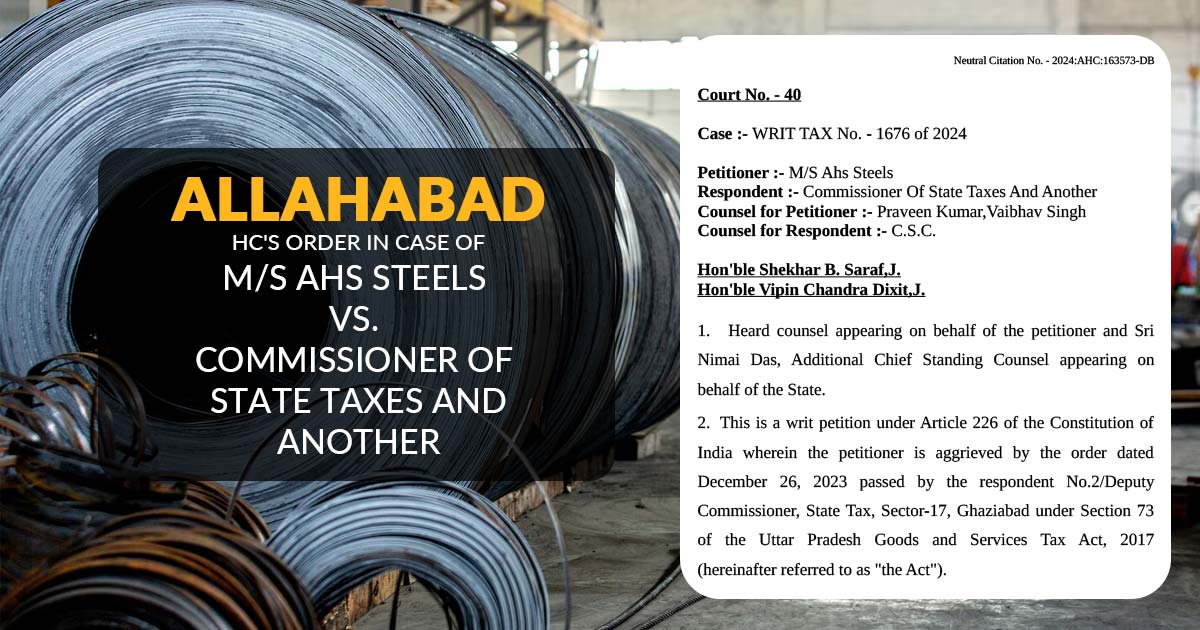

Goods and Services Tax (GST) notices are to be served via alternative means once registration of the taxpayer has been cancelled, and only uploading the notice on the GST portal is insufficient, Allahabad High Court mentioned in a ruling.

In this case, a writ petition was filed through a business, M/s Ahs Steels, whose GST registration had been cancelled dated March 18, 2019, after which no business activities were performed. Subsequently, an order u/s 73 of the Uttar Pradesh GST Act, 2017 was passed without serving the notices, which is certainly a breach of Natural Justice Principles.

The case is concerned with the fact that a show-cause notice concerning alleged tax obligations has been uploaded on the GST portal post the cancellation of the registration of the applicant directing to an order being passed without direct communication to the business owner.

Hearing the contentions of both parties the court mentioned that once the registration of the taxpayer gets cancelled then they are no longer needed to track the GST portal for the notices.

Hence the authorities need to serve the notices through other means like physical delivery or email, to ensure compliance with the principles of natural justice. The counsel of the applicant directed to the earlier ruling of the court in M/s Katyal Industries v. State of U.P., which supported this stance.

The Allahabad High Court, in the matter of Katyal Industries, with an identical case, referred the applicant to consider the GST demand order itself to be the notice.

It was found by Justice Shekhar B. Saraf and Vipin Chandra Dixit that the failure to serve the notice via other means breaches the principles of natural justice, which shall result in the cancellation of the impugned order.

Read Also: GST | Allahabad HC: Tax Cases Can’t Be Relegated to Alternate Remedy if Facts Are Uncontested

The bench referred the tax authorities to furnish a fresh notice and proceed as per the law.

| Case Title | M/S Ahs Steels Vs. Commissioner Of State Taxes And Another |

| Citation | WRIT TAX No. – 1676 of 2024 |

| Date | 15.10.2024 |

| Counsel for Petitioner | Praveen Kumar, Vaibhav Singh |

| Counsel for Respondent | C.S.C. |

| Allahabad High Court | Read Order |