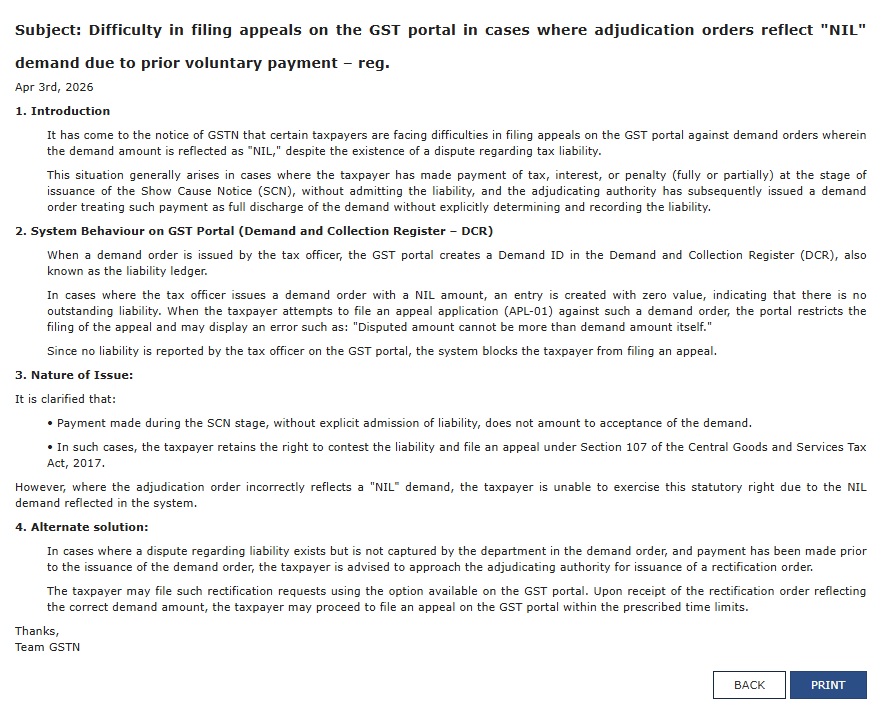

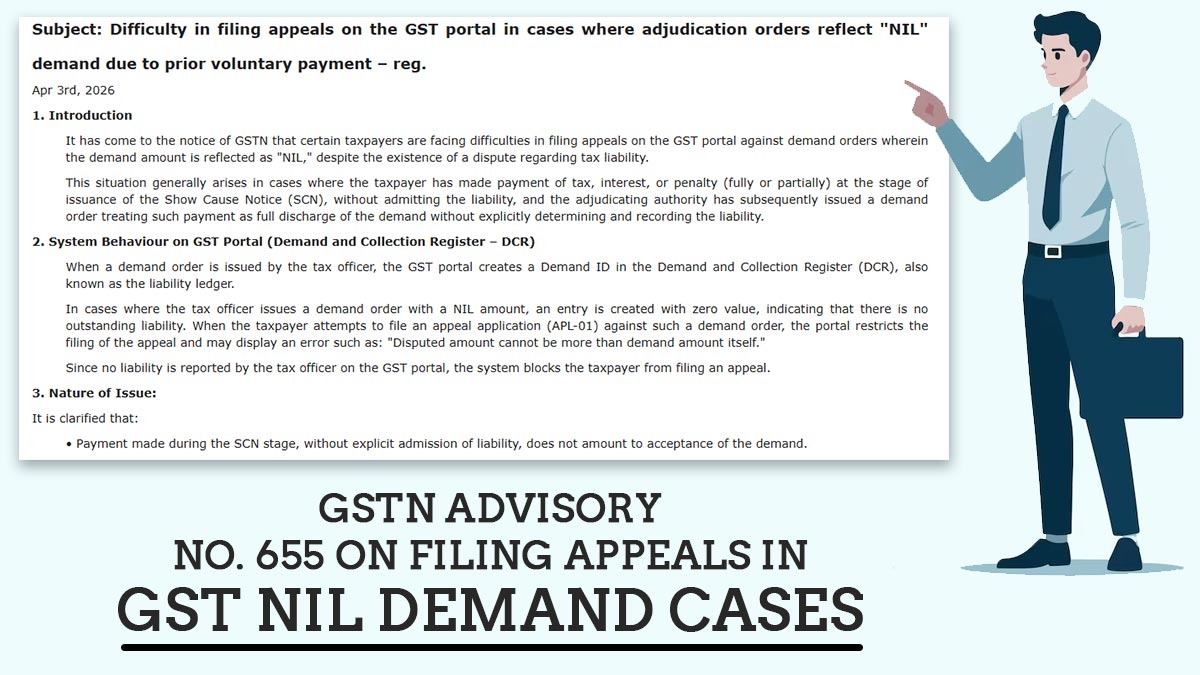

Advisory No. 655 has been released regarding a technical issue encountered by taxpayers while submitting appeals on the GST portal. The same problem occurs in cases where the demand order passed via the tax officer prompts NIL demand, even though there is still a dispute concerning the tax obligation.

The advisory specifies that the same issue normally arises when a taxpayer files payment of tax, interest or penalty at the time of the stage of the Show Cause Notice (SCN). In various cases, these payments are made voluntarily to prevent further litigation or penalty, but this does not imply that the taxpayer is accepting the obligation.

But, subsequently, when the adjudicating authority passes the final order, it is sometimes considered the same payment as a complete release of the demand without determining the actual obligation. Due to this, the order shows a NIL demand.

Because of this NIL demand, the GST portal records zero obligation in the Demand and Collection Register (DCR). When the taxpayer attempts to submit a plea with the help of Form APL-01, the system does not permit it. It may prompt an error message citing that the disputed amount could not exceed the demand amount itself. As the demand is depicted as zero, the system blocks the filing of an appeal.

GSTN has mentioned that a payment incurred at the time of the SCN phase without consideration of the obligation does not signify that the taxpayer has accepted the demand. Still, the taxpayer secures a legal right to contest the obligation and submit a plea u/s 107 of the CGST Act. However, due to the same technical limitation in the portal, the taxpayer could not exercise this right.

To resolve the problem, GSTN has advised another solution. The taxpayers can approach the adjudicating authority and request a rectification order. The same rectification order must specify the actual demand amount rather than showing NIL. Via the available option on the GST portal, the request for rectification can be submitted.

Read Also: GST Software vs GSTN: Main Key Differences Explained

After the completion of the rectification and the correct demand is specified in the system, the taxpayer can submit the appeal within the mentioned time duration. The same advisory is crucial because various taxpayers were encountering confusion and issues because of the same system issue, and were not able to proceed with their appeals.

GSTN Advisory No. 655