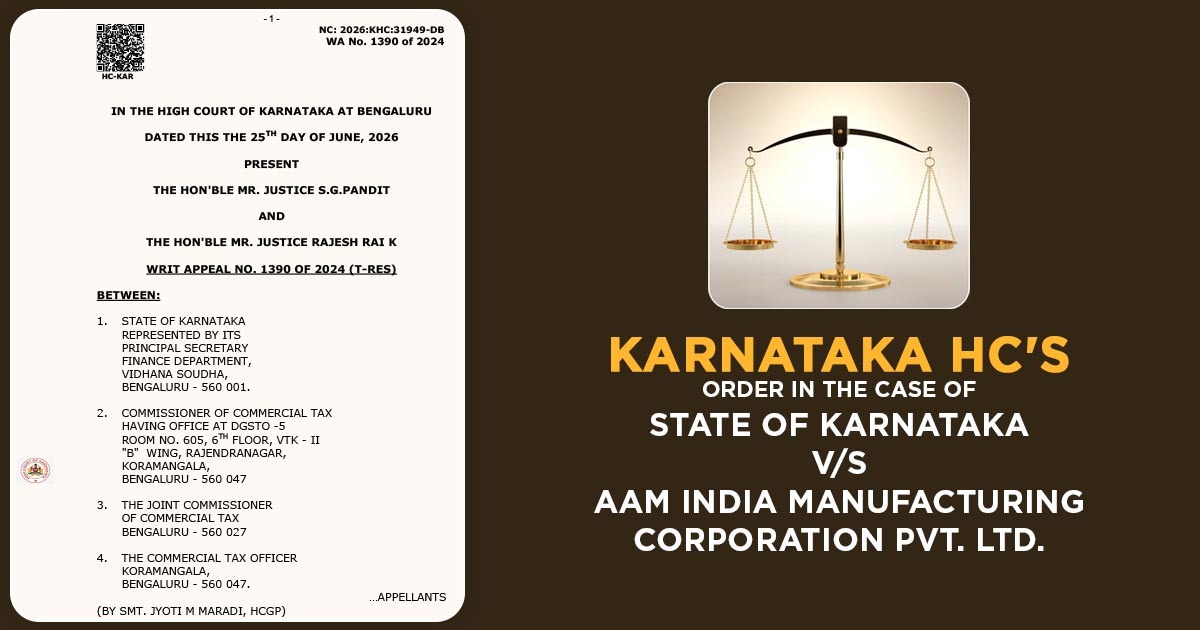

The Karnataka High Court held in its ruling dated June 25 that a company does not incur GST liability when it returns machinery to the seller for testing, provided that no fresh consideration is involved

The Court observed that such movement of goods does not constitute a taxable supply under the GST law and, therefore, does not attract GST.

A Division Bench of Justices S.G. Pandit and Rajesh Rai K quashed the appeal of the State and kept the order of the single judge reducing the penalty levied on AAM India Manufacturing Corporation Pvt. Ltd. to Rs. 25,000, while asking the Department to refund the amount due deposited by the company. It stated:

“The re-transportation would not attract consideration, and the instant transaction does not come within the purview of Section 7(1)(a) of CGST/KGST Act,”

AAM India Manufacturing Corporation Pvt. Ltd. purchased hydraulic fixtures and tooling body machines from Coimbatore in July 2020 and transported them to its manufacturing unit in Maharashtra.

After making certain customisations, the company sent the machines back to the supplier for testing using a delivery challan. However, it did not generate an e-way bill before transporting the machinery.

During transit, GST authorities seized the vehicle, detained the goods, and demanded payment of Integrated Goods and Services Tax (IGST) along with a penalty.

The State claimed that the return movement of the machinery constituted a separate taxable transaction because the company did not generate an e-way bill.

Apart from that, the State claimed that the company could not claim the benefits outlined in Section 129 of the Central Goods and Services Tax/Karnataka Goods and Services Tax Act, which deals with the detention, seizure, and release of goods and conveyances in transit.

The court rejected the state’s claim and said that Section 7(1)(a) of the CGST/KGST Act deems a transaction to be a “supply” only when a person makes it for consideration.

As the company returned the machinery just for testing, and no fresh consideration was involved, it said that the movement did not include a taxable supply. It mentioned that the company is required to comply with the e-way bill requirement under GST rules. The bench mentioned that-

“The CGST/KGST Act and Rules provide for certain exemptions from generating E-way bills in certain cases. However, the same does not cover the subject re-transportation/”

The Judges said that the company breached the GST norms by transporting the machinery without an e-way bill. Although they stated that the breach imposes only the statutory penalty for non-compliance and did not make the company obligated to pay GST on the movement.

Read Also: Karnataka HC Grants Relief on Common GST Notices, GSTR-2A/GSTR-3B ITC

As per that, the HC quashed the appeal of the State and confirmed the refund of the excess amount collected from AAM India Manufacturing Corporation Pvt. Ltd.

| Case Title | Karnataka vs. AAM India Manufacturing Corporation Pvt. Ltd. |

| Case No. | WRIT APPEAL NO. 1390 OF 2024 (T-RES) |

| For Appellants | Jyoti M Maradi |

| For Respondent | Prakash Shah and Mohan Maiya G.L. |

| Karnataka High Court | Read Order |