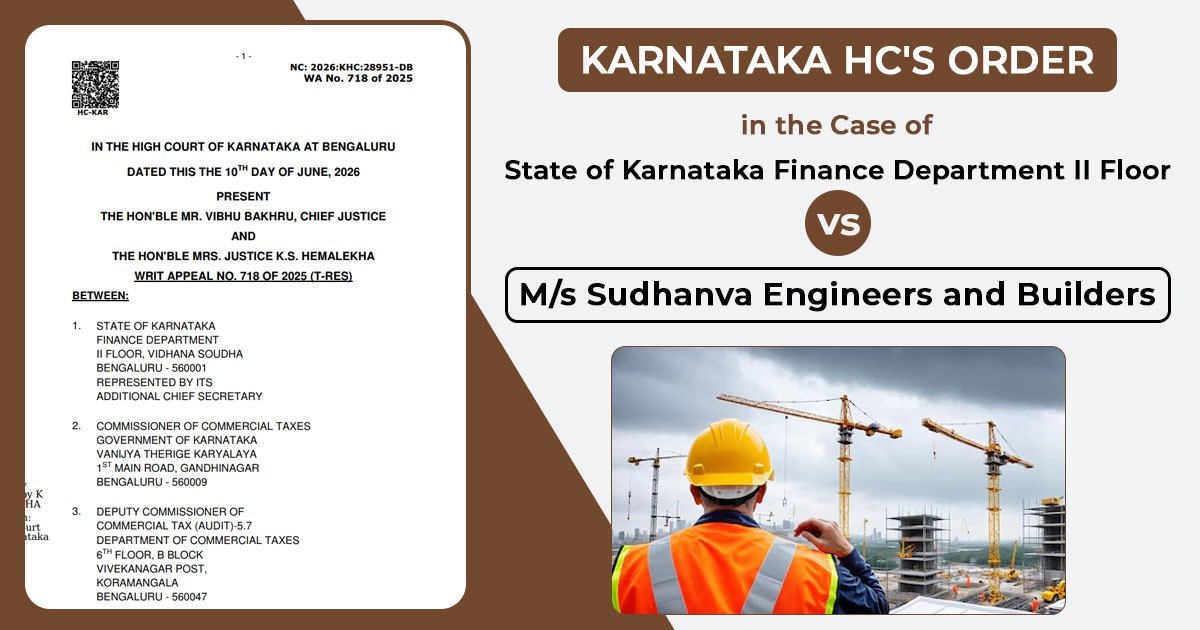

The Karnataka High Court has clarified the distinction between contractual rights and statutory tax obligations. In its ruling, the court overturned a previous decision made by a Single Judge, which had ordered the State Finance Department and tax authorities to pay the Goods and Services Tax (GST) dues, including interest and penalties, owed by a works contractor.

The issue has arisen from a contract given in March 2017 by the Karnataka Urban Water Supply and Drainage Board (the Employer) to a joint venture comprising M/s Sudhanva Engineers and Builders and two other entities for pipeline and pump set works worth more than ₹40 crore.

The original contract, finalised just months before the introduction of the GST regime on July 1, 2017, factored in a 4% VAT. When the GST at 12% (later 18%) became applicable to the balance works, the contractor stated that it had to bear an additional incremental tax burden of approximately ₹3.08 crore.

When the Board does not reimburse this differential tax, the contractor defaults on its GST payments. The commercial tax department afterwards issued a show-cause notice, culminating in a demand order in December 2023 for ₹2.42 Crores, including an 18% interest and a 10% penalty, taking the total cumulative demand to ₹4.84 crore.

To escape this recovery, the contractor filed a writ petition in the High Court. The Single Judge approved the petition, referencing a previous decision by a division bench in the case of Sri Chandrashekaraiah.

The Single Judge instructed the State and the Commercial Tax Department to pay the contractor’s GST dues directly to the tax authorities. Importantly, the order also followed the guidelines established in the Chandrashekaraiah case, which allowed contractors to submit amended returns based on revised tax calculations. This ruling explicitly waived any statutory interest, penalties, and limitation periods under the GST Act.

The State Finance Department and the Commercial Tax Department submitted the present writ appeal before the division bench of Chief Justice Vibhu Bakhru and Justice K.S. Hemalekha.

The division bench said that a contract between a contractor and an employer does not change the regulatory scheme for the charge of GST. The bench said that the obligation to file the GST, its assessment, recovery, and enforcement are cases of strict statutory prescription.

Read Also: Simple Guide to File Every GST Return Online for Taxpayers

The Court made a clear distinction between contractual disputes and statutory compliance. It noted that the question of whether a contractor is entitled to reimbursement of increased tax is purely a contractual matter between the contractor and the Employer.

The High Court overturned the instructions given to the tax authorities and the State. It then clarified that any directives concerning tax reimbursement should be interpreted strictly as applying only to the relevant employer (the Water Supply Board) under the contract, and not as a mandate for the State or GST authorities to settle the contractor’s dues.

| Case Title | The Case of State of Karnataka Finance Department II Floor Vs M/s Sudhanva Engineers and Builders |

| Case No. | WA No. 718 of 2025 |

| For Petitioner | Sri Aditya Vikram Bhat, AGA |

| For Respondent | Sri S.S Naganand, Senior Advocate |

| Karnataka High Court | Read Order |