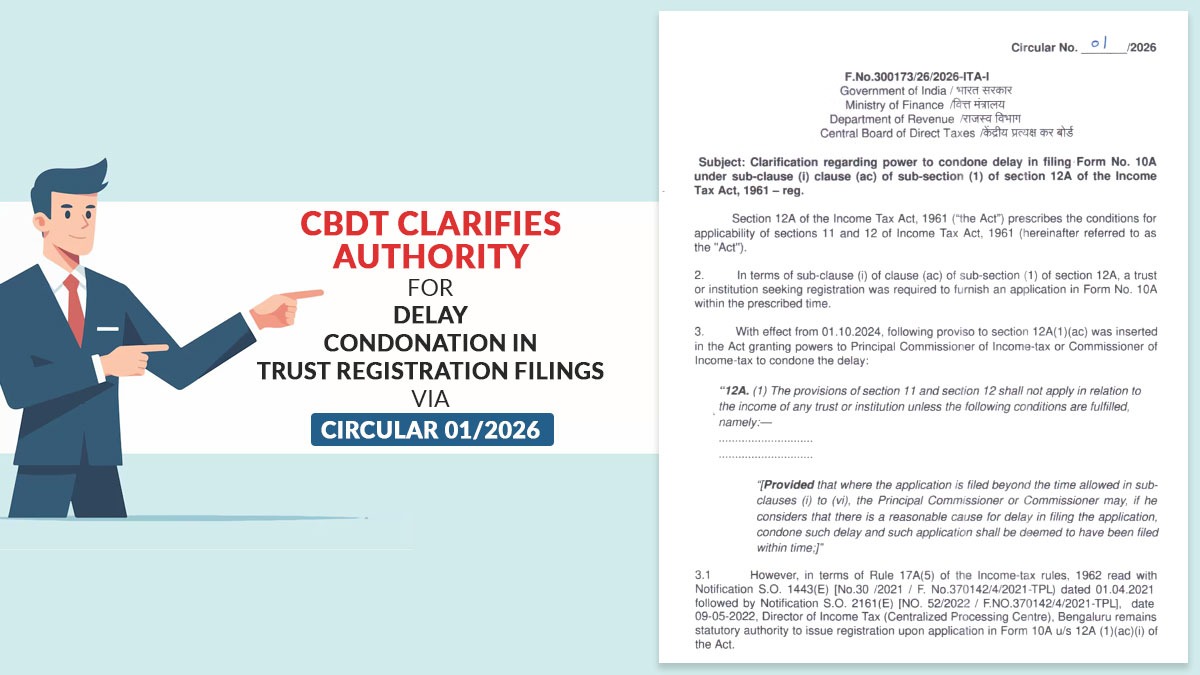

The Central Board of Direct Taxes (CBDT), in a relief to charitable trusts and institutions, has issued Circular No. 01/2026 clarifying the authority empowered to condone delays in filing Form No. 10A under Section 12A of the Income-tax Act, 1961.

The Board has expressed that the jurisdictional Principal Commissioner of Income-tax (PCIT) or Commissioner of Income-tax (CIT) shall have the authority to condone delays in filing Form 10A, provided there is a reasonable cause. This clarification seeks to determine whether such powers rest with the CPC Bengaluru or the jurisdictional authorities.

Previously, the Income Tax Department’s CPC in Bengaluru handled registration application processing, but there was still confusion about who was authorised to grant condonation for delayed filings.

CBDT, to avert genuine hardships, has exercised its authority under section 119(2)(b) and confirmed that eligible trusts are not refused registration benefits only due to delays.

Applicability:

The circular applies to all cases where Form 10A is submitted after the specified time periods and where condonation applications are due or submitted on or after the date of the circular’s issuance.

Effect:

The same decisions furnish transparency and relief to trusts and institutions seeking registration. It assures seamless compliance and reduces procedural hardships.

CBDT Circular No.1