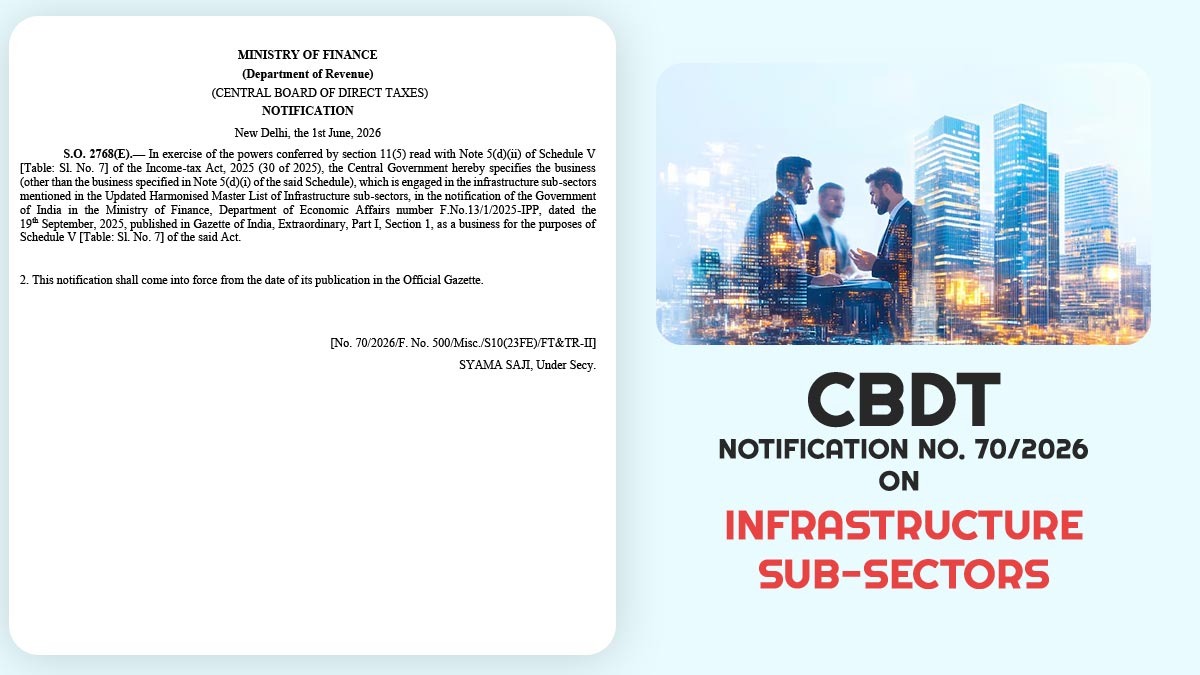

The Central Board of Direct Taxes (CBDT) has issued Notification No. 70/2026, dated June 1, 2026, identifying specific infrastructure-related businesses as eligible under the Income-tax Act, 2025.

The Ministry of Finance, Department of Revenue, issued the notification, in exercise of powers granted u/s 11(5) read with Note 5(d)(ii) of Schedule V [Table: Sl. No. 7] of the Income-tax Act, 2025.

The Central Government has officially recognised businesses in infrastructure sub-sectors listed in the Updated Harmonised Master List of Infrastructure Sub-Sectors issued by the Department of Economic Affairs (DEA) through notification F.No.13/1/2025-IPP dated September 19, 2025.

These infrastructure businesses, apart from those already covered under Note 5(d)(i) of Schedule V, will now be entitled as “specified businesses” for Schedule V [Table: Sl. No. 7] of the Income-tax Act, 2025.

The decision expands the range of eligible infrastructure activities recognised under the new tax framework, aligning tax norms with the government’s agenda for infrastructure development.

Infrastructure Policy Alignment

The notification links tax eligibility directly to the Updated Harmonised Master List of Infrastructure Sub-Sectors kept by the Department of Economic Affairs. The same list encompasses a wide range of infrastructure segments, including transport, energy, water and sanitation, communication, social infrastructure, and other strategic sectors recognised by the Government of India.

With the adoption of this harmonised list, the government’s motive is to confirm consistency across various policy, financing, and taxation frameworks applicable to infrastructure projects.

What Will be the Impact on Infrastructure Businesses?

This notification is anticipated to furnish advantage to businesses functioning in eligible infrastructure sub-sectors by delivering clarity concerning their status under Schedule V of the Income-tax Act, 2025. It may attract investment participation in infrastructure projects by extending the tax treatment available to the mentioned businesses under the Act.

Read Also: How Income Tax Software Companies Should Prepare for Act 2025

Industry stakeholders are pleased with these actions, recognising their role in fostering a more stable regulatory and tax landscape for enduring infrastructure projects.

Applicable Date

The CBDT has stated the notification will be effective upon its official gazette publication on June 1, 2026.

Read CBDT Notification No. 70/2026