was furnished for the AY 2014-15 or not, but, the accused was unable to furnish a response.

On January 10, 2018, a notice, under Section 142(1) of The Income Tax Act, 1961 (IT Act ) was issued to the accused with a directive to provide the return of AY 2014-15, however, no compliance was made via the taxpayer / accused, as per the Prosecution.

Subsequently, on January 22, 2018, ITO issued a notice, under Section 271F of The IT Act to the accused for non-filing of the return, and additionally accused had not initiated to answer to the same.

Accordingly, by way of an order on February 9, 2018, the accused was demanded to pay a penalty of Rs 5,000.

Before the Principal Commissioner of Income Tax, a proposal for the grant of sanction was sent.

Show cause notice under Section 276CC of the IT Act was issued to her before the issuance of a sanction. On behalf of the convict, a reply was filed via her authorized representative on March 18, 2018.

A sanction order allowing the launching of prosecution against the accused and directing the Income Tax Officer, to file the present complaint u/s 276CC read with 279 of IT Act is been issued by the Principal Commissioner of Income Tax, New Delhi, post acknowledging the aforesaid and providing chances to the convict,

On February 28 convicting Savitri, the Court held that the complainant has been able to prove beyond reasonable doubt the service of letter/notice issued to the accused on September 11, 2017, and notice issued under Section 142(1) of The Act on January 10, 2018, in which the accused was duty mandated to furnish the income return which admittedly not filed by the accused.

Recommended: Conditions, Who Can File ITR Even After Due Date Without Penalty

As per the court, the accused cannot draw any material to the court either to draw its case under the ambit of the provision of Section 276CC of The Act. No proof is been carried by the accused on record to rebut the presumption of the culpable mental state under Section 278E of The Act.

The court articulated in the judgment, “Accordingly, the accused is held guilty of not filing the return of income for the assessment year 2014-15 under Section 276CC of The Act. Accordingly, the accused is convicted for an offence punishable under Section 276CC of the Act,”

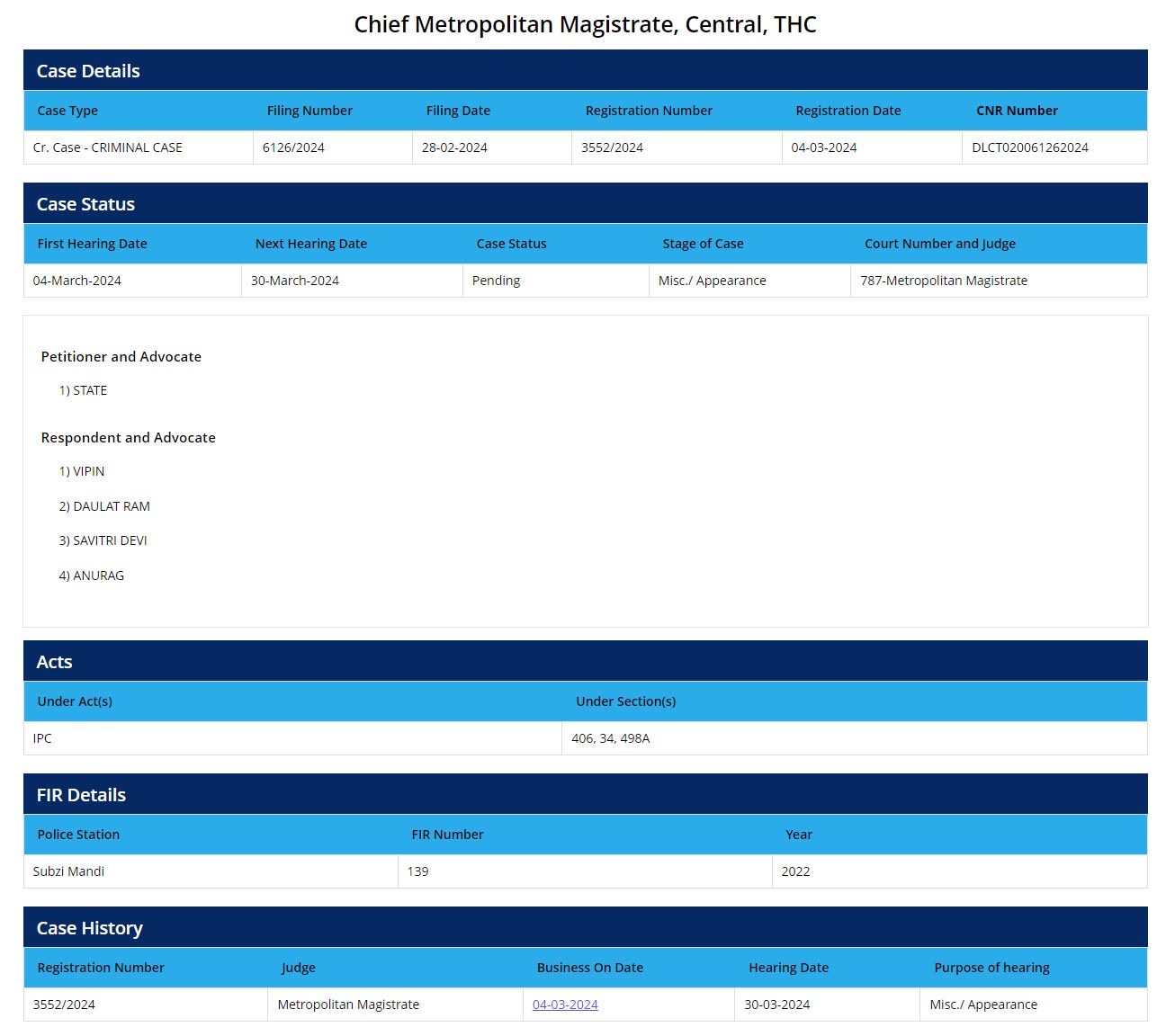

Case Details: