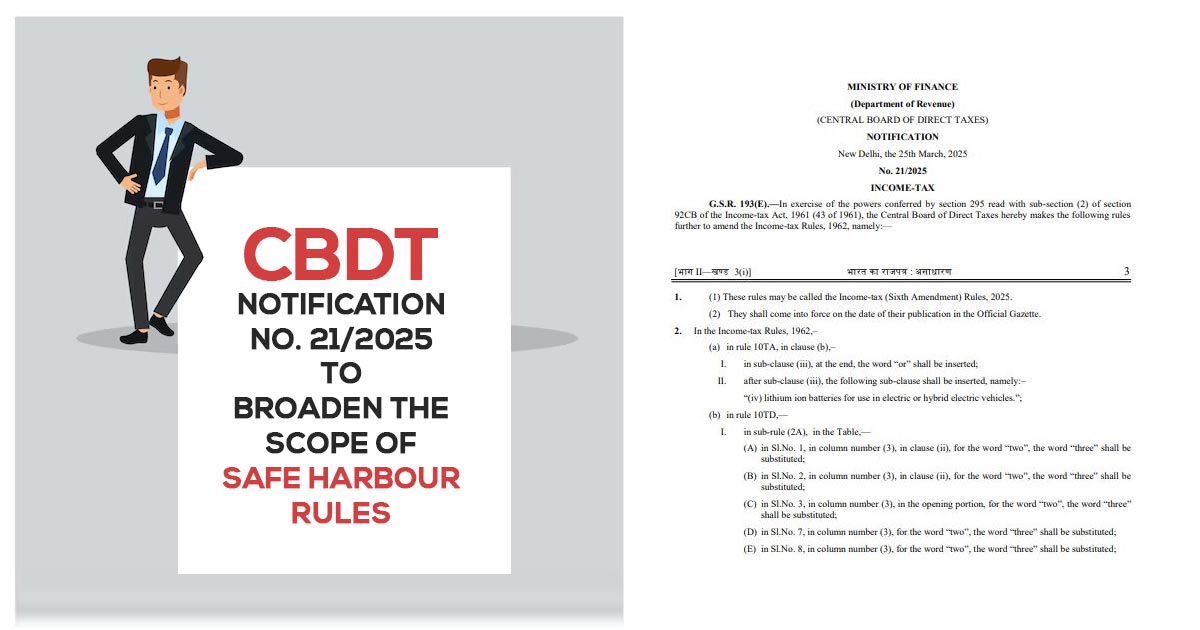

The Central Board of Direct Taxes (CBDT) has issued Notification No. 21/2025 dated March 25, 2025, amending the Income-tax Rules, 1962. The Income-tax (Sixth Amendment) Rules, 2025, introduce modifications impacting transfer pricing, electric vehicles, and assessment years.

Latest Update

The IT Notification 124/2024 regarding the application for the Safe Harbour option under Section 9(1)(i), Profits and Gains of Business or Profession, is now available for filing. Read the PDF

Amendments Introduced

- Extended Safe Harbor Period: Under Rule 10TD(3B), assessment years covered have been extended up to 2026-27, ensuring continued benefits for eligible taxpayers.

- Transparency on Assessment Year Validity: Now, the provision in Rule 10TE(2) cites that specific safe harbour benefits apply to one assessment year only, removing peculiarity.

- Rectified Safe Harbor Margins: Safe harbour margins for multiple international transactions have been revised, augmenting the prescribed profit margins from 2% to 3% in several cases under Rule 10TD.

- Lithium-Ion Batteries for EVs: An influential inclusion in Rule 10A now acknowledges lithium-ion batteries used in electric and hybrid vehicles under safe harbour provisions. With India’s enhancement of sustainable mobility, the same move has been aligned.

Importance for Taxpayers & Companies

- Expanded certainty for MNCs- Revised margins furnish clarity in transfer pricing disputes.

- Improve for the EV industry- Lithium-ion battery inclusion motivates the investment in clean energy.

- Longer Tax Planning Horizon- Extension of safe harbor rules benefits IT, ITeS, and R&D service providers.

The same notification is a significant step in improving tax compliance while assisting India’s green energy and business-friendly policies.