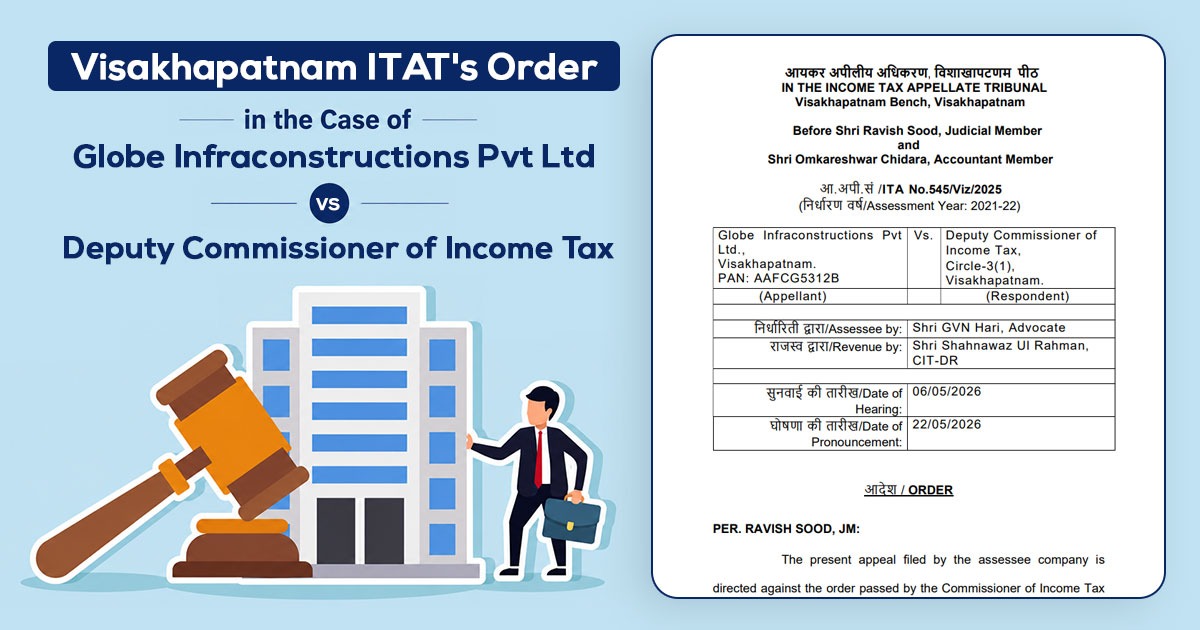

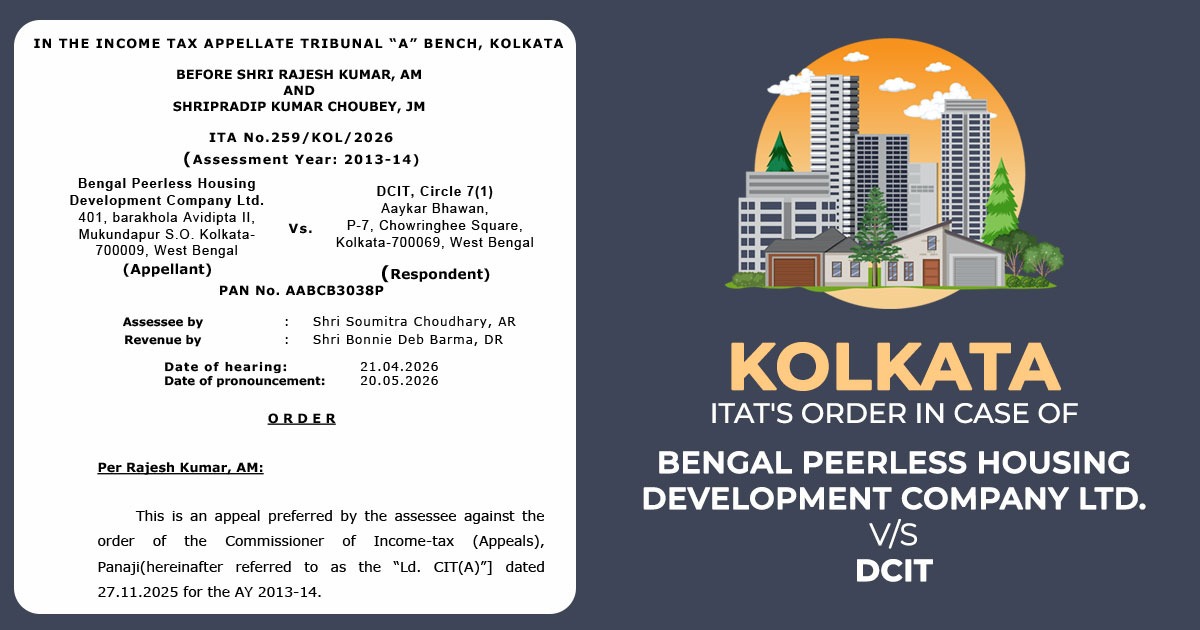

The Income Tax Appellate Tribunal (ITAT), Kolkata Bench, deleted a disallowance of Rs. 7.18 lakh, observing that a difference of opinion regarding the head of expenditure or its nomenclature could not justify the denial of a deduction when the expenses were incurred for the taxpayer’s business.

The taxpayer, Bengal Peerless Housing Development Company Ltd., had claimed legal and professional expenses of Rs. 62.16 lakh. In assessment proceedings, the AO noted that specific expenses of Rs 7.18 lakh did not come within the category of legal expenses. Therefore, the AO disallowed it.

The CIT(A) confirmed the disallowance made by the AO. The dissatisfied taxpayer filed an appeal before the Tribunal.

The taxpayer before the Tribunal claimed that the impugned expenses had been made for its business activities and were permissible as business expenditure. The revenue upheld the orders passed by the lower authorities.

Also Read: Kolkata ITAT Condones More Than 800-Day Delay After Consultant’s Death During COVID-19

The Tribunal, including Rajesh Kumar (Accountant Member) and Pradip Kumar Choubey (Judicial Member), said that the expenses had been made via monthly retainership charges. These retainership arrangements were very common in business where persons were retained every month.

The Tribunal emphasised that differing opinions regarding the head of expenditure or nomenclature should not be a reason to deny deductions, as long as the expenses are related to the assessee’s business and the Assessing Officer (AO) has not questioned their authenticity. In the absence of any findings that challenge the genuineness of the expenses, the disallowance cannot be upheld.

Therefore, the Tribunal set aside the order of the CIT(A) and asked to remove the disallowance of Rs. 7.18 lakh. The appeal of the taxpayer was authorised to that scope.

| Case Title | Bengal Peerless Housing Development Company Ltd. Vs. DCIT |

| Case No: | ITA No.259/KOL/2026 |

| Counsel For Appellant | Shri Soumitra Choudhary |

| Counsel For Respondent | Shri Bonnie Deb Barma |

| Kolkata ITAT | Read Order |