The Calcutta High Court has stayed reassessment proceedings initiated u/s 148 of the Income Tax Act, 1961, for the AY 2021-22, on a prima facie basis, that the reassessment notice seemed to have been issued without acknowledging the taxpayer’s detailed replies provided earlier in reply to a notice u/s 133(6) of the Income Tax Act.

The bench of Justice Om Narayan Rai stated that nothing was there to show that the assessing officer had applied his mind to the responses provided by the applicant in answer to the Section 133(6) notice.

The court said that the non-application of the mind can render the reopening notice unsustainable. It also mentioned that the norms specified in GKN Driveshafts shall apply in matters where the process under section 148A is not needed mandatorily, making the same obligatory for the revenue to dispose of the objections raised by the taxpayer.

A notice has been contested by the writ petition on June 3, 2025, issued u/s 148 by which the revenue asked to reopen the completed assessment. The applicant mentioned that the obligatory precondition for reopening the existence of details recommending escapement of income was not present.

An error has been committed by the assessing officer in issuing the notice without any tangible material and without revealing the details forming the grounds of reopening.

The applicant said that before issuing the impugned notice, the Revenue had asked for the clarifications via a notice on April 3, 2024, u/s 133(6), concerning (i) interest from deposits and (ii) interest reflected in the income tax return. The applicant cited that comprehensive replies supported by pertinent documents were submitted. While beginning the reassessment proceedings, such explanations were allegedly overlooked.

The applicant’s counsel relied on several High Court judgments, including Benaifer Vispi Patel vs. ITO (Bombay High Court), Vishal Garg v. ACIT (Punjab & Haryana High Court), and Arjun Sahu v. ACIT (Allahabad High Court), to claim that non-consideration of responses and objections vitiates reassessment proceedings.

The Supreme Court ruling in GKN Driveshafts (India) Ltd. v. ITO emphasises that objections to reassessment notices must be addressed with a reasoned order before any further action is taken.

Read Also: Delhi HC Sets Aside Reassessment Notice for Breaching Section 148A Norms

After determining that the petitioner had a strong prima facie case, the High Court prohibited the department from proceeding with the contested Section 148 notice until the end of March 2026, or until further orders are issued, whichever is earlier.

The Court granted the Revenue six weeks to submit its affidavit in opposition, with the petitioner allowed to respond afterwards. The case will be scheduled for further consideration after the completion of pleadings.

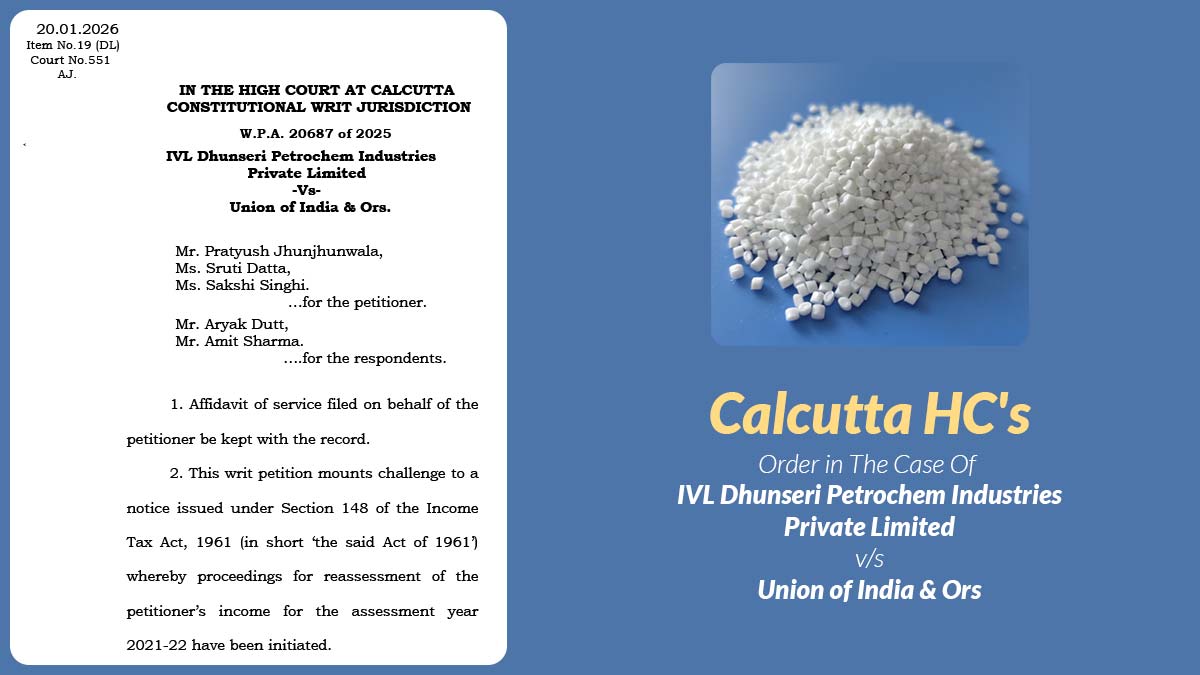

| Case Title | IVL Dhunseri Petrochem Industries Private Limited vs. Union of India & Ors |

| Case No. | W.P.A. 20687 of 2025 |

| For the petitioner | Mr Pratyush Jhunjhunwala, Ms Sruti Datta, Ms Sakshi Singhi |

| For the Respondents | Mr Aryak Dutt, Mr Amit Sharma |

| Calcutta High Court | Read Order |