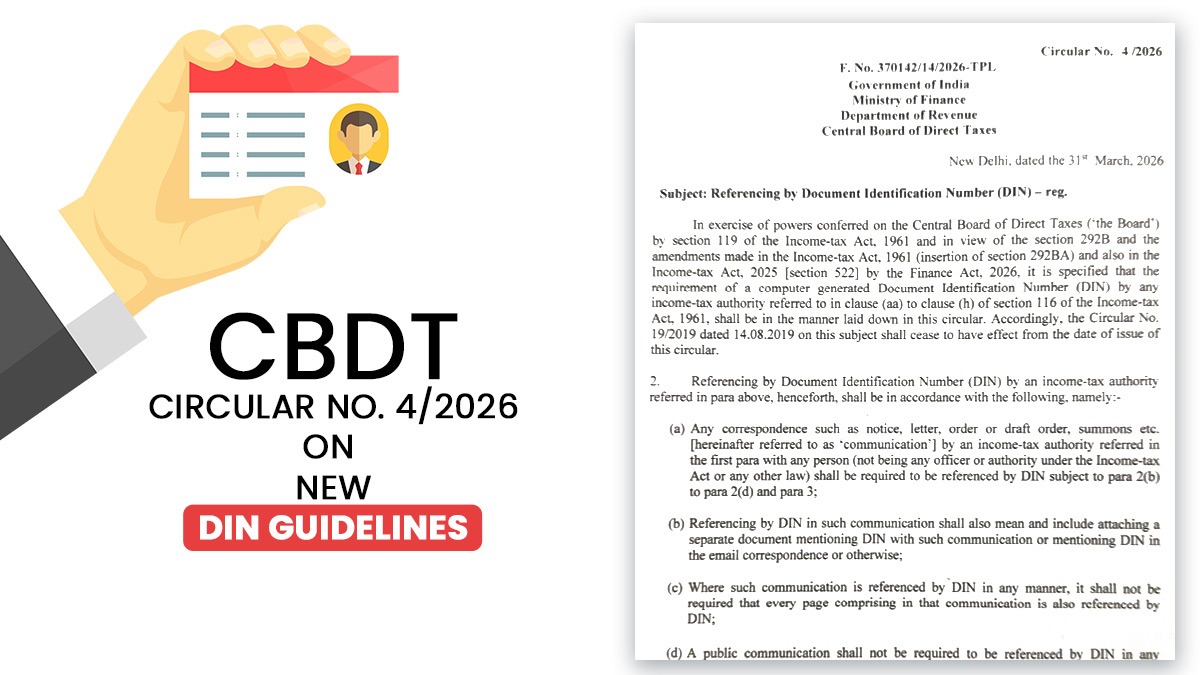

On March 31, 2026, the Central Board of Direct Taxes issued Circular No. 4/2026, introducing revised guidelines for the mandatory use of the Document Identification Number (DIN) in all communications issued by income-tax authorities.

The circular cites that every official communication, including notices, letters, orders, summons, and emails, should contain a computer-generated DIN. Also, each page of the same communication should state the DIN to ensure authenticity and traceability.

With this update, the earlier Circular No. 19/2019 on DIN has been withdrawn immediately.

CBDT cites specific exceptional situations where DIN may not be generated, like technical problems, absence of system access, or urgent field-level communications. But in some cases, the communication should specify the reason for the non-generation of the DIN and obtain post-facto approval from the competent authority within 15 days.

Read Also: How Income Tax Software Companies Should Prepare for Act 2025

All these exceptional communications need to be uploaded on the system and regularised with a DIN within the specified timeline.

The same objective is to strengthen transparency, accountability, and digital tracking in tax administration, aligning with revisions rolled out under the Income-tax Act, 1961, and the Finance Act, 2026.

CBDT Circular No. 4/2026