The Calcutta High Court has overturned a decision that denied a GST refund, stating that the tax department did not follow important rules about how quickly they should respond and provide a chance for taxpayers to voice their opinions.

The bench of Justice Kausik has stated that Rule 92(3) of the CGST Rules, 2017, provides that a taxpayer should be provided 15 days to answer a show-cause notice in refund matters. Concerning the case, the department had allotted only 7 days, thereby breaching the regulatory mandate.

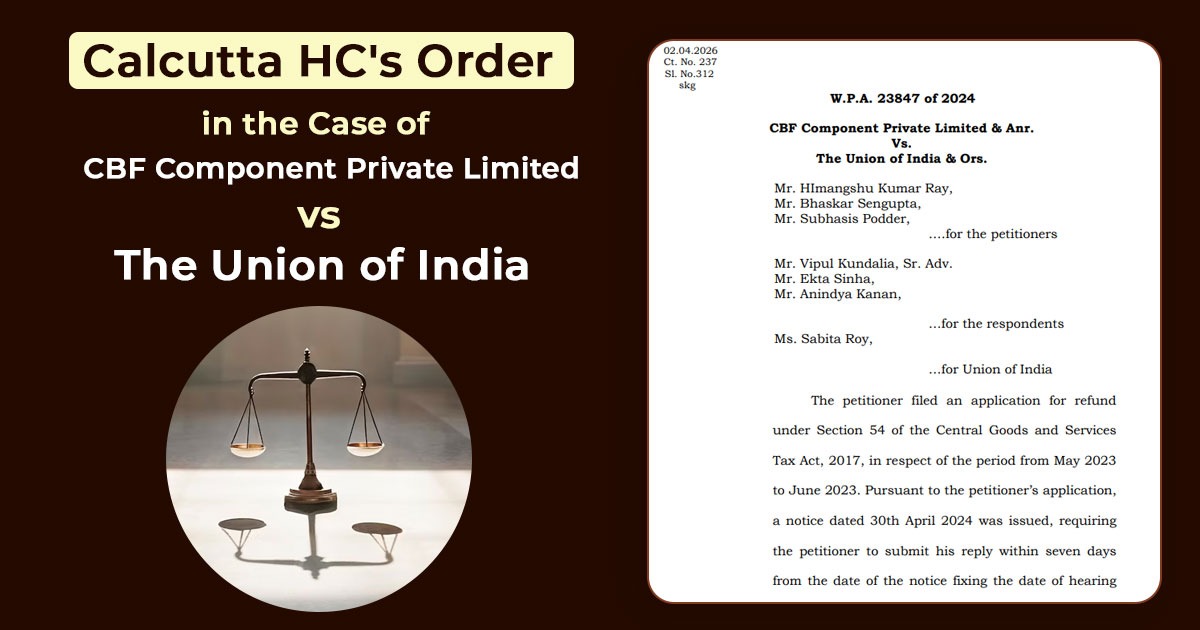

The issue has emerged from a refund application submitted u/s 54 of the CGST Act, 2017, concerning the period May 2023 to June 2023. Following the application, the refund authority issued an SCN on April 30, 2024, asking the applicant to file a response within 7 days and fixing a hearing on May 7, 2024.

On May 5, 2024, the applicant asked for an adjournment, requesting time until May 22, 2024, to file a response.

But the authority had denied the adjournment request allegedly dated May 6, 2024, without communicating this denial to the applicant. Thereafter, a final order was passed on May 17, 2024, by the authority rejecting the refund claim without providing a further chance of hearing.

Read Also: Calcutta HC Quashes GST Order for Ignoring GSTR-3B & GSTR-9 Data

On behalf of the revenue, it was claimed that adjournment could not be claimed as a case of right and that the authority was forced to dispose of the case within the regulatory time duration of 60 days. It was claimed that the applicant knew about the date of the hearing, but did not appear.

But the applicant contested the procedure, claiming that the regulatory structure under the GST law obligates a minimum duration for response and a fair chance of hearing, which were not complied with in this case.

The High Court highlighted that while adjournment is not a matter of right, the decision to reject such a request should be appropriate and clearly communicated. Failing to inform the applicant of the rejection of their adjournment request denied them the chance to appear and defend their case.

Additionally, the Court highlighted that the rejection order was issued without a personal hearing, which is a fundamental aspect of natural justice, especially when it is specifically required by the rules.

The court, under such findings, set aside the refund rejection order on May 17, 2024. It asked the refund authority to permit the applicant to file a response to the Show Cause Notice (SCN) within 15 days from the date of the communication of the order of the court.

Furnish a fresh hearing date, ensuring that the same is communicated at least 72 hours in advance. Within 1 month, conclude the hearing process as per the law.

Therefore, the writ petition was disposed of, with no order as to costs.

| Case Title | CBF Component Private Limited vs. The Union of India |

| Case No. | W.P.A. 23847 of 2024 |

| For Petitioner | Mr. HImangshu Kumar Ray, Mr. Bhaskar Sengupta, and Mr. Subhasis Podder |

| For Respondent | Mr. Vipul Kundalia, Mr. Ekta Sinha, Mr. Anindya Kanan |

| Calcutta High Court | Read Order |